Treaty trumps tax: Court favors DTAA over Income Tax Act in software royalty ca…

Full News

Treaty trumps tax: Court favors DTAA over Income Tax Act in software royalty case

Treaty trumps tax: Court favors DTAA over Income Tax Act in software royalty case

This case involves the Revenue (tax authorities) appealing against an order by the Income Tax Appellate Tribunal (ITAT) regarding the taxation of income from the sale of pre-packaged software. The main question was whether this income should be classified as royalty/fee for technical services or as business income. The Delhi High Court dismissed the Revenue's appeal, affirming that the Double Taxation Avoidance Agreement (DTAA) between India and the USA takes precedence over the Income Tax Act when it's more beneficial to the assessee.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs Commissioner of Income Tax (High Court of Delhi)

ITA 363, 365/2016

Date: 11th July 2016

Key Takeaways:

1. The DTAA prevails over the Income Tax Act when it's more beneficial to the assessee.

2. Sale of pre-packaged software is not considered royalty under the India-USA DTAA.

3. There's a clear distinction between transfer of copyright rights and transfer of copyrighted articles.

4. The court reaffirmed its previous decision in DIT v. Infrasoft Limited.

Issue:

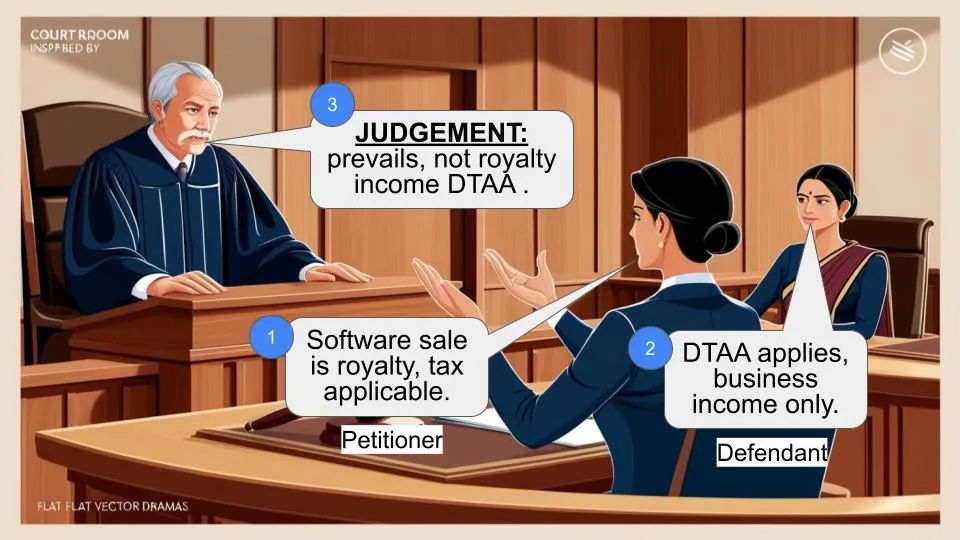

Is the consideration received by the Assessee on the sale of pre-packaged software taxable as 'royalty' or 'fee for technical services' under the India-USA DTAA, or should it be treated as business income?

Facts:

- The case concerns Assessment Years 2009-10 and 2010-11.

- The Assessee sold pre-packaged software.

- The Revenue argued that the income from this sale should be classified as royalty or fee for technical services.

- The ITAT had ruled in favor of the Assessee, and the Revenue appealed to the High Court.

- A similar issue for the same Assessee was decided for AY 2008-09 in ITA No. 477 of 2014.

Arguments:

Revenue's Argument:

- The consideration from the sale of pre-packaged software should be treated as royalty or fee for technical services.

- They sought to emphasize the impact of the amendment to Section 9(1)(vi) (of Income Tax Act, 1961).

Assessee's Argument (implied):

- The income should be treated as business income under the DTAA.

- The DTAA provisions are more beneficial and should prevail over the Income Tax Act.

Key Legal Precedents:

1. DIT v. Infrasoft Limited (ITA No. 1034 of 2009)

- This case established that the sale of pre-packaged software doesn't constitute royalty under the DTAA.

- It distinguished between "copyright rights" and "copyrighted articles".

2. ITA No. 477 of 2014 (Assessee's own case for AY 2008-09)

- This previous case involving the same Assessee had already decided the issue in favor of the Assessee.

Judgement:

1. The court dismissed the Revenue's appeal.

2. It reaffirmed that under Section 90(3) (of Income Tax Act, 1961), when the DTAA provisions are more beneficial to the Assessee, they prevail over the Act.

3. The court relied on its previous decision in DIT v. Infrasoft Limited, which had thoroughly examined the issue.

4. The court concluded that the sale of pre-packaged software doesn't amount to the transfer of copyright rights and thus isn't royalty under the DTAA.

5. The court declined to re-examine the issue of the amendment to Section 9(1)(vi) (of Income Tax Act, 1961), as the DTAA provisions were more beneficial to the Assessee.

FAQs:

1. Q: What's the difference between a "copyright right" and a "copyrighted article"?

A: A copyright right involves the transfer of rights related to the copyright itself, while a copyrighted article is simply a product that contains copyrighted material. Selling a copyrighted article (like pre-packaged software) doesn't transfer any copyright rights.

2. Q: Why didn't the court consider the amendment to Section 9(1)(vi) (of Income Tax Act, 1961)?

A: The court didn't need to examine this because the DTAA provisions were more beneficial to the Assessee, and in such cases, the DTAA prevails over the Act.

3. Q: Does this judgment apply to all software sales?

A: This judgment specifically applies to pre-packaged software sales under the India-USA DTAA. Other scenarios might be treated differently.

4. Q: What's the significance of this judgment for software companies?

A: It provides clarity that income from selling pre-packaged software to customers in the USA would likely be treated as business income rather than royalty, potentially resulting in more favorable tax treatment under the DTAA.

5. Q: Can the tax authorities appeal this decision further?

A: While the judgment doesn't mention it explicitly, the tax authorities could potentially appeal to the Supreme Court if they believe there's a substantial question of law involved.

CM No. 23807/2016 (Exemption) in ITA 365/2016

1. Exemption allowed subject to all just exemptions.

ITA 363/2016 and ITA 365/2016

2. The challenge in these appeals by the Revenue is to the common order dated 23rd October 2015 passed by the Income Tax Appellate Tribunal („ITAT‟) in ITA Nos. 6273/Del/2012 and 690/Del/2014 for the Assessment Years („AYs‟) 2009-10 and 2010-11.

3. The main question urged by the Revenue for consideration before the Court is whether the consideration received by the Respondent Assessee on sale of pre-packaged software was „royalty or „fee for technical services‟ and was, therefore, not taxable as business income?

4. It is not in dispute that Article 12 (3) of the Double Taxation Avoidance Agreement („DTAA‟) between India and the United States of America (USA) is relevant for deciding the above issue. In the synopsis forming part of the memoranda of appeals, it is mentioned that the above question also forms the subject matter of the ITA No. 477 of 2014. That ITA pertained to AY 2008-09. The said ITA No. 477 of 2014 was dismissed by this Court by an order dated 1st September 2014 which reads as under:

“The issue raised in the present appeal is whether the consideration received on sale of pre-packaged software is „royalty‟ or „fee for technical services‟ and thus was not taxable as business income?

In the present case, Double Taxation Avoidance Agreement between India and the United States of America is applicable and to construe „royalty‟ conditions stipulated in the DTAA have to be satisfied. The question raised, it is accepted, is covered by the decision of this Court in ITA No. 1034 of 2009, DIT v. Infrasoft Limited decided on 22nd November 2013.

In view of the aforesaid decision, the present appeal is dismissed. We note that the Revenue has not disputed that the issue is covered by the aforesaid decision, but has stated that an appeal has been filed before the Supreme Court.”

5. The short question considered by the Court in Director of Income Tax v. Infrasoft Limited (2014) 220 Taxman 273 (Del) was whether the term „royalty‟ covered by Article 12 (3) of the DTAA would apply in the context of sale of pre-packaged copyrighted software. The Court also examined the effect of the subsequent amendment to Section 9(1)(vi) (of Income Tax Act, 1961) ('Act'). The Court came to the following conclusions in paras 87 to 90 of the said order which read as under:

“87. In order to qualify as royalty payment, it is necessary to establish that there is transfer of all or any rights (including the granting of any licence) in respect of copyright of a literary, artistic or scientific work. In order to treat the consideration paid by the Licensee as royalty, it is to be established that the licensee, by making such payment, obtains all or any of the copyright rights of such literary work. Distinction has to be made between the acquisition of a "copyright right" and a "copyrighted article". Copyright is distinct from the material object, copyrighted. Copyright is an intangible incorporeal right in the nature of a privilege, quite independent of any material substance, such as a manuscript. Just because one has the copyrighted article, it does not follow that one has also the copyright in it. It does not amount to transfer of all or any right including licence in respect of copyright. Copyright or even right to use copyright is distinguishable from sale consideration paid for "copyrighted" article. This sale consideration is for purchase of goods and is not royalty.

88. The license granted by the Assessee is limited to those necessary to enable the licensee to operate the program. The rights transferred are specific o the nature of computer programs. Copying the program onto the computer's hard drive or random access memory or making an archival copy is an essential step in utilizing the program. Therefore, rights in relation to these acts of copying, where they do no more than enable the effective operation of the program by the user, should be disregarded in analyzing the character of the transaction for tax purposes. Payments in these types of transactions would be dealt with as business income in accordance with Article 7.

89. There is a clear distinction between royalty paid on transfer of copyright rights and consideration for transfer of copyrighted articles. Right to use a copyrighted article or product with the owner retaining his copyright, is not the same thing as transferring or assigning rights in relation to the copyright. The enjoyment of some or all the rights which the copyright owner has, is necessary to invoke the royalty definition. Viewed from this angle, a non-exclusive and non-transferable licence enabling the use of a copyrighted product cannot be construed as an authority to enjoy any or all of the enumerated rights ingrained in Article 12 of DTAA. Where the purpose of the licence or the transaction is only to restrict use of the copyrighted product for internal business purpose, it would not be legally correct to state that the copyright itself or right to use copyright has been transferred to any extent. The parting of intellectual property rights inherent in and attached to the software product in favour of the licensee/customer is what is contemplated by the Treaty. Merely authorizing or enabling a customer to have the benefit of data or instructions contained therein without any further right to deal with them independently does not, amount to transfer of rights in relation to copyright or conferment of the right of using the copyright. The transfer of rights in or over copyright or the conferment of the right of use of copyright implies that the transferee/licensee should acquire rights either in entirety or partially co-extensive with the owner/ transferor who divests himself of the rights he possesses pro tanto.

90. The license granted to the licensee permitting him to download the computer programme and storing it in the computer for his own use is only incidental to the facility extended to the licensee to make use of the copyrighted product for his internal business purpose. The said process is necessary to make the programme functional and to have access to it and is qualitatively different from the right contemplated by the said paragraph because it is only integral to the use of copyrighted product. Apart from such incidental facility, the licensee has no right to deal with the product just as the owner would be in a position to do.”

6. This Court then concluded in para 94 that “the right to use a copyright in a programme is totally different from the right to use a programme embedded in a cassette or a CD which may be a software and the payment made for the same cannot be said to be received as consideration for the use of or right to use of any copyright to bring it within the definition of royalty as given in the DTAA. What the licensee has acquired is only a copy of the copyright article whereas the copyright remains with the owner and the Licensees have acquired a computer programme for being used in their business and no right is granted to them to utilize the copyright of a computer programme and thus the payment for the same is not in the nature of royalty.”

7. Thereafter in para 95 the Court concluded as under:

“95. We have not examined the effect of the subsequent amendment to Section 9(1)(vi) (of Income Tax Act, 1961) and also whether the amount received for use of software would be royalty in terms thereof for the reason that the Assessee is covered by the DTAA, the provisions of which are more beneficial.”

8. It is sought to be urged by Mr. Rahul Chaudhary, learned Senior standing counsel for the Revenue, that although the Court in Director of Income Tax v. Infrasoft Limited (supra) took note of the subsequent amendment to Section 9(1)(vi) (of Income Tax Act, 1961) as regards the term „royalty‟, it actually did not discuss the effect of the said amendment.

9. Section 90(3) (of Income Tax Act, 1961) makes it clear in the context of an agreement ('treaty') for avoidance of double taxation, that it is only when the provisions of the Act are more beneficial to the Assessee the Act will prevail over the treaty. Conversely, where the provision of the treaty is more beneficial to the Assessee, the treaty would prevail over the Act. This legal position has been reiterated in Director of Income Tax v. Infrasoft Limited (supra) which was followed in dismissing the Revenue's appeal in the Assessee‟s own case for AY 2008-09 i.e. ITA No. 477 of 2014.

10. The Court is not persuaded to re-examine the above issue which stands answered against the Revenue by the aforementioned order.

11. No substantial question of law arises. The appeals are dismissed with no orders as to costs.

S. MURALIDHAR, J

NAJMI WAZIRI, J

JULY 11, 2016

×