Full News

Tax Tribunal Upholds Addition to Assessee's Income, High Court Dismisses Appeal

Tax Tribunal Upholds Addition to Assessee's Income, High Court Dismisses Appeal

A furniture retailer (the assessee) appealed against an Income Tax Appellate Tribunal decision. The Tribunal had upheld an addition to the assessee's income based on unexplained cash deposits. The High Court dismissed the appeal, agreeing with the Tribunal's factual findings.

Get the full picture - access the original judgement of the court order here

Case Name:

Naresh Kumar vs Commissioner of Income Tax (High Court of Punjab & Haryana)

ITA-382-2015 (O&M)

Date: 27th September 2016

Key Takeaways:

1. The court emphasized the importance of maintaining proper financial records, even for businesses operating under presumptive taxation schemes.

2. Unexplained cash deposits can be added to taxable income under Section 69A (of Income Tax Act, 1961).

3. The High Court showed deference to the Tribunal's factual findings, highlighting the limited scope for interference in tax appeals.

Issue:

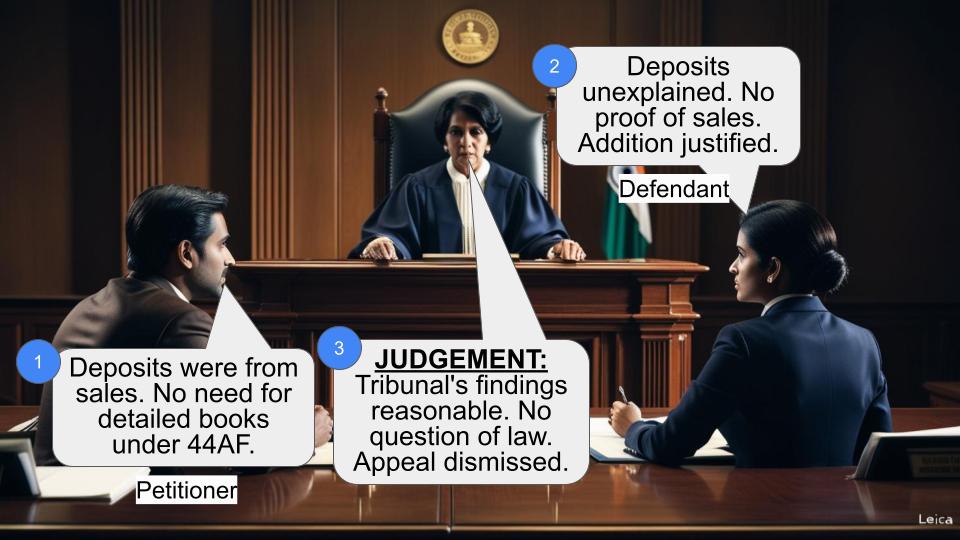

The main question here was whether the Income Tax Appellate Tribunal was correct in upholding the addition of Rs.18,31,500 to the assessee's income for unexplained cash deposits in his bank account.

Facts:

1. The assessee runs a wooden furniture retail business called M/s Shiva Furniture House in Mandi Gobindgarh, Punjab.

2. For the 2008-09 assessment year, he declared an income of Rs. 1,17,622 under Section 44AF (of Income Tax Act, 1961) (a presumptive taxation scheme for small retailers).

3. The Assessing Officer found cash deposits totaling Rs. 18,31,500 in the assessee's bank account, made in identical amounts of Rs. 49,500 on different dates.

4. When asked to explain these deposits, the assessee claimed they were from sales but couldn't provide satisfactory evidence.

5. The Assessing Officer added this amount to the assessee's income under Section 69A (of Income Tax Act, 1961).

6. The Commissioner of Income Tax (Appeals) deleted this addition, but the Income Tax Appellate Tribunal restored it.

Arguments:

The assessee's side:

- Claimed the deposits were from sales but couldn't provide complete sale/purchase bills.

- Argued that under Section 44AF (of Income Tax Act, 1961), he wasn't required to maintain detailed books of accounts.

- Said he usually purchased furniture on credit.

The tax department's side:

- Pointed out the lack of evidence linking the deposits to actual sales.

- Noted that the assessee couldn't name the parties from whom he purchased materials.

- Highlighted that withdrawals were made only at the end of the financial year.

Key Legal Precedents:

1. CIT vs. Surinder Pal Anand (2010) 48 DTR 135 (P&H): The Commissioner relied on this case to delete the addition, but the Tribunal distinguished the present case from it.

2. Section 44AF (of Income Tax Act, 1961): This section allows small retailers to pay tax on a presumptive basis without maintaining detailed books of accounts.

3. Section 69A (of Income Tax Act, 1961): This provision allows unexplained money to be added to the assessee's income.

Judgement:

The High Court dismissed the assessee's appeal, agreeing with the Tribunal's decision. They found that:

1. The Tribunal had decided questions of fact, not law.

2. The Tribunal's views were reasonable and not perverse or absurd.

3. No substantial question of law arose from the case.

FAQs:

1. Q: Does operating under a presumptive taxation scheme exempt a business from explaining large cash deposits?

A: No, even under presumptive taxation, unexplained cash deposits can be scrutinized and added to taxable income if not satisfactorily explained.

2. Q: What evidence could have helped the assessee's case?

A: Complete sale and purchase bills, names of suppliers, and a clear link between sales and deposits could have strengthened the assessee's position.

3. Q: Why did the High Court not interfere with the Tribunal's decision?

A: The High Court generally doesn't interfere with factual findings unless they're perverse or absurd. In this case, they found the Tribunal's reasoning reasonable.

4. Q: What's the takeaway for small businesses operating under presumptive taxation schemes?

A: While detailed books may not be required, it's crucial to maintain basic records and be able to explain significant financial transactions.

The present appeal under Section 260A (of Income Tax Act, 1961) (for short the 'Act') has been preferred by the assessee to challenge therein order dated 15.07.2015, passed by the Income Tax Appellate Tribunal, Division Bench, Chandigarh (for short the 'Tribunal').The appeal pertains to the assessment year 2008-09.

According to the appellant, the present appeal raises the following substantial questions of law: -

“1. Whether under the facts & circumstances of the case, the 'presumptive charge' of income u/s 44AF (of Income Tax Act, 1961) is distinguishable from arriving at 'chargeable income' u/s 29 (of Income Tax Act, 1961)?

2. Whether on facts and in circumstances of the case, the decision of the Tribunal is against the ratio laid down by the Hon'ble Court in the case of CIT vs. Surinder Pal Anand (2010) 48 DTR 135 (P&H) and hence violative of judicial discipline?”

The relevant facts which need to be noticed for adjudicating upon the present appeal are that the assessee is in the business of retail trading of wooden furniture and operates in the name and style of M/s Shiva Furniture House, Gole Market, Mandi Gobindgarh, Punjab. On 03.09.2008,for the assessment year in question, the assessee filed his return declaring therein an income of Rs.1,17,622/- which was assessed under Section 143(1) (of Income Tax Act, 1961). However, the assessing officer having reasons to believe that the income of the assessee had escaped assessment, after recording reasons, issued notice to the assessee under Section 148 (of Income Tax Act, 1961) as to why the income of the assessee may not be re-assessed. In response to such notice,the assessee filed his return, reiterating the income declared by him in his original return. Statutory notice under Sections 142(1) (of Income Tax Act, 1961)/143(2) of the Act, dated 31.10.2013, alongwith a questionnaire was issued and served upon the assessee in response to which the authorised representative of the assessee appeared and filed the required information. The assessee maintained that he was a retailer having a total turn-over of less than rupees forty lakhs and was filing his return of income under Section 44AF (of Income Tax Act, 1961). Thus, no books of accounts were being maintained by him. He, therefore, sought the re-assessment proceedings to be dropped.

The assessing officer went through the record before him, particularly the statement of the the assessee's savings account maintained by him with the Central Bank of India, Mandi Gobindgarh. The details of the same pertaining to the relevant assessment year as borne out from the record are as under: -

Value Post Details Chq Debit Credit Balance Date Date No.

BROUGHT FORWARD 0.00

16.06.07 16.06.07 DMINTA 000

DJ

30.06.07 30.06.07 BY INTT 1,817.00 1,05,618.00 Cr

13.08.07 13.08.07 BY CASH 49,500.00 1,55,118.00 Cr

14.08.07 14.08.07 BY CASH 49,500.00 2,04,618.00 Cr

16.08.07 16.08.07 BY CASH 49,500.00 2,54,118.00 Cr

17.08.07 17.08.07 BY CASH 49,500.00 3,03,618.00 Cr

18.08.07 18.08.07 BY CASH 49,500.00 3,53,118.00 Cr

20.08.07 20.08.07 BY CASH 49,500.00 4,02,618.00 Cr

22.08.07 22.08.07 BY CASH 49,500.00 4,52,118.00 Cr

27.08.07 27.08.07 BY CASH 49,500.00 5,01,618.00 Cr

28.08.07 28.08.07 BY CASH 49,500.00 5,51,118.00 Cr

30.08.07 30.08.07 BY CASH 49,500.00 6,00,618.00 Cr

27.09.07 27.09.07 BY CASH 49,500.00 6,50,118.00 Cr

28.09.07 28.09.07 BY CASH 49,500.00 6,99,618.00 Cr

01.10.07 01.10.07 BY CASH 49,500.00 7,49,118.00 Cr

04.10.07 04.10.07 BY CASH 49,500.00 7,98,618.00 Cr

05.10.07 05.10.07 BY CASH 49,500.00 8,48,118.00 Cr

08.10.07 08.10.07 BY CASH 49,500.00 8,97,618.00 Cr

09.10.07 09.10.07 BY CASH 49,500.00 9,47,118.00 Cr

10.10.07 10.10.07 BY CASH 49,500.00 9,96,618.00 Cr

11.10.07 11.10.07 BY CASH 49,500.00 10,46,118.00 Cr

30.10.07 30.10.07 BY CASH 49,500.00 10,95,618.00 Cr

31.10.07 31.10.07 BY CASH 49,500.00 11,45,118,00 Cr

01.11.07 01.11.07 BY CASH 49,500.00 11,94,618.00 Cr

02.11.07 02.11.07 BY CASH 49,500.00 12,44,118.00 Cr

05.11.07 05.11.07 BY CASH 49,500.00 12,93,618.00 Cr

06.11.07 06.11.07 BY CASH 49,500.00 13,43,118.00 Cr

07.11.07 07.11.07 BY CASH 49,500.00 13,92,618.00 Cr

08.11.07 08.11.07 BY CASH 49,500.00 14,42,118.00 Cr

10.11.07 10.11.07 BY CASH 49,500.00 14,91,618.00 Cr

16.11.07 16.11.07 BY CASH 49,500.00 15,41,118.00 Cr

26.11.07 26.11.07 BY CASH 49,500.00 15,90,618.00 Cr

28.11.07 28.11.07 BY CASH 49,500.00 16,40,118.00 Cr

01.12.07 01.12.07 BY CASH 49,500.00 16,89,618.00 Cr

03.12.07 03.12.07 BY CASH 49,500.00 17,39,118.00 Cr

04.12.07 04.12.07 BY CASH 49,500.00 17,88,618.00 Cr

CARRIED FORWARD 17,88,618.00 Cr

BROUGHT FORWARD 17,88,618.00 Cr

06.12.07 06.12.07 BY CASH 49,500.00 18,38,118.00 Cr

07.12.07 07.12.07 BY CASH 49,500.00 18,87,618.00 Cr

08.12.07 08.12.07 BY CASH 49,500.00 19,37,118.00 Cr

31.12.07 31.12.07 BY INTT 15,275.00 19,52,393.00 Cr

02.02.08 02.02.08 TO SELF 1,50,000.00 18,02,393.00 Cr Paid to SELF-3804

13.02.08 13.02.08 TO SELF 2,00,000.00 16,02,393.00 Cr Paid to SELF-3810-1”

There is nothing on the record to show that the assessee was maintaining any other bank account.

Since the above deposits were made by the assessee in cash, the assessing officer asked him to explain the source thereof. The assessee submitted that the above deposits were the result of sales effected by him. A few bills were produced. After considering the entire matter, the assessing officer found that the source of the afore-detailed cash deposits had not been satisfactorily explained by the assessee. Complete sale/purchase bills had not been produced. Photocopies of few bills which had been produced were those which had been issued during the current year only. The account details further did not show any withdrawals made by the assessee till February, 2008. The assessee failed to tell the names of the parties from whom he purchased the material/furniture for sale. Accordingly, invoking the provisions of Section 69A (of Income Tax Act, 1961), cash amounting to Rs.18,31,500/- deposited by the assessee, in his bank account, was ordered to be added to his income.

The assessee challenged the re-assessment order by filing an appeal before the Commissioner, Income Tax (Appeals), Patiala (for short the 'Commissioner'), who rejected the plea of the assessee with regard to the challenge to the very initiation of the re-assessment proceedings. The assessee had raised a ground that the assessing officer had not recorded any reasons but the Commissioner found the same to be duly recorded. The Commissioner further held that the assessee declared his income under Section 44AF (of Income Tax Act, 1961) and, thus, was not required to maintain books of accounts and explain each entry. After relying upon a judgment of this Court in CIT vs. Surinder Pal Anand (2010) 48 DTR 135 (P&H), the Commissioner allowed the assessee's appeal and ordered deletion of the amount of Rs.18,31,500/- as ordered to be added to his income by the assessing officer.

The order of the Commissioner led to the filing of the cross- appeals before the Tribunal. After considering the record and the orders passed by the assessing officer as also the Commissioner, the Tribunal decided the issues raised before it against the assessee. It was held that when the assessing officer had sought from the assessee the source of the cash deposits to the tune of Rs.18,31,500/- made by him in his bank account,virtually no documentary proof regarding purchases/sale of furniture was submitted by him. Photocopies of only a few of the bills which were produced pertained to the current year only. The names of the parties from whom the assessee had purchased the material were not disclosed. The Tribunal noted that throughout the year, on different dates the assessee had made deposits of identical amounts of Rs.49,500/- and it was only at the fag end of the financial year i.e. on 02.02.2008 and 13.02.2008 that the assessee had made withdrawals of Rs.1,50,000/- and Rs.2,00,000/-. The assessee was also found to have failed to prove any purchases made by him from his withdrawals especially when these withdrawals were made only in February,2008 i.e. at the fag end of the financial year. The Tribunal further noted that in his return, the assessee had shown sales of Rs.18,82,800/- with net profit of Rs.1,08,000/- and with this low profit margin, without making purchases no sale could have possibly been effected by the assessee. Thus, the cash deposited by the assessee in his bank account was not believed to be from sales effected by him.

The assessee's plea that he usually purchased furniture on credit basis was also considered and rejected as no evidence of making any purchases on credit had been filed by him before any of the authorities. The assessee was also found to have established no nexus with the receipts/turn over and the deposited cash in his bank account. Link evidence to show that the sales were directly related to the cash deposits made by him in his bank account, was also found missing by the Tribunal.

In view of the afore-referred facts, the Tribunal held that the assessee's case was distinguishable from Surinder Pal Anand's case (supra).

Accordingly, the appeal of the revenue was allowed and the addition made by the assessing officer was restored.

After going through the order of the Tribunal, we find that the Tribunal has essentially decided questions of fact and while doing so it has arrived at views which could have possibly be taken. The order of the Tribunal, thus, cannot be termed as perverse or absurd. No question of law much less any substantial question of law arise in the present appeal. Thus, the same is dismissed.

[ S.J. VAZIFDAR ]

CHIEF JUSTICE

27th September, 2016 [ DEEPAK SIBAL ]

shamsher JUDGE

Whether reasoned/speaking : Yes / No

Whether reportable : Yes / No

×