Rental Income from Long-Term Lease Taxed as 'Income from House Property', Not B…

Full News

Rental Income from Long-Term Lease Taxed as 'Income from House Property', Not Business Income

Rental Income from Long-Term Lease Taxed as 'Income from House Property', Not Business Income

This case involves Batra Palace P. Ltd. (the appellant-assessee) appealing against an Income Tax Appellate Tribunal decision. The dispute centered on whether income from leasing out a commercial property should be classified as 'income from house property' or 'business income' for tax purposes. The court upheld the Tribunal's decision, ruling that the income should be treated as 'income from house property'.

Get the full picture - access the original judgement of the court order here

Case Name:

Batra Palace P. Ltd. Vs Commissioner of Income Tax (High Court of Punjab & Haryana)

ITA No.56 of 2010

Date: 31st March 2016

Key Takeaways:

1. The intention of the assessee at the time of letting out the property is crucial in determining the nature of income.

2. Long-term lease agreements (12 years in this case) typically indicate an intention to earn rental income rather than temporary commercial exploitation.

3. The court distinguished this case from previous judgments where property was leased temporarily for commercial purposes.

Issue:

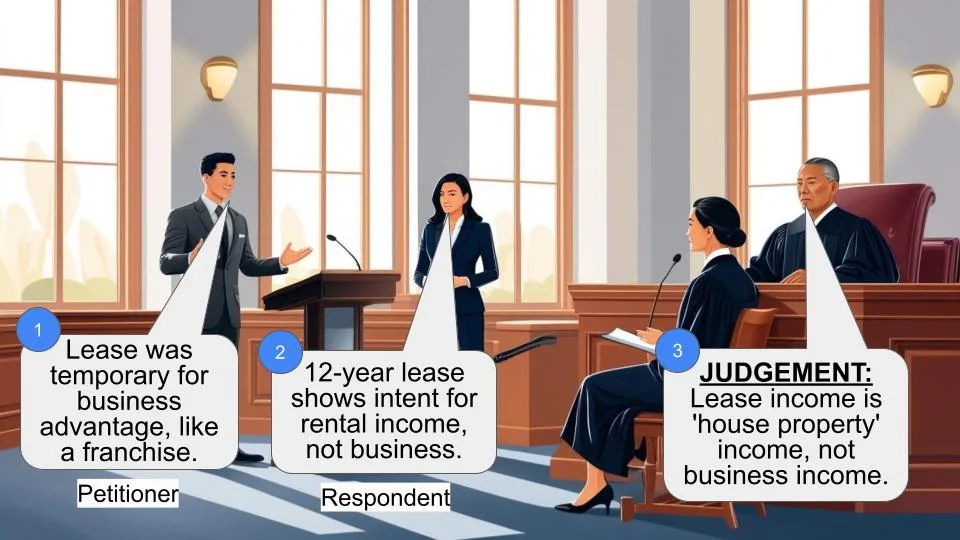

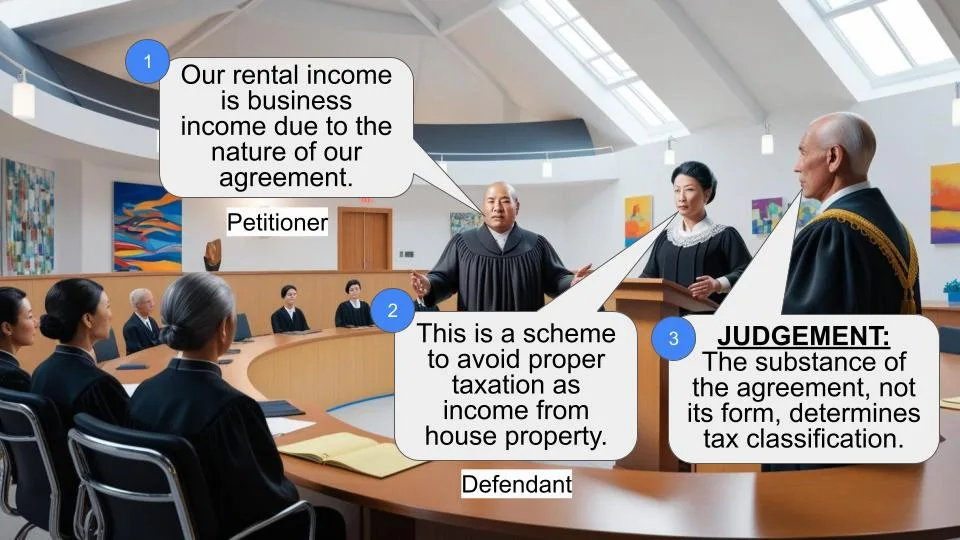

Whether the Income Tax Appellate Tribunal was justified in treating the lease income from a commercial property as 'income from house property' rather than 'business income' when the appellant had to provide various basic facilities similar to those provided to a franchisee?

Facts:

1. Batra Palace P. Ltd. is a company engaged in running a hotel and earning income from house property.

2. For the assessment year 2005-06, the company leased out a portion of its property to Pizza Hut for 12 years, renewable for another 12 years.

3. The assessee claimed this was done temporarily to tide over financial difficulties and gain a business edge.

4. The Assessing Officer classified the income as 'income from house property'.

5. The CIT(Appeals) overturned this decision, classifying it as business income.

6. The Income Tax Appellate Tribunal reversed the CIT(Appeals) decision, agreeing with the Assessing Officer's classification.

Arguments:

Appellant (Batra Palace P. Ltd.):

- The lease was temporary and meant to exploit a business opportunity.

- The arrangement with Pizza Hut was beneficial for their hotel business.

- They provided various facilities like AC, power backup, and specific brand requirements.

Revenue:

- The long-term nature of the lease (12 years, renewable for 12 more) indicated an intention to earn rental income.

- The intention at the time of letting out is crucial, not subsequent events like early termination.

Key Legal Precedents:

1. CIT vs. Anand Rubber and Plastics (P) Limited, (1989) 178 ITR 301: The court distinguished this case, noting that here the property was leased temporarily as a commercial asset, unlike the present case.

2. Sultan Brothers Private Limited vs. Commissioner of Income Tax, Bombay City II, AIR 1964 SC 1389: This case dealt with separating rent from building and income from furniture/fixtures for tax purposes.

Judgement:

The court dismissed the appeal, agreeing with the Tribunal's decision. Key points:

1. The 12-year lease agreement indicated an intention to earn rental income, not temporary commercial exploitation.

2. The intention at the time of letting out is crucial, not subsequent events like early termination.

3. The income was correctly classified as 'income from house property' by the Assessing Officer.

FAQs:

1. Q: What's the main factor in determining whether rental income is 'income from house property' or 'business income'?

A: The main factor is the intention of the assessee at the time of letting out the property.

2. Q: Does the duration of the lease matter?

A: Yes, a long-term lease (like 12 years in this case) typically indicates an intention to earn rental income rather than temporary commercial exploitation.

3. Q: Can providing additional facilities change the nature of the income?

A: Not necessarily. In this case, despite providing various facilities, the income was still classified as 'income from house property' due to the long-term nature of the lease.

4. Q: What if the tenant leaves early?

A: The court emphasized that the intention at the time of letting out is crucial, not subsequent events like early termination of the lease.

5. Q: How does this ruling affect similar cases?

A: While each case is decided on its own facts, this ruling emphasizes the importance of the initial intention and the terms of the lease agreement in determining the nature of rental income for tax purposes.

1. This appeal has been preferred by the appellant-assessee under Section 260A (of Income Tax Act, 1961) (in short, “the Act”) against the order dated 15.5.2009, Annexure A.1 passed by the Income Tax Appellate Tribunal, Chandigarh Bench 'A', Chandigarh (in short, “the Tribunal”) in ITA No.133/CHANDI/2009, for the assessment year 2005-06. It was admitted by this Court vide order dated November 23, 2010 to consider the following substantial question of law:-

“ Whether the ITAT was justified in reversing the order of CIT(A) and upholding the order of Assessing Officer, while treating the lease income out of leasing out commercial property to concern engaged in parallel business activities as income from House property and not income from business when the appellant has to provide various basic facilities as that to franchisee?”

2. A few facts relevant for the decision of the controversy involved as narrated in the appeal may be noticed. The appellant-assessee is a company engaged in the business of running a hotel and also earning income from house property. It filed its return of income for the assessment year 2005-06 on 30.10.2005 declaring nil income. The return was selected for scrutiny and notice under Section 143(2) (of Income Tax Act, 1961) was issued to the assessee on 30.10.2006. The assessee appeared before the Assessing Officer and filed reply. The appellant submitted that it was earning income by way of rent but was providing various facilities like 60 ton AC, 100% power backup, false ceiling, front elevation with glazing and flooring, sanitary facilities as per brand requirements etc. The lease was for a total period of 12 years but subject to the condition as per clause (3) of Memorandum of Understanding (MOU) that the lease rent will be subject to increase of 15% after completion of every three years. The tenant 'Pizza hut' was in the business of running Pizza Hut which had the potential of advertising the business of the assessee and introducing new customers and therefore, was beneficial for the business of the assessee and for this reason only, the assessee had offered the space to it on lease as it was not having a restaurant in its hotel which was required for running the hotel business efficiently and profitably. The tenant left the premises in a short period. The assessee submitted before the Assessing Officer that the collaboration with Pizza Hut as lease agreement was to tide over the financial crunch period, to gain edge in business and to exploit the business opportunity in the best possible way. After examining the matter, the Assessing Officer held the income from lease of commercial property declared as business income as income from house property vide order dated 28.12.2007, Annexure A.3. Aggrieved by the order, the assessee filed appeal before the Commissioner of Income Tax (Appeals) [CIT(A)]. Vide order dated 18.11.2008, Annexure A.2, the CIT(A) partly allowed the appeal and decided the issue in favour of the assessee. Not satisfied with the order, the revenue filed appeal before the Tribunal. Vide order dated 15.5.2009, Annexure A.1, the Tribunal partly allowed the appeal and decided the issue in favour of the revenue and against the assessee while distinguishing the judgment of this court in CIT vs. Anand Rubber and Plastics (P) Limited, (1989) 178 ITR 301. Hence the instant appeal by the appellant-assessee.

3. Learned counsel for the appellant-assessee submitted that the Tribunal erred in reversing the order passed by the CIT(A) and upholding the order passed by the Assessing Officer. Primary reliance was placed on judgment of this Court in Anand Rubber and Plastics (P) Limited's case (supra). On the other hand, learned counsel for the respondent-revenue supported the impugned order.

4. We have heard learned counsel for the parties.

5. Admittedly, the assessee was owning a building in which it was running a hotel and restaurant business. A portion of the said property was leased out to another concern for running a restaurant by the name of 'Pizza Hut'. The assessee claimed that this was done for a temporary period as the premises were vacated after two years and therefore the same had to be viewed as commercial exploitation of the asset. The Assessing Officer treated the income received from M/s Pizza Hut as income from house property instead of income from business. The CIT(A) treated the income earned by the assessee as business income. It has been categorically recorded by the Tribunal on appeal by the revenue that perusal of the memorandum of Understanding dated 27.8.2002 between the assessee and the lessee i.e. M/s Pizza Hut showed that the property in question was given for use for a period of 12 years which was renewable for a further period of 12 years. It was nowhere shown that the intention to let out was only for a temporary period. Thus, the CIT(A) was not held to be justified in concluding that the letting out was to be taken as commercial exploitation of the property. The intention of the assessee was to enjoy rental income from the letting out of the property which was rightly treated as income from house property by the Assessing officer. The relevant findings recorded by the Tribunal while reversing the order of the CIT(A) on this issue read thus:-

“17. We have considered the rival submissions carefully. The short controversy before us resolves around the accessibility of rental income derived by the assessee. The question is whether the rent is assessable as income from property or business income. It is a settled proposition that in order to address such controversy, what has to be seen is whether the asset in question is being exploited commercially by way of renting out or whether it is being rented out for the purpose of enjoying the rental income. The Hon'ble Punjab and Haryana High Court in the case of M/s Anand Rubber & Plastics Pvt. Limited, 178 ITR 301 has further observed that the distinction between the two approaches is a narrow one and has to depend on certain facts peculiar to each case. In the case of M/s Anand Rubber and Plastics Pvt. Limited (supra), the Hon'ble High Court found it as fact that property was leased out temporarily as a commercial asset and therefore, it was held that the rental income was assessable as business income. The CIT(Appeals) has also relied upon the aforesaid judgment to decide the controversy in favour of the assessee. In this regard, we have carefully examined the facts of the present case. In the present case, the facts are that the assessee is owning a building in which it is running a hotel and restaurant business. A portion of the said property was leased out to another concern for running a restaurant by the name of Piza Hut. The claim of the assessee is that such renting was done for a temporary period as the premises were vacated after two years and therefore, such letting out of the asset has to be viewed as commercial exploitation of the assets. In this regard, we have attempted to cull out the intention of the assessee while letting out the property in question. The assessee has placed on record a copy of MOU dated 27.8.2002 with the lessee. It is evident from perusal of the same that the property in question was given over for use for a period of 12 years which was renewable for a further period of 12 years as mutually agreed upon by both the parties. From such an arrangement, it does not show that the intention to let out was only for a temporary period. No doubt, the property has been put to use by the lessee also for running a restaurant business as done by the assessee, so however, the lease cannot be termed to be for a short period or temporary. We are conscious that the property has been vacated within a period of 2 to 3 years as canvassed by the assessee. However, what is of relevance is to cull out the intention of the assessee at the time of letting out of the property which clearly does not show that the letting out was for a temporary period. Thus, in our view, having regard to the facts and circumstances of the case, the CIT(Appeals) was not justified in inferring that the letting out in this case was to be taken as commercial exploitation of the property. The intention was clearly to enjoy rental income from the letting out of the property which in our considered opinion, was rightly brought to tax under the head 'income from house property' in the assessment order. The judgment of the Hon'ble Punjab and Haryana High Court in the case of Anand Rubber & Plastics (P) Limited (supra) was clearly inapplicable because of different facts. In view of the aforesaid discussion, we therefore, set aside the order of the CIT(Appeals) on this issue and restore that of the Assessing Officer.”

6. Adverting to the judgments relied upon by the learned counsel for the appellant-assessee, it may be noticed that in Anand Rubber and Plastics (P) Limited's case (supra), the factory premises of the assessee consisted of three portions – the main building, a front shed and a rear shed. In order to curtail the losses, production was reduced with the result that the rear shed became surplus. The said portion was leased out with a view to reduce the losses. After examining the matter, it was recorded by this court that in order to determine whether rent is assessable as income from property or business income, what has to be seen is whether the asset is being exploited commercially by the letting out or whether it is being let out for the purpose of enjoying the rent. It was held that the portion of the property was leased out temporarily as a commercial asset. Thus, the rent received was assessable as business income. Such is not the position in the present case. Herein the property was leased out for a period of 12 years as per memorandum of understanding dated 27.8.2002 between the assessee and the lessee. Thus, this judgment was rightly distinguished by the Tribunal while reversing the order passed by the CIT(A). In Sultan Brothers Private Limited vs. Commissioner of Income Tax, Bombay City II, AIR 1964 SC 1389, the Apex Court held that the rent from the building should be computed separately from the income from the furniture and fixtures and in the case of rent from the building, the assessee would be entitled to the allowances mentioned in sub section 4 (of Income Tax Act, 1961) of section 12 (of Income Tax Act, 1961), 1922 (in short, “the 1922 Act”) and in the case of income from the furniture and fixtures, to those mentioned in sub section 3 (of Income Tax Act, 1961), and that no part of the income could be assessed under section 9 (of Income Tax Act, 1961) or 10 (of Income Tax Act, 1961) the 1922 Act. The other judgments relied upon by the learned counsel for the appellant-assessee in CIT vs. Superfine Cables P. Limited, (1985) 154 ITR 532 (Del.), Commissioner of Excess Profits Tax, Bombay City vs. Shri Lakshmi Silk Mills Limited, (1951) 20 ITR 451, CIT vs. VST Motors Pvt. Limited, (1997) 226 ITR 155 (Mad.), CIT vs. Pateshwari Electrical and Associated Industries P. Limited, (2006) 282 ITR 61 (All.), CIT, A.P.1 vs. Aryan Industries (P) Limited, (1982) 138 ITR 718 (AP), CIT vs. Vikram Cotton Mills Limited (1988) 169 ITR 597 (SC) and ACIT vs. Rajindra Flour and Allied Industries P. Limited, (1981) 128 ITR 402 (Del.) are also based on individual fact situation involved therein. It was held therein that each case has to be decided on its own facts. Thus, the appellant cannot derive any advantage from the said decisions.

7. In the present case, the view adopted by the Tribunal is a plausible view based on appreciation of material on record and the relevant case law on the point. Learned counsel for the appellant-assessee has not been able to show any illegality or perversity in the impugned order. Thus,the substantial question of law is answered against the assessee and in favour of the revenue. Consequently, the appeal stands dismissed.

(Ajay Kumar Mittal)

Judge

March 31, 2016 (Raj Rahul Garg)

‘gs’ Judge

×

Similar Ripples

Questions

Rental Income from Long-Term Lease Taxed as 'Income from House Property', Not Business Income

Write your CommentSimilar Posts

Generic

- Reportdata/2947.pdf