Tax Tribunal's ruling on dividend income and zero coupon bonds upheld by High C…

Full News

Tax Tribunal's ruling on dividend income and zero coupon bonds upheld by High Court

Tax Tribunal's ruling on dividend income and zero coupon bonds upheld by High Court

The Income Tax Department (the revenue) filed appeals against M/s. Syndicate Bank (the assessee) regarding certain tax issues. The High Court heard these appeals and ultimately dismissed them, siding with the bank on key points related to dividend income and the application of certain tax provisions.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax and Anr Vs M/s. Syndicate Bank (High Court of Karnataka)

ITA No. 97 of 2010 C/W ITA No.99 of 2010

Date: 17th January 2020

Key Takeaways:

1. Section 14A (of Income Tax Act, 1961) doesn't apply when no actual expenditure is incurred to earn exempt income.

2. The court confirmed that Section 115JA (of Income Tax Act, 1961) (Minimum Alternate Tax) doesn't apply to banking companies.

3. The court upheld that Rule 8D (of Income Tax Rules, 1962) can't be applied retrospectively before the 2008-09 assessment year.

Issue:

The main question was whether the Income Tax Appellate Tribunal (ITAT) was correct in its rulings on various tax matters, particularly regarding the application of Section 14A (of Income Tax Act, 1961) and Section 115JA (of Income Tax Act, 1961) to the assessee's income.

Facts:

1. M/s. Syndicate Bank filed a tax return for the assessment year in question, declaring a certain amount as book profit under Section 115JA (of Income Tax Act, 1961).

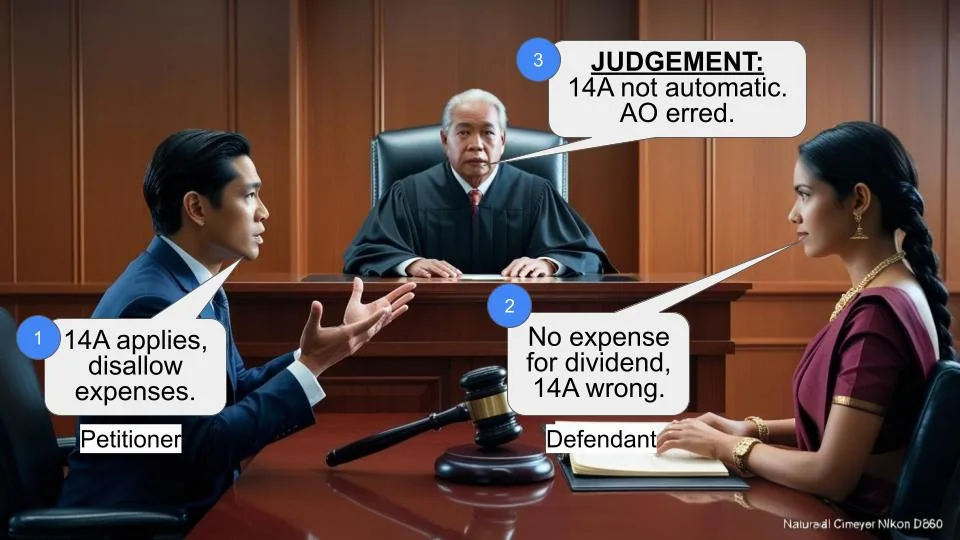

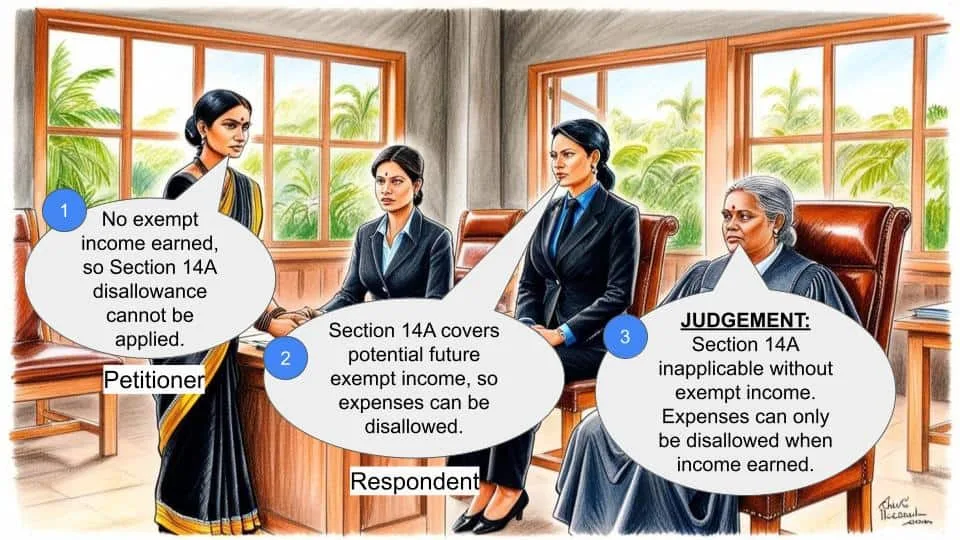

2. The Assessing Officer made some additions to the taxable income, including disallowing expenses related to dividend income under Section 14A (of Income Tax Act, 1961).

3. The bank appealed these decisions, and the case went through various stages of appeal before reaching the High Court.

Arguments:

The revenue (tax department) argued:

1. Section 14A (of Income Tax Act, 1961) should apply even without actual expenditure being incurred.

2. Provisions of Section 115JA (of Income Tax Act, 1961) should apply to the bank's profits.

The assessee (the bank) countered:

1. No expenditure was actually incurred to earn the dividend income, so Section 14A (of Income Tax Act, 1961) shouldn't apply.

2. Section 115JA (of Income Tax Act, 1961) doesn't apply to banking companies.

Key Legal Precedents:

The court relied on several important cases:

1. 'COMMISSIONER OF INCOME TAX VS. WALFORT SHARE & STOCK BROKERS (P) LTD.', (2010) 326 ITR 1

2. 'MAXOPP INVESTMENT LTD. VS. COMMISSIONER OF INCOME TAX, NEW DELHI', (2018) 402 ITR 640 (SC)

3. 'CIT VS. ESSAR TELEHOLDINGS LTD.', (2018) 401 ITR 445

These cases helped establish that Section 14A (of Income Tax Act, 1961) requires actual expenditure and that certain tax rules can't be applied retrospectively.

Judgement:

The High Court dismissed the revenue's appeals, agreeing with the ITAT's decisions. Here's the breakdown:

1. Section 14A (of Income Tax Act, 1961) doesn't apply here because the bank didn't actually spend money to earn the dividend income.

2. The court confirmed its earlier ruling that Section 115JA (of Income Tax Act, 1961) doesn't apply to banking companies.

3. The court agreed that Rule 8D (of Income Tax Rules, 1962) can't be applied to assessment years before 2008-09.

FAQs:

Q1: What does Section 14A (of Income Tax Act, 1961) deal with?

A1: It disallows deduction of expenses incurred to earn tax-exempt income.

Q2: Why didn't Section 14A (of Income Tax Act, 1961) apply in this case?

A2: Because the bank didn't actually spend any money to earn the dividend income.

Q3: What's the significance of the ruling on Section 115JA (of Income Tax Act, 1961)?

A3: It confirms that banking companies are exempt from the Minimum Alternate Tax provisions under this section.

Q4: What's the takeaway regarding Rule 8D (of Income Tax Rules, 1962)?

A4: It can't be applied retrospectively to assessment years before 2008-09.

Q5: How might this judgment affect other banks or financial institutions?

A5: It could provide a precedent for similar cases involving dividend income and the application of these tax provisions to banks.

1. These appeals under Section 260-A (of Income Tax Act, 1961), 1961 (hereinafter referred to as ‘the Act’, for short) have been filed by the revenue. ITA No.97/2010 was admitted by a bench of this court on the following substantial questions of law:

(i) Whether the Tribunal was correct in holding that the estimation of expenditure in respect of administrative or financial cost at 5% of dividend income earned by the Assessing Officer in accordance with Section 14A (of Income Tax Act, 1961) cannot be disallowed?

(ii) Whether the provisions of the Section 14A (of Income Tax Act, 1961) r/w Rule 8D (of Income Tax Rules, 1962) should be made applicable to all pending matters as the same is clarificatory in nature in view of the consistent stands taken by the department?

(iii) Whether the Tribunal was correct in holding that the estimated expenditure cannot be treated as book profit under Section 115JA (of Income Tax Act, 1961) despite Explanation (f) to Section 115JA (of Income Tax Act, 1961)?

(iv) Whether the Tribunal was correct in holding that the provision towards (i) doubtful debts (ii) standard assets (iii) depreciation on securities (iv) floating rate notes of London branch (v) DICGC loans (vi) suits filed accounts (vii) miscellaneous provision cannot be added back in accordance with Explanation of Section 115JA (of Income Tax Act, 1961) in the light of the judgment of the Apex court in H.C.L. Comnet when there is diminution in the value of assets as contended by the assessee and in view of the retrospective amendment to Explanation (g) to Section 115JA (of Income Tax Act, 1961)?

(v) Whether the Tribunal was correct in holding that the Assessing Officer cannot add the interest on zero coupon bonds to chargeable book profits by invoking explanation to Section 115JA(2) (of Income Tax Act, 1961)?

2. ITA No.99/2010 was admitted by a bench of this court on the following substantial question of law:

(i) Whether the appellate authorities were correct in holding that interest on zero coupen bonds cannot be reduced in arriving at Book Profit for the purpose of Section 115JB (of Income Tax Act, 1961), when Section 115JB (of Income Tax Act, 1961) (prior to amendment) allows reduction of any income credited to P & L account, which is covered by Sections 10, 10A, 10B 11 or 12 of the Act?

3. On account of similarity of the issues involved in the substantial questions of law, they were heard analogously and are being decided by this common judgment. For the facility of reference, facts from ITA No.97/2010 are being referred to.

4. The assessee filed a return of income on 28.11.2000 declaring gross total income of Rs.2,23,249/-. The assessee declared Rs.2,06,92,53,033/- as book profit under Section 115JA (of Income Tax Act, 1961). The return was processed under Section 143(1) (of Income Tax Act, 1961) resulting in refund of Rs.10,62,37,618/-. Thereafter a notice was issued under Section 143(2) (of Income Tax Act, 1961). The Assessing Officer by an order dated 31.12.2002 inter alia held that since exempted dividend does not form part of income, the assessee is not entitled to disallowance of proportionate expenses as required under Section 14A (of Income Tax Act, 1961). Accordingly, an addition of Rs.20,38,002/- was made by the Assessing Officer. The aforesaid order was upheld in appeal by the Commissioner of Income Tax (Appeals). Being aggrieved, the assessee filed an appeal before the Income Tax Tribunal. The Tribunal vide impugned order dated 09.10.2009 inter alia held that since, the business of the assessee is in the nature of indivisible, the expenditure cannot be disallowed. Accordingly, the claim of the appellant under Section 14A(1) (of Income Tax Act, 1961) was allowed. The claim of the assessee for interest on zero coupon bonds being purely notional income was also excluded form the book profit for the purposes of computation of Minimum Alternative Tax. Being aggrieved, the revenue has filed these appeals before this court.

5. Learned counsel for the revenue submitted that the finding recorded by the Income Tax Appellate Tribunal that in the absence of sub-Sections (2) and (3) of the Act, the provisions of Section 14A(1) (of Income Tax Act, 1961) cannot be applied is perverse. It is further submitted that the liability to pay the tax arises under the provisions of Section 14A(1) (of Income Tax Act, 1961). It is submitted that sub- Sections (2) & (3) were incorporated in Section 14A (of Income Tax Act, 1961) by Finance Act, 2006 with effect from 01.04.2007.

However, even prior to amendment, the Assessing Officer had to assess the total income on the basis of best judgment assessment. It is pointed out that basic reason for insertion of Section 14A (of Income Tax Act, 1961) is that certain incomes are includable while computing total income as they are exempt under certain provisions of the Act. It is further submitted that there is a proximate cause for disallowance, which is in relationship with Tax exempt income under Section 14A (of Income Tax Act, 1961). In support of aforesaid submissions, reliance has been placed on decision of the Supreme Court in ‘COMMISSIONER OF INCOME TAX VS. WALFORT SHARE & STOCK BROKERS (P) LTD.’, (2010) 326 ITR 1, ‘GODREJ & BOYCE MANUFACTURING COMPANY LTD. VS. DEPUTY COMMISSIONER OF INCOME-TAX’, (2017) 394 ITR 449 and ‘MAXOPP INVESTMENT LTD. VS. COMMISSIONER OF INCOME TAX, NEW DELHI’, (2018) 402 ITR 640 (SC)’. It is fairly submitted by the learned counsel for the revenue that substantial question of law Nos.1 and 3 are interlinked. While inviting the attention of this Court to Explanation to Section 115JA (of Income Tax Act, 1961), it is submitted that in the assessee’s appeal with reference, to explanation to Section 115JA(c) (of Income Tax Act, 1961) namely ITA No.164/2009 dated 04.12.2018, the matter was remitted. Therefore, the issue involved in substantial question of law Nos.4 and 5 be remitted for fresh consideration to the Commissioner of Income Tax (Appeals).

6. On the other hand, learned counsel for the assessee has submitted that in order to attract the applicability of Section 14A (of Income Tax Act, 1961), there has to be a pay out i.e., an assessee has to incur expenditure. While inviting the attention of this Court to paragraph 17 of the decision in the case of WALFORT supra, it is pointed out that expenditure is a pay out and pay back is not expenditure in the scheme of Section 14A (of Income Tax Act, 1961). It is further submitted that condition precedent for invoking Section 14A (of Income Tax Act, 1961) is pay out. In the instant case, since the assessee has not incurred any expenditure, therefore, the provisions of Section 14A (of Income Tax Act, 1961) do not apply to the fact situation of the case.

7. It is also argued that a division bench of Punjab & Haryana High Court in ‘PRINCIPAL COMMISSION OF INCOME TAX VS. STATE BANK OF PATIALA (2017) 78 TAXMANN.COM 3 (PUNJAB & HARYANA) has held that return of investment would not fall within the expression “expenditure incurred” under Section 14A (of Income Tax Act, 1961). It is further submitted that when no expenditure is incurred by the assessee in earning dividend income, no notional expenditure could be deducted from the income. Learned counsel for the assessee has also referred to the order dated 16.10.2019 passed by division bench of Delhi High Court in, PRINCIPAL COMMISSIONER OF INCOME TAX-7 VS. M/S PUNJAB AND SINDH BANK, wherein by placing reliance on the decision of the Supreme Court in MAXOPP INVESTMENT PVT LTD supra, the Delhi High Court held that the assessee had earned the revenue on the shares held as stock in trade only by quirk of fate and held that no substantial question of law is involved.

It is further submitted that the Supreme Court had initially granted leave to file an appeal against the aforesaid order. However, the appeal preferred by the revenue was subsequently dismissed. Therefore, in view of law laid down by the Supreme Court in case of MAXOPP INVESMENT LTD, as well as WALFORT supra, the first substantial question of law deserves to be answered in favour of the assessee. It is also argued that since this court by an order passed on 16.01.2020 in ITA No.18/2014 has held that the provisions of Section 115JA (of Income Tax Act, 1961) do not apply to the Banking Company, therefore, the remaining issues are rendered academic.

8. We have considered the submissions made by learned counsel for the parties and have perused the record. Before proceeding further, it is apposite to take note of Section 14A (of Income Tax Act, 1961):

Section 14A(1) (of Income Tax Act, 1961) For the purposes of computing the total income under this Chapter, no deduction shall be allowed in respect of expenditure incurred by the assessee in relation to income which does not form part of the total income under this Act.

(2) The Assessing Officer shall determine the amount of expenditure incurred in relation to such income which does not form part of the total income under this Act in accordance with such method as may be prescribed, if the Assessing Officer, having regard to the accounts of the assesee, is not satisfied with the correctness of the claim of the assessee in respect of such expenditure in relation to income which does not form part of the total income under this Act.

(3) The provisions of sub-Section (2) shall also apply in relation to a case where an assesee claims that no expenditure has been incurred by him in relation to income which does not form part of the total income under this Act.

Provided that nothing contained in this Section shall empower the Assessing Officer either to reassess under Section 147 (of Income Tax Act, 1961) or pass an order enhancing the assessment or reducing a refund already made or otherwise increasing the liability of the assessee under Section 154 (of Income Tax Act, 1961), for any assessment year beginning on or before the 1st day of April 2001.

9. From perusal of Section 14A (of Income Tax Act, 1961), it is evident that for the purposes of computing the total income under this chapter, no deduction shall be allowed in respect of the expenditure incurred by the assessee in relation of the income which does not form part of his total income under the Act. The expenditure, the return of investment and cost of requisition are distinct concepts. Therefore the word ‘incurred’ in Section 14A (of Income Tax Act, 1961) have to be read in the context of the scheme of the Act and if so read, it is clear that it disallows certain expenditures incurred to earn exempt income from being deducted from other incomes which is includable in the total income for the purposes of chargeability to the tax. It is equally well settled that expenditure is a pay out. In order to attract applicability of section 14A (of Income Tax Act, 1961), there has to be a pay out and return of investment or a pay back is not such a debit item. [See: WALFORT SHARE AND STOCK BROKERS (P) LTD SUPRA as well as MAXOP INVESTMENTS LTD SUPRA]. In the instant case, the assessee has admittedly not incurred any expenditure. This case pertains to income on dividend, which by no stretch of imagination can be treated to be an expenditure to attract the provisions of Section 14A (of Income Tax Act, 1961). In view of aforesaid enunciation of law by the Supreme Court, the first substantial question of law framed by this court is answered in favour of the assessee and against the revenue.

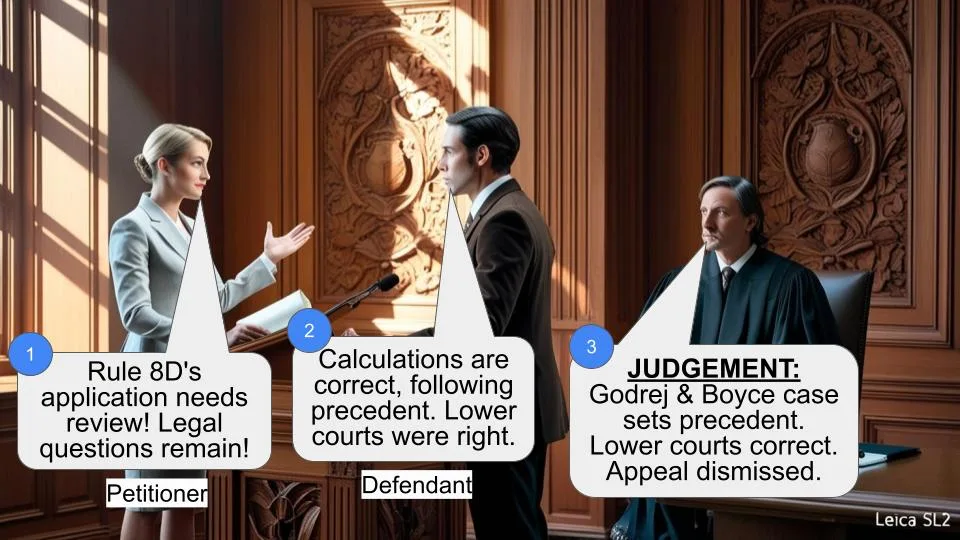

10. Learned counsel for parties, have fairly admitted that in case this court frames a substantial question of law that whether provisions of Section 115JA (of Income Tax Act, 1961) apply to the Banking Companies are not the remaining substantial questions of law would be reduced otiose. This court has already framed a substantial question of law in this regard today. This court by an order passed on 16.01.2020 passed in ITA No.18/2014 has already held that the provisions of Section 115JA (of Income Tax Act, 1961) do not apply to the banking companies. Therefore, the substantial questions of law Nos.3, 4 and 5 and substantial question of law framed in ITA 99/2010 are rendered academic and need not be answered. So far as substantial question of law No.2 in ITA No.97/2010 is concerned, the same is squarely covered by the decision of the Supreme Court in ‘CIT VS. ESSAR TELEHOLDINGS LTD.’, (2018) 401 ITR 445, wherein it has been held that provisions of Section 114A (of Income Tax Act, 1961) read with rule 8D (of Income Tax Rules, 1962) are prospective in nature and can not be applied to any assessment year prior to Assessment Year 2008-09. Accordingly, the aforesaid substantial question of law is answered against the revenue and in favour of the assessee.

In view of preceding analysis, the appeals fail and are hereby dismissed.

Sd/-

JUDGE

Sd/-

JUDGE

×

Similar Ripples

Questions

Tax Tribunal's ruling on dividend income and zero coupon bonds upheld by High Court

Write your CommentSimilar Posts

Generic

- Reportdata/6118.pdf