"Supreme Court Dismisses Appeal Challenging Income Tax Department's Auction of …

Full News

"Supreme Court Dismisses Appeal Challenging Income Tax Department's Auction of Attached Property for Debt Recovery".

"Supreme Court Dismisses Appeal Challenging Income Tax Department's Auction of Attached Property for Debt Rec…

This appeal is against the judgment of the Division Bench of the High Court of Andhra Pradesh at Hyderabad in a writ petition. The main question in this appeal is whether the Income Tax Department was justified in auctioning the attached property for debt recovery. The appellant, M/s Janatha Textiles, is a registered firm with four partners. The firm and its partners had tax arrears for certain assessment years, but the demands for those years were stayed and never enforced for collection. However, the demand for the assessment year 1985-86 was enforced, and the agricultural lands owned by the partners were attached and sold in public auction. The appellant firm had a demand of Rs. 4,99,133/- for the assessment year 1985-86, along with additional amounts for interest and penalty. The total amount due from the appellants for that assessment year was Rs. 12,55,150/-. The Income Tax Department auctioned the property to recover its outstanding dues. The appellants raised objections to the auction sale, claiming that their objections were not disposed of before the sale took place. They also argued that the application for waiver of interest and the stay application were pending. They further contended that the nature of the lands in the auction notice was incorrectly mentioned as dry lands when they were actually a mango orchard and building structure. The High Court rejected the appellants' arguments and upheld the auction sale. The court stated that the appellants had an alternate remedy under the Income Tax Act but chose to file a petition before the High Court instead. The court also emphasized the principle of protecting the rights of bona fide purchasers for value and cited various precedents in support of this principle. The Supreme Court heard the appeal and upheld the judgment of the High Court. The court reiterated the distinction between a stranger bona fide purchaser at an auction sale and a decree-holder purchaser, stating that the former is afforded protection by the court. The court concluded that the auction sale was valid and dismissed the appeal. This summary provides an overview of the case and the main arguments made by the parties. It highlights the key points discussed in the judgment of the Supreme Court, which affirmed the decision of the High Court.

This appeal pertains to a judgment passed by the Division Bench of the High Court of Andhra Pradesh at Hyderabad in writ petition No.22038 of 1996 on 6.9.2001. The central question in this appeal is whether the Income Tax Department is justified in auctioning the attached property for debt recovery.

The appellant, M/s Janatha Textiles, is a registered firm with four partners. The firm and its partners had outstanding tax arrears for various assessment years, with the demands for assessment years 1986-87 to 1989-90 being stayed by different Income Tax Authorities. However, the demand for assessment year 1985-86 was enforced.

The agricultural lands owned by the partners of the appellant firm were attached and sold in a public auction on 5.8.1996, following the prescribed procedures. The highest bid was made by L. Krishna Prasad, and there were no allegations of irregularities in the auction process.

The total outstanding amount due from the appellants for the assessment year 1985-86, including tax, interest, and penalty, was Rs. 12,55,150/-. The respondent-department argued that they were justified in auctioning the property to recover their dues. The demands related to assessment years 1986-87 to 1989-90 had not been enforced due to stay orders.

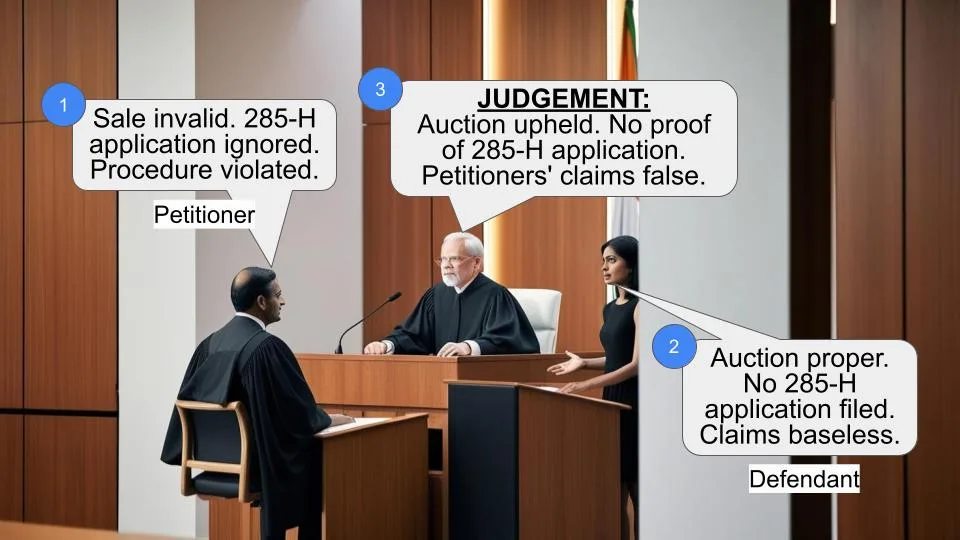

The appellants contended that the respondent-department proceeded with the auction sale without disposing of their objections and that the sale was illegal and unsustainable. They also mentioned that their application for waiver of interest was pending, and their stay application was not disposed of, making the sale illegal.

The High Court failed to consider that the property mentioned in the auction notice was wrongly described as dry lands, while it was actually a mango orchard and building structure with a higher value. The appellants argued that this error alone should invalidate the auction.

The appellants further argued that the respondent-department failed to give them notice of demand concerning their share in the partnership firm, but the court found no merit in this argument as individual notices were received and no prejudice was caused.

The respondent-department stated that the auction proceedings were initiated only for the arrears related to the assessment year 1985-86 and that the appellants had an alternate remedy available under the Income Tax Act.

The case discussed the principle of protecting the rights of bona fide purchasers for value in auction sales. The court referred to various judgments, including the Privy Council's ruling in Nawab Zain-Ul-Abdin Khan v. Muhammad Asghar Ali Khan & others, to emphasize that bona fide purchasers who are strangers to the decree should be protected.

After considering the arguments and reviewing the documents, the court found no merit in the appeal and upheld the judgment of the High Court. The appeal was dismissed, and the parties were directed to bear their own costs.

Date: May 16, 2008.

1. This appeal is directed against the judgment of the

Division Bench of the High Court of Andhra Pradesh at

Hyderabad passed in writ petition No.22038 of 1996 on

6.9.2001.

2. The short question which arises for consideration in this

appeal is whether the Income Tax Department is justified in

auctioning the attached property for recovery of debt?

3. Brief facts which are necessary to dispose of this appeal

are as under:

The appellant M/s Janatha Textiles is a registered firm

with four partners viz. Radhey Shyam Modi, Pawan Kumar

Modi, Padmadevi Modi and Indira Chirmar. The firm and its

partners were in arrears of tax for the assessment years 1985-

86, 1986-87, 1987-88, 1989-90. All the demands pertaining

to assessment years 1986-87 to 1989-90 have been stayed by

various Income Tax Authorities and these demands were

never enforced for collection. The demand pertaining to

assessment year 1985-86 was alone enforced.

4. The agricultural lands owned by the partners of the

appellant firm at Bodametlapalem had been attached and sold

in public auction on 5.8.1996 after following the entire

procedure laid down under second schedule to the Income

Tax Act, 1961 (hereinafter referred to as “the 1961 Act”). Nine

people participated in the public auction held on 5.8.1996.

The sale was confirmed in favour of L. Krishna Prasad who

offered the highest price. No procedural irregularity or

illegality in public auction process was even alleged by the

appellants.

5. A demand of Rs.7,84,072/- for the assessment year

1985-86 was initially raised against the appellant firm. By

virtue of grant of partial relief in the appeal, the demand was

reduced to Rs.4,65,174/- and as against the said amount, the

appellant firm paid only Rs.4,34,927/- leaving a balance of

Rs.30,247/-. In addition to this, there was demand of

Rs.5,65,538/- raised by virtue of levy of penalty imposed

under section 271(1)(c) of the Income Tax Act, 1961 for the said

assessment year. The levy was confirmed in appeal by the

Commissioner of Income Tax (Appeals). Further demands

were also raised for a sum of Rs.2,82,160/-, Rs.3,42,518/-

and Rs.2,86,075/- at the hands of individual assessment of

appellant nos.2, 3, and 4 respectively. In the assessment year

1985-86, partial relief was granted and ultimately quantified

the amount due from the appellant firm and its partners.

After adjusting the amounts paid, the amount due as on the

date of auction for the assessment year 1985-86 stood at

Rs.4,99,133/-. In addition to these arrears, an amount of

Rs.7,56,017 fell due by way of interest. Thus, a total amount

of Rs.12,55,150/- was due from the appellants for the

assessment year 1985-86 towards tax, interest and penalty.

6. It may be pertinent to mention that the demands

relatable to assessment years 1986-87 to 1989-90 have never

been enforced because of the various stay orders by the

different Income Tax authorities.

7. Even after issuance of sale proclamation, the

respondent-department issued communication in SR No.2/94

dated 15.7.1996 informing the appellants that a sum of

Rs.5,68,913/- was due as on that date towards tax, interest

and penalty under the 1961 Act. The said amount, however,

does not include interest payable under section 220(2) (of Income Tax Act, 1961) of the

1961 Act. The appellant firm acknowledged receipt of the

letter on 17.7.1996 and had not contradicted the quantum of

tax and interest as mentioned in the said letter. It was made

clear that the demand for the assessment year 1985-86 alone

was being enforced. Therefore, it was absolutely no warrant

for the appellant to mix up the said demands relatable to the

assessment year 1985-86 in this appeal. According to the

records of the Income Tax Department, the net amount of tax,

interest and penalty due for the assessment year 1985-86 as

on the date of auction stood at Rs.12,55,150/- and hence the

respondent-department was fully justified in auctioning the

property of the appellants to recover its outstanding dues.

8. Learned counsel for the appellants contended that even

though they had filed objections at various stages of the notice

issued for the auction sale, but the respondent-department

without disposing of the said objections proceeded with the

sale and, therefore, even on that ground the sale conducted by

the respondent-department was illegal and unsustainable.

The appellants further submitted that with reference to the

assessment year 1985-86, the application for waiver of

interest was pending before the authorities and further the

stay application filed before the Commissioner was not

disposed of. Even on that count also the sale conducted by

the respondent-department on 5.8.1996 was illegal and

unsustainable.

9. It was categorically mentioned on behalf of the

respondent-department that the sale proceedings were

initiated continued only with reference to arrears relating to

the assessment year 1985-86.

10. The appellants contended that the High Court has failed

to notice that the nature of the lands in the auction notice was

wrongly mentioned as dry lands. In fact the said lands were a

mango orchard and building structure and of much higher

value. The auction ought to be vitiated on this ground alone.

11. Learned counsel for the appellants also submitted that

the appellants have received the notice of demand as

defaulters in their individual capacity and also as the partners

of the firm, however, the respondent-department has failed to

give notice of demand to the appellants qua their share in the

partnership firm. They did not receive the notices indicating

their respective shares. The appellants have raised hyper

technical ground. Admittedly, no prejudice of any kind has

been caused to the appellants when notices were received

individually by each partner of the firm both in their

individual capacity and in the capacity as a partner of the

firm. This argument of the appellants is devoid of any merit

and is accordingly rejected.

12. Learned counsel for the respondent-department

submitted that it is not the case of the assessee appellants

that they do not owe the amount to the respondent-

department towards tax for the assessment year 1985-86.

The appellants also failed to make out the case that the proper

procedure which has been laid down has not been followed by

the respondent-department in recovering its outstanding

amount. It was asserted on behalf of the respondent-

department that the amount fetched in the public auction was

more than reasonable.

13. The reserve price and the amounts fetched in the auction

are mentioned hereunder:

Name Reserve price fixed by the assessing officer (with the prior

approval of Dy. Commissioner)

Sale Value

Pawan Kumar 89,800 1,67,800

Radheshyam Modi 96,000 1,84,400

Padmadevi Modi 40,000 76,600

14. The appellants had never complained about fixing of the

reserve price before holding of auction, though they were

intimated of the same through sale proclamation.

15. In pursuance to the notice issued by this court,

respondent-department filed the counter affidavit.

Respondent no. 2 also filed a separate counter affidavit.

Respondent no. 2 in the counter affidavit stated that it is

totally incorrect to suggest that the auction sale did not fetch

the actual market value of the property. Respondent no.2 also

mentioned in the counter affidavit that the said lands are

agricultural dry lands and there are no mango gardens as

alleged by the appellants. There are however few mango trees

scattered all over the land.

16. Respondent-department in the counter affidavit stated

that the appellant firm had alternate efficacious remedy by

way of filing a petition under rules 60 (of Income Tax Rules, 1962) and 61 (of Income Tax Act, 1961) of the Second

Schedule to the 1961 Act. The appellant ought to have availed

of the statutory remedy for ventilating its grievances instead of

filing a petition before the High Court.

17. There is another very significant aspect of this case,

which pertains to the rights of the bona fide purchaser for

value. It was asserted that respondent no. 2 is a bona fide

purchaser of the property for value. It was further stated that

he had purchased the said property in a valid auction and he

cannot be disturbed according to the settled legal position.

18. It is an established principle of law that in a third party

auction purchaser’s interest in the auctioned property

continues to be protected notwithstanding that the underlying

decree is subsequently set aside or otherwise. This principle

has been stated and re-affirmed in a number of judicial

pronouncements by the Privy Council and this court.

Reliance has been placed on the following decisions.

19. The Privy Council in Nawab Zain-Ul-Abdin Khan v.

Muhammad Asghar Ali Khan & others (1887) 15 I.A. 12 for

the first time crystallized the law on this point, wherein a

three Judge Bench held as follows:

“A great distinction has been made between

the case of bona fide purchasers who are not

parties to a decree at a sale under execution and

the decree-holders themselves. In Bacon’s

Abridgment, it is laid down, citing old authorities,

that “If a man recovers damages, and hath

execution by fieri facias, and upon the fieri facias

the sheriff sells to a stranger a term for years, and

after the judgment is reversed, the party shall be

restored only to the money for which the term was

sold, and not to the term itself, because the sheriff

had sold it by the command of the writ of fieri

facias.”. So in this case, those bona fide purchasers

who were no parties to the decree which was then

valid and in force, had nothing to do further than to

look to the decree and to the order of sale.”

20. In the case of Janak Raj vs. Gurdial Singh & Another

(1967) 2 SCR 77, the Division Bench comprising Justice

Wanchoo and Justice Mitter held that in the facts of the said

case the appellant auction-purchaser was entitled to a

confirmation of the sale notwithstanding the fact that after the

holding of the sale, the decree was set aside. It was observed:

“The policy of the Legislature seems to be that

unless a stranger auction-purchaser is protected

against the vicissitudes of the fortunes of the suit,

sales in execution would not attract customers and

it would be to the detriment of the interest of the

borrower and the creditor alike if sales were allowed

to be impugned merely because the decree was

ultimately set aside or modified.”

21. In the case of Gurjoginder Singh v. Jaswant Kaur

(Smt.) & Another (1994) 2 SCC 368, this court relying on the

judgment rendered by the Privy Council held that the status of

a bona fide purchaser in an auction sale in execution of a

decree to which he was not a party stood on a distinct and

different footing from that of a person who was inducted as a

tenant by a decree-holder-landlord. It was held as follows:

“A stranger auction purchaser does not derive

his title from either the decree-holder or the

judgment-debtor and therefore restitution may not

be granted against him but a tenant who obtains

possession from the decree-holder landlord cannot

avail of the same right as his possession as a tenant

is derived from the landlord.”

22. In the case of Padanathil Ruqmini Amma v. P. K.

Abdulla (1996) 7 SCC 668, this court in para 11 observed as

under:

“11. In the present case, as the ex parte decree

was set aside, the judgment-debtor was entitled to

seek restitution of the property which had been sold

in court auction in execution of the ex parte decree.

There is no doubt that when the decree-holder

himself is the auction-purchaser in a court auction

sale held in execution of a decree which is

subsequently set aside, restitution of the property

can be ordered in favour of the judgment-debtor.

The decree-holder auction-purchaser is bound to

return the property. It is equally well settled that if

at a court auction sale in execution of a decree, the

properties are purchased by a bona fide purchaser

who is a stranger to the court proceedings, the sale

in his favour is protected and he cannot be asked to

restitute the property to the judgment-debtor if the

decree is set aside. The ratio behind this distinction

between a sale to a decree-holder and a sale to a

stranger is that the court, as a matter of policy, will

protect honest outsider purchasers at sales held in

the execution of its decrees, although the sales may

be subsequently set aside, when such purchasers

are not parties to the suit. But for such protection,

the properties which are sold in court auctions

would not fetch a proper price and the decree-

holder himself would suffer. The same

consideration does not apply when the decree-

holder is himself the purchaser and the decree in

his favour is set aside. He is a party to the litigation

and is very much aware of the vicissitudes of

litigation and needs no protection.”

23. In Para 16, the court further elaborated the distinction

between the decree-holder auction purchaser and a stranger

who is a bona fide purchaser in auction. Para 16 reads as

under:

“16. The distinction between a stranger who

purchases at an auction sale and an assignee from

a decree-holder purchaser at an auction sale is

quite clear. Persons who purchase at a court

auction who are strangers to the decree are afforded

protection by the court because they are not in any

way connected with the decree. Unless they are

assured of title; the court auction would not fetch a

good price and would be detrimental to the decree-

holder. The policy, therefore, is to protect such

purchasers. This policy cannot extend to those

outsiders who do not purchase at a court auction.

When outsiders purchase from a decree-holder who

is an auction-purchaser clearly their title is

dependent upon the title of decree-holder auction-

purchaser. It is a defeasible title liable to be

defeated if the decree is set aside. A person who

takes an assignment of the property from such a

purchaser is expected to be aware of the

defeasibility of the title of his assignor. He has not

purchased the property through the court at all.

There is, therefore, no question of the court

extending any protection to him. The doctrine of a

bona fide purchaser for value also cannot extend to

such an outsider who derives his title through a

decree-holder auction-purchaser. He is aware or is

expected to be aware of the nature of the title

derived by his seller who is a decree-holder auction-

purchaser.”

24. In the case of Ashwin S. Mehta & Another v.

Custodian & Others (2006) 2 SCC 385, this court whilst

relying upon the aforementioned two judgments stated the

principle in the following words:

“In any event, ordinarily, a bona fide

purchaser for value in an auction sale is treated

differently than a decree holder purchasing such

properties. In the former event, even if such a

decree is set aside, the interest of the bona fide

purchaser in an auction sale is saved.”

25. We have heard the learned counsel for the parties at

length and have perused the material documents on record.

26. Law makes a clear distinction between a stranger who is

a bona fide purchaser of the property at an auction sale and a

decree holder purchaser at a court auction. The strangers to

the decree are afforded protection by the court because they

are not connected with the decree. Unless the protection is

extended to them the court sales would not fetch market value

or fair price of the property.

27. In our opinion, the view taken by the High Court in the

impugned judgment is eminently just and fair. No

interference is therefore called for.

28. The appeal being devoid of any merit is accordingly

dismissed. In the facts and circumstances of the case, we

direct the parties to bear their own costs.

(Ashok Bhan)

(Dalveer Bhandari)

New Delhi;

May 16, 2008

×

Similar Ripples

Questions

"Supreme Court Dismisses Appeal Challenging Income Tax Department's Auction of Attached Property for Debt Recovery".

Write your CommentSimilar Posts

Generic

- Reportdata/2377_ODNLXOF.pdf