Tribunal's Power to Enhance Assessment Curtailed: Supreme Court Upholds Taxpaye…

Full News

Tribunal's Power to Enhance Assessment Curtailed: Supreme Court Upholds Taxpayer's Benefit

Tribunal's Power to Enhance Assessment Curtailed: Supreme Court Upholds Taxpayer's Benefit

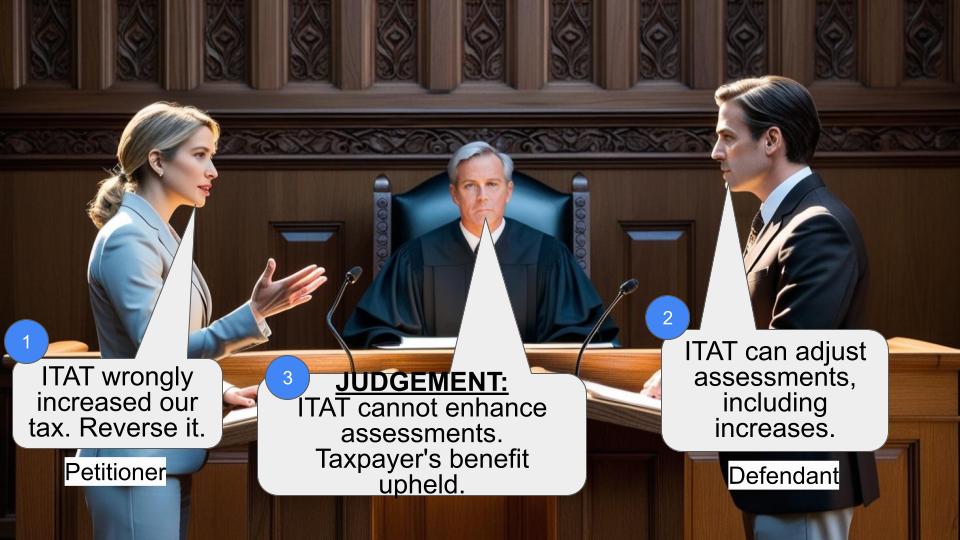

This case involves an appeal by Fidelity Shares and Security Ltd. against a judgment of the Income Tax Appellate Tribunal (ITAT) in Ahmedabad. The Supreme Court ruled that the ITAT doesn't have the power to enhance assessments or take away benefits granted to taxpayers by the Assessing Officer. This decision upholds the principle that tribunals can't increase tax liabilities beyond what the original assessment determined.

Get the full picture - access the original judgement of the court order here

Case Name:

Fidelity Shares and Security Ltd. vs Deputy Commissioner of Income Tax (High Court of Gujarat)

Tax Appeal No. 187 of 2001

Date: 13th June 2016

Key Takeaways:

1. The Income Tax Appellate Tribunal (ITAT) cannot enhance assessments or remove benefits given by the Assessing Officer.

2. This ruling reinforces the limits of the ITAT's powers in tax appeals.

3. The decision protects taxpayers from unexpected increases in tax liability during the appeal process.

Issue:

Does the Income Tax Appellate Tribunal have the power to enhance an assessment or take away benefits granted to an assessee by the Assessing Officer?

Facts:

- The case relates to the Assessment Year 1989-90.

- The ITAT Ahmedabad Bench "B" had allowed the Department's appeal, effectively increasing the assessee's tax liability.

- The High Court initially framed five questions of law, but the appellant only pursued the fifth question regarding the Tribunal's power to enhance the assessment.

Arguments:

The appellant argued that the ITAT had no power to enhance the assessment or take away benefits granted by the Assessing Officer. They relied on a Supreme Court precedent to support this claim.

The respondent (Income Tax Department) contended that the Tribunal has the power to enhance or reduce benefits given by the Assessing Officer.

Key Legal Precedents:

1. Mcorp Global (P) Ltd. v. Commissioner of Income-tax, Ghaziabad [2009] 178 taxman 347 (SC)

2. Hukumchand Mills Ltd. v. CIT (1967) 63 ITR 232

These cases established that under Section 254(1) (of Income Tax Act, 1961) (equivalent to Section 33(4) (of Income Tax Act, 1961), 1922), the Tribunal is not authorized to take back benefits granted to the assessee by the Assessing Officer.

Judgement:

The Supreme Court ruled in favor of the appellant (Fidelity Shares and Security Ltd.). The Court held that the ITAT has no power under the Income Tax Act to enhance the assessment in an appeal. This decision was based on the precedent set in the Mcorp Global case, which itself relied on the Hukumchand Mills case.

FAQs:

1. Q: What was the main issue in this case?

A: The main issue was whether the Income Tax Appellate Tribunal has the power to enhance an assessment or remove benefits granted by the Assessing Officer.

2. Q: What did the Supreme Court decide?

A: The Supreme Court ruled that the ITAT does not have the power to enhance assessments or take away benefits granted by the Assessing Officer.

3. Q: What legal precedent did the Court rely on?

A: The Court primarily relied on the Mcorp Global (P) Ltd. v. Commissioner of Income-tax, Ghaziabad case, which in turn was based on the Hukumchand Mills Ltd. v. CIT case.

4. Q: How does this decision affect taxpayers?

A: This decision protects taxpayers from having their tax liabilities unexpectedly increased during the appeal process at the ITAT level.

5. Q: Does this mean the ITAT can never change an assessment?

A: The ITAT can still reduce assessments or confirm them, but it cannot enhance them beyond what the Assessing Officer originally determined.

1. By way of this Appeal, the Appellant– has challenged the judgment and order dated 12.03.1999 of the Income Tax Appellate Tribunal, Ahmedabad Bench “B”, Ahmedabad in ITA No.1889/Ahd/1993 for the Assessment Year : 1989-90 whereby the Appeal of the Department was allowed.

2. While admitting the matter on 16.07.2001, the following substantial questions of law were framed by the Court for consideration :-

“1. Whether, on the facts and in the circumstances of the case, the Tribunal was right in law in adjudicating a ground of appeal not taken by the Department viz. whether the surplus of service charges i.e. total service charges less expenses connected therewith is to be excluded from the total profit of the business?

2. Whether, on the facts and in the circumstances of the case, the Tribunal was right in holding that such surplus is to be excluded from the profits of business for arriving at export profit under sec. 80HHC (of Income Tax Act, 1961)? 3. Whether, on the facts and in the circumstances of the case, the Tribunal was right in law in adjudicating a ground of appeal not taken by the revenue viz. whether Rs.16,39,443/- being sale of REP licence will form part of total turnover?

4. Whether, on the facts and in the circumstances of the case, the Tribunal was right in law in holding that Rs.16,39,443/- being sales of REP licence it is to be included in total turnover for the purpose of deduction u/s. 80HHC (of Income Tax Act, 1961)?

5. Whether the Tribunal had the power to pass such an order whereby the total income of the assessee was far much more than the total income assessed by the Assessing Officer and that too, in absence of any grounds of appeal taken by the revenue praying for such decision and without hearing the assessee on such proposed result?”

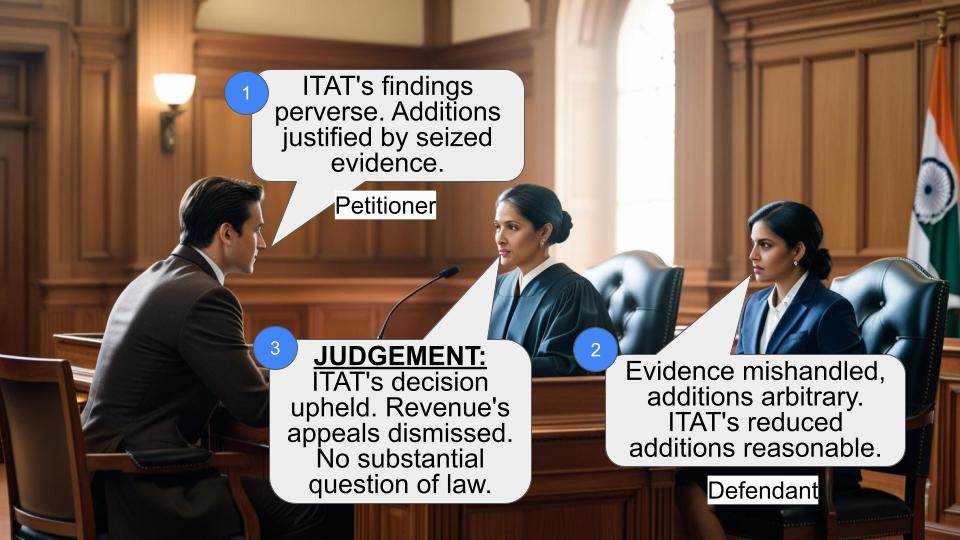

3. At the outset, learned Counsel for the appellant has stated that he does not press into service the issues 1, 2, 3 and 4. Qua issue No.5, it is submitted that the said issue is covered by the decision of this Court in the case of Mcorp Global (P) Ltd. v. Commissioner of Income-tax, Ghaziabad reported in [2009] 178 taxman 347 (SC) and Paragraph 6 of the said judgment reads as under :-

“6. In the case of Hukumchand Mills Ltd. v. CIT reported in (1967) 63 ITR 232 this Court has held that under Section 33(4) of the Income- tax Act, 1922 (equivalent to Section 254(1) of the 1961 Act), the Tribunal was not authorized to take back the benefit granted to the assessee by the AO. The Tribunal has no power to enhance the assessment. Applying the ratio of the said judgment to the present case, we are of the view that, in this case, the AO had granted depreciation in respect of 42,000 bottles out of the total number of bottles (5,46,000), by reason of the impugned judgment. That benefit is sought to be taken away by the Department, which is not permissible in law. This is the infirmity in the impugned judgment of the High Court and the Tribunal.”

Learned Counsel for the appellant has taken this Court to the relevant issues raised in this Appeal which are detailed hereunder :-

As per U/s. Profit of Business x Export Turnover

Total Turnover

80HHC Relief

Assessee 2,08,55,959 x 3,02,19,746 3,20,09,756

=19689678

Assessing Officer

143(3) order

2,11,92,759 x 3,02,19,746 4,79,42,313

=13351438 (32009756 +17507000 - 1639443)

Assessing Officer 154 order

2,11,92,759 x 3,02,19,746 4,95,81,756 with 16,39,443

=12927582

CIT (Appeals)

2,11,92,759 x 3,02,19,746 3,20,09,756 + 17,50,700 3,37,60,456

=19582000

Order of Tribunal 54,36,459 x 3,02,19,746 3,37,69,456

=4892813

Learned Counsel for the appellant has also drawn our attention to Sections 251(1)(a) and 253 of the Income Tax Act as also to Section 24(5) of the Wealth Tax Act, which read as under :-

Section 251(1)(a) (of Income Tax Act, 1961) “Power of the Commissioner (Appeals) 251(1) In disposing of an appeal, the Commissioner (Appeals) shall have the following powers -

(a) in an appeal against an order of assessment, he may confirm, reduce, enhance or annul the assessment.”

Appeals to the appellate Tribunal “253. (1) Any assessee aggrieved by any of the following orders may appeal to the Appellate Tribunal against such order -

(a) an order passed by a [Deputy Commissioner (Appeals)] [before the 1st day of October, 1998] [or, as the case may be, a Commissioner (Appeals) under [***] [section 154 (of Income Tax Act, 1961)], [***] section 250 (of Income Tax Act, 1961), [section 271 (of Income Tax Act, 1961), section 271A (of Income Tax Act, 1961) or section 272A (of Income Tax Act, 1961)]; or

(b) an order passed by an Assessing Officer under clause (c) of section 158BC (of Income Tax Act, 1961), in respect of search initiated under section 132 (of Income Tax Act, 1961) or books of account, other document or any assets requisitioned under section 132A (of Income Tax Act, 1961), after the 30th day of June, 1995, but before the 1st day of January, 1997; or

(ba) an order passed by an Assessing Officer under sub-section (1) of section 115VZC (of Income Tax Act, 1961); or

(c) an order passed by a [Principal Commissioner or] Commissioner [under section 12AA (of Income Tax Act, 1961) [or under clause (vi) of sub-section (5) of section 80G (of Income Tax Act, 1961)] or] under section 263 (of Income Tax Act, 1961) [or under section 271 (of Income Tax Act, 1961)] [or under section 272A (of Income Tax Act, 1961)] [***] or an order passed by him under section 154 (of Income Tax Act, 1961) amending his order under section 263 (of Income Tax Act, 1961)] [or an order passed by [Principal Chief Commissioner or] Chief Commissioner or a [Principal Director General or] Director General or a [Principal Director or] Director under section 272A (of Income Tax Act, 1961); [or]]

(d) an order passed by an Assessing Officer under sub-section (3), of section 143 (of Income Tax Act, 1961) or section 147 (of Income Tax Act, 1961) [or section 153A (of Income Tax Act, 1961) or section 153C (of Income Tax Act, 1961)] in pursuance of the directions of the Dispute Resolution Panel or an order passed under section 154 (of Income Tax Act, 1961) in respect of such order;]

(e) an order passed by an Assessing Officer under sub-section (3) of section 143 (of Income Tax Act, 1961) or section 147 (of Income Tax Act, 1961) or section 153A (of Income Tax Act, 1961) or section 153C (of Income Tax Act, 1961) with the approval of the [Principal Commissioner or] Commissioner as referred to in sub-section (12) of section 144BA (of Income Tax Act, 1961) or an order passed under section 154 (of Income Tax Act, 1961) or section 155 (of Income Tax Act, 1961) in respect of such order;

(f) an order passed by the prescribed authority under sub- clause (vi) or sub-clause (via) of clause (23) of section 10 (of Income Tax Act, 1961).]”

Section 24(5) of the Wealth Tax Act,1957 “(5) The Appellate Tribunal may, after giving both parties to the appeal an opportunity of being heard, pass such orders thereon as it thinks fit, and any such orders may include an order enhancing the assessment or penalty: 446 [Provided that if the valuation of any asset is objected to, the Appellate Tribunal shall,

(a) in a case where such valuation has been made by a Valuation Officer under section 16A (of Income Tax Act, 1961), also give such Valuation Officer an opportunity of being heard;

(b) in any other case, on a request being made in this behalf by the 439 [Assessing Officer], give an opportunity of being heard also to any Valuation Officer nominated for the purpose by the Assessing Officer;

Provided further that no order enhancing an assessment or penalty shall be made unless the person affected thereby has been given a reasonable opportunity of showing cause against such enhancement.”

4. Learned Counsel for the respondent Mrs. Mauna M. Bhatt has supported the order of the Tribunal and contended that in view of the observations, the Tribunal has all the powers to enhance and/or deduct the benefits given by the Assessing Officer.

5. We have heard learned Advocates for the respective parties. In view of the above referred decision in the case of Mcorp Global (P) Ltd. (supra), we are of the view that the contention raised by learned Counsel for the appellant requires to be accepted as the Tribunal has no power under the Income Tax Act to enhance the assessment in Appeal in view of the statutory provisions. Hence, issues No.1 to 4 are not considered and the issue No.5 is answered in favour of the assessee and against the department.

Sd/-

(K.S. JHAVERI, J.)

Sd/-

(G.R. UDHWANI, J.)

×

Similar Ripples

Questions

Tribunal's Power to Enhance Assessment Curtailed: Supreme Court Upholds Taxpayer's Benefit

Write your CommentSimilar Posts

Generic

- Reportdata/2775.pdf