Tax Appeal Dismissed: High Court Upholds Tribunal's Decision in Favor of Assess…

Full News

Tax Appeal Dismissed: High Court Upholds Tribunal's Decision in Favor of Assessee

Tax Appeal Dismissed: High Court Upholds Tribunal's Decision in Favor of Assessee

The Principal Commissioner of Income Tax (the tax department) filed an appeal against a company called M/s Amravati Infrastructures Developers Pvt. Ltd. The tax department wasn't happy with a decision made by the Income Tax Appellate Tribunal, which had ruled in favor of the company. But guess what? The High Court ended up dismissing the tax department's appeal, agreeing with the Tribunal's decision.

Get the full picture - access the original judgement of the court order here

Case Name:

Principal Commissioner of Income Tax vs M/s Amravati Infrastructures Developers Pvt. Ltd. (High Court of Punjab & Haryana)

Income Tax Appeal No.378 of 2016(O&M)

Date: 11th February 2020

Key Takeaways:

1. The High Court emphasized the importance of respecting the Tribunal's role as the final fact-finding authority.

2. Additional evidence can be considered by appellate authorities if proper procedures are followed.

3. The case highlights the significance of maintaining proper documentation for share capital, loans, and business agreements.

Issue:

The main question here was: Did the Income Tax Appellate Tribunal err in dismissing the Revenue's appeal and upholding the CIT(A)'s order that deleted additions made by the Assessing Officer?

Facts:

1. M/s Amravati Infrastructures Developers Pvt. Ltd. is a colonizer (a company that develops land).

2. For the 2009-10 assessment year, the Assessing Officer made some additions to the company's income, totaling Rs. 3,95,00,000.

3. These additions were on three counts:

a) Rs. 1.65 Crores for share capital and premium

b) Rs. 1.10 Crores for alleged accrued income from M/s Satya Developers Limited

c) Rs. 1.20 Crore for loans received

4. The company appealed to the CIT(A), who deleted all these additions.

5. The tax department then appealed to the Tribunal, which dismissed their appeal.

6. Now, the tax department has come to the High Court, challenging the Tribunal's decision.

Arguments:

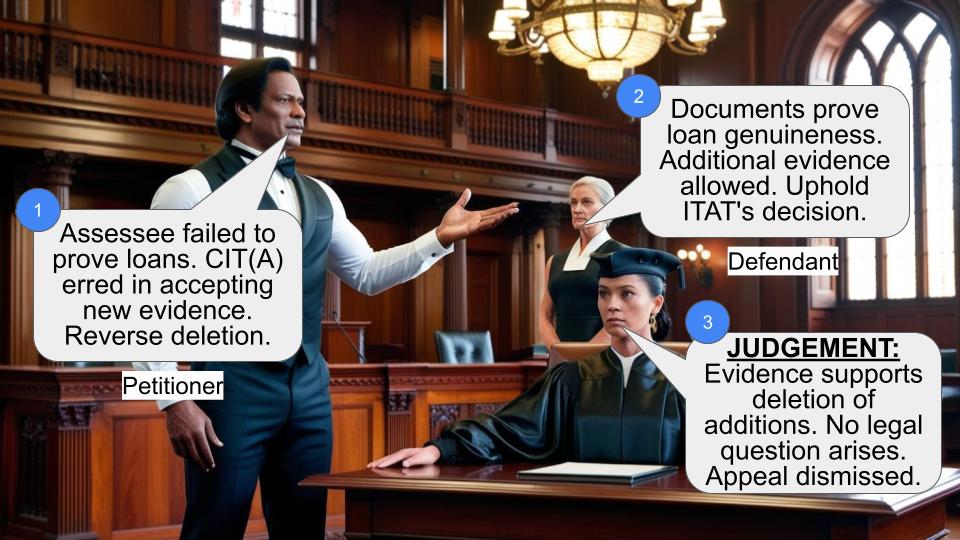

The tax department's main argument was that the CIT(A) shouldn't have considered additional evidence without giving the Assessing Officer a proper chance to comment on it. They said this evidence should only be allowed under specific circumstances mentioned in Rule 46A(1) (of Income Tax Rules, 1962).

On the flip side, the company argued that the CIT(A) did share the additional info with the Assessing Officer, who didn't object to it and even asked for it to be considered during the final decision.

Key Legal Precedents:

Interestingly, this case doesn't heavily rely on previous legal precedents. Instead, it focuses more on the procedural aspects and the interpretation of the facts presented. The judgment does mention Section 260A (of Income Tax Act, 1961), which is about appeals to the High Court, and Rule 46A(1) (of Income Tax Rules, 1962), which deals with producing additional evidence in appellate proceedings.

Judgement:

The High Court dismissed the tax department's appeal. Here's why:

1. They found that both the CIT(A) and the Tribunal had thoroughly examined the issues and reached consistent conclusions.

2. The court noted that the Tribunal is the final fact-finding authority, and the High Court's scope for interference is limited.

3. They rejected the tax department's argument about additional evidence, pointing out that the Assessing Officer had been given a chance to comment and hadn't objected.

4. The court found no errors in the Tribunal's findings on the genuineness of investors, accrued income, or loan transactions.

FAQs:

1. Q: Why did the High Court dismiss the appeal?

A: The court found no substantial question of law and agreed with the concurrent findings of the CIT(A) and Tribunal.

2. Q: What was the main issue with the additional evidence?

A: The tax department claimed it wasn't properly shared with the Assessing Officer, but the court found this argument to be incorrect.

3. Q: How important was the Tribunal's role in this case?

A: Very important! The High Court emphasized that the Tribunal is the final fact-finding authority, and its decisions carry significant weight.

4. Q: What does this case mean for taxpayers?

A: It highlights the importance of maintaining proper documentation and following correct procedures when dealing with tax authorities and appeals.

5. Q: Can the tax department appeal this decision further?

A: While the judgment doesn't mention it explicitly, typically, the next step would be to appeal to the Supreme Court if they choose to do so.

1. That Appellant-Principal Commissioner of Income Tax has filed instant appeal under Section 260A (of Income Tax Act, 1961) (for short ‘IT Act’ seeking quashing of order dated 03.02.2016 (Annexure A-3) passed by Ld. Income Tax Appellate Tribunal, Amritsar Bench, Amritsar (for short ‘Tribunal’) whereby appeal of the present appellant had been dismissed.

2. That the Respondent-Assessee is a colonizer. The Assessing Authority vide order dated 29.12.2011 framed assessment under Section 143(3) (of Income Tax Act, 1961) for the assessment year 2009-10 whereby income was assessed Rs.3,95,00,000/-. The Assessing Authority made additions on three counts namely:

i) Rs.1.65 Crores on account of failure of Assessee to prove identity and genuineness of the persons having introduced share capital and share premium.

ii) Rs.1.10 Crores on account of failure to account for accrued income @ Rs.10 Lakh per month from May’ 2008 to March’ 2009 from M/s Satya Developers Limited as per agreement.

iii) Rs.1.20 Crore on account of failure to prove capacity of the loan creditors as well as genuineness of transactions.

3. The Respondent-Assessee assailing aforesaid additions filed an appeal before Ld. CIT(A) who vide order dated 20.12.2012 allowed appeal of the Respondent-Assessee and deleted all the additions made by Assessing Authority. It is apt to notice here that Assessee furnished additional information/evidence before CIT (A) who supplied copy of said information to Assessing Authority while asking remand report. The Assessing Authority in its remand report did not object to the information filed by Assessee rather asked for the same to be considered at the time of disposal of the appeal.

4. Feeling dissatisfied, the Revenue filed an appeal before Tribunal who vide order dated 03.02.2016 dismissed appeal of the Revenue.The Tribunal while dismissing appeal of Department returned findings as below: “ 12. The ld. CIT(A) while giving relief to the assessee on account of share application money has relied upon the above judgments. He has not commented on the merits of the case. However, we have examined the issue from the angle of merits also. We find that the three shareholders from whom share capital money along with share premium has been collected are all Private Limited Companies which have been incorporated under the Companies Act and all these Companies are having PAN numbers and have filed their income tax returns. Therefore, there cannot be any doubt about the identity of these Companies.

13. As regards the creditworthiness of these companies, we find that these three companies had filed audited accounts and investment in the assessee company has been made duly reflected in their respective balance sheets. We find that the investments in the assessee-company has been out of share capital and reserves of the investing Companies. For example, the net worth of M/s. Dhir Management Consultants (P) Ltd., (one of the investing companies) as on 31.03.2009 as per balance sheet placed at paper book page 8 (in short ‘PB-8’) is Rs.99,34,843/- out of which it had made investments to the tune of Rs.75,45,930/- in various companies as is apparent from Schedule-VI of balance sheet placed at PB-9. The Schedule reflects the name of assessee company where the investment has been reflected to the tune of Rs.70,00,000/-. 14. Similar is the position with other investing company, M/s S.K.M. Securities (P) Ltd. The second investing company has net worth of Rs.1,01,05,370/- as on 31.3.2009, out of which Rs.65,00,000/- has been invested in the assessee company. This fact is verifiable from the copy of balance sheet of investing company placed at PB-13.

15. Similarly the third company M/s Singhal Securities (P) Ltd., as on 31.3.2009 had net worth of Rs.10,49,97,000/- out of which Rs.7,02,55,000/- has been invested in shares of various companies and which fact is verifiable from PB-22, where a copy of balance sheet as on 31.3.2009 is placed. The investment made in the assessee company is included in this total investment.

16. From the above facts and figures, the creditworthiness of the investing Companies is also proved.

17. As regards the genuineness of transactions, we find that the assessee company has received the share capital alongwith share premium amount through Banking channels and from the analysis of the Bank Accounts of the investing companies, we find that there were no cash deposits before investments in the assessee company except an amount of Rs.1,50,000/- and these companies had sufficient balance in their bank account to make investments in the assessee company. For example, in the case of M/s SKM Securities Pvt. Limited, the company had balance of Rs.35,28,860/- in its bank account with Indusind Bank as on 27.6.2008 out of which Rs.15,00,000/- was invested in the assessee company on 28.6.2008 and further the investing company had balance of Rs.50,28,835/- as on 10th July, 2008 out of which Rs.50,00.000/- has been invested in the assessee-company on 12th July, 2008. The analysis of bank account statement reveals that the deposit in the bank account before investments in the assessee company were all through Banking transactions. Therefore, the genuineness of transaction cannot be doubted.

18. As regards the investment made by M/s Dhir Management Consultants Pvt. Ltd., its bank statement is placed at PB-10. From the analysis of this bank account, we find that the assessee company had invested Rs.40,00,000/- on 10.6.2008 through RTGS and further Rs.30,00,000/- was invested on 13.6.2008 through RTGS and investing company had sufficient balance in its bank account. Similar is the case with bank account of M/s Singhal Securities Pvt. Ltd placed at PB 27-28, where the investing company had made an investment of Rs.30,00,000/- out of the available bank balance. The investing company had received an amount of Rs.30,00,500/- from one M/s. Tulika Securities on 5.6.2008 and out of this amount of Rs.30,00,000/- for investment was made in the assessee company. 18.1. Therefore, the above facts and figures not only the source of investments but the source of source has also been established. 19. In view of the above facts and findings, we find that all the three ingredients required for fulfillment of provisions of section 68 (of Income Tax Act, 1961) are met and therefore, the ld. CIT(A) has rightly deleted the addition made by the AO u/s 68 (of Income Tax Act, 1961). Accordingly, keeping in view the peculiar facts and circumstances of the case, Ground no. 1 (i) of the appeal is dismissed.

20. As regards Ground no. 1(ii), the ld. DR argued that per the agreement with M/s Satya Developers Pvt. Limited, the income had accrued to the assessee @ Rs. 10 lacs per month for 11 months and invited our attention to the agreement with M/s Satya Developers Pvt. Ltd.

21. The ld. Counsel for the assessee, on the other hand, submitted that the agreement with M/s Satya Developers Pvt. Ltd. was an exhaustive agreement containing 33 clauses and one of the conditions as per clause-14 says that if the delay is because of the force-majeure conditions, no compensation is payable. He submitted that the PUDA had not given possession for development of the property even till 11.9.2006 and therefore, the delay in the execution of the project work was beyond the control of the developer. The ld. Counsel for the assessee further submitted that from the balance sheet of the developer obtained by the AO by calling the information u/s 131 (of Income Tax Act, 1961), it can be seen that the developer had declared project, as work-in-progress and furthermore, he submitted that clause-14 of the collaboration agreement provides that the construction has to be completed within 24 months from the date of sanction of plan or handing over the possession, whichever is later. The ld. Counsel submitted that handing over of the possession itself was delayed, therefore, no compensation accrued to the assessee.

22. We find that the ld. CIT(A) has made a finding of fact that as per clause-14, the developer had to complete the project within 24 months from the date of sanction of plan or handing over possession, whichever is later excepting force majeure circumstances or any action of the Statutory Authority or Court orders. The clause-14 reproduced by the ld. CIT(A) at page 10 of his order states that period of 24 months shall be subject to force majeure conditions and in view of the facts, we hold that no compensation accrued to the assessee company as there was delay in handing over clear cut possession to the assessee company by PUDA, which delayed the completion of project. Moreover, we find that assessee had filed additional evidence before the ld. CIT(A) which was forwarded to the AO and the AO has not made any adverse comments on the additional evidence. In view of the above, we do not find any infirmity in the order of the ld. CIT(A).

23. In view of the above discussion, Ground no. 1(ii) is also dismissed.

24. As regards Ground no. 1(iii), the AO made addition u/s 68 (of Income Tax Act, 1961) on account of loan from M/s Golden Laminates Ltd. The ld. DR heavily relied upon the assessment order, whereas the ld. Counsel for the assessee relied upon the order of the ld. CIT(A). 25. In this respect, we find that the assessee had received a total loan of Rs.255 lakhs from M/s Golden Laminates Ltd., and the assessee had filed a confirmation from the M/s Golden Laminates Ltd., regarding advancing a loan of Rs.255 lakhs by them and the confirmation the date, cheque no. and other relevant information alongwith company’s PAN was also filed. The AO had accepted the loan of Rs.1.05 Crore as genuine and he has rejected the loan of Rs.1.20 Crore on the plea that the same does not appear in the bank statement of M/s Golden Laminates Ltd., whereas the ld. CIT(A) has made a finding of fact that the source of this Rs.1.20 Crore was from HDFC Bank and the ld. CIT(A) had also forwarded a copy of Bank Account of HDFC to AO for his comments. The AO in the remand report has not objected to the documents and has requested the ld. CIT(A) to consider the case while disposing of the appeal. The ld. CIT(A) has further made a finding of fact that in the statement of HDFC, all the entries relating to advancing of loan of Rs.1.20 Crores to assessee do appear. Therefore, keeping in view the facts and circumstances of the case, we do not find any force in the arguments of the ld. DR. In view of the above, ground no. 1(iii) is also dismissed.

26. In nutshell, the appeal filed by the Revenue is dismissed. ”

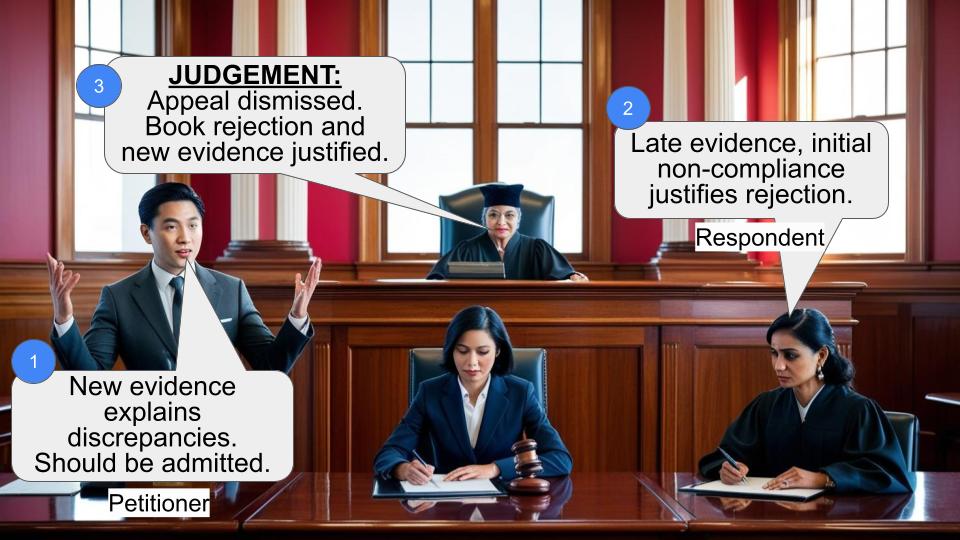

5. Ld. Counsel for the Appellant-Revenue vehemently contended that Ld. CIT (A) without granting opportunity to Assessing Authority to comment upon additional evidence; considered additional evidence which was not supplied to Assessing Authority inspite of proper opportunities to Assessee while framing assessment, thus CIT (A) as well Tribunal has wrongly allowed appeal of the Assessee. He further contended that there was no reason to consider additional evidence which could be considered only in case of circumstances mentioned in Rule 46A(1) (of Income Tax Rules, 1962).

6. Per contra counsel for the Respondent-Assessee contended that additional information was supplied to Assessing Authority by CIT (A) and Assessing Authority in its remand report did not dispute the additional information rather asked to consider at the time of disposal of the case, thus it is unfair on the part of department to raise a plea that Assessing Authority was not granted proper opportunity to comment upon additional information.

7. Having scrutinized record and heard arguments of both sides, we find that present appeal is bereft of merits and deserves to be dismissed.There are concurrent findings of First Appellate Authority as well as Tribunal. We are not oblivious of the fact that Tribunal is final fact finding authority and scope of interference of this Court lies in narrow compass.The core issue raised by Appellant is that Appellate Authority without recording reasons to entertain additional evidence and without granting proper opportunity to Assessing Authority while relying upon additionalinformation allowed appeal of the Assessee. Plea of Appellant is fallacious,in view of the fact that no such plea was raised before Tribunal apart from fact that remand report was sought from Assessing Authority and who in its report did not object to additional information rather asked to consider at the time of final disposal which vindicates stand of the Respondent-Assessee.The Revenue could be aggrieved had Appellate Authority not supplied additional evidence to Assessing Authority or some objection had been raised at that stage. Failing to object rather extending implied consent demolishes entire case of the Revenue. There is nothing in the order of Tribunal to show that Revenue raised objection of additional evidence before Tribunal. Thus, we do not find any merit in the argument of the Appellant.

8. Questions of i) genuineness of investors who introduced share capital and premium; ii) accrued income on account of delayed completion of project by M/s Satya Developers Limited; iii) capacity of persons from whom loan was borrowed and genuineness of transactions, have been considered at length by First Appellate Authority as well Tribunal. Both the Authorities below have returned categorical findings on each issue and counsel for Revenue has failed to point out any infirmity in fact or law warranting interference of this Court.

9. In view of our findings, we do not find that any question of law much less substantial question of law arises for our consideration. Accordingly present appeal is dismissed.

×

Similar Ripples

Questions

Tax Appeal Dismissed: High Court Upholds Tribunal's Decision in Favor of Assessee

Write your CommentSimilar Posts

Generic

- Reportdata/6284.pdf