Reopening Tax Assessments: Court Sides with Assessee Over Revenue

Full News

Reopening Tax Assessments: Court Sides with Assessee Over Revenue

Reopening Tax Assessments: Court Sides with Assessee Over Revenue

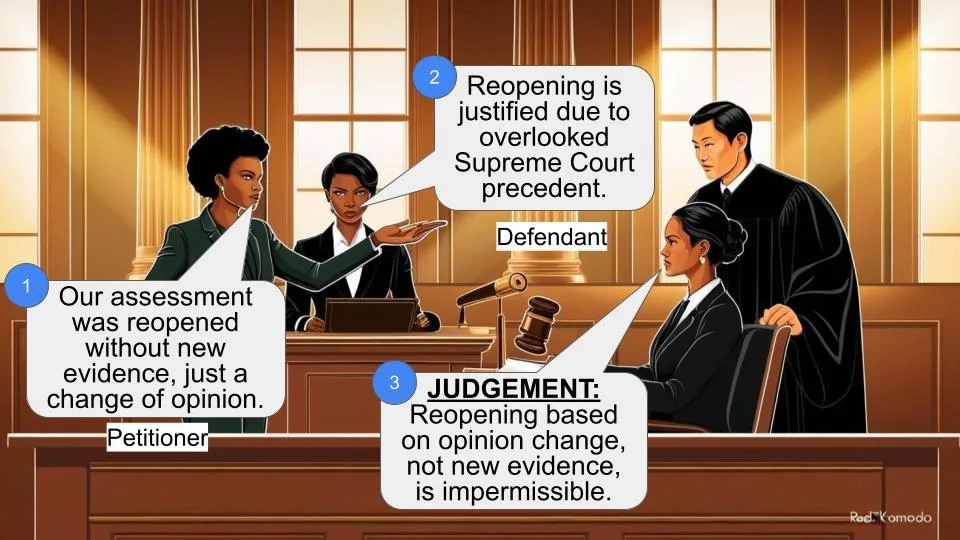

In the case of Coperion Ideal Private Limited vs. Commissioner of Income Tax, the court examined whether the reopening of a tax assessment beyond four years was justified. The court ruled in favor of the assessee, stating that the reopening was not based on new tangible material but rather on a change of opinion, which is impermissible.

Get the full picture - access the original judgement of the court order here

Case Name:

Coperion Ideal Private Limited vs. Commissioner of Income Tax (High Court of Delhi)

ITA 557/2015

Date: 9th October 2015

Key Takeaways:

- The court emphasized that reopening an assessment after four years requires tangible material indicating income escapement due to the assessee’s failure to disclose material facts.

- A mere change of opinion by the Assessing Officer (AO) is not sufficient grounds for reopening an assessment.

- The decision reinforces the need for a schematic interpretation of “reason to believe” under Section 147 (of Income Tax Act, 1961).

Issue:

Was the reopening of the tax assessment for Coperion Ideal Private Limited justified under Section 147 (of Income Tax Act, 1961), given that it occurred more than four years after the original assessment?

Facts:

- Coperion Ideal Private Limited filed its income tax return for the Assessment Year 2002-03, which was initially assessed in 2005.

- The AO later sought to reopen the assessment in 2009, citing a Supreme Court decision from 1997 that was not considered during the original assessment.

- The AO argued that the royalty payments should have been treated as capital expenditure, not revenue expenditure.

Arguments:

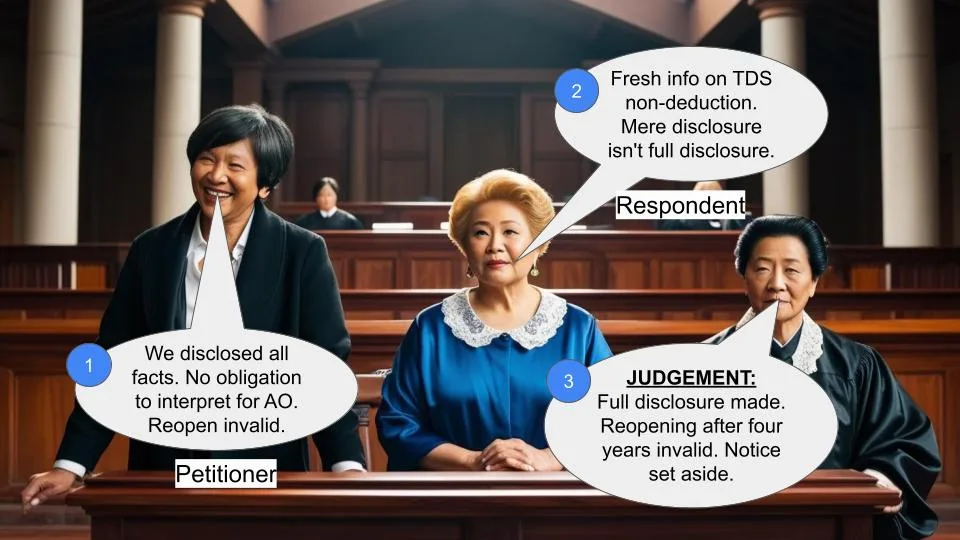

- Assessee’s Argument: The reopening was based on a change of opinion, not on new tangible material. The royalty payments had been consistently treated as revenue expenditure in previous years.

- Revenue’s Argument: The AO had overlooked a binding Supreme Court precedent, which justified the reopening of the assessment.

Key Legal Precedents:

- CIT v. Kelvinator of India Ltd.: The Supreme Court held that reopening an assessment requires tangible material and cannot be based on a mere change of opinion.

- ALA Firm v. CIT: Cited by the Revenue, but the court found it inapplicable as it dealt with a different context and legal framework.

Judgement:

The court ruled in favor of Coperion Ideal Private Limited, setting aside the ITAT’s order. It concluded that the reopening of the assessment was not justified as it was based on a change of opinion rather than new tangible material. The court emphasized the need for certainty in concluding that there was a failure to disclose material facts.

FAQs:

Q1. Why was the reopening of the assessment deemed unjustified?

A1. The court found that the reopening was based on a change of opinion rather than new tangible material, which is not permissible under the law.

Q2. What does this decision mean for other taxpayers?

A2. It reinforces the principle that tax assessments cannot be reopened after four years without new tangible evidence of income escapement due to non-disclosure of material facts.

Q3. How does this case impact the interpretation of Section 147 (of Income Tax Act, 1961)?

A3. It underscores the importance of having tangible material and not merely a change of opinion to justify reopening an assessment under Section 147 (of Income Tax Act, 1961).

1. This appeal by the Assessee under Section 260A (of Income Tax Act, 1961),

1961 („Act‟) is directed against an order dated 26th September 2014 passed by the Income Tax Appellate Tribunal („ITAT‟) in ITA No. 4375/D/2010 for the Assessment year („AY‟) 2002-03.

2. Admit.

3. Having heard learned counsel for the parties, the following question of law is framed:

“Whether the ITAT erred in law in upholding the reopening of

the assessment by the Assessing Officer under Section 147 (of Income Tax Act, 1961) of

the Income Tax Act, 1961 in the facts of the case?”

4. The Assessee filed its return of income for the Assessment Year („AY‟)2002-03 on 31st October 2002 declaring income at Rs.67,91,500. The

Assessee‟s case was selected for scrutiny under Section 143(1) (of Income Tax Act, 1961) on 24th June 2003. An order was passed on 31st January 2005 under Section 143(3) (of Income Tax Act, 1961), assessing the income at Rs.71,46,170. One of the items of expenditure was a sum of Rs.20,71,489 under the head “Royalty & Cess”.

5. On 5th September 2005, the Assistant Commissioner of Income Tax

(„ACIT‟) issued a notice under Section 154 (of Income Tax Act, 1961) to the Assessee

seeking explanation on the ground that there was mistake apparent from the record since the aforesaid amount should have been treated as capital expenditure as the benefit was of enduring nature. The Assessee replied to this notice on 21st September 2005 clarifying that (a) it was paying royalty at 5% on its domestic sales to M/s Coperion Waeschle Co. Germany on year to year basis; (b) that the payment did not pertain to acquisition of technical knowhow and therefore was booked as revenue expenditure and debited to the profit and loss (P&L) account. The Assessee also pointed out that it had been paying royalty for the previous 5-6 years based on the turnover and in all those years it has been allowed as a revenue expenditure.

6. It appears that an audit objection was raised, in response to which the ACIT wrote to the Senior Audit Officer on 28th October 2005, clarifying that the expenditure was rightly treated as revenue expenditure.

7. On 24th March 2009, more than four years after the assessment was

completed, the ACIT penned the reasons for reopening of assessment as

under:

“The return of income in this case was filed on 31.10.2002 at an

income of Rs. 6791500 and processed u/s 143(1) (of Income Tax Act, 1961)

on 24.06.2003. Subsequently, the case was selected for scrutiny

and order u/s 143(3) (of Income Tax Act, 1961) was passed on 31.01.2005 at

assessed income of Rs. 7146170.

Section 37 (of Income Tax Act, 1961), provides that any expenditure

not being expenditure of capital nature laid out wholly or

exclusively for the purpose of business is allowable as deduction

in computation of the income chargeable under the head 'profit

and gain of business and profession'. The Hon'ble Supreme

Court had held (232 ITR 359 - Southern Switchgears Ltd. vs.

CIT dated 11.12.1997) that grant of technical aid fees for setting

up factory and right to sell the products as per collaboration

agreement is not allowable as revenue expenditure and was to be

treated as capital expenditure.

The perusal of asstt. records for the AY 02-03 reveals that the

assessee has debited an amount of Rs 2071489/- under the head

'royalty and cess' (Royalty Rs 1973337/-) that was of enduring

nature and hence was a capital expenditure and not allowable.

As per the decision of the Hon'ble Supreme Court in the

aforesaid case, the said expenditure is not allowable.

In view of above facts of the case, I have reasons to believe that

the income to the tune of Rs 1973337/- has escaped assessment

because of failure on part of assessee to disclose fully and truly

material facts necessary for asstt. and hence notice u/s 148 (of Income Tax Act, 1961) is

hereby issued for reopening u/s 147 (of Income Tax Act, 1961).”

8. On that basis, notice was issued to the Assessee on 30th March 2009 under Section 148 (of Income Tax Act, 1961) seeking to reopen the assessment for AY 2002-03.

The Assessee‟s objections to the reopening were negatived and a fresh order of assessment was passed on 30th November 2009 by the Assessing Officer(„AO‟). The amount of Rs.19,73,337 was added to the income of the

Assessee and initiation of penalty proceedings was directed.

9. The Commissioner of Income Tax (Appeals) [CIT (A)] allowed the

appeal of the Assessee by order dated 2nd July 2010. The ITAT, by the

impugned order dated 26th September 2014, allowed the Revenue‟s appeal.

10. Reliance has been placed by Mr. N.P. Sahni, learned Senior Standing

counsel for the Revenue, on the decision of the Supreme Court in ALA Firm v. CIT (1991) 189 ITR 285 (SC) to urge that in similar circumstances where the AO had overlooked a binding precedent on the issue, it was construed as a sufficient material to justify reopening of the assessment.

11. It requires to be noticed that in ALA Firm (supra) the relevant AY was 1961-62. An item of expenditure in respect of „house property‟ was allowed as deduction on the ground that it was not assessable either as revenue or capital expenditure. When for the subsequent AY 1962-63 the Assessee filed its return showing nil income, the Income Tax Officer issued notice on 3rd September 1963 stating that the amount ought to have been brought to tax in AY 1961-62 in view of the decision of the Madras High Court in Ramachari & Co. v. CIT (1961) 41 ITR 142. Following the reply given by the Assessee, the ITO issued a notice under Section 148 (of Income Tax Act, 1961) read with Section 147(b) (of Income Tax Act, 1961). The Assessee objected to reopening of the assessment. It was in the above facts and circumstances, that the Supreme Court held that the material which constituted information and the basis of which the assessment was reopened was the decision of the Madras High Court which had not been considered at the time of the original assessment. Accordingly, the reopening of the assessment was upheld.

12. There are at least two reasons why the decision in ALA Firm (supra)

would not be applicable in the facts of the present case. In the first place, it is apparent that the said decision was not in the context of reopening of assessment sought to be made four years after the expiry of the relevant assessment year of the original assessment. The reopening was done not very long after the initial assessment. Secondly, the decision was rendered in respect of Section 147 (of Income Tax Act, 1961) as it stood prior to its amendment with effect from 1st April 1989.

13. The effect of the change brought about to Section 147 (of Income Tax Act, 1961) by way of

amendment with effect from 1st April 1989 requires to be examined. Prior to 1st April 1989, in order to reopen an assessment the AO ought to have had reason to believe that the income of the Assessee has escaped assessment on account of the omission or failure by the Assessee to file a return or to disclose fully and truly all material facts necessary for assessment for that year. After the amendment the only requirement as far as Section 147(1) (of Income Tax Act, 1961) is concerned is that the AO should have reason to believe that the income of the Assessee has escaped assessment. However the proviso to Section 147(1) (of Income Tax Act, 1961) as amended kicks in where the reopening is sought to be done after four years after the end of the relevant assessment year for which the original assessment was made. This brings in the requirement of the AO satisfying himself of the existence of either jurisdictional fact. The escapement of income should be occasioned "by reason of the failure on the part of the

assessee to make a return under section 139 (of Income Tax Act, 1961) or in response to a notice issued under sub-section(1) of section 142 (of Income Tax Act, 1961) or section 148 (of Income Tax Act, 1961)" or "to disclose fully and truly all material facts necessary for his assessment, for that assessment year."

14. The Supreme Court in CIT v. Kelvinator of India Ltd. (2010) 320 ITR

561 (SC) has held that, even in terms of the amended Section 147 (of Income Tax Act, 1961) there has to be some tangible material for an AO to have reason to believe that income has escaped assessment. The Supreme Court emphasised that although the

power to reopen is much wider after the amendment, the words “reason to

believe” needed a schematic interpretation and that the AO ought not be

given power to reopen the assessment on the basis of a mere change of

opinion. It was emphasised that "re-assessment has to be based on

fulfillment of certain pre-condition and if the concept of 'change of opinion'is removed, as contended on behalf of the Department, then, in the garb of re-opening the assessment, review would take place. One must treat the concept of 'change of opinion' as an in-built test to check abuse of power by the Assessing Officer”. The Supreme Court held as under:

“Hence, after 1st April, 1989, Assessing Officer has power

to re-open, provided there is "tangible material" to come to

the conclusion that there is escapement of income from

assessment.”

15. In Haryana Acrylic Manufacturing Co. Ltd. v. CIT, 308 ITR 38 (Del.),

this Court reiterated the law in relation to reopening of an assessment under Section 147 (of Income Tax Act, 1961)/148 of the Act after the expiry of four years after the assessment year for which the original assessment was made. Recently, in its decision dated 22nd September 2015 in ITA No. 356 of 2013 (Commissioner of Income Tax II v. Multiplex Trading & Industrial Co. Ltd.) this Court, in a case where reopening of assessment was sought to be made four years after the expiry of the original assessment, held that “in order to reopen an assessment which is beyond the period of four years from the end of the relevant assessment year, the condition that there has been a failure on the part of the Assessee to truly and fully disclose all material facts must be concluded with certain level of certainty.”

16. In the present case, there was no failure on the part of the Assessee to disclose the material particulars with the return originally filed. On the contrary, the AO himself replied to the audit objection pointing out that royalty was allowed to be claimed as revenue expenditure by the Assessee for the years earlier to AY 2002-03. A copy of the agreement under which royalty was being paid was provided to the Revenue. The only reason for reopening the assessment was that the decision in Southern Switchgears Ltd. v. CIT 232 ITR 359, which was rendered by the Supreme Court several years earlier on 11th December 1997 was not noticed by the AO at the time of finalization of assessment at the first instance on 31st January 2005 under Section 143(3) (of Income Tax Act, 1961).

17. In light of the legal position after the amendment to Section 147 (of Income Tax Act, 1961), as explained in CIT v. Kelvinator of India Ltd. (supra), the Court is of the view that, in a case where the assessment is sought to be reopened in 2009, four years after it was originally made, i.e. 2005, the mere fact that there was a judgment of the Supreme Court of 1997 which was not noticed by the AO when he framed the original assessment cannot per se constitute the only material on the basis of which the assessment could have been reopened. When on the same material, four years after the assessment year for which the original assessment is finalised, the AO seeks to reopen the assessment on the basis of a judicial precedent delivered more than eight years earlier, it would be a case of mere 'change of opinion', something clearly held impermissible by CIT v. Kelvinator of India Ltd. (supra), The threshold requirement of that the AO should, on the basis of some tangible material, conclude that there was escapement of income on account of the Assessee failing to disclose material particulars, is not fulfilled in the present

case. Consequently, the reopening of the assessment was, in the facts of the present case, not justified.

18. The question is accordingly answered in the affirmative, i.e. in favour of the Assessee and against the Revenue. The impugned order of the ITAT is set aside.

19. The appeal is allowed, but in the circumstances, with no orders as to costs.

S.MURALIDHAR, J

VIBHU BAKHRU, J

OCTOBER 09, 2015

×

Similar Ripples

Questions

Reopening Tax Assessments: Court Sides with Assessee Over Revenue

Write your CommentSimilar Posts

Generic

- Reportdata/3387.pdf