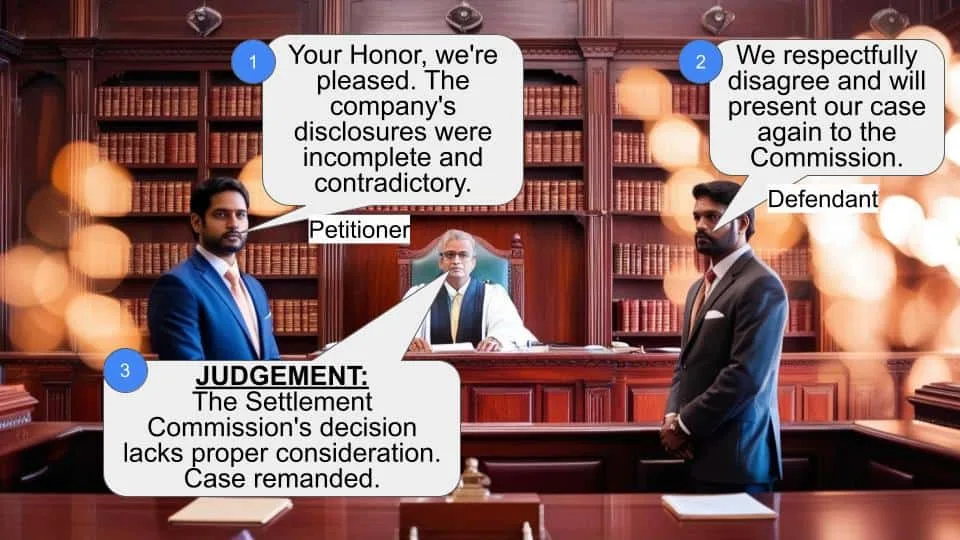

Tax Settlement Commission's Decision Quashed; Case Remanded for Fresh Hearing

Full News

Tax Settlement Commission's Decision Quashed; Case Remanded for Fresh Hearing

Tax Settlement Commission's Decision Quashed; Case Remanded for Fresh Hearing

This case involves the Commissioner of Income Tax challenging a decision made by the Income Tax Settlement Commission regarding a tax settlement application filed by a company. The High Court quashed the Settlement Commission's order and remanded the case back for a fresh hearing, citing inconsistencies in the company's disclosures and the Commission's acceptance of disputed facts without proper deliberation.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax vs Income Tax Settlement Commission (High Court of Madras)

W.P.No.17347 of 2008 and M.P.No.1 of 2008

Date: 19th May 2020

Key Takeaways:

1. The court emphasized the importance of full and true disclosure in tax settlement applications.

2. The Settlement Commission's decision-making process was scrutinized, not just the final decision.

3. The case highlights the need for thorough examination of contradictions and discrepancies in settlement applications.

4. The court's power to intervene in Settlement Commission decisions when there are apparent irregularities was affirmed.

Issue:

Did the Income Tax Settlement Commission err in settling the case of the respondent company without properly considering the objections raised by the Income Tax Department and the apparent contradictions in the company's disclosures?

Facts:

1. The 2nd respondent (a company) filed a tax settlement application on 11.7.2005 for assessment years 1998-99 and 1999-2000.

2. The company had entered into transactions with Bellary Steel and Alloys Ltd (BSAL) for a turnkey project.

3. There were discrepancies between the amounts invoiced, received, and disclosed by the company.

4. The Income Tax Department raised objections to the settlement application.

5. The Settlement Commission accepted the company's version and settled the case.

6. The Commissioner of Income Tax challenged this decision in the High Court.

Arguments:

Petitioner (Income Tax Department):

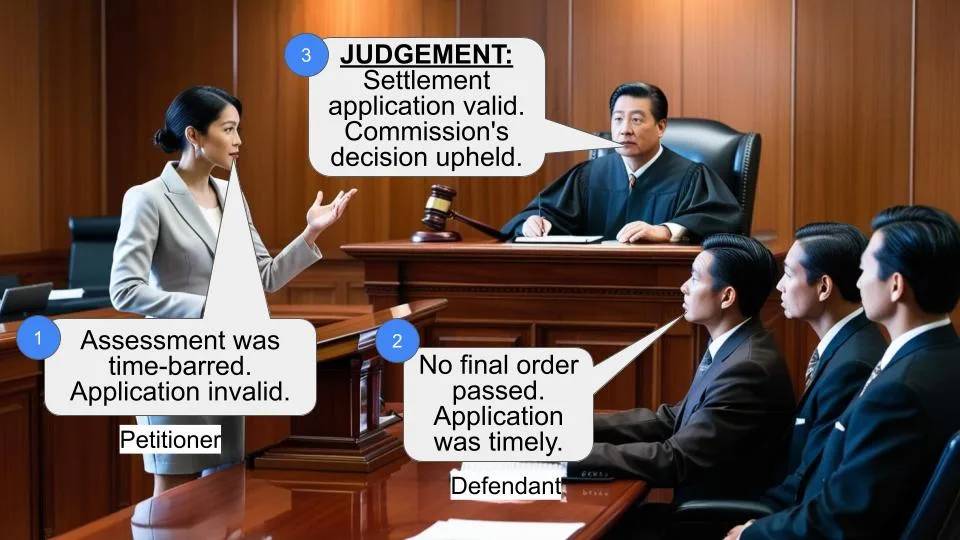

- The 2nd respondent failed to make full and true disclosure of its income.

- There were contradictions in the company's statements about amounts received and transactions made.

- The Settlement Commission ignored the department's objections filed under Rule 9 of the Settlement Commission (Procedure) Rules, 1997.

Respondent (Company):

- The company had paid the admitted tax liability before the cut-off date as per the amended Section 245D (of Income Tax Act, 1961).

- The Settlement Commission had jurisdiction to proceed with the application.

- The court should not interfere with the Commission's decision-making process.

Key Legal Precedents:

1. Union of India and Others Vs. Ind-Swift Laboratories Limited, (2011) 4 SCC 635

2. Commissioner of Income-tax (C) – III Vs. Gopal Gupta, (2014) 46 taxmann.com 312 (Delhi)

3. N. Krishnan Vs. Settlement Commission, (1989) 47 TAXMANN 294 (KAR)

4. R.B. Shreeram Durga Prasad V. Settlement Commission and another – 1989 1 SCC 628

5. Jyotendrasinhji V. S.L. Tripathi & Ors. – 1993 (3) SCC 38

Judgement:

1. The court found that the Settlement Commission had jurisdiction to proceed with the application as the company had paid the additional tax before the cut-off date (31st July 2007) as per Section 245D (of Income Tax Act, 1961).

2. However, the court quashed the Settlement Commission's order, citing:

- Lack of full and true disclosure by the company

- Contradictions in the company's statements

- The Commission's failure to properly consider the department's objections

3. The case was remanded back to the Settlement Commission for a fresh hearing within 6 months, considering the department's Rule 9 (of Income Tax Rules, 1962) report.

FAQs:

Q1: Why did the court quash the Settlement Commission's order?

A1: The court found that the company hadn't made a full and true disclosure, and the Commission hadn't properly considered the contradictions and objections raised by the Income Tax Department.

Q2: Does this mean the company's tax settlement is cancelled?

A2: Not necessarily. The case has been sent back to the Settlement Commission for a fresh hearing, so the outcome could still change.

Q3: What is the significance of Section 245D (of Income Tax Act, 1961) in this case?

A3: This section deals with the procedure for tax settlement applications. The 2007 amendment to this section set a deadline (31st July 2007) for paying additional tax on pending applications, which the company met.

Q4: Can the High Court interfere with the Settlement Commission's decisions?

A4: Yes, the High Court can intervene if it finds that the Commission's decision-making process was flawed or if there were apparent irregularities in the settlement.

Q5: What should taxpayers learn from this case?

A5: This case emphasizes the importance of making full and true disclosures when applying for tax settlements. Inconsistencies or contradictions in statements can lead to the settlement being challenged and potentially overturned.

The petitioner has challenged the impugned order dated 24.3.2008 passed by the 1st respondent in Application No. TN/CN 01/05-06/5/IT filed by the 2nd respondent on the ground that the 2nd respondent had failed to pay the admitted liability in terms of Section 245D(2A) (of Income Tax Act, 1961), 1961. According to the petitioner there was a shortfall in the payment of tax on the admitted liability.

2. It is therefore submitted that the impugned order of the first respondent was without jurisdiction. According to the petitioner there was a short fall of Rs.70,396/- detailed as under:-

“The entire TDS claims as refundable on the basis of returned loss for A.Y.1999-2000 was issued vide intimation issued under Section 143(1) (of Income Tax Act, 1961) on 30.06.2000 and revision order dated 23.10.2003. Thus total refund issued was Rs.20,61,963/- which included interest under Section 244 (of Income Tax Act, 1961) A. Under proviso (ii) to section 245C(1) (of Income Tax Act, 1961), tax and interest payable would be such tax and interest which would have been paid under the provisions of the Act had the income disclosed in the application been declared in the return of income before the Assessing Officer on the date of filing of application. The tax payable, therefore, would have been as follows: Amount in Rs.

Total income as disclosed 14,96,469

Tax payable thereon: 5,23,764

TDS: 18,00,086

Refund due 12,76,322

Interest under Section 244 (of Income Tax Act, 1961) A 1,91,445

Total Refund due 20,61,963

Balance payable 5,94,196

Amount actually paid by the

applicant 5,23,800

Amount of shortfall in tax 70,396

3.Operative portion of the impugned order reads as under:-

“3.The applicant had entered into agreement with BSAL for carrying out a turn-key project for Rs.102 Crores. For execution in the project, initially an amount of Rs.20.14 crores was required for import of machinery from Germany. This amount was directly paid by the BSAL by opening L.C. In favour of the German company and this amount was not received by the applicant but was paid on behalf of the applicant by BSAL.

4.The applicant received, in addition to the amount paid to Germany Company, amount of Rs.35,77 crores which was booked as contract receipts. The applicant fairly stated that out of this amount of Rs.35.77 crores, an amount of Rs.12.24 crores was received in A.Yr.1998-99 and was duly accounted for as income in 1007-98. Hence the same is not a part of the application before the Commission. This amount was considered as part of receipt and income for the year 1997-98. The balance amount of Rs.23.53 crores is to be considered in the present case.

5.The A/R fairly stated that as the circumstances had changed from the both the BSAL and applicant did not wish to go to the execution of the contact. This amount received was ultimately dealt as accommodation entries for BSAL. The applicant arranged to issue of cheques for supplies after keeping 5% of the amount for itself and the cash so generated was paid to BSAL through various suppliers. The applicant has offered 5% of the amount and further amount of Rs.1.5 crores by way of undisclosed income.

6.The CIT has stated in his report that the applicant had actually invoiced Rs.72.43 crores to BSAL. The invoice amount should be considered as income of the applicant. We do not see any substance in the CIT (DR)'s argument. The billed amount cannot be considered as income when the applicant has not at all received the balance amount. Under the circumstances, we do not see any reason to make any adjustment on this account.

7.The CIT has raised the issue of discrepancy between contract receipts shown by the applicant and payments claimed by BSAL. The A/R fairly stated that the CIT's contention that Rs.72.43 crores was illed to BSAL is correct. However the fact remains that the applicant received payment of only Rs.35.77 crores. Definitely the BSAL had not paid Rs.102.00 crores (agreement valued to the entire contract to the applicant). The BSAL had not even paid the entire billed amount. Considering the circumstances, we hold that there is no discrepancy in the amounts as claimed by the CIT.

8.The CIT also raided the issue that as per the ledger accounts of applicant in BSAL, larger amount was paid. However, it is seen that other amounts shows are stated to have been transferred to head office. We do not agree that amount transferred to head office by BSAL is a payment to the applicant. It is only transfer to the head office of BSAL. In any case the applicant has nothing to do with such transfer. In view of the above, we do not see any reason to make any adjustment to the offer made by the applicant on account of BSAL.

9.Next issue raised in the Rule-9 (of Income Tax Rules, 1962) report is purchase of windmills from applicant by First Leasing Company of India Ltd. (FLCIL). The CIT in Rule-9 (of Income Tax Rules, 1962) report has stated that FLCIL claimed to have purchased 13 windmills from the applicant for Rs.13 Crores (In A.Yr.1997-98 which is not before the Commission). He further stated that in case of FLCIL, lease rent has been disallowed.

10.The A/R stated that the applicant had never sold any mills to FLCIL. The applicant had agreed to construct windmissls for FLCIL for which the applicant received Rs.3.32 crores as advance. Subsepuently, the contract was cancelled and the FLCIL encashed the bank guarantee given to the applicant and recovered back the advance. Since the contract was cancelled, we do not see any reason to make adjustment on this account. We would also like to add that if the applicant had leased windmills then it would have been entitled to deduct the lease rent paid. Such payment has not been claimed by the applicant either original assessment or before the Commission. Hence in our opinion, no adjustment is required on this account.

11.The CIT has stated that the entire transaction for BSAL is bogus and profit cannot be estimated on bogus transaction. There is merely an issue which we have already dealt with and we do not see any reason to make adjustment on this account.

12.In view of the above, the income is settled at Rs.2.69 Crores.

A.Yr.1998-99 Rs.1,83,00,000

A.Yr.1999-00 Rs.86,00,000.

13.In view of the statutory time limit prescribed u/s.245D(4A) (of Income Tax Act, 1961), the Settlement Commission directs the Commissioner of Income-tax to compute the total income, incometax, interest and penalty, if any, payable as per this order and communicate to the applicant immediately along with demand notice and challan under intimation to this office.

14.The applicant shall pay the tax within 35 days of receipt of a demand notice. The applicant shall furnish proof of the tax payment to the Settlement Commission and the Assessing Officer within 10 days of making the payment. If the tax is not paid within the due date, the tax along with interest under section 245D(6A) (of Income Tax Act, 1961) of the Income- tax Act shall be recovered by the Assessing Office as per Chapter XVII of the Income Tax Act.

15.Considering the co-operation extended by the applicant in the completion of the present proceeding, immunity is granted from prosecution under the I.T. Act and under the relevant provisions of the I.P.C. And also from the imposition of any penalty under the I.T.Act, with reference to the case covered by the present settlement. However, the immunity so granted shall be withdrawn, if it is subsequently found that the conditions mentioned in Sub-Section (1A) and/or Sub-Section (2) of the Sec.245H (of Income Tax Act, 1961) are satisfied.

16.This settlement shall be declared void, if it is subsequently found by the Settlement Commission that it has been obtained by fraud or misrepresentation of facts.” 4.The 2 nd respondent filed an application to settle the case on

11.7.2005 before the 1 st respondent Income Tax Settlement Commission in Application No. TN/CN 01/05-06/5/IT.

5.The case of the petitioner is that the 2 nd respondent had entered into dubious transactions wherein without carrying out any work the petitioner had raised invoices on Bellary Steel and Alloys Ltd. (BASL)and had received payments but had suppressed the taxable income by raising invoices for fictitious supply and services to write of such payment as expenditure during the assessment years 1998-1999 and 1999 -2000.

6.Since assessment orders were passed which called upon the 2nd the 2nd respondent to pay differential tax, the 2nd respondent filed application to settle the case under the provisions of the Income Tax Act,1961 before the 1st respondent Income Tax Settlement Commission by not correctly declaring the tax liability.

7. According to the petitioner, despite the petitioner filing of a report on 12.10.2005 under Rule 6 (of Income Tax Rules, 1962) and 9 of the Income-tax Settlement Commission (Procedure) Rules, 1997 ,the 1st respondent proceeded to admit the case of the 2nd respondent contrary to section 245D (of Income Tax Act, 1961) after its amendment by Finance Act, 2007.

8.According to the petitioner the 1st respondent ought not to have proceeded with the aforesaid application filed by the 2nd respondent in as much as the 2nd respondent failed to comply with the mandatory requirement of the amended section 245D (of Income Tax Act, 1961) as amended by Finance Act, 2007.

9.According to the petitioner, there shall be deemed admission in respect of applications filed before 1.6.2007 which were pending before the amendment provided the applicant (the 2nd respondent has by the 2nd respondent) pays the admitted tax on the income disclosed in the settlement application and interest thereon on or before 31.7.2007.

10.According to the petitioner, the 2nd respondent only paid partially the admitted tax liability and interest thereon on 23.7.2007 and since there was short payment of the admitted tax liability, the 1st respondent erred settling the case of the 1st respondent contrary to section 245D (of Income Tax Act, 1961).

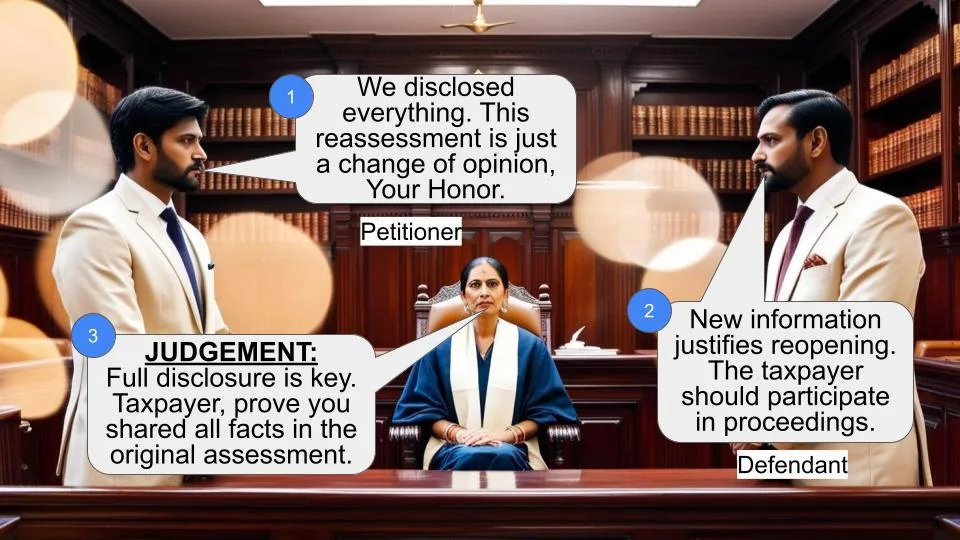

11.It is further submitted that the 1st respondent has ignored the report of the petitioner filed under Rule 9 (of Income Tax Rules, 1962). It is further submitted that the 2nd respondent also failed to truly and fully disclose all the material facts in the application and therefore the 1st respondent erred in allowing the application filed by the 2nd respondent.

12.It is submitted that according the 2nd respondent the total value of the invoice raised was Rs. 72.43 Crores out of which even as per the 2nd respondent, BSAL had paid a sum of Rs.60.50 Crores.

However, in the same application filed for settling the case, the 2nd respondent has further contracted itself by stating that it has received only a sum of Rs.35.77 Crores.

13.The learned counsel for the petitioner relied on the following decision:-

i.Union of India and Others Vs. Ind-Swift Laboratories Limited, (2011) 4 SCC 635.

ii.Commissioner of Income-tax (C) – III Vs. Gopal Gupta, (2014) 46 taxmann.com 312 (Delhi).

iii.N.Krishnan Vs. Settlement Commission, (1989) 47 TAXMANN 294 (KAR).

iv.M/s. Akshar Developers Vs. Income – Tax Settlement Commission Additional Bench II, Judgment dated 04.02.2019 passed by the High Court of Gujarat at Ahmedabad in R/Special Civil Application No.13572 of 2018 and batch of cases.

v. Commissioner of Income-tax, Karnataka (Central), Bangalore Vs. RNS Infrastructure Limited, (2016) 67 taxmann.com 77 (Karnataka).

14.On the other hand, it is the case of the 2nd respondent that the Asst. Commissioner by an order dated 28.4.2008 has given effect to the impugned order of the 1st respondent and has concluded that the 2nd respondent was eligible for a refund of Rs. 2,08,256 /- and therefore alleged shortfall in payment of Rs.70,396/- in payment of admitted tax liability on the additional amount cannot be countenanced.

15.It is therefore submitted that the impugned order was neither irregular nor without jurisdiction as the 2ndrespondent had paid the admitted tax liability on 23.7.2007 which was much before the cut off date as per the amended Section 245D (of Income Tax Act, 1961) in the year 2007.

16. 2nd respondent further submits that the present writ petition is nothing but an abuse of court proceedings in as much as the petitioner is re agitating the issues on merits and that same is impermissible under article 226 of the Constitution of India as this court is not sitting as an appellate court.

17.It is submitted that this court is not really concerned with the decision of the 1st respondent but with the decision making process adopted by the 1st respondent and since there is no error in the decision-making process, there is no scope for interference. It is therefore the present writ petition is liable to be dismissed with cost.

18.It is further submitted that there is also no perversity in the impugned order passed by the 1st respondent for this court to interfere and therefore the present writ petition is liable to be dismissed with costs.

19. It is further submitted that the 1st respondent had examined the issue at length and it is only after considering the objection of the petitioner filed under Rule 6 (of Income Tax Rules, 1962) and under Rule 9 (of Income Tax Rules, 1962) of the Income-tax Settlement Commission (Procedure) Rules, 1997 after impugned order has been passed.

20.The learned counsel for the respondent relied on the following decisions :-

i.R.B.Shreeram Durga Prasad V. Settlement Commission and another – 1989 1 SCC 628

ii.Jyotendrasinhji V. S.L.Tripathi & Ors. – 1993 (3) SCC 38

iii.Shryans Prasad Jain V. Income Tax Officer and Ors. 1993 Supp. 4 SCC 727

iv.Union of India and others V. Ind-Swift Laborataries – 2011 (4) SCC 635

v.Commissioner of Income Tax, Vijayawada vi. Settlement Commission (IT & WT) -Civil Misc. Writ Petition (Tax) No.1015 of 2013 1 passed by the Hon’ble High Court of Andhra Pradesh.

vii. Commissioner of Income tax (Chennai), (2014) 51 taxmnn.com 451 (Kerala) by Hon’ble High Court of Kerala.

21. I have considered the arguments advanced on behalf of the petitioner and respondent. The learned counsel for the petitioner was directed to produce records of the files pertaining to the above case from the 1st respondent. SGR was made available. I have perused the records.

22. It is noticed that the application for settling the case was filed by the 2nd respondent before the 1st respondent on 11.7.2005. The 2nd respondent had admitted to pay an additional amount of tax of Rs. 5,23,800 years 1998-99 and assessment years 1999-2000. Details of the amount agreed to be paid by the 2nd respondent are as follows:-

Assessment Year Additional income Additional tax agreed to

disclosed in the application be paid 1998-99 Rs.1,83,00,000/- Nil

1999-2000 Rs.86,00,000/- Rs.5,23,800

23. Before touching on the merits of the case, I will first refer to Section 245C (of Income Tax Act, 1961)/D of the Income Tax Act,1961 and the amendment to it in the year 2007.

24. Prior to amendment in 2007, under sub section (2A) to section 245D (of Income Tax Act, 1961) subject to the provisions of sub-section (2B), the assessee shall, within thirty-five days of the receipt of a copy of the order under sub-section (1) allowing the application to be proceeded with, pay the additional amount of income-tax payable on the income disclosed in the application and shall furnish proof of such payment to the Settlement Commission.

25. However, after amendment, Sub-clause (ii) to sub-section (2A) was substituted. An application filed under sub-section (1) of section 245C (of Income Tax Act, 1961) before the 1st day of June, 2007shall be deemed to have been allowed to be proceeded with if the additional tax on the income disclosed in such application and the interest was paid on or before the 31st day of July, 2007 if an order under the provisions of subsection (1) of the said section as it stood prior to their amendment by the Finance Act, 2007 was not made before the 1st day of June, 2007.

26. Since no order of admission was passed prior to the aforesaid date, the application shall be deemed to have been admitted if the an applicant pays the additional amount of tax on the additional amount admitted in the application before 31st day of July, 2007. In the present case, there is payment of additional amount of tax before 31st day of July, 2007.

27. Therefore, the 1st respondent Settlement Commission had jurisdiction to proceed further with the application filed by the 2nd respondent under Section 245 (of Income Tax Act, 1961). Therefore to that extent, I find no infirmity in the procedure adopted by the Settlement Commission in proceeding further with the application filed by the 2nd respondentunder Section 245 (of Income Tax Act, 1961).

28. However, at the same time, I am unable to uphold the impugned order of the 1st respondent Settlement Commission in accepting the case of 2nd respondent as I find the 2nd respondent has not made full and true disclosure of its income.

29. Prior to above applications, the petitioner had filed returns on 13.11.1998 for the assessment year 1998-99 and on 13.12.1999 for the assessment year 1999-2000. These returns ultimately lead to passing of two separate assessment orders dated 29.3.2005 for the respective assessment years.

30. Thus, as against the tax liability of Rs.11,65,11,970/- + Rs.36,40,99,161/- determined in the two assessment order, the petitioner has agreed to pay a sum of Rs.5,23,800 alone as admitted tax for settling the case under the provisions of the Income Tax Act, 1961.

31. Explanation to sub-section (2A) to Section 245D (of Income Tax Act, 1961), further stated that in respect of the applications referred to in this sub-section, the 31st day of July, 2007 shall, for the purposes of sub-section (1), be deemed to be the date of order of rejection or allowing the application to be proceeded with.

32. There are several contradictions in the case put forward by the 2nd respondent before the 1st respondent which remain unanswered and therefore the case ought not have been settlement under the Act.

What was expected was full disclosure of the facts and active co- operation by the petitioner and not a controlled disclosure of facts by the 2nd respondent in bits and pieces before the 1st respondent Settlement Commission.

33.In the application for settling the case before the 1st respondent, the 2ndrespondent has stated the principal namely Bellary Steel and Alloys Limited(BSAL) had awarded a turnkey contact to the 2ndrespondent for commissioning and installing an Integrated Steel Plant for a total value of Rs. 60.5 crores.

34. There were escalations in the value of the contract. According to the 2nd respondent, it had raised invoices over a period of time for a total sum of Rs.72.43 crores and against the invoices raised the received a sum of Rs. 60.50 crore.

35. In the said application, the 2nd respondent further submitted that it encountered difficulty in sourcing of materials required for additional work. Therefore, the 2ndrespondent agreed with BSAL for latter to directly identify the suppliers of materials for the additional work.

36. At the same time in paragraph 7 of the application, the 2nd respondent has stated that up to 31.3.1999, the said BSAL had transferred an amount of Rs. 35.77 crores through banking channels and these amounts were paid for contractual payments. 37. According to the 2nd respondent, the value of such additional materials were agreed, identified by BSAL which amounted to Rs.43.05 crores. Since procurements were directly made by BSAL, the expenses aggregating to the aforesaid sum of Rs.43.05 crores were debited towards such purchases and credit was given in the account of BSAL.

38. The 2nd respondent has also stated that as against the total invoice value of Rs.72.43 crores, a sum of Rs. 21.05 represents the value of machineries imported directly by BSAL which was paid by BSAL directly and a Rs.22.05 crores was invoiced fictitious transactions totaling to Rs.44.05 crores out of The Aforesaid Amount of Rs.72.43 Crores.

39.Thus, there are not only contradictions in the applications but it also lacks clarity. Rule 9 (of Income Tax Rules, 1962) report dated 10.3.2008 of the petitioner has also elicited several contradictions in the case of the 2nd respondent which has been ignored he 1st respondent.

40. From the records, it is also discernible that at one stage the 2nd respondent submitted that it had received a total sum of Rs.37.00 crores out of which about Rs. 6. crores was spent towards design charges and towards civil contract work and that a sum of Rs. 30.05 crores encashed and shown towards fictitious transactions.

41. The 1st respondent has accepted the version of the 2nd respondent received only a total sum of Rs. 35.77 crores up to 31.3.1999.from BSAL, out of which an amount of Rs. 12.24 crores was received during assessment year 1998-99 and was duly accounted as income, in the previous year 1997-98.

42. The 1st respondent has accepted that the statement of 2nd respondent that it retained only 5% of the amount paid to it by BSAL as commission. Since the 2ndrespondent agreed to add another amount of Rs.1.5 crores to the aforesaid sum as undisclosed income the 1 strespondent has accepted the case of the 2ndrespondent.

43. The arithmetic of the transactions disclosed before the 1st respondent Settlement Commission do not add up and clearly shows that there were large-scale suppression resorted by the petitioner not only before the assessing officer but also before the 1st respondent settlement commission.

44. The 1st respondent Settlement Commission has accepted the case of the 2nd respondent that a sum of Rs.20.14 crores was directly paid by BSAL by opening a LC directly in favour of the German company and that the amount was not received by the petitioner.

45. There are several discrepancies in the manner in which the case has been allowed to be settled by the 1st respondent settlement commission. The calculations has been accepted without any deliberations do not inspire confidence.

46. There are several disputed questions of fact which have been glossed over by the 1st respondent Settlement Commission while settling be case of the 2nd respondent vide impugned order.

47. Though, this court is not sitting in appeal against the impugned order of the 1st respondent Settlement Commission, I find sufficient reasons to interfere with the impugned order as there are several contradictions and the 2nd respondent appears to have not disclosed truly all facts that are required for settling the case. The impugned order has accepted cases without any discussions, I am therefore of the view that the impugned order is not sustainable.

48. Under these circumstances, the impugned order passed by the 1st respondent is quashed and the case is remanded back to the 1st respondent Settlement Commission to pass a fresh order after considering the objections of the petitioner filed under rule 9 of the Settlement Commission (Procedure) Rules 1997. Since the dispute pertains to the assessment years 1997-98 and 1999-2000 and the application filed by the 2nd respondent was of the year 2005, the 1st respondent Settlement Commission is requested to pass a fresh order within a period of 6 months from the date of receipt of this order after considering the report of the petitioner filed under Section 9 of the Settlement Commission (Procedure) Rules 1997 through videoconferencing, if situations so warrants on account of continuance of Covid19 pandemic. 49.The writ petition stands disposed with the above observation. Connected miscellaneous petition is closed. No cost.

C.SARAVANAN, J.

×

Similar Ripples

Questions

Tax Settlement Commission's Decision Quashed; Case Remanded for Fresh Hearing

Write your CommentSimilar Posts

Generic

- Reportdata/5966.pdf