Tribunal Overturns AO's MAT Calculation, Upholds Assessee's Audited Accounts

Full News

Tribunal Overturns AO's MAT Calculation, Upholds Assessee's Audited Accounts

Tribunal Overturns AO's MAT Calculation, Upholds Assessee's Audited Accounts

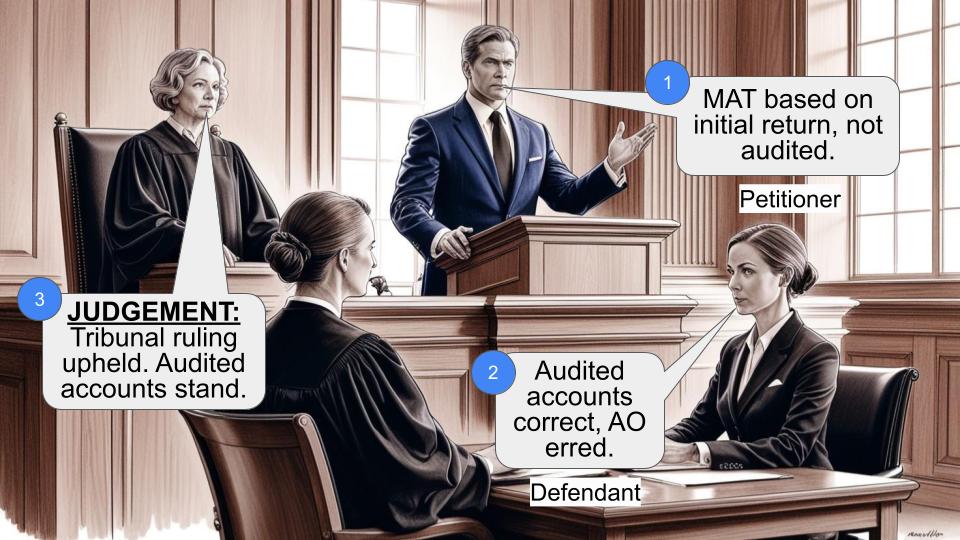

This case involves a dispute between the Commissioner of Income Tax (CIT) and Jajodia Engineering (P) Ltd. (the assessee) regarding the calculation of Minimum Alternate Tax (MAT) under Section 115JB (of Income Tax Act, 1961). The Income Tax Appellate Tribunal ruled in favor of the assessee, overturning the Assessing Officer's (AO) computation of book profit and tax liability.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs Jajodia Engineering (P) Ltd. (High Court of Gauhati)

ITA No. 7/2012

Date: 18th March 2016

Key Takeaways:

1. The AO has limited power to examine and adjust audited accounts for MAT calculation.

2. Audited accounts prepared in accordance with the Companies Act should be accepted for MAT purposes.

3. The AO cannot go behind the net profit shown in the profit and loss account except as provided in the explanation to Section 115JB (of Income Tax Act, 1961).

4. Corrected returns, even if filed late, should be considered for assessment if they align with audited accounts.

Issue:

Can the Assessing Officer recalculate book profit under Section 115JB (of Income Tax Act, 1961) by disregarding the assessee's audited accounts and using figures from an initially filed electronic return?

Facts:

- For the assessment year 2006-2007, Jajodia Engineering (P) Ltd. electronically filed a return showing NIL income.

- The electronic return showed a total income of Rs. 24,15,43,513 and a net profit of Rs. 7,95,62,134.

- The audited profit and loss account, however, disclosed a net loss of Rs. 4,08,72,066.

- The assessee explained the discrepancy as an inadvertent error in electronic filing and submitted a corrected return.

- The AO disregarded the corrected return as it was filed beyond the time limit and assessed MAT based on the initial electronic return figures.

Arguments:

Assessee:

- The AO should not tinker with audited accounts prepared in accordance with the Companies Act.

- The corrected return should be considered for assessment.

Revenue:

- The AO's computation was based on the material furnished by the assessee.

- It's not a case of tinkering with audited accounts but using the figures provided by the assessee in the initial return.

Key Legal Precedents:

1. Apollo Tyres Ltd. vs. Commissioner of Income Tax [2002] 255 ITR 273 (SC): The AO has limited power to examine whether books of accounts are certified as per the Companies Act and can only make increases and reductions as provided in the explanation to Section 115JB (of Income Tax Act, 1961).

2. Malayala Manorama Co. Ltd. vs. Commissioner of Income Tax [2008] 300 ITR 251 (SC): Emphasized the assessee's obligation to prepare profit and loss accounts as per Parts II and III of Schedule VI of the Companies Act, 1956.

3. Amines and Plasticizers Ltd. vs. Deputy Commissioner of Income Tax [2008] 296 ITR 727 (Gau): Followed the Apollo Tyres Ltd. ratio, stating that the AO cannot scrutinize profit and loss accounts certified by statutory auditors.

Judgement:

The Tribunal ruled in favor of the assessee, concluding that:

- The AO's computation was of his own making and not based on the audited accounts.

- The assessee cannot be held liable for tax on income that was returned but adjusted against brought forward losses.

- The AO should have considered the corrected return aligned with the audited profit and loss account for MAT calculation under Section 115JB (of Income Tax Act, 1961).

The High Court dismissed the revenue's appeal, affirming the Tribunal's order.

FAQs:

1. Q: Why was the initial electronic return disregarded?

A: The initial electronic return contained an inadvertent error, and a corrected return was filed to align with the audited accounts.

2. Q: Can the AO recalculate book profit by ignoring audited accounts?

A: No, the AO has limited power to examine and adjust audited accounts prepared in accordance with the Companies Act for MAT calculation.

3. Q: What should the AO do if there's a discrepancy between the filed return and audited accounts?

A: The AO should consider the corrected return that aligns with the audited accounts, even if filed late.

4. Q: What is the significance of this judgment for other taxpayers?

A: It reinforces the importance of audited accounts in MAT calculations and limits the AO's power to recalculate book profits arbitrarily.

5. Q: Does this mean the AO can never question the audited accounts?

A: The AO can still make adjustments as provided in the explanation to Section 115JB (of Income Tax Act, 1961), but cannot go behind the net profit shown in the audited accounts beyond this scope.

Heard Mr. S. Sarma, the learned standing counsel for the Income Tax Department. Also heard Mr. R. Goenka, the learned counsel appearing for the respondent (asse ssee).

2. This is an Appeal filed under Section 260-A (of Income Tax Act, 1961), 1961 (hereinafter referred to as the I.T. Act ) whereby the Commissioner of Income Tax in short the CIT, challenges the order dated 9.2.2012 (Annexure-C) of the Inc ome Tax Appellate Tribunal, Guwahati Bench in the I.T.A. No. 79/Gau/2010. By the impugned order, the Appellate Tribunal allowed the application filed by the res pondent, hereinafter referred to as the Assessee , and set aside the computation of the Assessing Officer (AO), taxing the book profit, in accordance with Section 115JB (of Income Tax Act, 1961).

3. For the assessment year 2006-2007 the assessee had electronically filed their return of income on 30.11.2006 showing NIL income. The case was processed under Section 143(1) (of Income Tax Act, 1961) and selected for scrutiny. Notice was issued to the assessee who filed copy of their audited balance sheet and other documents. As per the return filed electronically, the assessee who were in furniture business had shown total income at Rs.24,15,43,513/- (sale of furniture at Rs.65,02,788/- + other miscellaneous income at Rs.23,50,40,725/-) and calculated net profit at Rs.7,95,62,134/-. However as per the audited profit and loss account submitted, the assessee disclosed a net loss of Rs.4,08,72,066/-. Thus they were asked to explain the variation in the return submitted electronically and the audited accounts.

4. The assessee explained that since this was the first year in which return of income was filed electronically, the person who was entrusted with the work had inadvertently punched the figure of miscellaneous income at Rs.23,50,40,725/- (instead of Rs.11,46,06,525/-) and hence the assessee had later filed a corre cted copy of return. But the AO did not consider this corrected return as the sa me was filed beyond time and on that basis, proceeded to make the assessment of the Minimum Alternate Tax, in short MAT under Section 115JB (of Income Tax Act, 1961).

5. As the assessee had shown net profit at Rs.7,95,62,134/- and in the audi ted profit and loss account, a net loss of Rs.4,08,72,066/- was reflected, the MAT liability under Section 115JB (of Income Tax Act, 1961) was assessed at Rs.86,78,955/-, by the AO on 30.12.2008 (Annexure-A).

6. The aggrieved assessee then approached the CIT (Appeals) to challenge the determination of book profit under Section 115JB (of Income Tax Act, 1961) by contending that the AO was not justified in calculating the book profit by ignoring the net loss reflected in the audited profit and loss account prepared in accordance with the Part-II of Schedule VI of the Companies Act, 1956. However the Appellate Authority considered that the figure of net profit was taken into consideration from the return filed by the assessee themselves. It was further held that the AO had not tampered with the figures for calculating the book profit. Thus it was declared that the AO committed no error in rejecting the revised return of income because it was filed after expiry of the statutory time limit and accordingly the assessment for payment of MAT under Section 115JB (of Income Tax Act, 1961), was upheld through the order dated 9.2.2010 (Annexure-B), by the CIT (Appeals).

7. Aggrieved by the decision of the CIT(Appeals), the assessee approached t he Income Tax Appellate Tribunal, Guwahati Bench, where they contended that the departmental authorities are not entitled to tinker with audited accounts submitted by the assessee which is prepared in accordance with the Schedule-VI of the Companies Act, 1956. On the other hand, the departmental representative contended that the computation of MAT by the AO was upon due consideration of all materi al particulars furnished by the assessee and it is not a case of tinkering with the audited accounts, submitted by the assessee.

8. The Income Tax Appellate Tribunal considered the jurisdictional power of the AO in computing the MAT under Section 115JB (of Income Tax Act, 1961) and noted that the accounts furnished by the assessee are audited and certified, in accordance with Part-II & III of Schedule VI of the Companies Act, 1956. Hence it was opined that the figures of the said return should be accepted and there should be no tinkering with the duly audited accounts, for computation of tax under Section 115JB (of Income Tax Act, 1961). On the basis of such conclusion, the assessment of MAT by taking into account the book profit under Section 115JB (of Income Tax Act, 1961) by the AO was held to be unjustified and hence the assessment to tax was quashed.

9. We have heard the submission made by the respective counsel for the appe llant and the respondent.

10. Special provision for payment of tax is made by Section 115JB (of Income Tax Act, 1961) and in such cases where the tax liability of a company is less than 7.5% (10% for the assessment year 2007-2008) of the book profit, such book profit shall be deemed to be the total income of the assessee and tax became payable on such income. The total amount of income is to be computed under the I.T. Act on the basis of return furnished by the assessee and necessary determination is required to be made by following the procedure under Section 143 (of Income Tax Act, 1961) as found in National Thermal Power Co. Ltd. vs. Commissioner of Income Tax, reported in (1998) 229 ITR 383 (SC) where the Apex Court opined that: The purpose of the assessment proceedings before the taxing authorities is to assess correctly the tax liability of an assessee in accordance with law .

11. The assessee has the obligation to prepare his profit and loss account in conformity with Part-II & III of Schedule VI of the Companies Act, 1956 and if the audited accounts satisfy the requirement of Part-II & III of Schedule VI of the Companies Act, 1956, the Income Tax Officer has no jurisdiction to re-determine the book profit under Section 115J (of Income Tax Act, 1961), by substituting the figures incorporated in the audited return filed by the assessee.

12. Section 115JB (of Income Tax Act, 1961) was introduced in the I.T. Act with a deeming provision which makes a company liable to pay tax on its book profit as reflected in their own audited accounts and the authenticity of the accounts which are prepared in the manner provided by the Companies Act are to be accepted by the AO. When the a ccounts produced by an assessee are found to be maintained in accordance with the requirements of the Companies Act , it is not open to the AO to embark upon a fresh inquiry in regard to the entries made in the books of accounts of the company. In other words, computing the income under Section 115J (of Income Tax Act, 1961), the AO has limited power of examining whether the books of accounts are certified by the authorities, as having been properly maintained in accordance with the requirement of the Companies Act. When such books of accounts are produced, the AO has limited power of making appropriate correction in accordance with the explanation to Section 115JB (of Income Tax Act, 1961). To put it differently the AO does not have the jurisdiction to go behind the net profit reflected in the profit and loss account except to the limited extent permitted by the explanation to Section 115J (of Income Tax Act, 1961).

13. In the Apollo Tyres Ltd. vs. Commissioner of Income Tax reported in (200 2) 255 ITR 273 (SC), the Apex Court opined that &..while so looking into the accounts of the company, an AO under the IT Act has to accept the authenticity of the accounts with reference to the provisions of the Companies Act which obligates the Company to maintain its account in a manner provided by the Companies Act and the same to be scrutinized and cert ified by statutory auditors and will have to be approved by the company in its general meeting and thereafter to be filed before the Registrar of Companies who has a statutory obligation also to examine and satisfy that the accounts of company are maintained in accordance with the requirements of the Companies Act. In spite of all these procedures contemplated under the provisions of the Companies Act, we find it difficult to accept the argument of the Revenue that it is still open to the AO to re-scrutinise this account and satisfy himself that these ac counts have been maintained in accordance with the provisions of Companies Act.

In our opinion, reliance placed by the Revenue on sub-s. (IA) of s.115J of the IT Act in support of the above contention is misplaced. Sub-s. (IA) of s.115J does not empower the AO to embark upon a fresh inquiry in regard to the entries made in the books of account of the Company & Therefore, we are of the opinion, the AO while computing the income under s.115J has only the power of examining whether the books of account are certified by the authorities under the Companies Act as having been properly maintained in accordance with the Companies Act. The AO thereafter has the limited power of making increases and reductions as provided for in the Explanation to the said section. To put it differently, the AO does not have the jurisdiction to go behind the net profit shown in the P&L a/c except to the extent provided in the Explanation to s.115J.

14. On the same line, the Supreme Court in Malayala Manorama Co. Ltd. vs. Co mmissioner of Income Tax, reported in (2008) 300 ITR 251 (SC) laid down as under:-

It was further submitted that under s.115J the assessee has the obligation to prepare his P&L a/c as per Parts-II and III of Sch.VI to the 1956 Act. No dispute has been raised at any stage of the proceedings by the Revenue that the P&L a/c of the assessee is not in compliance with the provisions of the 1956 Act, particularly Sch.VI, Parts II and III. In Sch. VI, there is no reference to ss. 205 and 350 or Sch.XIV to the 1956 Act.

15. Following the ratio enunciated by the Supreme Court in the above case, o ur High Court in Amines and Plasticizers Ltd. vs. Deputy Commissioner of Income Tax, reported in (2008) 296 ITR 727 (Gau) held as follows:

The decision in Apollo Tyres Ltd. (supra) on the other hand shows that the AO cannot scrutinize the P&L a/cs of the assessee company certified by the statutory auditors. The question raised and answered in that case in our considered view is of no held in the given context of the case at hand. The directors have formed an opinion as to what is reasonably necessary for meeting the known liability against debts due. The P&L a/cs have been prepared as per relevant provision of the Companies Act, 1956 and the same is not in dispute. Regular accounting proce dures have been followed. The directors’ opinion shows that as against doubtful debts of Rs.51,79,064 and doubtful advance of Rs.2,40,132, as sum of Rs.11,52,221 has been provided for during the assessment year, as considered adequate by the management in view of the continued efforts for recovery. Therefore, the claim of the assessee could not be rejected simply on the ground that the doubtful de bts have not been written-off as actual bad debt .

16. In the present case, at no stage of the proceedings, the departmental au thorities have concluded that the profit and loss account furnished by the assessee is not in compliance with the provisions of Part-II & III of Schedule VI of the Companies Act, 1956. Therefore having regard to the ratio in Apollo Tyres Ltd. (supra) the AO couldn’t have gone behind the figures in the profit and loss account, certified by the statutory auditors of the assessee.

17. When the profit and loss account for the relevant years were prepared in accordance with the provisions of Part-II & III of Schedule VI of the Companies Act, 1956, the reference to any other figure than what is reflected in the audited profit and loss account, for determination of the book profit under Section 115JB (of Income Tax Act, 1961) by the AO would not be justified. But we find here that the AO had failed to take into account the corrected return although it was obliged to consider the said return for the purpose of assessment. Instead the authority tinkered with the final accounts prepared in accordance with the requirement of Schedule-VI of the Companies Act without determining that such profit and loss accounts are not in accordance with the requirement of the Companies Act. When the assessee has prepared their profit and loss account in consonance with the schedule of the Companies Act, the departmental authorities have no right to tinker with them, unless it is established that the final accounts are not prepared in accordance with Part-II of the Schedule-VI of the Companies Act.

18. But in the instant case, there was no determination of the AO that the final accounts of the assessee were not prepared in accordance with the Schedule-VI of the Companies Act. Hence the determination of liability for payment of MAT under Section 115JB (of Income Tax Act, 1961), by ignoring the profit and loss account was not through due process. When the corrected return in consonance with the audited profit and loss account was submitted, those figures should have been the basis for determination of MAT under Section 115JB (of Income Tax Act, 1961).

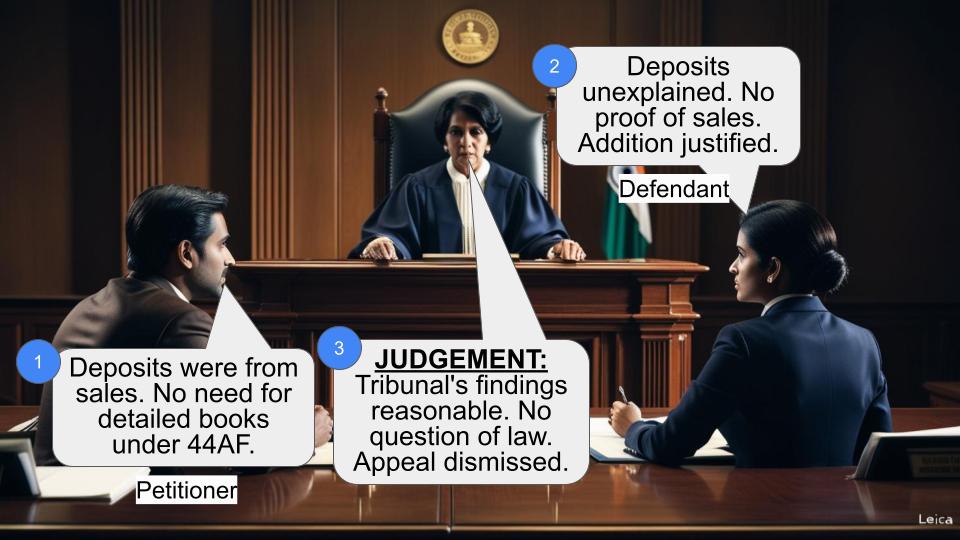

19. In the proceeding under consideration, the Appellate Tribunal concluded that the end result as computed by the AO was of his own making and the assessee could not be held liable to tax for non-disclosure of the income which the assessee had returned but adjusted against brought forward losses. We find such observation of the Tribunal with regard to the procedure adopted by the AO, is consistent with the ratio of Apollo Tyres Ltd. (supra); Malayala Manorama Co. Ltd. vs. Commissioner of Income Tax, reported in (2008) 300 ITR 251 and also this Court’s decision in Amines and Plasticizers Ltd. vs. Deputy Commissioner of Income Tax reported in (2008) 296 ITR 727 (Gau). Therefore we declare that no substantial question of law in this case is required to be decided as the issue is authoritatively decided by judicial pronouncements. Consequently this appeal by the rev enue is found devoid of merit and the same is dismissed by affirming the impugned order of the Income Tax Appellate Tribunal.

×

Similar Ripples

Questions

Tribunal Overturns AO's MAT Calculation, Upholds Assessee's Audited Accounts

Write your CommentSimilar Posts

Generic

- Reportdata/2991.pdf