Supreme Court ruling on tax exemption for early retirees upheld, Board's power …

Full News

Supreme Court ruling on tax exemption for early retirees upheld, Board's power to relax rules affirmed

Supreme Court ruling on tax exemption for early retirees upheld, Board's power to relax rules affirmed

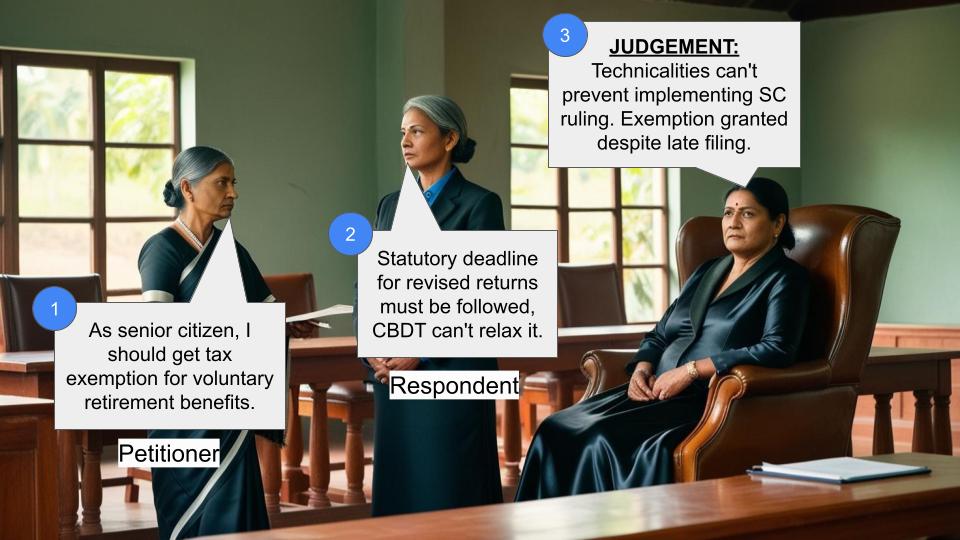

This case involves a retired ICICI Bank employee who sought tax exemption under Section 10(10C) (of Income Tax Act, 1961) for voluntary retirement benefits. The court ruled in favor of the petitioner, directing the Income Tax Officer to grant the exemption despite the late filing of a revised return, based on a previous Supreme Court decision and CBDT circular.

To delve deeper, you can read the original judgement of the court order here.

Case Name:

S. Sevugan Chettiar Vs Principal Chief Commissioner of Income Tax & Ors.(High Court of Madras)

Writ Petition No.42385 of 2016

Key Takeaways

1. The court affirmed the CBDT's power to relax rules for genuine hardship cases.

2. Technical deadlines should not prevent implementation of Supreme Court rulings.

3. The High Court can exercise powers similar to CBDT under Article 226 of the Constitution.

4. Senior citizens may receive special consideration in tax matters.

Issue

Can a taxpayer claim exemption under Section 10(10C) (of Income Tax Act, 1961) for voluntary retirement benefits after the deadline for filing a revised return has passed?

Facts

- The petitioner is a 68-year-old retired employee of ICICI Bank.

- He filed his original tax return, which was assessed.

- Later, he learned of a Supreme Court decision (S.Palaniappan Vs. I.T.O.) granting exemption under Section 10(10C) (of Income Tax Act, 1961) for voluntary retirement schemes.

- CBDT issued a circular on 13.4.2016 to implement this decision for ICICI Bank retirees.

- The petitioner filed a revised return claiming the exemption.

- The Income Tax Officer rejected the revised return as it was filed beyond the time limit specified in Section 139(5) (of Income Tax Act, 1961).

Arguments

Petitioner:

- The Supreme Court decision and CBDT circular should be binding on tax officers.

- As a senior citizen, he should be granted relief.

- Cited previous High Court decisions granting similar relief.

Revenue:

- Section 139(5) (of Income Tax Act, 1961) sets a strict time limit for revised returns.

- The tax officer correctly applied this statutory deadline.

- Suggested the petitioner could approach CBDT for relief.

Key Legal Precedents

1. S. Palaniappan Vs. I.T.O. [Civil Appeal No. 4411 of 2010 dated 28.9.2015]

2. K.R. Alagappan Vs. A.C.I.T. [W.P.(MD) No.3986 of 2007 etc. cases dated

3.11.2010]

3. C. Navaneet hakrishnan Vs. A.C.I.T. [W.P.(MD) No.3263 of 2012 etc. cases dated 10.9.2012]

Judgement

The court allowed the petition, setting aside the Income Tax Officer's order and directing the grant of exemption under Section 10(10C) (of Income Tax Act, 1961) within three months. Key points:

1. Technicalities should not prevent implementation of Supreme Court rulings.

2. CBDT's circular under Section 119 (of Income Tax Act, 1961) is binding on tax officers.

3. The court can exercise powers similar to CBDT under Article 226 of the Constitution.

4. The petitioner's status as a senior citizen and the financial benefit involved were considered.

FAQs

Q1: Can the CBDT relax statutory deadlines?

A1: Yes, under Section 119 (of Income Tax Act, 1961), CBDT can relax certain requirements to avoid genuine hardshi

Q2: Does a Supreme Court decision automatically apply to similar cases?

A2: Not automatically, but it should be considered by tax authorities and can be enforced through CBDT circulars or court orders.

Q3: Can High Courts override statutory deadlines in tax matters?

A3: In certain cases, High Courts can use their powers under Article 226 of the Constitution to provide relief, especially when implementing Supreme Court decisions.

Q4: Are senior citizens given special consideration in tax matters?

A4: While not a rule, courts may consider advanced age as a factor when deciding on tax relief in certain cases.

Q5: What should taxpayers do if they discover they're eligible for an exemption after the deadline for revised returns

A5: They can approach the CBDT for relief or, if necessary, file a writ petition in the High Court.

1. Mr. J. Narayanaswamy, learned Senior Standing Counsel accepts notice for the respondents. Heard both. By consent, the writ petition itself is taken up for final disposal.

2. The petitioner is a retired employee of the ICICI Bank and is presently aged 68 years. He is constrained to approach this Court in terms of the proceedings dated 4.8.2016 issued by the third respondent.

3. The issue lies in a narrow compass. The petitioner, upon retirement, filed his return of income for the relevant year and the assessment was finalized. Subsequently, the petitioner came to know that the Hon'ble Supreme Court, in the case of S.Palaniappan Vs. I.T.O. [Civil Appeal No. 4411 of 2010 dated 28.9.2015] held that a person, who has opted for voluntary retirement under the Early Retirement Option Scheme shall be entitled to exemption under Section 10(10C) (of Income Tax Act, 1961), 1961 (hereinafter referred to as the Act). Following the said decision, the Central Board of Direct Taxes issued a circular dated 13.4.2016 stating that the judgment of the Hon'ble Supreme Court be brought to the notice of all officials in the respective jurisdiction so that relief may be granted to such retirees of the ICICI Bank under Early Retirement Option Scheme, 2003.

4. The petitioner, on coming to know of the same, filed a revised return by referring to the said decision and stating that only after the said decision came to his notice, he had been advised to file the revised return.

However, this has been rejected vide the impugned proceedings dated 4.8.2016 by the third respondent by referring to Section 139(5) (of Income Tax Act, 1961). In other words, the revised return was refused to be accepted as it is beyond the time stipulated under Section 139(5) (of Income Tax Act, 1961). Assailing the correctness of the order of the third respondent, the petitioner is before this Court.

5. The learned counsel for the petitioner has submitted that the petitioner is a senior citizen and the law having been laid down by the Hon'ble Supreme Court, it would bind the Assessing Officers and all the Authorities, apart from the fact that a circular has been issued by the Central Board of Direct Taxes, which also binds the Assessing Officers. Therefore, it is submitted that the relief may be granted to the petitioner.

6. The learned counsel for the petitioner also places reliance on the decision of the Madurai Bench of this Court in the case of K.R.Alagappan Vs. A.C.I.T. [W.P.(MD) No.3986 of 2007 etc. cases dated 3.11.2010], which was followed in the case of C.Navaneethakrishnan Vs. A.C.I.T. [W.P.(MD) No.3263 of 2012 etc. cases dated 10.9.2012].

7. Mr.J.Narayanasamy, learned Senior Standing Counsel for the Revenue has referred to Section 139(5) (of Income Tax Act, 1961) and contended that when the said provision stipulates the outer time limit, within which, the assessee is entitled to file a revised return of income, this has been rightly taken note of by the third respondent, as the third respondent is not entitled to entertain a revised return beyond the statutory time limit. It is further submitted that the petitioner can always move the Central Board for appropriate relief, which is entitled to consider the grant of exemption.

8. After hearing the learned counsel for the parties and perusing the materials placed on record, this Court is of the view that the technicality should not stand in the way while giving effect to the order passed by the Hon'ble Supreme Court. The Board also issued a circular on 13.4.2016 with a view to grant relief to the retirees of the ICICI Bank under the Early Retirement Option Scheme. Several persons, who had filed writ petitions before the Madurai Bench of this Court, have been granted the relief. In fact,in those orders, the Court took into consideration the decision of the Hon'ble Supreme Court and granted the relief.

9. The circular issued by the Central Board of Direct Taxes is in exercise of the powers conferred under Section 119 (of Income Tax Act, 1961). The said provision deals with instructions to Subordinate Authorities. Sub-Section (1) of Section 119 (of Income Tax Act, 1961) states that the Board may, from time to time, issue such orders, instructions and directions to other Income Tax Authorities, as it may deem fit, for the proper administration of the provisions of the Act and such Authorities and all other persons employed in the execution of this Act shall observe and follow such orders, instructions and directions of the Board.

The Proviso carves out certain exceptions, under which circumstances, the Board will not issue instructions.

10. Clause (a) to Sub-Section (2) of Section 119 (of Income Tax Act, 1961) states that without prejudice to the generality of the power under Section 119(1) (of Income Tax Act, 1961), the the Board may, if it considers it necessary or expedient so to do, for the purpose of proper and efficient management of the work of assessment and collection of revenue, issue, from time to time (whether by way of relaxation of any of the provisions of the Act as mentioned therein, general or special orders in respect of any class of income or fringe benefits or class of cases,setting forth directions or instructions as to the guidelines, principles or procedures to be followed by other Income-Tax Authorities in the work relating to assessment or collection of revenue or the initiation of proceedings for the imposition of penalties and any such order may be made if the Board is of opinion that it is necessary in the public interest. It is relevant to point out that one of the provisions, which are listed out under Clause (a) to Sub-Section (2) of Section 119 (of Income Tax Act, 1961) is Section 139 (of Income Tax Act, 1961).

11. Admittedly, the case, which was considered by the Hon'ble Supreme Court related to an individual employee namely S.Palaniappan, who was also a similarly placed person as that of the petitioner. Thus, the Board,in its wisdom, while implementing the judgement in the case of S.Palaniappan, took a decision that such a benefit should be extended to the similarly placed persons treating them as class of cases. Therefore, the Board observed that the order should be communicated to all the Commissioners,so that relief can be granted to such retirees of the ICICI Bank. Thus, the petitioner cannot be non-suited solely on the ground that he had filed a revised return well beyond the period stipulated under Section 139(5) (of Income Tax Act, 1961).

12. Furthermore, it is relevant to point out that Clause (c) to Sub- Section (2) of Section 119 (of Income Tax Act, 1961) states that the Board may, if it considers it desirable or expedient so to do for avoiding genuine hardship in any case or class of cases, by general or special order, relax any requirement contained in any of the provisions contained in Chapter IV or Chapter VI-A of the Act, which deal with computation of total income and deductions to be made in computing the total income and such power is exercisable where the petitioner failed to comply with any requirement specified in such provision for claiming deduction thereunder, subject to the conditions that (i) the default is due to circumstances beyond the control of the assessee and (ii) the assessee has complied with the requirement before the assessment in relation to previous year, in which, such deduction is claimed.

13. Thus, if the default in complying with the requirement was due to circumstances beyond the control of the assessee, the Board is entitled to exercise its power and relax the requirement contained in Chapter IV or Chapter VI-A. If such a power is conferred upon the Board, this Court, while exercising jurisdiction under Article 226 of The Constitution of India, would also be entitled to consider as to whether the petitioner's case would fall within one of the conditions stipulated under Section 119(2)(c) (of Income Tax Act, 1961).

14. Considering the hard facts, the petitioner, being a senior citizen, cannot be denied of the benefit of exemption under Section 10(10C) (of Income Tax Act, 1961) and the financial benefit that had accrued to the petitioner, which would be more than a lakh of rupees. Therefore, this Court is of the view that the third respondent should grant the benefit of exemption to the petitioner.

15. Accordingly, the writ petition is partly allowed, the impugned order is set aside and the third respondent is directed to grant the benefit of exemption under Section 10(10C) (of Income Tax Act, 1961) and refund the appropriate amount to the petitioner, within a period of three months from the date of receipt of a copy of this order. Considering the facts and circumstances of the case, the prayer for interest is rejected. No costs.

Internet : Yes

To

1.The Principal Chief Commissioner of Income Tax, Aayakar Bhawan, Office of the Chief Commissioner of I.T., Chennai- M.G., 121, Nungambakkam High Road, Tirumurthy Nagar, Chennai-34.

2.The Commissioner of Income Tax, (Appeals), Office of the Commissioner of Income Tax (Appeals), No.4, Williams Road, Cantonment, Tiruchirappalli-1.

3.The Income Tax Officer, Ward I(2), Kumbakonam.RS

T.S.SIVAGNANAM,J

02.12.2016

×

Similar Ripples

Questions

Supreme Court ruling on tax exemption for early retirees upheld, Board's power to relax rules affirmed

Write your CommentSimilar Posts

Generic

- Reportdata/11441-madras-hc.pdf