Tax on Salary: Court Rules Employee's Self-Paid Tax Not Includible in Income

Full News

Tax on Salary: Court Rules Employee's Self-Paid Tax Not Includible in Income

Tax on Salary: Court Rules Employee's Self-Paid Tax Not Includible in Income

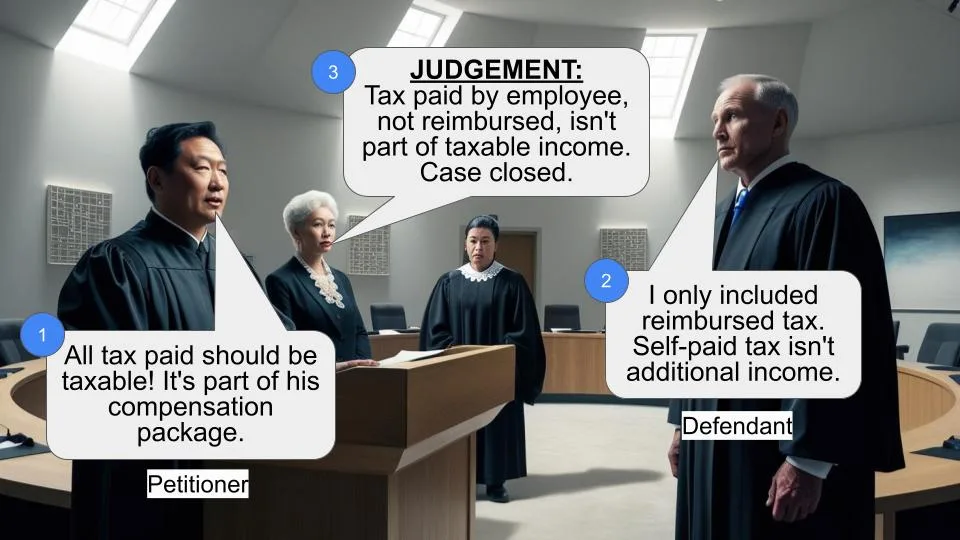

This case involves a dispute between the Commissioner of Income Tax and Jaydev H. Raja, an employee of Coca-Cola Inc. USA, regarding the taxation of his salary income. The main issue was whether the tax paid by the employee from his salary, which was not reimbursed by the company, should be added to his taxable income. The court ruled in favor of the employee, stating that the self-paid tax should not be included in his income.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs Jaydev H. Raja (High Court of Bombay)

Income Tax Appeal No.87 of 2020

Date: 25th September 2012

Key Takeaways:

1. Tax paid by an employee from their salary, which is not reimbursed by the employer, should not be added to the employee's taxable income.

2. When an employer reimburses tax on a portion of an employee's salary, only the reimbursed amount should be added to the taxable income.

3. The court's decision clarifies the application of tax equalization policies in international assignments.

Issue:

Should the tax paid by the assessee (employee) from his salary income, which was not reimbursed by the company, be added to his taxable income?

Facts:

1. The case pertains to the Assessment Year 1994-1995 .

2. Jaydev H. Raja, the assessee, was an employee of Coca-Cola Inc. USA, working on a foreign assignment in India .

3. The company had a Tax Equalization Policy, under which it would reimburse the tax liability arising from the foreign assignment, but only to the extent of that assignment .

4. The assessee received a salary of Rs.77.00 lakhs in India .

5. The total tax paid by the assessee was Rs.50.00 lakhs, of which Rs.35.00 lakhs was reimbursable by the company.

6. The assessee included Rs.35.00 lakhs (the reimbursable amount) in his taxable income, making it Rs.113.00 lakhs (77.00 + 35.00).

7. The dispute arose over whether the remaining Rs.15.00 lakhs (50.00 - 35.00) should also be added to the taxable income.

Arguments:

The Revenue (Income Tax Department) argued that:

1. The entire tax amount paid (Rs. 50.00 lakhs) should be considered part of the assessee's taxable income.

2. The Tribunal was not justified in holding that tax borne by the employee is not part of the pay .

The Assessee (Jaydev H. Raja) contended that:

1. Only the reimbursed tax amount (Rs.35.00 lakhs) should be added to his taxable income.

2. The remaining Rs.15.00 lakhs, which he paid from his own salary, should not be included in his taxable income .

Key Legal Precedents:

The judgment mentions a precedent case:

M.A.E. Paes reported in 230 ITR 60 - This case was cited by the Tribunal in relation to the second question about notional interest on interest-free deposits.

Judgement:

1. The court ruled in favor of the assessee, Jaydev H. Raja.

2. It held that the Tribunal was justified in its decision that the tax amounting to Rs. 15.00 lakhs paid by the assessee from his salary income (not reimbursed by the company) could not be added to his taxable income.

3. The court dismissed the appeal by the Commissioner of Income Tax.

FAQs:

Q1: Why was only part of the tax reimbursed by the company?

A1: The company's Tax Equalization Policy only covered tax liability arising from the foreign assignment, not the employee's entire tax liability.

Q2: Why did the assessee initially add Rs.50.00 lakhs to his income and then deduct Rs.15.00 lakhs?

A2: This was a computational error that led to confusion. The assessee should have only added the reimbursable amount of Rs. 35.00 lakhs to his taxable income.

Q3: What is the significance of this judgment for other employees working on foreign assignments?

A3: This judgment clarifies that employees should only include reimbursed tax amounts in their taxable income, not the portion they pay themselves from their salary.

Q4: Did the court address any other issues in this case?

A4: Yes, there was a second question about notional interest on interest-free deposits for accommodation, but the court didn't entertain this question as it followed a previous decision.

Q5: What was the total taxable income determined for the assessee?

A5: The court agreed with the Tribunal's finding that the assessee's taxable income should be Rs.113.00 lakhs (Rs.77.00 lakhs salary + Rs.35.00 lakhs reimbursed tax).

1) According to the revenue the following questions of law arise out of the order of the ITAT dated 30/3/1999.

a) Whether on the facts and circumstances of the case and in law, the Tribunal was justified in holding that tax borne by the employee is not part of the pay?

b) Whether on the facts and circumstances of the case and in law the Tribunal was justified in holding that notional interest on interest free deposit made for accommodation is not part of perquisite of the assessee?

2) The assessment year involved herein is AY 1994-1995.

3) The respondent-assessee a resident but not ordinarily resident individual was an employee of Coca-Cola Inc. USA and had income under the head “Salalries”. Under the Tax Equalization Policy framed by the said company, the assessee's tax liability arising out of his foreign assignment was to be borne by the company but restricted only to the extent of liability arising out of such foreign assignment. As the assessee had foreign assignment in India during the assessment year in question, the company under its tax equalization policy was liable to reimburse the tax payable on total salary which the assessee was entitled to receive in India.

4) In the assessment year in question the assessee had returned income of Rs.1.13 crores and paid tax there on the said income at Rs.50.00 lakhs. Since the assessee had received Rs.77.00 lakhs in India and the tax payable thereon was Rs.35.00 lakhs which was to be reimbursed by the employer, the assessee had included Rs.35.00 lakhs to the salary income of Rs.77.00 lakhs and offered Rs.113.00 lakhs (round figure) to tax. Though tax on Rs.113.00 lakhs at Rs.50.00 lakhs was paid, the assessee claimed that out of Rs.50.00 lakhs only Rs.35.00 lakhs was includible in the total income and not the balance amount of Rs.15.00 lakhs. The Assessing officer rejected the contention of the assessee, CIT(A) upheld the decision of the Assessing Officer.

5) On further appeal, the ITAT in Paragraph 11 of its order has recorded a finding that the total salary received by the assessee in India was Rs.77.00 lakhs on which the tax payable at the maximum rate of 44.8% comes to Rs.35.00 lakhs. Since the assessee under the Tax Equalization Policy was entitled to get reimbursement of the tax payable on the amount of Rs.77.00 lacs, the assessee was justified in computing the salary income at Rs.113.00 lakhs (Rs.77.00 lacs plus Rs.35.00 lacs) which almost tallies with the income declared by the assessee. The Tribunal has further recorded that though the assessee had paid tax amounting to Rs.50.00 lakhs, the assessee was entitled to reimbursement of tax amounting to Rs.35.00 lakhs and the balance Rs.15.00 lakhs was borne out of the salary income received by the assessee in India. The Tribunal has recorded a finding that the confusion has arisen, because, the assessee in his computation had added Rs.50.00 lakhs as income and deducted Rs.15.00 lakhs from the income, when in fact the said amount of Rs.15.00 lakhs was not received from the company but paid out of the salary amount received in India. In other words, though the assessee had paid tax of Rs.50.00 lakhs, since the assesses was entitled to reimbursement of Rs.35.00 lakhs from the Company, the salary income (Rs.77.00 lakhs) received by the assesses had to be enhanced by Rs.35.00 lakhs only and not the balance Rs.15.00 lakhs which is paid by the assesses from the salary income. In these circumstances, the Tribunal was justified in holding that the tax amounting to Rs.15.00 lakhs paid by the assessee from the salary income (not reimbursed by the company) could not be added to that income of the assessee. Accordingly the first question cannot be entertained.

6) As regards the second question is concerned, the Tribunal has allowed the claim of the assesee by following the decision of this Court in the case of M.A.E. Paes reported in 230 ITR 60. Accordingly, the second question cannot be entertained.

7) The appeal is accordingly dismissed with no order as to costs.

( M.S. SANKLECHA, J. ) ( J.P. DEVADHAR, J.)

×

Similar Ripples

Questions

Tax on Salary: Court Rules Employee's Self-Paid Tax Not Includible in Income

Write your CommentSimilar Posts

Generic

- Reportdata/5411.pdf