Full News

Rental and Interest Income Included in Section 32AB (of Income Tax Act, 1961) Deduction, Court Rules

Rental and Interest Income Included in Section 32AB (of Income Tax Act, 1961) Deduction, Court Rules

This case involves South India Sugars Ltd. appealing against a decision by the Commissioner of Income Tax (CIT) and the Income Tax Appellate Tribunal (ITAT) regarding the calculation of depreciation and the inclusion of rental and interest income in the computation of deduction under Section 32AB (of Income Tax Act, 1961). The High Court partially allowed the appeal, ruling in favor of the assessee on the inclusion of rental and interest income.

Get the full picture - access the original judgement of the court order here

Case Name:

South India Sugars Ltd. vs Deputy Commissioner of Income Tax (High Court of Madras)

Tax Case (Appeal) No.248 of 2004

Date: 6th November 2007

Key Takeaways:

1. Depreciation cannot exceed the actual cost of assets, even in transitional years.

2. Rental and interest income should be included when computing deduction under Section 32AB (of Income Tax Act, 1961).

3. Profits for Section 32AB (of Income Tax Act, 1961) should be calculated according to the Companies Act, not the Income Tax Act.

Issue:

1. Can depreciation allowance exceed the actual cost of assets in a transitional year?

2. Should rental and interest income be excluded while computing deduction under Section 32AB (of Income Tax Act, 1961)?

Facts:

- The case pertains to the assessment year 1989-90.

- South India Sugars Ltd. is engaged in the manufacture and sale of sugar.

- The assessee claimed depreciation of Rs. 2,49,06,101, including Rs. 98,66,304 on energy-saving equipment.

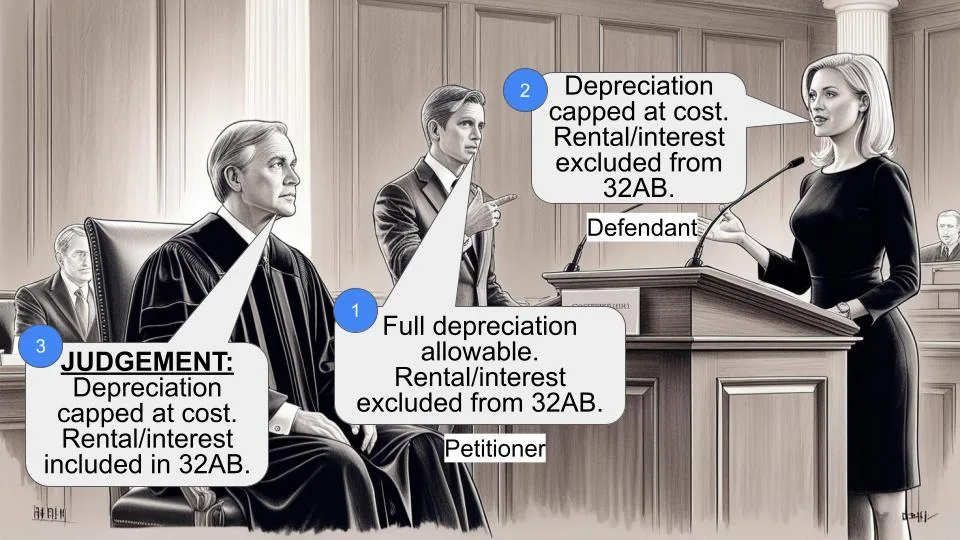

- The assessing officer allowed deduction of rental income (Rs. 3,84,237) and interest income (Rs. 5,49,144) under Section 32AB (of Income Tax Act, 1961).

- The CIT revised the order, directing the assessing officer to restrict depreciation to the actual cost and exclude rental and interest income from Section 32AB (of Income Tax Act, 1961) calculations.

- The ITAT largely confirmed the CIT's order but allowed relief for concessional rent collected from employees.

Arguments:

Assessee:

- Claimed 100% depreciation on energy-saving devices, increased proportionately for the 17-month transitional year.

- Argued that there was no statutory prescription limiting depreciation to actual cost.

Revenue:

- Contended that depreciation cannot exceed the actual cost of assets.

- Argued for the exclusion of rental and interest income from Section 32AB (of Income Tax Act, 1961) calculations.

Key Legal Precedents:

1. CIT vs. Tamil Nadu Mercantile Bank Ltd. (2002) 255 ITR 205 (Mad)

2. Carborandum Universal Ltd. vs. CIT (2004) 265 ITR 372 (Mad)

These cases established that profits for Section 32AB (of Income Tax Act, 1961) should be calculated according to the Companies Act, not the Income Tax Act.

Judgement:

1. The court upheld the restriction of depreciation to the actual cost of assets, agreeing with the CIT and ITAT.

2. The court ruled in favor of the assessee regarding the inclusion of rental and interest income in Section 32AB (of Income Tax Act, 1961) calculations, based on the precedents cited.

FAQs:

1. Q: Why did the court rule against allowing depreciation exceeding the actual cost?

A: The court reasoned that allowing depreciation beyond 100% would result in a negative written down value, which wasn't the legislature's intention.

2. Q: What is the significance of the ruling on rental and interest income?

A: It clarifies that all income, including rental and interest, should be considered when calculating profits for Section 32AB (of Income Tax Act, 1961) deductions, as per the Companies Act.

3. Q: How does this judgment impact the calculation of profits for Section 32AB (of Income Tax Act, 1961)?

A: It reinforces that profits should be calculated according to the Companies Act, without importing concepts from the Income Tax Act.

4. Q: What is the importance of the transitional year in this case?

A: The transitional year (17 months) raised questions about how to calculate depreciation, which the court addressed by limiting it to the actual cost.

5. Q: How does this ruling affect other companies claiming deductions under Section 32AB (of Income Tax Act, 1961)?

A: It provides clarity that all income sources should be included when calculating profits for Section 32AB (of Income Tax Act, 1961) deductions, potentially increasing the deduction amount for some companies.

The relevant assessment year is 1989-90. The appeal is filed formulating the following substantial questions of law:

1. Whether on the facts and in the circumstances of the case, the Tribunal was right in sustaining the action of the respondent herein by invoking the provisions of Section 263 (of Income Tax Act, 1961)?

2. Whether on the facts and in the circumstances of the case, the Tribunal was right in sustaining the action of the respondent in restricting the claim in terms of Section 32AB (of Income Tax Act, 1961) excluding the rental and interest income?

2. The necessary facts as culled out from the statement of facts are as follows:

The appellant was a company engaged in the business of manufacture and sale of sugar. For the relevant assessment year 1989-90, while computing the assessment under Section 143(3) (of Income Tax Act, 1961), the assessing officer allowed depreciation of Rs.2,49,06,101/- which included depreciation claimed by the assessee on energy saving equipment at Rs.98,66,304/-. The assessee had claimed depreciation at 100% on those equipment, the cost of which was Rs.69,64,450/- . The same was claimed as allowable being increased in proportion to the number of months in the transitional previous year. The assessing officer also allowed deduction of the rental income and interest income in a sum of Rs.3,84,237/- and Rs.5,49,144/- respectively under Section 32AB (of Income Tax Act, 1961).

3. The said assessment order was considered by the Commissioner of Income-tax, as erroneous and prejudicial to the interest of the revenue and on that reason initiated action under Section 263 (of Income Tax Act, 1961). After hearing the assessee, the Commissioner of Income-tax by his order dated 24.3.1995 directed the assessing officer to restrict the allowance of depreciation to the actual cost of the assets. He further directed the assessing officer to exclude the rental and interest income while calculating the relief under Section 32AB (of Income Tax Act, 1961).

4. Aggrieved by the revisional order, the assessee carried the matter on appeal to the Income-tax Appellate Tribunal, which by its order dated 13.6.2001 confirmed the issue of depreciation by holding that the commissioner was justified in setting aside the assessment order and directing the assessing officer to allow depreciation limited to the written down value of the asset.

5. As regards the rental income considered as part of business income, the Tribunal has granted the relief for a sum of Rs.3,56,235/- being the concessional rent collected from the employee of the assessee for the premises let out to them but in other respect the revisional order was confirmed. The correctness of the said order is now canvassed before us.

6. In respect of the first question of law, it was contended by the counsel for the assessee that as per depreciation Table Appendix I, the depreciation allowance for energy saving devises was 100% under item Nos.(i) (iii). The devises were installed by the assessee during the previous year ending 31.2.1989. So, for the assessment year 1989-90, the depreciation allowable was 100% of the cost of the assets. As per Rule 5 (of Income Tax Rules, 1962) of the Tenth Schedule, the depreciation allowable was in proportion to the number of months in the previous year. For the assessment year 1989- 90, the transitional previous year extending to a period of 17 months, allowance of depreciation was to increased by multiplying the normal depreciation of 100% with 17 months and reduced to one year by dividing the same by 12. In the absence of any statutory prescription that the allowance of depreciation should not exceed the actual cost, the order of the Commissioner as confirmed by the Tribunal is not correct.

7. Refuting the contention, the learned counsel for the Revenue submitted that the question of law on which the appeal was admitted, is pertaining to invocation of power of the Commissioner under Section 263 (of Income Tax Act, 1961). The assessee cannot be allowed to argue the appeal in deviation to the questions of law. The twin requirements for invoking Section 263 (of Income Tax Act, 1961) are very much present in the case, in the sense, the order of assessment was considered by the Commissioner as erroneous and prejudicial to the interest of the Revenue. Hence, the invocation of Section 263 (of Income Tax Act, 1961) is very much in order. As to the correctness of the revisional order, directing the assessing officer to restrict the depreciation allowance to the W.D.V. of the assets has not been questioned by framing any question of law, which is the requirement for determination of an issue under Section 260A (of Income Tax Act, 1961). He further contended that at no case the depreciation cannot be allowed over and above the actual cost of the asset.

8. We heard the argument of the learned counsel on either side and perused the materials on record.

9. It is true that the the first question of law on which the appeal has been admitted is very general in nature questioning the correctness of the order of the Tribunal in sustaining the action of the Commissioner invoking the provisions of Section 263 (of Income Tax Act, 1961). As rightly contended by the learned counsel for the Revenue, the Commissioner has invoked the revisional power under Section 263 (of Income Tax Act, 1961) on being satisfied that the order of assessment was not only erroneous in nature, but also prejudicial to the interest of the revenue. Further, it could be seen from the revisional order as well as the order of the Tribunal, the correctness of the invocation of Section 263 (of Income Tax Act, 1961) was never been an issue for consideration before the authorities. Hence, the contention on behalf of the revenue is correct in this regard. However, an issue as to the allowability of the depreciation over and above the actual cost of the assets acquired during the relevant period, which is transitional previous year of extended 17 months was made with reference to Rule 5 (of Income Tax Rules, 1962) of the Tenth Schedule of the Income-tax Act, we heard the counsel on either side on merits.

10. Even on merits, we are not able to countenance the argument of the learned counsel for the assessee for the reason given in the order passed by the Tribunal. In respect of transitional previous year it was provided in Rule 5 (of Income Tax Rules, 1962) that there could be enhancement of depreciation allowance in proportion to the number of months in the previous year. The depreciation was an allowance on the written down value of the assets concerned. Section 43(6)(c) (of Income Tax Act, 1961)((ii) of the Act defined the written down value of any block of assets in respect of any previous year relevant to the assessment year commencing on or after the 1st day of April 1989 as written down value of that block of assets in the immediately preceding previous year as reduced by the depreciation actually allowed in respect of that block of assets in relation to the said preceding previous year. For the transitional previous year, if the depreciation is allowed at more than 100% of the actual cost on the basis of the number of months in the previous year, that would give a negative figure for the written down value. That would not have been the intention of the Legislature, if one have regard to the concept of depreciation with reference to Section 32(1)(ii) (of Income Tax Act, 1961), which provided that depreciation would be allowed in the case of block of assets such percentage on the written down value, as prescribed in Rule 5 (of Income Tax Rules, 1962). The Tribunal has also taken note of the Circular No.549 dated 31.10.1998 issued by the C.B.D.T. after the introduction of Tenth Schedule by the Direct Tax Laws (Amendment) Act, 1987 with effect from 1st April, 1989 stating the scope and effect of the Schedule and also referred Paragraph No.2.8 which dealt with the transitory provisions for the assessment year 1989-90. The Board Circular proceeded as follows:

"(iv) Rule 5 (of Income Tax Rules, 1962) provides that where in a transitional previous year the assessee's income under the head "profits and gains of business or profession" is included in the total income for a period of 13 months or more, the depreciation allowance u/s.32(1)(ii) (of Income Tax Act, 1961) shall be increased proportionately. However, ;while allowing enhanced depreciation, care should be taken that the total amount of depreciation allowed during the extended transitional previous year,including the depreciation allowed in earlier years, does not exceed the actual cost of the asset. Similar care will also have to be taken where 100% depreciation is allowable on certain block of assets under the rate schedule for depreciation provided in Appendix-I to the IT Rules, 1962 or where 100% depreciation is available on machinery or plant costing upto Rs.5000 under the provisions of the first proviso to Sec.32(1)(i) (of Income Tax Act, 1961)."

11. Thus, it could be clear that even for the transitional previous year, the intention was not to allow depreciation in excess of the original cost of the assets.

The Tribunal has also rejected the contention of the assessee that after the deletion of Section 34(2) (of Income Tax Act, 1961) with effect from 1.4.1988, there was no restriction on the allowance of depreciation by taking note of Rule 5(1A) (of Income Tax Rules, 1962), 1997 introduced by way of an amendment by the Income-tax (Twelfth Amendment) Rules, 1997 and the proviso thereto. As per the sub-rule, the allowance under clause (i) of sub-section (1) of Section 32 (of Income Tax Act, 1961) in respect of depreciation of assets acquired on or after 1st day of April, 1997 shall be calculated at the percentage specified in the second column of the Table in Appendix 1A of these rules on the actual cost thereof to the assessee as are used for the purposes of the business of the assessee at any time during the previous year. It also provided that the aggregate depreciation allowed in respect of any asset for different assessment years shall not exceed the actual cost of the said assets. The proviso to sub-rule 1A (of Income Tax Rules, 1962) clearly restricted that the aggregate of the depreciation allowed in respect of any asset should not exceed the actual cost of that asset.

12. Thus, even on merits, the assessee has not made out any case in this appeal for taking a different view than the one taken by the Tribunal. Hence, the first question of law is decided in affirmative against the assessee.

13. In respect of the second question of law, learned counsel on either side submitted and agreed that the issue is covered in favour of the assessee by the decision of this Court in the case of COMMISSIONER OF INCOME-TAX VS. TAMIL NADU MERCANTILE BANK LIMITED reported in (2002) 255 ITR 205 and CARBORANDUM UNIVERSAL LIMITED VS. COMMISSIONER OF INCOME- TAX reported in (2004) 265 ITR 372, wherein this Court has held that the calculations required to be made for the purpose of section 32AB (of Income Tax Act, 1961), are to commence with the figure representing the profits of the eligible business as computed in accordance with the requirements of Parts II and III of Schedule VI to the Companies Act, 1956. From that figure the amount equal to the depreciation computed in accordance with section 32(1) (of Income Tax Act, 1961), is to be deducted. After such deduction, that amount is to be increased by the aggregate of the amounts set out in clauses (i) to (vii) of section 32(3) (of Income Tax Act, 1961). A sum equal to 20 per cent. of that amount was to be allowed as a deduction under section 32AB(1)(ii) (of Income Tax Act, 1961). The determination of the profit required to be made in accordance with Parts II and III of Schedule VI to the Companies Act was required to be made after taking into account all the activities of the assessee governed by the Companies Act, as the profit and loss account required to be drawn up by a company must necessarily reflect all the income and all the expenditure incurred by the company in that year. Section 32AB (of Income Tax Act, 1961) does not require the profit for the purpose of section 32AB(1) (of Income Tax Act, 1961) to be calculated in accordance with the provisions of the Income-tax Act. All that it provides was that the calculations should first be made in accordance with the Companies Act and the requirements more specifically required of Parts II and III of Schedule VI to the Companies Act. There was, therefore, no scope at all for importing the concept of different heads of income found in the Income-tax Act, into the calculation of profit required to be made.

14. Thus, the issue the deletion of the interest amount and certain part of the rental received by the assessee is only held to be incorrect. Thus, the second question of law framed above is answered in favour of the assessee and against the revenue.

15. For the fore-going reasons, the appeal is partly allowed as indicated above.

×

Similar Ripples

Questions

Rental and Interest Income Included in Section 32AB (of Income Tax Act, 1961) Deduction, Court Rules

Write your CommentSimilar Posts

Generic

- Reportdata/5198.pdf