Full News

Tax Appeal Dismissed: Reimbursement Deemed Capital Receipt, Not Income

Tax Appeal Dismissed: Reimbursement Deemed Capital Receipt, Not Income

The Commissioner of Income Tax (that's the tax department) filed an appeal against M/s. Sutherland Global Services Pvt. Ltd. (let's call them Sutherland). The main issue was about how to classify some money Sutherland received from another company. The tax folks thought it should be taxed as income, but Sutherland said it wasn't taxable. Long story short, the court sided with Sutherland and dismissed the tax department's appeal.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs M/s. Sutherland Global Services Pvt. Ltd. (High Court of Madras)

Tax Case Appeal No.305 of 2018

Date: 7th July 2020

Key Takeaways:

1. The court upheld previous decisions in similar cases involving the same company.

2. The tax department's failure to appeal earlier decisions played a crucial role.

3. Reimbursements for asset purchases used in business operations can be considered capital receipts, not taxable income.

Issue:

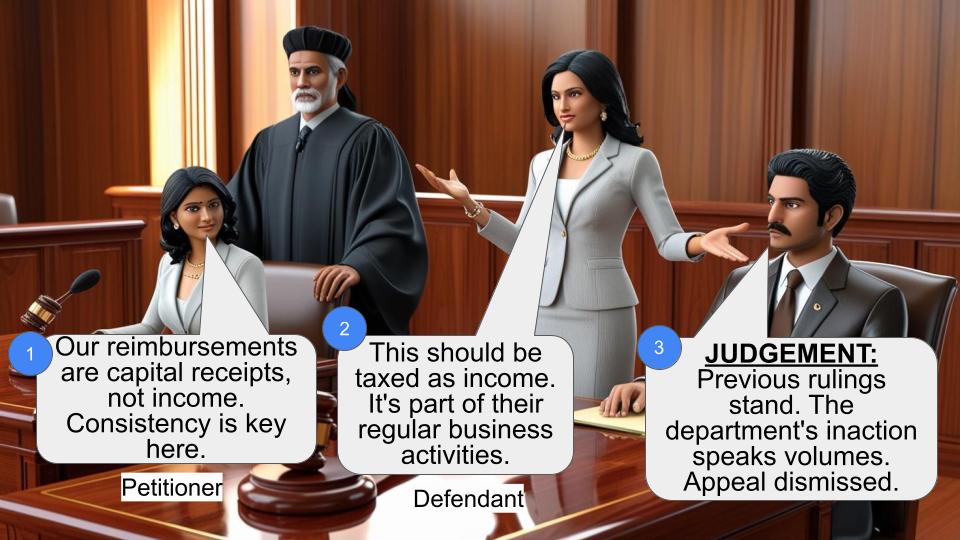

The main question here was: Should the excess amount Sutherland received as reimbursement from Symantec Corporation, USA for assets purchased and used for work be treated as "Capital Receipts" or as "Income from Other Sources"?

Facts:

- This case is about the Assessment Year 2005-06.

- Sutherland received some extra money from Symantec Corporation, USA as reimbursement for assets they bought and used for Symantec's work.

- The Assessing Officer (tax guy) said this extra money should be taxed as "Income from Other Sources".

- Sutherland disagreed and appealed.

- There were similar cases for the same company in Assessment Years 2006-07 and 2007-08 where the Income Tax Appellate Tribunal sided with Sutherland.

Arguments:

Tax Department's Side:

1. The extra money should be taxed as "Income from Other Sources".

2. This money wasn't from selling fixed assets but was received during regular business activities.

3. Sutherland itself had initially recorded this under "Other Income".

Sutherland's Side:

1. This money should be treated as "Capital Receipts", which aren't taxable.

2. Similar cases in previous years were decided in their favor.

Key Legal Precedents:

The court relied heavily on previous decisions made by the Income Tax Appellate Tribunal for the same company (Sutherland) in Assessment Years 2006-07 and 2007-08. These earlier decisions had treated similar reimbursements as capital receipts.

Judgement:

The court dismissed the tax department's appeal. Here's why:

1. The Commissioner of Income Tax (Appeals) had already partly allowed Sutherland's appeal, following decisions from similar cases in 2006-07 and 2007-08.

2. When that decision was made, the tax department hadn't appealed the earlier tribunal decisions, implying they had accepted those rulings.

3. The tax department didn't provide any evidence to the tribunal showing they had appealed those earlier decisions.

Given all this, the court felt the tax department couldn't maintain this appeal. They answered the questions of law against the tax department and dismissed the case without any costs.

FAQs:

1. Q: What does this decision mean for companies receiving reimbursements?

A: It suggests that reimbursements for asset purchases used in business operations might be treated as capital receipts rather than taxable income, but each case would depend on its specific facts.

2. Q: Why was the tax department's failure to appeal earlier decisions so important?

A: It implied that they had accepted those earlier rulings, making it harder for them to argue against similar treatment in this case.

3. Q: Could this decision apply to other companies in similar situations?

A: While it might be used as a reference, tax laws can be complex. Other companies would need to consult with tax professionals to understand how this might apply to their specific situations.

4. Q: What's the difference between "Capital Receipts" and "Income from Other Sources"?

A: Capital receipts generally aren't taxable as they're considered returns of capital, while income from other sources is typically taxable. The classification can significantly impact a company's tax liability.

5. Q: Does this mean the tax department can never challenge similar cases in the future?

A: Not necessarily. While this decision sets a precedent, the tax department could potentially challenge similar cases if they can distinguish them from this one or if there are changes in tax laws.

This appeal by the revenue is filed under Section 260A (of Income Tax Act, 1961) (the 'Act' for brevity), challenging the order passed by the Income Tax Appellate Tribunal 'A' Bench, Madras, in ITA No.658/Mds/2016 dated 28.12.2016 for the Assessment Year 2005-06.

2. The appeal was admitted on 04.12.2019 on the following Substantial Questions of Law:

“(i) Whether on the facts and in the circumstances of the case, Tribunal was correct in holding that the excess amount received by the assessee on reimbursement received from M/s.Symantec Corporation, USA on account of assets purchased and used by the assessee for the work towards the payee company as “Capital Receipts” as against the stand of the Assessing Officer that it was “Income from other Sources”?

(ii) Whether on the facts and in the circumstances of the case and in law, the Tribunal has erred in not considering the fact the above sum is not due to any sale of fixed assets exclusively and that it is received only during the course of business activity which the assessee itself credited under the head “Other Income”?”

3. We have heard Mr.J.Narayanasamy, learned Senior Standing Counsel for the appellant/Revenue and Mr.N.V.Balaji, learned counsel for the respondent/assessee.

4. After elaborately hearing the learned counsel for the parties, we find that the revenue cannot sustain this appeal for more than one reason.

Firstly, the Commissioner of Income Tax (Appeals), while deciding the appeal petition filed by the assessee against the order of assessment dated 31.03.2013, partly allowed the assessee's appeal by following the decision in the assessee's own case in respect of an identical transaction for the Assessment Years 2006-07 and 2007-08. It was pointed out that since the facts of the case are identical to the Assessment Years referred above, the CIT (A) followed the order of the tribunal.

5. It is evident that as on the date when the CIT(A) allowed the assessee's appeal by an order dated 17.12.2015, no appeal was preferred before the Division Bench of this Court, questioning the correctness of the order passed by the tribunal dated 26.07.2012, for the Assessment Year 2006-07 or 08.03.2013, for the Assessment Year 2007-08. Had an appeal been preferred, revenue could have taken a stand before the CIT(A) that the decisions of the Income Tax Appellate Tribunal dated 26.07.2012 and 08.03.2013, have not been accepted by the Department and not attained finality. Since no such stand was taken, it is clear that the decisions have been accepted by the Department. Nevertheless, for the Assessment Year under consideration, the revenue thought it fit to file an appeal before the tribunal. The tribunal took note of its earlier decisions, referred above and dismissed the appeal. Even before the tribunal, the revenue did not produce any material to show that the orders passed by the tribunal for the Assessment Years 2006-07 and 2007-08 were taken on appeal before the Division Bench of this Court.

6. Therefore, we are of the considered view that the revenue cannot maintain this appeal. For the above reasons the Tax Case Appeal is dismissed. The Substantial Questions of Law are answered against the revenue. No Costs.

T.S.SIVAGNANAM, J.

AND

V.BHAVANI SUBBAROYAN, J.

×

Similar Ripples

Questions

Tax Appeal Dismissed: Reimbursement Deemed Capital Receipt, Not Income

Write your CommentSimilar Posts

Generic

- Reportdata/6231.pdf