Trust Deed's Dissolution Clause Secures Tax Registration, Court Affirms

Full News

Trust Deed's Dissolution Clause Secures Tax Registration, Court Affirms

Trust Deed's Dissolution Clause Secures Tax Registration, Court Affirms

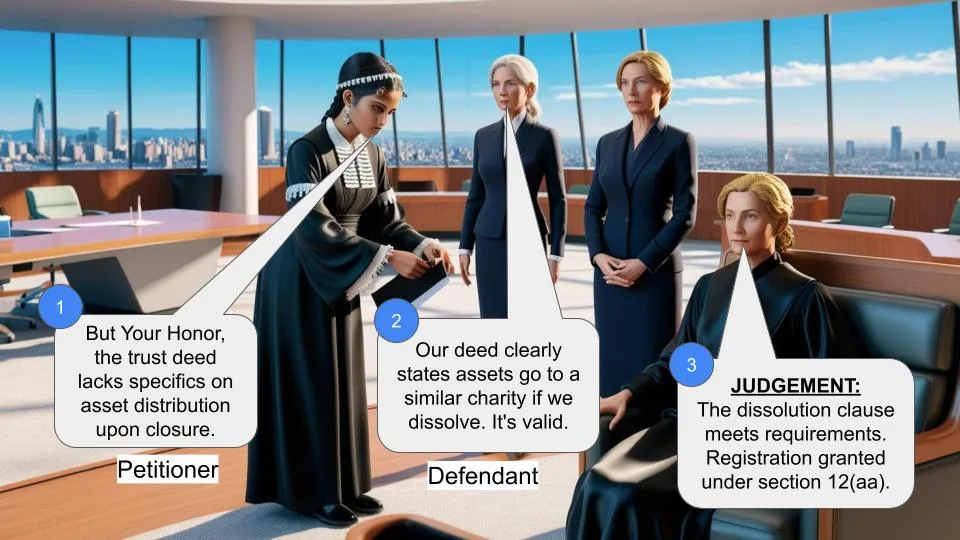

This case involves the Director of Income Tax (Exemptions) appealing against a decision by the Income Tax Appellate Tribunal (ITAT) that granted registration under section 12(aa) (of Income Tax Act, 1961) to a charitable trust. The High Court dismissed the appeal, affirming the ITAT's decision to grant registration based on the presence of a dissolution clause in the trust deed.

Get the full picture - access the original judgement of the court order here

Case Name:

Director of Income Tax (Exemption) Vs Vanchhara Tirthadhipati-Chintamani Paraswaprwabhu (High Court of Gujarat)

Tax Appeal No.548 of 2014

Key Takeaways:

1. A dissolution clause in a charitable trust deed is crucial for tax registration.

2. The court affirmed that the ITAT was correct in directing registration when such a clause exists.

3. The decision emphasizes the importance of proper provisions for trust closure in charitable trust deeds.

Issue

Was the Income Tax Appellate Tribunal correct in directing the Director of Income Tax (Exemptions) to grant registration under section 12(aa) (of Income Tax Act, 1961) to a charitable trust based on the presence of a dissolution clause in the trust deed?

Facts

1. The respondent is a charitable trust that applied for registration under section 12(aa) (of Income Tax Act, 1961).

2. The trust deed contained a clause regarding the closure of the trust.

3. The Income Tax Appellate Tribunal (ITAT) directed the Director of Income Tax (Exemptions) to grant registration to the trust.

4. The revenue department appealed this decision to the High Court.

Arguments

Revenue's Arguments:

1. The ITAT erred in setting aside the order of the Director of Income Tax (Exemptions).

2. A public charitable trust's deed should have a clause stating that upon dissolution, no asset will go to any trustee, donor, settler, etc.

Respondent's Arguments:

1. The trust deed contains a dissolution clause that meets the requirements for registration.

2. The ITAT's decision was based on a previous case (Shri Chargam Dasha Porwad Mahamandal) that was upheld by the High Court.

Key Legal Precedents

1. Shri Chargam Dasha Porwad Mahamandal, ITA Nos.337 and 338/Ahd/2013 - This case was relied upon by the ITAT in making its decision.

2. Tax Appeal No.1147 of 2013 with Tax Appeal No.1148 of 2013 - The High Court confirmed the ITAT's decision in the Shri Chargam Dasha Porwad Mahamandal case.

Judgement

1. The High Court dismissed the appeal, affirming the ITAT's decision.

2. The court found that the trust deed did provide a dissolution clause, which was sufficient for granting registration under section 12(aa) (of Income Tax Act, 1961).

3. The court noted that the dissolution clause in the trust deed specified that if the trust were to be closed, its property would be handed over to another institution with similar objects, subject to a 2/3 majority vote and unanimous decision of the working trustees.

4. The court emphasized that any decision to close the trust would require permission from the Charity Commissioner under the Bombay Public Trust Act.

FAQs

Q1: Why was the dissolution clause important in this case?

A1: The dissolution clause was crucial because it demonstrated that the trust had proper provisions for its closure, which is a requirement for registration under section 12(aa) (of Income Tax Act, 1961).

Q2: What happens to the trust's property if it's dissolved?

A2: According to the trust deed, the property would be handed over to another institution with similar objects, subject to a 2/3 majority vote and unanimous decision of the working trustees.

Q3: Does this decision mean that all charitable trusts must have a dissolution clause?

A3: While the court didn't explicitly state this, the decision emphasizes the importance of having a dissolution clause in charitable trust deeds for tax registration purposes.

Q4: Is the Charity Commissioner's permission required for closing a trust?

A4: Yes, the court noted that any decision to close the trust would require permission from the Charity Commissioner under the Bombay Public Trust Act.

Q5: What was the significance of the Shri Chargam Dasha Porwad Mahamandal case?

A5: This case set a precedent that the ITAT relied on in making its decision, and it was also upheld by the High Court in a separate appeal.

1. Feeling aggrieved by and dissatisfied with the impugned judgment and order passed by the learned Income Tax Appellate Tribunal, Ahmedabad (hereinafter referred to as “learned Tribunal”) dated 11.10.2013 passed in ITA No.610/ Ahd/2013, by which the learned Tribunal has allowed the said appeal preferred by the respondent herein and has directed the DIT (E) to grant the registration under section 12(aa) (of Income Tax Act, 1961) to the assessee, the revenue has preferred the present appeal raising the following substantial questions of law.

“A. Whether the appellate Tribunal has substantially erred in setting aside the order of DIT (E) holding that dissolution clause is not necessary in the deed of charitable trust?

B. Whether in view of the fact that the assessee is a public charitable trust, should the deed not have a clause that upon dissolution no asset will go to any trustee, donor settler etc.?”

2. We have heard Shri M.R. Bhatt, learned counsel appearing on behalf of the appellant and Shri Hemani, learned advocate appearing on behalf of the respondent – original appellant.

3. From the impugned judgment and order passed by the learned Tribunal, it appears that the learned Tribunal has allowed the appeal preferred by the respondent herein relying upon the decision of the Coordinate Bench in the case of Shri Chargam Dasha Porwad Mahamandal, ITA Nos.337 and 338/Ahd/2013 and considering the fact that in the case of the respondent trust, there is a dissolution clause and the provisions made in the trust deed itself, in the eventuality, the trust is closed.

4. It is required to be noted that as such, the decision of the learned Tribunal in the case of Shri Chargam Dasha Porwad Mahamandal in ITA Nos.337 and 338/Ahd/2013 has been confirmed by the Division Bench of this Court vide order dated 18.2.2014 passed in Tax Appeal No.1147 of 2013 with Tax Appeal No.1148 of 2013.

5. Considering the fact that in the case of the respondent trust, as such, the trust deed does provide the dissolution clause, as such, substantial questions of law raised in the present tax appeal would not survive. So, in the impugned judgment and order passed by the learned Tribunal, the learned Tribunal has not held that the dissolution clause is not necessary in the deed of charitable trust. Even otherwise, from the order passed by the DIT (E), it appears that in the trust deed of the respondent trust, there is a provision/clause with respect to closure of the trust, which reads as under:

“If necessary to close the trust then the property of trust be handover other institution trust having similar objects by passing resolution by minimum 2/3rd majority of members and unanimous decision of committee working trustees.”

6. Under the circumstances, when the trust deed specifically provides for a closure of the trust and it specifically provides that if necessary to close the trust, than the property of the trust be handed over to other institution – trust having similar objects by passing resolution by minimum 2/3rd majority of the trust and unanimous decision of the committee working trustees and considering the above, when the learned Tribunal has directed the DIT (E) to grant the registration under section 12(aa) (of Income Tax Act, 1961), it cannot be said that the learned Tribunal has committed any error, which calls for the interference of this Court. It goes without saying that any decision to close the trust even in the eventuality as per the aforesaid clause shall always be after obtaining appropriate permission from the Charity Commissioner under the Bombay Public Trust Act.

7. Under the circumstances, and in view of the above and for the reasons stated above, the substantial questions of law raised/framed are not required to be answered and are accordingly not answered.

8. With this, present tax appeal is dismissed. No costs.

(M.R.SHAH, J.)

(S.H.VORA, J.)

×

Questions

Trust Deed's Dissolution Clause Secures Tax Registration, Court Affirms

Write your CommentSimilar Posts

Generic

- Reportdata/4183.pdf