TDS Deduction Dispute: Tribunal Favors Assessee Over Revenue

Full News

TDS Deduction Dispute: Tribunal Favors Assessee Over Revenue

TDS Deduction Dispute: Tribunal Favors Assessee Over Revenue

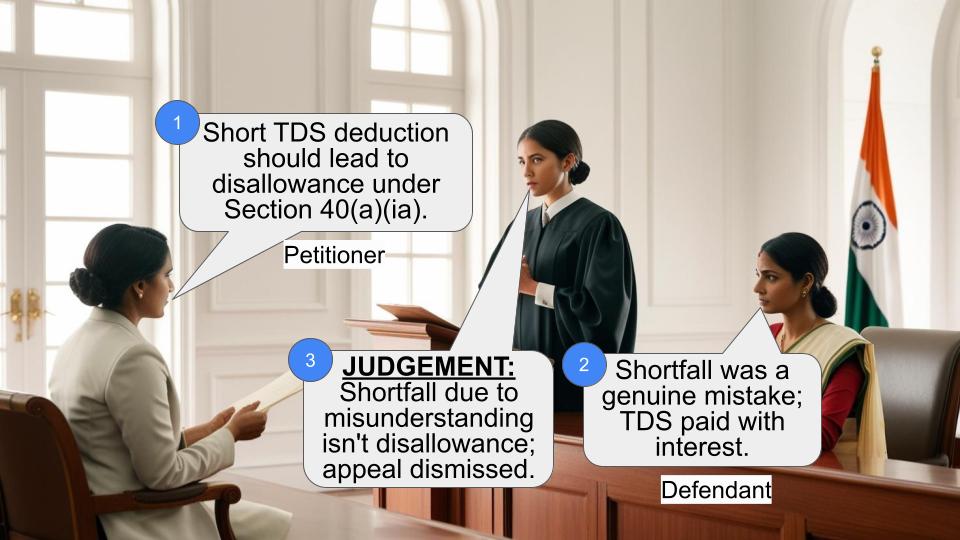

In this case, the Revenue appealed against a decision favoring the assessee, who had made a short deduction of tax at source. The central issue was whether the disallowance of expenditure under Section 40(a)(ia) (of Income Tax Act, 1961) was justified. The court upheld the Tribunal's decision, which relied on a precedent from the Calcutta High Court, ruling that a shortfall in TDS due to a bona fide misunderstanding does not warrant disallowance.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax and Another vs. Kishore Rao and Others (HUF) (High Court of Karnataka)

ITA No. 660 of 2015

Date: 17th March 2016

Key Takeaways:

- The court emphasized that a shortfall in TDS due to a bona fide misunderstanding does not lead to disallowance under Section 40(a)(ia) (of Income Tax Act, 1961).

- The decision relied heavily on the precedent set by the Calcutta High Court in the case of S.K. Tekriwal.

- The ruling clarifies that the provisions of Section 40(a)(ia) (of Income Tax Act, 1961) apply only in cases of non-deduction, not short deduction.

Issue

Is the disallowance of expenditure under Section 40(a)(ia) (of Income Tax Act, 1961) justified when there is a shortfall in TDS due to a bona fide misunderstanding?

Facts

The assessee deducted TDS at 1% instead of the required 2% on certain payments. Upon realizing the mistake, the assessee paid the balance TDS with interest. The Revenue argued for disallowance of the expenditure under Section 40(a)(ia) (of Income Tax Act, 1961), while the assessee contended that the shortfall was due to a misunderstanding.

Arguments

- Revenue's Argument: The Revenue contended that the short deduction of TDS warranted disallowance under Section 40(a)(ia) (of Income Tax Act, 1961) as the deduction was not in accordance with the provisions.

- Assessee's Argument: The assessee argued that the shortfall was due to a bona fide misunderstanding and that the balance TDS was paid with interest, thus disallowance was not justified.

Key Legal Precedents

- S.K. Tekriwal Case: The Calcutta High Court held that a shortfall in TDS due to a misunderstanding does not lead to disallowance under Section 40(a)(ia) (of Income Tax Act, 1961) if the TDS is eventually paid.

- Section 40(a)(ia) (of Income Tax Act, 1961): This section deals with disallowance of expenditure for non-deduction of TDS.

Judgement

The court dismissed the Revenue's appeal, upholding the Tribunal's decision that no disallowance can be made under Section 40(a)(ia) (of Income Tax Act, 1961) for a shortfall in TDS due to a bona fide misunderstanding. The court found no substantial question of law in the Revenue's appeal.

FAQs

Q1: What does this judgment mean for taxpayers?

A1: It clarifies that a shortfall in TDS due to a genuine misunderstanding does not automatically lead to disallowance of expenditure under Section 40(a)(ia) (of Income Tax Act, 1961).

Q2: How does this affect the application of Section 40(a)(ia) (of Income Tax Act, 1961)?

A2: The judgment limits the application of Section 40(a)(ia) (of Income Tax Act, 1961) to cases of non-deduction, not short deduction, of TDS.

Q3: What was the role of the S.K. Tekriwal case in this judgment?

A3: The S.K. Tekriwal case was pivotal as it set a precedent that a shortfall due to misunderstanding does not warrant disallowance, which the court relied upon in this judgment.

Revenue has preferred the present appeal by raising the following substantial questions of law:

“Whether, on the facts and in the circumstances of the case, the Tribunal is

right in law in holding that disallowance of expenditure claimed by the assessee towards payments amounting to Rs.3,42,86,912/- under Section 40(a)(ia) (of Income Tax Act, 1961) is not proper by relying upon the decision which is not applicable to facts of the present case and when the ingredients of Section 194H (of Income Tax Act, 1961) and 40(a) (ia) are satisfied in the instant case?

2, We have heard Mr.Arvind, learned counsel appearing for appellant-Revenue.

3. The relevant discussion in the impugned order of the Tribunal on the aforesaid aspect is at paragraphs 5.3 to 5.3.3 which read as under:

“5.3.1 We have heard the rival contentions

on the ground at S.No.5 and perused and

carefully considered the material on record;

including the judicial pronouncements cited

and placed reliance upon. It is not in dispute

that the assessee had made short deduction

of tax at source @ 1% instead of 2% on certain

payments and failed to remit the said TDS

within the due date of filing the return of

income for Assessment Year 2010-11 under

Section 139(1) (of Income Tax Act, 1961). On examination by

the Assessing Officer, the assessee explained

that subsequently, on realisation that TDs on

the said payments were to be made @ 2%

thereon, instead of 1% as had been done by

the assessee, the balance TDS was paid on

31.1.2011 along with interest under Section

201(1A) of the Act. The Assessing Officer, on

examination of the assessee's claim, was of

the view that deduction of tax at a lower rate

cannot be taken as TDS made in accordance

with the provisions of Chapter XVII-B and,

following the decisions of the Chennai ITAT in

the case of Frontier Offshore Exploration (I)

Ltd. (supra) and Pixie Enterprises (supra),

held that even in case of short deduction, the

liability to deduct tax exists as on the date of

filing the return of income and therefore those

amounts which have not suffered TDS was

liable to disallowance under Section 40(a)(ia) (of Income Tax Act, 1961)

of the Act. On appeal, the learned CIT

(Appeals) upheld the decision of the

Assessing Officer.

5.3.2 According to the learned Authorised

Representative if, as in the case on hand,

there is any shortfall in deduction of tax at

source due to any difference in understanding

or opinion as to the taxability of any payment

or the nature of payments made under TDS

provisions, no disallowance can be made by

invoking the provisions of Section 40(a)(ia) (of Income Tax Act, 1961) of

the Act. We have had occasion to peruse the

decision of the Hon'ble High Court of Calcutta

in the case of S.K. Tekriwal (supra), wherein

their Lordships had considered the very same

issue of the applicability of the provisions of

Section 40(a)(ia) (of Income Tax Act, 1961) in a case where

there was short deduction of tax at source on

payments made to sub-contractors and find

that the facts of that case are similar to those

of the case on hand. In the cited case, the

Hon'ble Calcutta High Court has held that if

there is any shortfall in deduction of tax due

to difference in opinion or understanding as to

the taxability of any item or nature of

payments falling under various TDS

provisions, no disallowance can be made by

invoking the provisions of Section 40(a)(ia) (of Income Tax Act, 1961) of

the Act. We are of the considered view that

the cited case would cover the issue squarely

in favour of the assessee and against

Revenue. At paras 2 and 3 of its order, the

Hon'ble High Court of Calcutta has held as

under :-

“2. The reasoning appearing at paragraph 6

of the judgment and/or order under challenge

reads as follows:

“In the present case before us the assessee

has deducted tax under Section 194C(2) (of Income Tax Act, 1961) of

the Act being payments made to sub-

contractors and it is not a case of non-

deduction of tax or no deduction of tax as is

the import of section 40a(ia) (of Income Tax Act, 1961). But

the revenue’s contention is that the payments

are in the nature of machinery hire charges

falling under the head ‘rent’ and the previous

provisions of section 194I (of Income Tax Act, 1961) are

applicable. According to revenue, the

assessee has deducted tax @ 1% 2 under

Section 194C(2) (of Income Tax Act, 1961) as against the

actual deduction to be made at 10% under

Section 194I (of Income Tax Act, 1961), thereby lesser

deduction of tax. The revenue has made out a

case of lesser deduction of tax and that also

under different head and accordingly

disallowed the payments proportionately by

invoking the provisions of section 40(a)(ia) (of Income Tax Act, 1961) of

the Act. The ld. CIT, DR also argued that there

is no word like failure used in section 40(a)(ia) (of Income Tax Act, 1961)

of the Act and it referred to only non-

deduction of tax and disallowance of such

payments. According to him, it does not refer

to genuineness of the payment or otherwise

but addition under section 40(a)(ia) (of Income Tax Act, 1961)

can be made even though payments are

genuine but tax is not deducted as required

under section 40(a)(ia) (of Income Tax Act, 1961). We are of

the view that the conditions laid down under

section 40(a)(ia) (of Income Tax Act, 1961) for making addition

is that tax is deductible at source and such

tax has not been deducted. If both the

conditions are satisfied then such payment

can be disallowed under section 40(a)(ia) (of Income Tax Act, 1961) of

the Act but where tax is deducted by the

assessee, even under bonafide wrong

impression, under wrong provisions of TDS,

the provisions of section 40(a)(ia) (of Income Tax Act, 1961)

cannot be invoked.

Here in the present case before us, the

assessee has deducted tax under Section

194C(2) of the Act and not under Section 194I (of Income Tax Act, 1961)

of the Act and there is no allegation that this

TDS is not deposited with the Government

account. We are of the view that the

provisions of section 40(a)(ia) (of Income Tax Act, 1961) has

two limbs one is where, inter alia, assessee

has to deduct tax and the second where after

deducting tax, inter alia, the assessee has to

pay into Govt. Account. There is nothing in the

said section to treat, inter alia, the assessee

as defaulter where there is a shortfall in

deduction. With regard to the shortfall, it

cannot be assumed that there is a default as

the deduction is not as required by or under

the Act, but the facts is that this expression,

on which tax is deductible at source under

Chapter XVII-B and such tax has not been

deducted or, after deduction has not been

paid on or before the due date specified in

sub-section 3(1) (of Income Tax Act, 1961) of section 139 (of Income Tax Act, 1961). This section

40(a)(ia) of the Act refers only to the duty to

deduct tax and pay to government account. If

there is any shortfall due to any difference of

opinion as to the taxability of any item or the

nature of payments falling under various TDS

provisions, the assessee can be declared to

be an assessee in default under Section 201 (of Income Tax Act, 1961)

of the Act and no disallowance can be made

by invoking the provisions of section 40(a)(ia) (of Income Tax Act, 1961)

of the Act.

Accordingly, we confirm the order of CIT

(Appeals) allowing the claim of assessee and

this issue of revenue’s appeal is dismissed.”

3. We find no substantial question of law is

involved in this case and therefore, we refuse

to admit the appeal. Accordingly, the appeal

is dismissed.”

5.3.3 Respectfully following the decision of

the Hon’ble High Court of Calcutta in the case

of S.K. Tekriwal (supra), which is factually

similar to the case on hand, we hold that no

disallowance can be made by invoking the

provisions of Section 40(a)(ia) (of Income Tax Act, 1961) if

there was any shortfall in deduction of tax at

source due to any difference of understanding

or opinion as to the taxability of any item or

the nature of payments falling under various

TDS provisions and therefore reverse the

findings of the authorities below and allow

the assessee’s appeal in respect of Ground

No.5.”

The aforesaid shows that the Tribunal has gone by the

decision taken by the High Court of Calcutta and has

found that it was not a case of no deduction of TDS

whatsoever and therefore, the provisions of Section

40(a) and (ia) of the Act cannot be attracted and

resultantly the assessee’s appeal has been allowed.

4. However, Mr.Aravind, learned counsel

appearing for appellant contended that the decision of

Calcutta High Court in case of Commissioner of IT vs.

S.K.Tekriwal reported in (2014) 361 ITR 432(Cal.) is

wrongly applied by the Tribunal. The facts of the case

in the decision of Calcutta High Court were altogether

different. He submitted that, in the said case, the TDS

was deducted at a lesser percentage but the payment

was credited in the Revenue in time whereas, in the

present case, the TDS was deducted at a lesser rate but

no payment was credited with the revenue in time.

5. He submitted that, as per Scheme of Sec.40(a) (of Income Tax Act, 1961)

(ia) of the Act read with proviso, if no deduction is made,

the amount is disallowable as revenue expenditure and

if TDS is made succeeding year, it would be admissible

in that year and not the year in which the claim has

been made. In his submission, the decision of Calcutta

High Court in case of S.K.Tekriwal has not laid down

that, if the deduction is at a lesser percentage than

required, then expenses cannot be disallowed. In his

submission, the Tribunal has committed an error and

hence this Court may consider the matter.

6. In our view, as per the decision of the Calcutta

High Court, the view taken by the Tribunal is that

Section 40(a)(ia) (of Income Tax Act, 1961) may be invoked only in case

of there being an absence of deduction. Further, in case

of bona fide wrong impression, if the deduction is at a

lesser rate, the same cannot be a ground for

disallowance by invoking the provisions of Section

40(a)(ia).

7. Examining the matter, we find that there are

two angles to the matter: The first is, whether it was a

case of `no deduction’ or not in the present case. The

answer would be in the negative because, the deduction

was already made at the rate of 1%. The second angle

would be as to whether it was under a bona fide wrong

impression that only 1% was deducted instead of 2%.

The contention of the assessee was that, having realized

that deduction was 2% instead of 1%, the amount of

TDS has been paid with interest. It is also a matter of

fact that, two separate rate of deductions have been

provided for the same work of contractor, one is at the

rate of 1% if the contractor is individual or HUF,

whereas, it is 2% if the contractor is other than

individual or HUF. The Tribunal, in view of facts and

circumstances, found that, it is a bona fide wrong

impression.

8. As such, on the aspects of the bona fide wrong

impression keeping in view the contention of the

assessee that in the middle of year, there is change of

law about the deduction, as well as on the non-

availability of the provisions of Section 40(a)(ia) (of Income Tax Act, 1961), when

the issue is covered by the Calcutta High Court

Judgment in case of S.K.Tekriwal supra, we do not find

that any substantial question of law would arise for

consideration as sought to be canvassed.

Hence, the appeal is dismissed.

Sd/-

JUDGE

Sd/-

JUDGE

×

Similar Ripples

Questions

TDS Deduction Dispute: Tribunal Favors Assessee Over Revenue

Write your CommentSimilar Posts

Generic

- Reportdata/2996.pdf