Tax Deduction Dispute: Court Upholds CIT's Revision Power in Section 10B (of In…

Full News

Tax Deduction Dispute: Court Upholds CIT's Revision Power in Section 10B (of Income Tax Act, 1961) Case

Tax Deduction Dispute: Court Upholds CIT's Revision Power in Section 10B (of Income Tax Act, 1961) Case

This case involves Sesa Starlite Limited (the Appellant-Assessee) and the Commissioner of Income Tax (CIT). The dispute centers around the CIT's use of revision powers under Section 263 (of Income Tax Act, 1961) to review a deduction allowed under Section 10B (of Income Tax Act, 1961). The High Court ultimately upheld the CIT's action, dismissing the Appellant's appeal.

Get the full picture - access the original judgement of the court order here

Case Name:

Sesa Starlite Limited Vs Commissioner of Income Tax (High Court of Bombay)

Tax Appeals No.27 of 2015 & 28 of 2015

Date: 2nd November 2020

Key Takeaways:

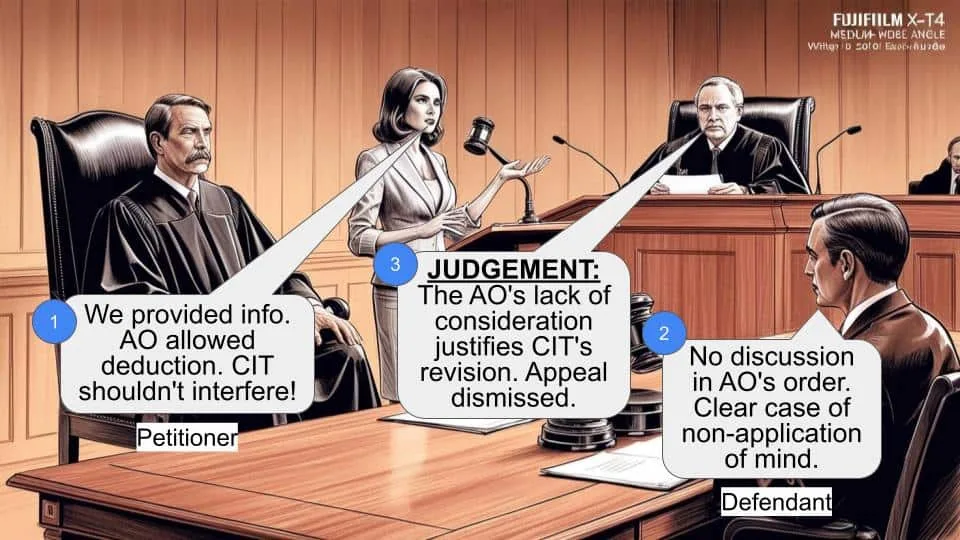

1. The CIT can exercise revision powers when an Assessing Officer (AO) fails to properly consider relevant issues.

2. Mere calling for information is not equivalent to applying mind to that information.

3. An order can be considered erroneous if passed without application of mind.

4. The distinction between 'no consideration' and 'inadequate consideration' is crucial in determining the validity of revision powers.

Issue:

Whether the Commissioner of Income Tax (CIT) could consider the assessment order passed by the Assessing Officer (AO) under section 143(3) (of Income Tax Act, 1961), for the assessment year 2006-2007, on the issue of claim for deduction allowed to the Appellant under Section 10-B (of Income Tax Act, 1961), as erroneous and prejudicial to the interest of the revenue, within the meaning of section 263 (of Income Tax Act, 1961)?

Facts:

1. The Appellant filed its original return for AY 2006-07 on 30/11/2006, declaring income of Rs.786,78,62,697/- without claiming any deduction under Section 10B (of Income Tax Act, 1961).

2. A revised return was filed on 29/3/2008, claiming deduction under Section 10B (of Income Tax Act, 1961).

3. The AO sought information from the Assessee regarding the 10B claim through communications dated 16/9/2009 and 2/12/2009.

4. The Assessee responded on 28/10/2009 and 7/12/2009.

5. The AO completed the assessment on 23/12/2009, allowing the 10B deduction without discussing it in the order.

6. On 14/2/2012, the CIT issued a notice invoking Section 263 (of Income Tax Act, 1961) to revise the AO's order.

7. The CIT set aside the AO's order on 29/3/2012 and directed a fresh assessment.

8. The Assessee appealed to the Income Tax Appellate Tribunal (ITAT), which dismissed the appeal on 18/7/2014.

Arguments:

Appellant's Arguments:

1. The AO had applied his mind and allowed the 10B deduction after due consideration.

2. The CIT lacked jurisdiction to interfere with a plausible view taken by the AO.

3. The ITAT had allowed similar deductions for subsequent years.

4. The CIT's notice was based on an SFIO report that was later withdrawn.

Revenue's Arguments:

1. There was no discussion or consideration of the 10B deduction in the AO's order.

2. This was a case of 'no consideration' rather than 'inadequate consideration'.

3. The AO failed to apply his mind to the information provided by the Assessee.

Key Legal Precedents:

1. Commissioner of Income Tax vs. Max India Ltd.

2. CIT vs. Vodafone Essar South Ltd.

3. Malabar Industrial Co. Ltd. vs. Commissioner of Income Tax

4. CIT vs. Gabriel India Ltd.

5. Rampyari Devi Saraogi vs. CIT

Judgement:

The High Court dismissed the Appellant's appeal, ruling in favor of the Revenue. Key points:

1. The court found that the AO had not applied his mind to the information provided by the Assessee.

2. This was a case of 'no consideration' rather than 'inadequate consideration'.

3. The CIT was justified in exercising revision powers under Section 263 (of Income Tax Act, 1961).

4. The court emphasized that merely calling for information is not equivalent to considering it.

FAQs:

Q1: What is the difference between 'no consideration' and 'inadequate consideration'?

A1: 'No consideration' means the AO didn't look at the information at all, while 'inadequate consideration' means the AO looked at it but didn't examine it thoroughly enough.

Q2: Can the CIT revise an order if the AO has taken a plausible view?

A2: Generally, no. If the AO has taken one of two possible views, the CIT shouldn't interfere just because they disagree.

Q3: Does this judgment mean all Section 10B (of Income Tax Act, 1961) deductions will be disallowed?

A3: No, it means each case must be properly examined on its merits by the AO.

Q4: What should taxpayers learn from this case?

A4: It's crucial to ensure that all claims for deductions are properly substantiated and that the AO clearly considers and addresses them in the assessment order.

Q5: Can the Assessee still claim the Section 10B (of Income Tax Act, 1961) deduction?

A5: Yes, the case has been sent back for fresh assessment, so the Assessee can present their case again to the AO.

Heard Mr. Pardiwalla, learned Senior Advocate along with Mr. Pranav Kakodkar for the Appellant-Assessee in both the Appeals and Ms. Susan Linhares, learned Standing Counsel for the Income Tax Department for the Respondent in both the Appeals.

2. The learned Counsel for the parties state that both these Appeals can be disposed of by a common Judgment and Order, since the issue involved in both these Appeals is the same, except that Tax Appeal No.28/2015 relates to the Assessment Year 2006-07 and Tax Appeal No.27/2015 relates to the Assessment Year 2007-08. The learned Counsel for the parties state that Tax Appeal No.28/2015 be treated as the lead matter.

3. Tax Appeal No.28/2015 was admitted on 30th April, 2015, on the following substantial question of law:

Whether, on the facts and circumstances of the case, the learned Commissioner of Income Tax (CIT) could have considered that the assessment order passed by the A.O. under section 143(3) (of Income Tax Act, 1961), for the assessment year 2006-2007, on the issue of claim for deduction allowed to the Appellant under Section 10-B (of Income Tax Act, 1961), was erroneous in so far as it was prejudicial to the interest of the revenue, within the meaning of section 263 (of Income Tax Act, 1961) ?

4. The Appellant-Assessee filed its original return of income on 30/11/2006 under Section 139 (of Income Tax Act, 1961) (IT Act) for the Assessment Year 2006-07, declaring income of Rs.786,78,62,697/- and it is pertinent to note that in filing this original return, the Assessee did not claim any deduction under Section 10B (of Income Tax Act, 1961).

5. Thereafter, the Assessee filed revised return of income on 29/3/2008 under Section 139(5) (of Income Tax Act, 1961) for the same Assessment Year. This time, the Assessee claimed deduction under Section 10B (of Income Tax Act, 1961).

6. The Assessing Officer (AO), vide communications dated 16/9/2009 and 2/12/2009, called for detailed information from the Assessee, inter alia, relating to the claim for deduction under Section 10B (of Income Tax Act, 1961) in the revised returns. By responses dated 28/10/2009 and 7/12/2009, the Assessee responded to the aforesaid communications.

7. The AO vide Assessment Order dated 23/12/2009, completed the assessment under Section 143(3) (of Income Tax Act, 1961). Although there is no discussion in the assessment order about the claim for deduction under Section 10B (of Income Tax Act, 1961), the AO accepted the Assessee's claim for deduction under Section 10B (of Income Tax Act, 1961) in respect of the Assessee's plant at Codli mines.

8. On 14/2/2012, the Commissioner of Income Tax (CIT) issued notice to the Assessee invoking the provisions of Section 263 (of Income Tax Act, 1961) and requiring the Assessee to show cause as to why the AO's order dated 23/12/2009 be not revised on the grounds referred to in the notice.

9. The Assessee filed a response dated 1/3/2012, pointing out that there were errors in the assessment order date 23/12/2009. This was followed by yet another response dated 15/3/2012, in the context of various issues raised in the CIT's notice dated 14/2/2012, purporting to invoke revision powers under Section 263 (of Income Tax Act, 1961).

10. CIT, on 23/3/2012, issued yet another notice under Section 263 (of Income Tax Act, 1961), mainly relating to the issue of additional depreciation. The Assessee responded to this notice on 29/3/2012.

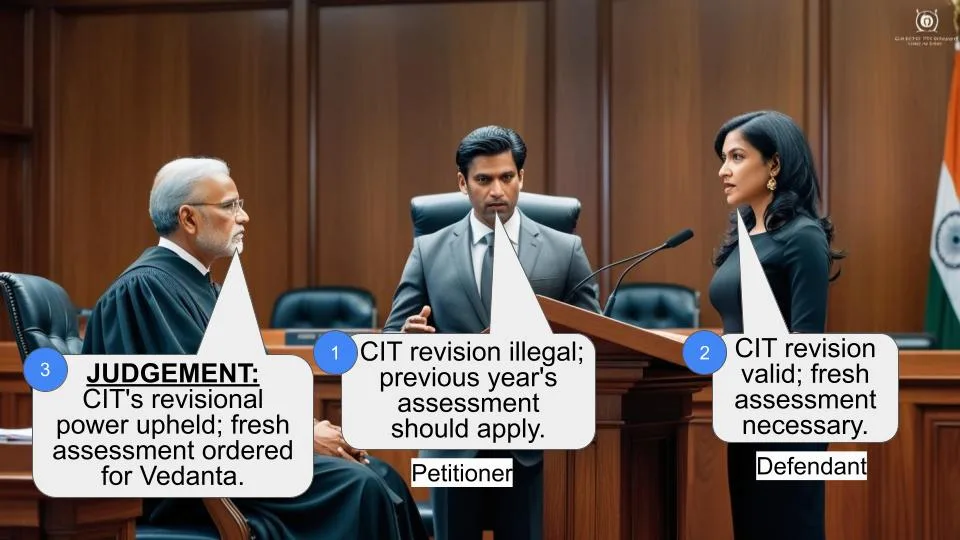

11. The CIT, vide order dated 29/3/2012 exercising revision powers under Section 263 (of Income Tax Act, 1961), set aside the AO's order dated 23/12/2009 and directed the AO to undertake a fresh assessment for the Assessment Year 2006-07.

12. The Assessee, on 17/5/2012, appealed against the CIT's Order dated 29/3/2012 to the Income Tax Appellate Tribunal (ITAT). This appeal was dismissed by the ITAT vide impugned order dated 18/7/2014. Hence the present Appeal.

13. Mr. Pardiwalla, the learned Senior Advocate for the Appellant, at the outset, submitted that even when the Assessee's Appeal was pending before the CIT in this matter, the ITAT, vide order dated 8/3/2013, upheld the Assessee's claim for deduction under Section 10B (of Income Tax Act, 1961) for the Assessment Year 2009-10. Similarly, the ITAT, vide yet another order dated 17/5/2013, allowed the Assessee's claim for deduction under Section 10B (of Income Tax Act, 1961) for Assessment Year 2008-09. He submits that the impugned order dated 18/7/2014, therefore, conflicts with the ITAT's earlier orders dated 8/3/2013 and 17/5/2013 on the same issue, though in respect of different assessment years. He, therefore, submits that the ITAT's impugned order dated 18/7/2014 warrants interference.

14. Mr. Pardiwalla further submits that in this case, the twin requirements for exercising powers under Section 263 (of Income Tax Act, 1961) were not existent. Therefore, the CIT exceeded the jurisdiction in invoking the provisions of Section 263 (of Income Tax Act, 1961). He submits that there was absolutely nothing erroneous in the AO's order dated 23/12/2009, in which the AO after due application of mind, had allowed the Assessee's claim for deduction under Section 10B (of Income Tax Act, 1961). He submits that unless an order is both, erroneous and prejudicial to the interests of Revenue, the CIT lacked jurisdiction to exercise the revision powers. He submits that on this ground as well, the CIT's order dated 23/12/2009 and the ITAT's impugned order dated 18/7/2014 confirming the same, warrant interference.

15. Mr. Pardiwalla submits that the AO, by his communications dated 16/9/2009 and 2/12/2009 raised specific queries on the issue of claim for deduction under Section 10B (of Income Tax Act, 1961). He points out that the Assessee, vide responses dated 28/10/2009 and 7/12/2009, furnished all the necessary details in support of the claim for deduction under Section 10B (of Income Tax Act, 1961). Thereafter, the AO, after due application of mind to such details, allowed its claim under Section 10B (of Income Tax Act, 1961). Thus, this was a case where the AO, after due consideration of the material on record, and after due application of mind, concluded that the Assessee was entitled to deduction under Section 10B (of Income Tax Act, 1961). He submits that this was a correct view or, in any case, a plausible view taken by the AO. The CIT, in such a situation, lacked jurisdiction to style the AO's order dated 23/12/2009 as erroneous and interfere with the same by exercising revision jurisdiction. He submits that the settled law is that a plausible view of the AO is not interfered with by the CIT in exercise of powers under Section 263 (of Income Tax Act, 1961) merely because the Commissioner may entertain a different view in the matter. He relies on the following decisions in support of his contention:

(a) Commissioner of Income Tax vs. Max India Ltd. 1;

(b) CIV vs. Design Automation Engineers (Bom.) (P) Ltd.

16. Mr. Pardiwalla contends that even assuming that this is a case of inadequate consideration on the issue of claim under Section 10B (of Income Tax Act, 1961), the Commissioner still has no jurisdiction under Section 263 (of Income Tax Act, 1961) to interfere with such order. He relies on the following decisions in support of this contention:

(i) CIT vs. Vodafone Essar South Ltd.

(ii) CIT vs. Gabriel India Ltd.

(iii) Malabar Industrial Co. Ltd. vs. Commissioner of Income Tax

17. Mr. Pardiwalla contends that the notice dated 14/2/2012 purporting to invoke the revision powers under Section 263 (of Income Tax Act, 1961) was based upon SFIO Report. This itself indicates non- application of mind on the part of the CIT. In any case, the SFIO report was eventually withdrawn and, therefore, the very basis for issuance of notice dated 14/2/2012 did not survive. He, therefore, submits that the entire proceedings under Section 263 (of Income Tax Act, 1961) are without jurisdiction and deserve to be set aside.

18. Mr. Pardiwalla submits that even, otherwise on merits, there was ample material available on record from which it was evident that the Assessee fulfilled all the prescribed requirements for claim under Section 10B (of Income Tax Act, 1961). On the basis of fulfillment of such requirements, the Assessee had in fact been granted such deduction for the subsequent assessment years. Therefore, even on merits, the impugned orders made by the CIT and the ITAT, warrant interference.

19. Ms. Linhares, the learned Standing Counsel defends the impugned orders based on the reasoning reflected therein. She points out that there is absolutely no discussion in the AO's order dated 23/12/2009 for allowing the Assessee's claim for deduction under Section 10B (of Income Tax Act, 1961), which claim was belatedly made by the Assessee though filed by revised return. She points out that at least during the relevant assessment year, there was really no material on record to hold that the Assessee fulfilled the prerequisites for claim of deduction under Section 10B (of Income Tax Act, 1961). In any case, she points out that there was absolutely no consideration by the AO on this issue and this is not a case of some sort of inadequate consideration as contended on behalf of the Assessee. She points out that even the decisions relied upon by the Assessee make it clear that the revision powers can be exercised where the AO fails to even consider the relevant and vital issues that arise in the matter. For these reasons, she submits that the present Appeals may be dismissed.

20. Ms. Linhares also pointed out that this Court, vide its Judgment and Order dated 12th March, 2020 in Tax Appeal No.24/2011 remanded the matter to the Commissioner of Income Tax to reconsider the issue of deduction under Section 10B (of Income Tax Act, 1961) in respect of this very Assessee for the Assessment Year 2005-06. She points out that the claim for deduction has to be considered in respect of each assessment year, depending upon whether the Assessee fulfills the prerequisites for the relevant assessment year or not.

21. Ms. Linhares also relies on the decision of the Hon'ble Supreme Court in Malabar Industrial Co. Ltd. (supra) to submit that where the AO accepts any entry in the statement of account of the Assessee without any supporting materials and without making any inquiry, such exercise of jurisdiction by the Commissioner under Section 263(1) (of Income Tax Act, 1961) is justified.

22. Ms. Linhares also relied upon Rampyari Devi Saraogi vs. CIT to submit that the CIT in this case had merely directed the AO to consider the issue of deduction under Section 10B (of Income Tax Act, 1961) afresh and, therefore, the Assessee was not prejudiced in any manner. She points out that in similar circumstances, the High Court, as well as the Supreme Court, had refused to interfere with the exercise of revision jurisdiction by the Commissioner.

23. For all the aforesaid reasons, Ms. Linhares submits that these Appeals may be dismissed.

24. Rival contentions now fall for our determination.

25. In this matter, records reveal that the Assessee in its original return of income did not claim any deductions under Section 10B (of Income Tax Act, 1961). However, in the revised returns, filed within the prescribed period of limitation, the claim for deduction under Section 10B (of Income Tax Act, 1961) was made.

26. The AO, by his communication dated 16/9/2009 required the Assessee to attend his office on 24/9/2009 and to produce or cause to be produced at the said time any documents, accounts and any other evidence on which the Assessee may rely upon in support of the return filed. It is pertinent to note that at least in this communication dated 16/9/2009, there were no specific queries raised in respect of any deduction claimed either in the original return or in the revised return.

27. The Assessee submitted its response on 28/10/2009. At paragraph 11 of this response, the Assessee referred to Annexure 12 for justification for Section 10B (of Income Tax Act, 1961) deduction. In Annexure 12, the Assessee did provide some information in support of its claim for deduction under section 10B (of Income Tax Act, 1961).

28. The AO addressed yet another communication dated 2/12/2009 to the Assessee. This time raising several queries in relation to the Assessee's claim for deduction under Section 10B (of Income Tax Act, 1961).

29. Again the Assessee, vide response dated 7/12/2009, submitted information in relation to the deduction claimed under Section 10B (of Income Tax Act, 1961).

30. Based upon the information supplied by the Assessee in its responses dated 28/10/2009 and 7/12/2009, Mr. Pardiwalla contended that not only the AO was conscious of the ingredients of Section 10B (of Income Tax Act, 1961), but further, took pains to obtain from the Assessee details on the basis of which, the claim of the Assessee for deduction under Section 10B (of Income Tax Act, 1961) could be allowed. He, therefore, contended that this is a case where the AO has allowed the Assessee's claim for deduction under Section 10B (of Income Tax Act, 1961) and, therefore, there was no question of exercise of revision jurisdiction by the CIT in such a matter.

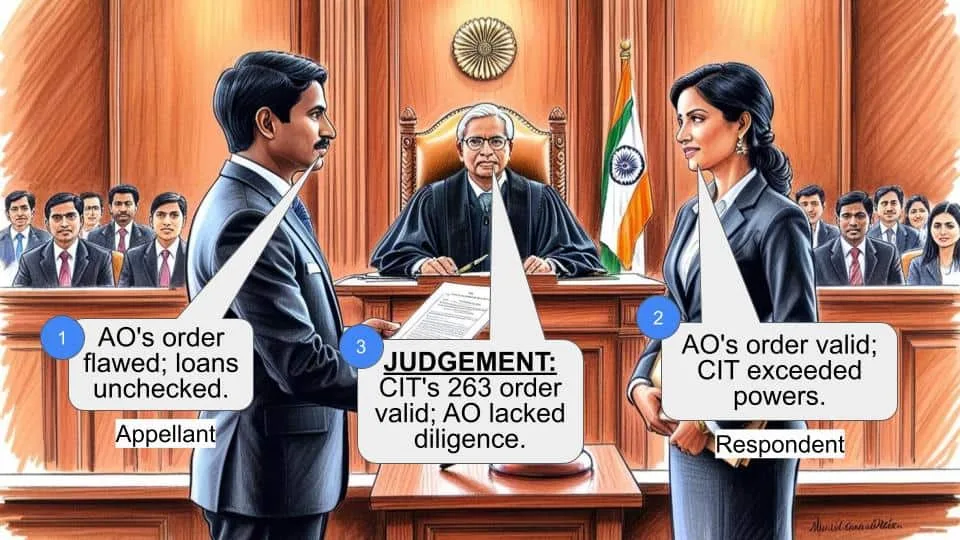

31. The material on record does indicate that the AO, in this case, sought for information from the Assessee with regard to its claim for deduction under Section 10B (of Income Tax Act, 1961) vide its communication dated 2/12/2009. However, according to us, this by itself can never be regarded as sufficient. What is further necessary is that the AO actually applies his mind to the information that may be supplied by the Assessee and considers such information and thereafter forms an opinion whether the Assessee is actually entitled to deduction under Section 10B (of Income Tax Act, 1961) for the relevant assessment year. There is a distinction between merely calling for information on a particular issue and considering such information with due application of mind if and when such information is actually provided by the Assessee.

32. Now, if the order dated 23/12/2009 made by the AO is perused, we find merit in the contention of Ms. Linhares that there was no consideration whatsoever of the information provided by the Assessee in the context of its claim for deduction under Section 10B (of Income Tax Act, 1961). The assessment order dated 23/12/2009 indicates that the AO has not even considered, much less, applied his mind to such information before allowing the deduction under Section 10B (of Income Tax Act, 1961). On perusal of the assessment order dated 23/12/2009, an impression is created that the AO proceeded on the basis that such deduction was allowable without considering whether the same was actually allowable at all in the context of the various prerequisites provided in Section 10B (of Income Tax Act, 1961).

33. Analysis of the assessment order dated 23/12/2009 indicates that in its first three paragraphs, there is a reference to the nature of business undertaken by the Assessee and reference of the case of the Assessee under Section 92CA (of Income Tax Act, 1961) to the Transfer Pricing Officer for determination of arm’s length price in respect of international transactions reported for the relevant assessment year. Then paragraph 4, along with its sub-paragraphs 4.1 to 4.7 deal with disallowance under Section 40(a)(ia) (of Income Tax Act, 1961) in the context of commission exceeding Rs.18.00 crore paid by the Assessee during the relevant assessment year, even though the TDS on the commission paid was negligible. Paragraph 5 deals with the expenditure incurred towards research and development. Paragraph 6 deals with the issue of depreciation on UPS. Finally, paragraph 7 deals with computation on the basis of the opinion in paragraphs 4,5 and 6. Thus, on the issue of deduction under Section 10B (of Income Tax Act, 1961), there is absolutely no consideration and yet, the AO has allowed such deduction. This is, according to us, is a case of 'no consideration' as opposed to mere 'inadequate consideration'. This is, according to us, a clear case of non-application of mind to the material on record, without even going into the issue whether the material supplied by the Assessee was adequate or inadequate to determine its claim for deduction under Section 10B (of Income Tax Act, 1961). In such a situation, the exercise of revision jurisdiction by the CIT under Section 263 (of Income Tax Act, 1961), cannot be said to be prohibited even based upon the decisions relied upon by Mr. Pardiwalla, the learned Counsel for the Assessee in this matter.

34. In Vodafone Essar South Ltd. (supra), Delhi High Court has held that if there is some inquiry by the AO in the original proceedings, even if inadequate that cannot clothe the Commissioner with jurisdiction under Section 263 (of Income Tax Act, 1961) merely because he has formed another opinion in the matter. This decision is basically an authority for the proposition that revision powers under section 263 (of Income Tax Act, 1961) cannot be exercised merely because the Commissioner may have formed another opinion in the matter. This decision is also an authority for the proposition that revision jurisdiction is not to be exercised merely because the Commissioner is of the opinion that the inquiries made by the AO were inadequate.

35. In the present case, however, whatever status of the queries, it is apparent that the AO did not even bother to look into or consider the information provided by the Assessee in the context of the claim for deduction under Section 10 (of Income Tax Act, 1961). Therefore, this is not a case of some inadequate inquiries. This is a case of no inquiries. This is a case of non-consideration and consequently, non- application of mind to the material on record.

36. In Malabar Industrial Co. Ltd. (supra), the Hon'ble Supreme Court has held that the revision jurisdiction under Section 263 (of Income Tax Act, 1961) cannot be invoked to correct each and every type of mistake or error committed by the AO. It is only when an order is erroneous that the section will be attracted. An incorrect assumption of facts or an incorrect application of law will satisfy the requirement of the order being erroneous. In the same category fall orders passed without applying the principles of natural justice or without application of mind. Further, where the AO adopts one of the courses permissible in law and it has resulted in loss of revenue, or where two views are possible and the AO has taken one view with which the Commissioner does not agree, it cannot be treated as an erroneous order prejudicial to the interests of the revenue, unless the view taken by the AO is unsustainable in law.

37. Further, the Hon'ble Supreme Court noted that the AO in the case before it, passed the order of nil assessment without application of mind. The Court also recorded a finding that the AO failed to apply his mind to the case in all perspective and the order passed by him was erroneous. The AO in the said case, accepted an entry in the statement of the account filed by the appellant in the absence of any supporting material and without making any inquiry.

The Hon'ble Apex Court then held that on these facts, the conclusion that the order of the AO was erroneous was irresistible. Therefore, the High Court had rightly upheld that the exercise of the jurisdiction by the Commissioner under Section 263(1) (of Income Tax Act, 1961).

38. This decision, according to us, assists the case of the Revenue, since, in the present case as well, there was no inquiry by the AO on the issue of fulfillment of requirements under Section 10B (of Income Tax Act, 1961). The mere seeking of information but thereafter, not even looking into the same is not the same thing as inquiring into the matter. Further, the AO has to consider the information so furnished and after applying the mind, arrive at a decision one way or the other on the issue before him,

39. In Gabriel India Ltd. (supra), this Court has held that the decision of the AO cannot be regarded as erroneous simply because the AO did not make an elaborate discussion in the order. In our case, as noted earlier, there is no discussion whatsoever, much less any inadequate discussion. Moreover, in Gabriel India Ltd. (supra), the Commissioner after initiating proceedings for revision, could not himself say that the allowance of the claim of the Assessee was erroneous and that the expenditure was not revenue expenditure, but an expenditure of capital nature. It is in these circumstances that the exercise of revision jurisdiction was interfered with by this Court.

40. In Commissioner of Income Tax vs.Nirav Modi, this Court noted that the AO had not only made detailed inquiries, but recorded a finding that the Assessee had duly proved the identity, source and creditworthiness of donors. In these circumstances, the Court held that if two views are possible and the AO has taken one of the possible views, no occasion to exercise powers of revision can arise. In this case, this Court has also observed that power of revision can be exercised only where there was no inquiry as required under law and not where inquiry was held and the same was inadequate.

41. In NTPC Ltd. vs. CIT.it was held that where the view taken by the AO is endorsed by law, there was no question of exercise of revision jurisdiction by the Commissioner. The Court reiterated the legal position that as long as the AO's opinion is a plausible one, the exercise of revision powers would be unwarranted.

42. The principles in Max India Ltd. (supra) and Design Automation Engineers (Supra) are of no assistance to the Assessee because this is not a case of interference with a plausible view of the AO based on some different opinion held by the Commissioner.

43. In K.A. Ramaswamy Chettiar and anr. vs. CIT,it was held that when an officer is expected to make inquiry of a particular item of income and if he does not make any inquiry as expected, that would be a ground to interfere with the order passed by the officer, since such an order passed by the Officer is erroneous and prejudicial to the interests of the Revenue.

44. In several decisions, it has been held that it is incumbent on the AO to investigate the facts stated in the return when the circumstance would make such an inquiry prudent and when the word 'erroneous' in Section 263 (of Income Tax Act, 1961) includes failure to make an inquiry, the order becomes erroneous when such an inquiry had been made and not because there is anything wrong with the order if all the facts stated therein are assumed to be correct. Duggal and Co. vs. Commissioner of Income Tax.

45. In a case of this nature, it is not sufficient that the AO merely raises queries or poses questions. If such queries are answered, it is the duty of the AO to consider such answers and based thereon, to take further steps to arrive at a reasoned decision. Perusal of the impugned order does not indicate that the AO has even adverted to, much less, considered the responses filed by the Assessee. There is not even finding in the assessment order that the Assessee was entitled to deduction under Section 10B (of Income Tax Act, 1961) on account of the answers furnished by the Assessee to the queries raised by the AO. In respect of such order, the CIT was entitled to exercise the revision jurisdiction since the order is both, erroneous as well as prejudicial to the interests of the Revenue.

46. Ms. Linhares has quite correctly relied upon Rampyari Devi Saraogi (supra), in which the Hon'ble Supreme Court has held that the Commissioner can regard the AO's order as erroneous on the ground, that in the circumstances of the case, the AO should have made further inquiries before accepting the statement made by the Assessee in his return. Besides, the Hon'ble Supreme Court, in the facts of the said case, held that the Assessee had not suffered in any way from the failure of the Commissioner to indicate results of inquiries since, the Assessee would have full opportunity of showing the AO whether he has jurisdiction or not, and whether the income assessed in the assessment orders which were originally passed was correct or not.

47. The circumstance that for certain subsequent assessment years the claim of the Assessee for deduction under Section 10B (of Income Tax Act, 1961) was allowed by the ITAT is not strictly speaking relevant to determining whether revision jurisdiction was correctly invoked. Firstly, the view taken by the ITAT has till date, not attained the finality. Secondly, the view was in the context of the subsequent assessment years. It is possible that for a given assessment year the Assessee does not fulfill the prerequisites for claiming the deduction under Section 10B (of Income Tax Act, 1961), but for the subsequent years such prerequisites are duly fulfilled. For the assessment year with which we are concerned, the AO, without considering the material on record and without application of mind to the responses furnished by the Assessee, proceeded on the basis that the Assessee was entitled to the deduction under Section 10B (of Income Tax Act, 1961). In these circumstances, it cannot be said that the CIT exceeded the jurisdiction in exercising powers under Section 263 (of Income Tax Act, 1961).

48. From the material on record, it is not possible to say that the CIT, in this case, acted under dictation from any extraneous authority. It is true that the CIT, in this case, in invoking revision jurisdiction, made reference to the SFIO report. However, that does not mean that the CIT acted under dictation. Therefore, any subsequent and allegedly changed SFIO report would not dent the exercise of jurisdiction by the CIT under Section 263 (of Income Tax Act, 1961).

49. Mr. Pardiwalla did attempt to urge that the Assessee was indeed involved in manufacture and, therefore, was entitled to deduction under Section 10B (of Income Tax Act, 1961). According to us, it was for the AO to examine the matter by due application of mind and, thereafter, decide afresh whether the Assessee was indeed entitled to deduction under Section 10B (of Income Tax Act, 1961). The decision of the AO to allow such deduction to the Assessee without making any inquiries whatsoever or rather without addressing the issue in his order, rendered his order quite erroneous and prejudicial to the interests of the Revenue. At this stage, therefore, it will not be appropriate for us to examine the issue as to whether the Assessee indeed fulfilled the requirements of Section 10B (of Income Tax Act, 1961) during the relevant assessment year.

50. Ms. Linhares pointed out that in pursuance of the orders made by the CIT and the ITAT, the AO has made a fresh assessment order. Mr. Pardiwalla, on instructions, states that said assessment order has been appealed and the appeal is pending. Be that as it may, it is for the Appellate Authority to go into the issue of eligibility of the Assessee for deduction under Section 10B (of Income Tax Act, 1961) during the relevant assessment year. Therefore, it will not be appropriate for us, at this stage and in these proceedings to go into such issues, now that we have held that there was no error in exercise of revision jurisdiction by the CIT for the relevant assessment year.

51. The substantial question of law is, therefore, required to be answered against the Assessee and in favour of the Revenue. As a consequence, both these Appeals are liable to be dismissed and are hereby dismissed. There shall be no order as to costs.

Dama Seshadri Naidu, J. M.S. Sonak, J.

×

Similar Ripples

Questions

Tax Deduction Dispute: Court Upholds CIT's Revision Power in Section 10B (of Income Tax Act, 1961) Case

Write your CommentSimilar Posts

Generic

- Reportdata/6159.pdf