Tax Deduction at Source: Firms Deemed Defaulters for Non-Compliance

Full News

Tax Deduction at Source: Firms Deemed Defaulters for Non-Compliance

Tax Deduction at Source: Firms Deemed Defaulters for Non-Compliance

This case where three partnership firms appealed against an order from the Income Tax Appellate Tribunal. These firms were accepting loans as deposits and paying interest, but they didn't deduct tax on this interest as required by law. The tax department said, "Hey, you're in default!" The firms fought this at various levels, but ultimately, the High Court sided with the tax department.

Get the full picture - access the original judgement of the court order here

Case Name:

M/s.Popular Dealers (Rep. by its Managing Partner, Thomas Daniel) and Ors. Vs Income Tax Officer (Tds) (High Court of Kerala)

ITA. No.209 of 2019

Date: 9th June 2020

Key Takeaways:

1. Firms paying interest must deduct tax at source, or they'll be considered defaulters.

2. The burden of proof is on the deductor to show the payee has paid the tax.

3. Partnerships aren't separate legal entities; partners are jointly liable for the firm's obligations.

Issue:

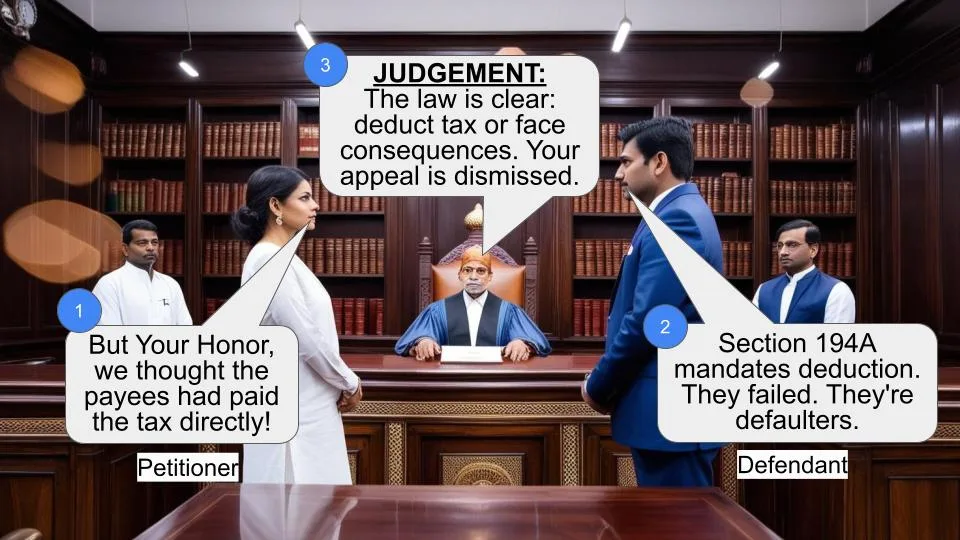

The main question here is: Can these firms be treated as "assessees in default" for not deducting tax at source when paying interest, even if they didn't confirm whether the payee (the person receiving the interest) had paid the tax directly?

Facts:

- Three partnership firms were accepting loans as deposits and paying interest.

- They were required to deduct tax on this interest under Section 194A (of Income Tax Act, 1961) but didn't do so.

- The case covers assessment years 2013-14 to 2016-17.

- The Assessing Officer treated them as "assessees in default" under Section 201 (of Income Tax Act, 1961).

- The firms appealed this decision at various levels but lost each time.

Arguments:

The firms argued:

1. The tax department should have checked if the payee paid the tax directly before declaring them defaulters.

2. The authorities didn't correctly identify who was responsible for deducting the tax.

The tax department countered:

1. Section 194A (of Income Tax Act, 1961) clearly requires the person paying interest to deduct tax.

2. Failure to do so automatically makes them defaulters under Section 201 (of Income Tax Act, 1961).

Key Legal Precedents:

1. CIT v. R.M. Chidambaram Pillai (1977) 1 SCC 431:

This case established that a partnership isn't a legal person and has no separate existence from its partners.

2. Jagran Prakashan Ltd. v. Deputy Commissioner of Income-tax (TDS) [2012 (21) Taxman.com.489 (Allahabad)]:

The court noted this case but said it wasn't applicable here because the law had changed since then.

Judgement:

The High Court dismissed the appeals, agreeing with the tax department. They said:

1. Section 194A (of Income Tax Act, 1961) clearly requires tax deduction at source for interest payments.

2. Section 201 (of Income Tax Act, 1961) automatically treats those who fail to deduct as defaulters.

3. The firms didn't provide proof that the payees had paid the tax, as required by the law.

4. It's okay to hold the firm and its partners liable because a partnership isn't a separate legal entity.

FAQs:

Q1: Does this mean all interest payments need tax deduction at source?

A1: Not all. Section 194A(3) (of Income Tax Act, 1961) lists some exceptions, but these firms didn't fall under any of them.

Q2: Can a firm avoid being a defaulter if the payee has paid the tax?

A2: Yes, but the firm needs to provide a certificate from an accountant proving this.

Q3: Why were the partners held liable along with the firm?

A3: Because a partnership isn't a separate legal entity, so its liabilities extend to the partners.

Q4: Does this judgment apply to all businesses?

A4: This specifically applies to those required to deduct tax at source under Section 194A (of Income Tax Act, 1961).

Q5: What's the main takeaway for businesses from this case?

A5: If you're required to deduct tax at source, make sure you do it. If you don't, you could be treated as a defaulter, even if the other party pays the tax directly.

1. Three different assessees, which are partnership firms, have filed the appeals against a common order of the Income-tax Appellate Tribunal, Cochin Bench. The orders relate to the assessment years 2013-14 to 2016-17. A common question is raised in all these appeals and hence they are heard and disposed of together.

2. The assessees have been accepting loans in the form of deposits and paying interest on such borrowings. Even though the assesses were required to deduct tax on the interest paid under Section 194A (of Income Tax Act, 1961), they have failed to do so. The Assessing Officer proceeded to assess the appellants treating them as assessees in default under Section 201 (of Income Tax Act, 1961). Even though the appellants challenged the assessment orders before the Appellate Authority, the same were dismissed and further appeals before the Income-Tax Appellate Tribunal have also been dismissed as per the orders impugned in these appeals.

3. Heard Sri Harisankar V.Menon on behalf of the appellants and Sri Christopher Abraham on behalf of the respondents.

4. The main contention of the counsel for the appellants is that the Assessing Authority ought to have confirmed the failure of the 'payee-assessee' to pay the tax directly as per Section 191 (of Income Tax Act, 1961), before declaring the 'deductor-assessee' as an assessee-in-default under Section 201 (of Income Tax Act, 1961). It was also contended that the authorities have failed to fix the liability on the correct person who is responsible for deduction of tax at source, as the firms have many Managers, who were actually responsible for the same. According to the counsel, the fixing of liability on the assessee and its partners as assessee-in-default was hence not in accordance with law. The counsel for the Department on the other hand contended that Section 194A (of Income Tax Act, 1961) obliges the person who is paying the interest to deduct income-tax thereon at the rates in force and a failure to do so will immediately lead, to the said person who is liable to deduct, being deemed to be an assessee-in-default in respect of such tax.

5. The following questions of law arise for consideration in these appeals:

(a) Whether on the facts and in the circumstances of the case, has not the Tribunal erred in holding that burden of proof lies on the appellant in terms of the first proviso to Section 201(1) (of Income Tax Act, 1961)?

(b) Whether on the facts and circumstances of the case the assessment impugned herein is against the principles laid down in Jagran Prakash Ltd. v. DCIT (TDS) 345 ITR 288?

(c) Ought not the learned Tribunal have held that Section 201 (of Income Tax Act, 1961) is found on the instance when the deductee/payee fails to pay the tax on the payment made by the deductor or fails to show the same in the return filed?

(d) Ought not the learned Tribunal have held that the assessing authority passed a vague order in respect of liability of the appellant along with Principal Officer, partner and Managing Partner to deduct tax U/s.194A (of Income Tax Act, 1961)?

(e) Are not the findings of the learned Tribunal perverse and against the provisions of the Income Tax Act, 1961?

6. The relevant portions of Sections 194A and 201 are extracted below:

“194A. Interest other than “Interest on securities”. (1) Any person, not being an individual or a Hindu undivided family, who is responsible for paying to a resident any income by way of interest other than income by way of interest on securities, shall, at the time of credit of such income to the account of the payee or at the time of payment thereof in cash or by issue of a cheque or draft or by any other mode, whichever is earlier, deduct income-tax thereon at the rates in force .

(2) Omitted by the Finance Act, 1992 w.e.f. 1.6.1992.

(3) The provisions of sub-section (1) shall not apply—

(i) where the amount of such income or, as the case may be, the aggregate of the amounts of such income credited or paid or likely to be credited or paid during the financial year by the person referred to in sub-section (1) to the account of, or to, the payee, does not exceed—

(a) forty thousand rupees, where the payer is a banking company to which the Banking Regulation Act, 1949 (10 of 1949) applies (including any bank or banking institution, referred to in section 51 (of Income Tax Act, 1961) of that Act);

(b) forty thousand rupees, where the payer is a co-operative society engaged in carrying on the business of banking;

(c) forty thousand rupees, on any deposit with post office under any scheme framed by the Central Government and notified by it in this behalf; and

(d) five thousand rupees in any other case.” 201. Consequences of failure to deduct or pay.

(1) Where any person, including the principal officer of a company,—

(a) who is required to deduct any sum in accordance with the provisions of this Act; or

(b) referred to in sub-section (1A) of section 192 (of Income Tax Act, 1961), being an employer,

does not deduct, or does not pay, or after so deducting fails to pay, the whole or any part of the tax, as required by or under this Act, then, such person, shall, without prejudice to any other consequences which he may incur, be deemed to be an assessee-in-default in respect of such tax.

Provided that any person, including the principal officer of a company, who fails to deduct the whole or any part of the tax in accordance with the provisions of this Chapter on the sum paid to a payee or on the sum credited to the account of a payee shall not be deemed to be an assessee-in-default in respect of such tax if such payee-

(i) has furnished his return of income under section 139 (of Income Tax Act, 1961)

(ii) has taken into account such sum for computing income in such return of income; and

(iii) has paid the tax due on the income declared by him in such return of income, and the person furnishes a certificate to this effect from an accountant in such form as may be prescribed.”

7. Section 194A (of Income Tax Act, 1961) is categoric when it says that any person who is responsible for paying to a resident any income by way of interest other than income by way of interest on securities, shall deduct income-tax thereon at the rates in force, at the time of credit of such income to the account of the payee. It can be seen from sub-section (3) of Section 194A (of Income Tax Act, 1961) that the Legislature has carved out the cases in which such deduction need not be made. Admittedly, the case of the appellants does not come under any of the categories identified in sub-section (3). As such, the appellants cannot contend that they are not liable to deduct the tax at the time of payment of the interest income to its customers. A reading of Section 201 (of Income Tax Act, 1961), again, clearly shows that the failure to deduct such tax will entail the consequence of such person being deemed to be an assessee-in-default in respect of such tax. The first proviso to Section 201 (of Income Tax Act, 1961) was added by the Finance Act, 2012 with effect from 01.07.2012. As per the proviso, a person who fails to deduct such tax shall not be deemed to be an assessee-in-default, if it satisfies the conditions stated in the proviso.

As per the proviso, the payee in such cases ought to have furnished his return of income under Section 139 (of Income Tax Act, 1961), taking into account such sum for computing income in such return of income, and, paid the tax due on the income declared by him in such return of income. It is also provided that the assessee (deductor) should furnish a certificate to this effect from an Accountant in such form, as may be prescribed. Admittedly, the appellants have not furnished any such certificate as required by the Statute. Having not complied with the conditions laid down in Section 201 (of Income Tax Act, 1961), the appellants are not entitled to contend that they should not be treated as assessee-in-default under Section 201 (of Income Tax Act, 1961).

8. The appellants have a contention that the Assessing Authority ought to have confirmed the failure of the payee-assessee to pay tax directly as per Section 191 (of Income Tax Act, 1961) before declaring the appellants as assessee-in-default. Section 191 (of Income Tax Act, 1961) is extracted below:

“191. Direct payment. In the case of income in respect of which provision is not made under this Chapter for deducting income-tax at the time of payment, and in any case where income-tax has not been deducted in accordance with the provisions of this Chapter, income-tax shall be payable by the assessee direct.

Explanation.—For the removal of doubts, it is hereby declared that if any person including the principal officer of a company,—

(a) who is required to deduct any sum in accordance with the provisions of this Act; or

(b) referred to in sub-section (1A) of section 192 (of Income Tax Act, 1961), being an employer, does not deduct, or after so deducting fails to pay, or does not pay, the whole or any part of the tax, as required by or under this Act, and where the assessee has also failed to pay such tax directly, then, such person shall, without prejudice to any other consequences which he may incur, be deemed to be an assessee-in-default within the meaning of sub-section (1) of section 201 (of Income Tax Act, 1961), in respect of such tax.”

Section 191 (of Income Tax Act, 1961) only says that in case of failure to deduct income-tax at the time of payment, income-tax shall be payable by the assessee direct. The Explanation to the Section says that if a person does not deduct the tax as required under the Act and where the assessee has also failed to pay such tax directly, then such person shall without prejudice to any other consequences which he may incur, be deemed to be an assessee-in-default within the meaning of sub-section (1) of Section 201 (of Income Tax Act, 1961). It can thus be seen that there is no requirement under the Statute that the Assessing Officer should ensure whether the payee has directly paid tax before declaring the appellants as assessee-in-default. As a matter of fact, the appellants by operation of Section 201 (of Income Tax Act, 1961) will be deemed to be assessee-in-default, even without any such declaration by the Assessing Officer.

9. The counsel for the appellants places reliance on the judgment of the High Court of Allahabad in Jagran Prakashan Ltd. v. Deputy Commissioner of Income-tax (TDS) reported in [2012 (21) Taxman.com.489 (Allahabad) in support of his contention. It can be seen that the judgment was rendered in a case which relates to the assessment years 2009-10 and 2010-11. The proviso to Section 201 (of Income Tax Act, 1961) came into force only in 2012. As such, no reliance can be placed on the above judgment, since the statutory provision itself has undergone a change in the relevant assessment year and the Section as it stood at the time action was taken against the appellants, created a fiction by deeming such persons who defaulted in deducting tax at the time of payment of interest, as assessee-in- default. The burden to prove that the payee-assessee had paid the tax, which the assessee-deductor failed to deduct was placed on the latter; by production of a certificate from the Accountant. The questions (a) to (c) are thus answered against the assessee and in favour of the Revenue.

10. The appellants have a further contention that the orders of the authorities are vague in the sense that it does not fix the liability to pay the tax on the correct person. According to the appellants, the authorities ought not to have fixed the liability on the assessee and its partners and thereafter issued demand only against the Managing Director. We do not find anything illegal or inappropriate in such direction. In CIT v. R.M. Chidambaram Pillai reported in (1977) 1 SCC 431, the Hon'ble Supreme Court observed as follows:-

“5. First principles plus the bare text of the statute furnish the best guidelight to understanding the message and- meaning of the provisions of law. Thereafter, the sophisticated exercises in precedents and booklore. Here the first thing that we must grasp is that a firm is not a legal person even though it has some attributes of personality. Partnership is a certain relation between persons, the product of agreement to share the profits of a business. “Firm” is a collective noun, a compendious expression to designate an entity, not a person. In income tax law a firm is a unit of assessment, by special provisions, but is not a full person; which leads to the next step that since a contract of employment requires two distinct persons viz. the employer and the employee, there cannot be a contract of service, in strict law, between a firm and one of its partners.”

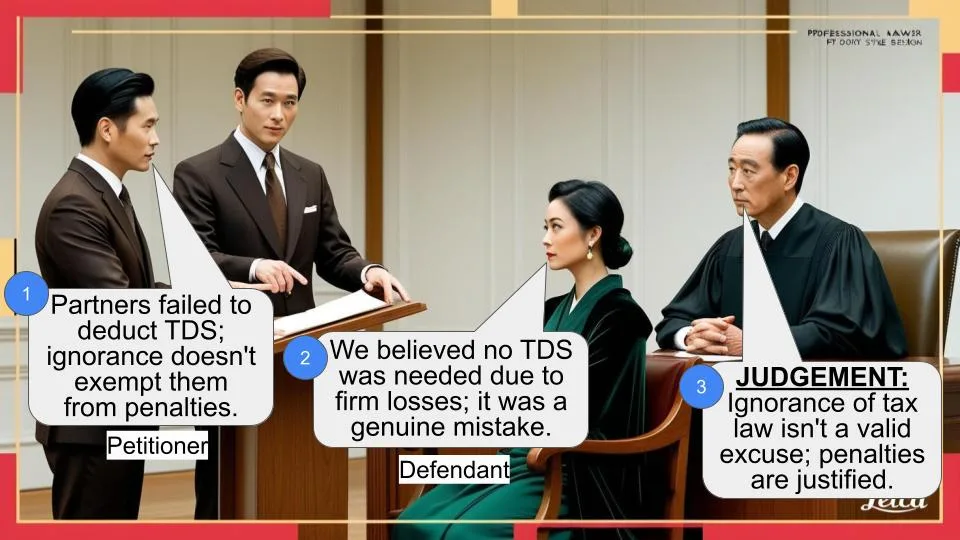

It is settled law that a partnership is neither a natural person nor a juristic person. It has no separate existence than its partners. The liability of a partnership firm is the liability of its partners. As such, fixing the liability of the firm on its partners can never be held to be illegal. In fact, it necessarily has to be fixed on the partners. In the light of the legal nature of a partnership firm, a demand raised on the Managing Partner can never be visualised as a wrong fixation of liability. It can only be seen as a demand made on the person who is managing the affairs of the firm, for and on behalf of all its partners. Such a demand does not in any way amount to a conclusion that the claim against the other partners has been given up, since the liability of the partners is joint and several.

We do not find any perversity in the findings of the Appellate Tribunal. The questions (d) and (e) raised in the appeal are answered against the assessee and in favour of the Revenue. The appeals are dismissed, however, without any order as to costs.

Sd/-

K. VINOD CHANDRAN

JUDGE

Sd/-

T.R. RAVI JUDGE

APPENDIX OF ITA 209/2019

PETITIONER'S/S EXHIBITS:

ANNEXURE A COPY OF ORDER ISSUED BY THE 1ST RESPONDENT FOR THE YEAR 2013-14 DATED 17.05.2016.

ANNEXURE B COPY OF ORDER ISSUED BY THE COMMISSIONER OF INCOME TAX (APPEALS), KOTTAYAM DATED 06.04.2018.

ANNEXURE C COPY OF ORDER IN ITA NO. 329/COCH/2018 FOR THE YEAR 2013-14 ISSUED BY THE INCOME TAX APPELLATE TRIBUNAL, COCHIN BENCH, COCHIN DATED 18.02.2019.

APPENDIX OF ITA 210/2019

PETITIONER'S/S EXHIBITS:

ANNEXURE A COPY OF ORDER ISSUED BY THE 1ST RESPONDENT FOR THE YEAR 2013-14 DATED 17.05.2016.

ANNEXURE B COPY OF ORDER ISSUED BY THE COMMISSIONER OF INCOME TAX (APPEALS), KOTTAYAM DATED 06.04.2018.

ANNEXURE C COPY OF ORDER IN ITA NO.321/COCH/2018 FOR THE YEAR 2013-14 ISSUED BY THE INCOME TAX APPELLATE TRIBUNAL, COCHIN BENCH, COCHIN DATED 18.02.2019.

APPENDIX OF ITA 212/2019

PETITIONER'S/S EXHIBITS:

ANNEXURE A COPY OF ORDER ISSUED BY THE 1ST RESPONDENT FOR THE YEAR 2013-14 DATED 17.05.2016.

ANNEXURE B COPY OF ORDER ISSUED BY THE COMMISSIONER OF INCOME TAX (APPEALS), KOTTAYAM, DATED 06.04.2018.

ANNEXURE C COPY OF ORDER IN ITA.NO.325/COCH/2018 FOR THE YEAR 2013-14 ISSUED BY THE INCOME TAX APPELLATE TRIBUNAL, COCHIN BENCH, COCHIN DATED 18.02.2019.

APPENDIX OF ITA 220/2019

PETITIONER'S/S EXHIBITS:

ANNEXURE A COPY OF ORDER ISSUED BY THE IST RESPONDENT FOR THE YEAR 2016-17 DATED 12.8.2016

ANNEXURE B COPY OF ORDER ISSUED BY THE COMMISSIONER OF INCOME TAX (APPEALS), KOTTAYAM DATED 6.4.2018.

ANNEXURE C COPY OF ORDER IN ITA NO.324/COCH/2018 FOR THE YEAR 2016-17 ISSUED BY THE INCOME TAX APPELLATE TRIBUNAL, COCHIN BENCH, COCHIN DATED 18.2.2019.

APPENDIX OF ITA 221/2019

PETITIONER'S/S EXHIBITS:

ANNEXURE A COPY OF ORDER ISSUED BY THE IST RESPONDENT FOR THE YEAR 2016-17 DATED 31.05.2016.

ANNEXURE B COPY OF ORDER ISSUED BY THE COMMISSIONER OF INCOME TAX (APPEALS), KOTTAYAM DATED 6.4.2018.

ANNEXURE C COPY OF ORDER IN ITA NO.328/COCH/2018 FOR THE YEAR 2016-17 ISSUED BY THE INCOME TAX APPELLATE TRIBUNAL, COCHIN BENCH, COCHIN DATED 18.2.2019.

APPENDIX OF ITA 222/2019

PETITIONER'S/S EXHIBITS:

ANNEXURE A COPY OF ORDER ISSUED BY THE IST RESPONDENT FOR THE YEAR 2015-16 DATED 31.5.2016.

ANNEXURE B COPY OF ORDER ISSUED BY THE COMMISSIONER OF INCOME TAX (APPEALS), KOTTAYAM DATED 6.4.2018.

ANNEXURE C COPY OF ORDER IN ITA NO.323/COCH/2018 FOR THE YEAR 2015-16 ISSUED BY THE INCOME TAX APPELLATE TRIBUNAL, COCHIN BENCH, COCHIN DATED 18.2.2019.

APPENDIX OF ITA 224/2019

PETITIONER'S/S EXHIBITS:

ANNEXURE A COPY OF ORDER ISSUED BY THE 1ST RESPONDENT FOR THE YEAR 2015-16 DATED 31.05.2016.

ANNEXURE B COPY OF ORDER ISSUED BY THE COMMISSIONER OF INCOME TAX (APPEALS), KOTTAYAM DATED 06.04.2018.

ANNEXURE C COPY OF ORDER IN ITA NO.331/COCH/2018 FOR THE YEAR 2015-16 ISSUED BY THE INCOME TAX APPELLATE TRIBUNAL, COCHIN BENCH, COCHIN DATED 18.02.2019.

APPENDIX OF ITA 226/2019

PETITIONER'S/S EXHIBITS:

ANNEXURE A COPY OF ORDER ISSUED BY THE 1ST RESPONDENT FOR THE YEAR 2014-15 DATED 23.05.2016.

ANNEXURE B COPY OF ORDER ISSUED BY THE COMMISSIONER OF

INCOME TAX(APPEALS) KOTTAYAM DATED 06.04.2018.

ANNEXURE C COPY OF ORDER IN ITA NO.322/COCH/2018, FOR THE YEAR 2014-15 ISSUED BY THE INCOME TAX APPELLATE TRIBUNAL, COCHIN BENCH, COCHIN DATED 18.02.2019.

APPENDIX OF ITA 227/2019

PETITIONER'S/S EXHIBITS:

ANNEXURE-A COPY OF ORDER ISSUED BY THE 1ST RESPONDENT FOR THE YEAR 2014-15 DATED 23.05.2016

ANNEXURE-B COPY OF ORDER ISSUED BY THE COMMISSIONER OF INCOME TAX (APPEALS), KOTTAYAM DATED 06.04.2018

ANNEXURE-C COPY OF ORDER IN ITA NO. 326/COCH/2018 FOR THE YEAR 2014-15 ISSUED BY THE INCOME TAX APPELLATE TRIBUNAL, COCHIN BENCH, COCHIN DATED 18.02.2019

APPENDIX OF ITA 230/2019

PETITIONER'S/S EXHIBITS:

ANNEXURE A COPY OF ORDER ISSUED BY THE 1ST RESPONDENT FOR THE YEAR 2014-15 DATED 23.05.2016

ANNEXURE B COPY OF ORDER ISSUED BY THE COMMISSIONER OF INCOME TAX(APPEALS), KOTTAYAM DATED 06.04.2018

ANNEXURE C COPY OF ORDER IN ITA NO.330/COCH/2018 FOR THE YEAR 2014-15 ISSUED BY THE INCOME TAX APPELLATE TRIBUNAL, COCHIN BENCH, COCHIN DATED 18.02.2019.

APPENDIX OF ITA 233/2019

PETITIONER'S/S EXHIBITS:

ANNEXURE A COPY OF ORDER ISSUED BY THE 1ST RESPONDENT OF THE YEAR 2015-16 DATED 31.05.2016

ANNEXURE B COPY OF ORDER ISSUED BY THE COMMISSIONER OF INCOME TAX(APPEALS), KOTTAYAM DATED 06.04.2018

ANNEXURE C COPY OF ORDER IN ITA NO.327/COCH/2018 FOR THE YEAR 2015-16 ISSUED BY THE INCOME TAX APPELLATE TRIBUNAL, COCHIN BENCH, COCHIN DATED 18.02.2019

APPENDIX OF ITA 234/2019

PETITIONER'S/S EXHIBITS:

ANNEXURE A COPY OF ORDER ISSUED BY THE 1ST RESPONDENT FOR THE YEAR 2016-17 DATED 12.08.2016.

ANNEXURE B COPY OF ORDER ISSUED BY THE COMMISSIONER OF INCOME TAX (APPEALS), KOTTAYAM DATED 06.04.2018.

ANNEXURE C COPY OF ORDER IN ITA NO.332/COCH/2018 FOR THE YEAR 2016-17 ISSUED BY THE INCOME TAX APPELLATE TRIBUNAL, COCHIN BENCH, COCHIN DATED 18.02.2019.

×

Similar Ripples

Questions

Tax Deduction at Source: Firms Deemed Defaulters for Non-Compliance

Write your CommentSimilar Posts

Generic

- Reportdata/5955.pdf