Trust’s Business Clause Doesn’t Bar Educational Exemption

Full News

Trust’s Business Clause Doesn’t Bar Educational Exemption

Trust’s Business Clause Doesn’t Bar Educational Exemption

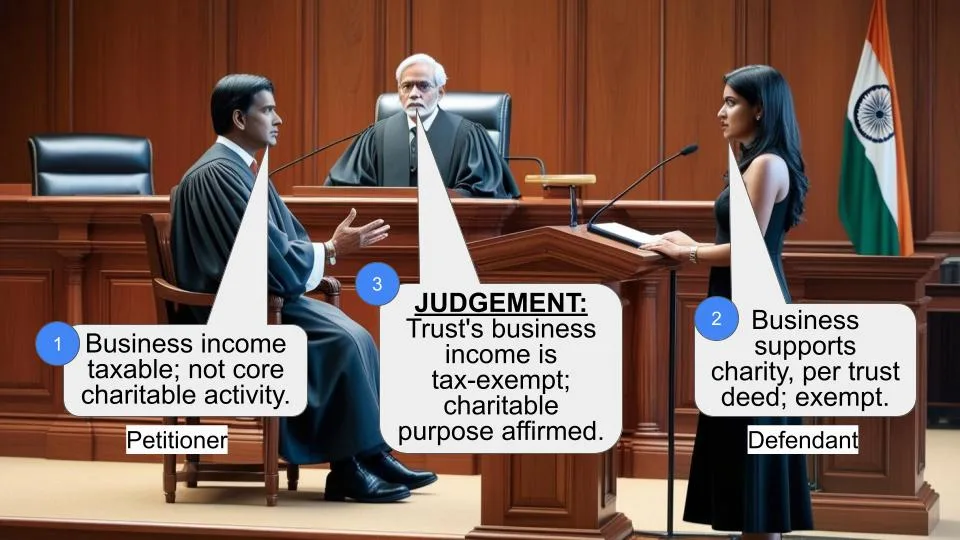

The case involves HARF Charitable Trust and the Chief Commissioner of Income Tax. The dispute centers on whether the Trust should be denied tax exemption under Section 10(23C)(vi) (of Income Tax Act, 1961) due to a clause in its deed allowing business activities. The court ruled in favor of the Trust, stating that the mere presence of a business clause does not disqualify it from being considered for educational purposes exemption.

Get the full picture - access the original judgement of the court order here

Case Name:

Harf Charitable Trust (Regd.) Vs Chief Commissioner of Income Tax & Another (High Court of Punjab & Haryana)

CWP No. 24895 of 2014

Date: 6th July 2015

Key Takeaways:

- The court emphasized the “predominant object test,” which assesses whether the main purpose of an institution is educational, not profit-making.

- A clause allowing business activities in a trust deed does not automatically disqualify a trust from tax exemption if the primary purpose is educational.

- The court quashed the rejection of the Trust’s application for exemption and ordered a fresh decision considering the predominant object of the Trust.

Issue

Does the presence of a business clause in a trust deed disqualify a trust from tax exemption under Section 10(23C)(vi) (of Income Tax Act, 1961) if its primary purpose is educational?

Facts

- HARF Charitable Trust operates a school and sought tax exemption under Section 10(23C)(vi) (of Income Tax Act, 1961).

- The Chief Commissioner of Income Tax rejected the application, citing a clause in the trust deed that allowed the Trust to engage in business activities.

- The Trust argued that its primary purpose was educational, and the business clause was not its main objective.

Arguments

- Trust’s Argument: The Trust maintained that its primary purpose was educational, and the business clause was not intended to override this. They also pointed out that the objectionable clause had been removed.

- Commissioner’s Argument: The Commissioner argued that the presence of a business clause indicated an intention to engage in profit-making activities, which disqualified the Trust from exemption.

Key Legal Precedents

- Pine Grove International Charitable Trust vs Union of India: This case was referenced to support the argument that a trust can still qualify for exemption if its predominant purpose is educational, even if it generates surplus income.

- Queen’s Educational Society vs CIT: The Supreme Court’s decision in this case was cited to emphasize that the predominant object test should be applied.

Judgement

The court ruled in favor of HARF Charitable Trust, stating that the mere presence of a business clause does not disqualify the Trust from exemption if its primary purpose is educational. The court quashed the rejection of the Trust’s application and ordered the competent authority to reconsider the application, focusing on the Trust’s predominant object.

FAQs

Q1: Does a trust lose its educational status if it makes a profit?

A1: No, as long as the predominant purpose is educational, making a profit does not change its status.

Q2: What is the predominant object test?

A2: It’s a legal test to determine if the main purpose of an institution is educational rather than profit-making.

Q3: Can a trust with a business clause still get tax exemption?

A3: Yes, if the primary purpose of the trust is educational, a business clause does not automatically disqualify it from exemption.

1. Challenge in the present writ petition is to the order dated 17.09.2012 (Annexure P-5) passed by the Chief Commissioner of Income Tax-respondent no. 1 wherein, the application of the petitioner for grant of approval for exemption under Section 10(23C)(vi) (of Income Tax Act, 1961), 1961 (in short 'the Act') has been rejected.

The predominant reason which weighed with respondent no. 1-

The Chief Commissioner of Income Tax, Ludhiana was that the petitioner-

Trust had an intention to carry out business activity which was not

permissible for charitable organizations. The trustees were in place for the

whole duration of their life and it gave the organization a look and character of a private body rather than a charitable organization and the objectives were not related to the promotion of education and the educational trust did not exist solely for educational purposes.

The petitioner's case is that the Trust is registered under the

Societies Registration Act, 1860 and is a public charitable trust and running a school in the name of Sohrab Public School, Nabha Raod, Malerkotla

solely for educational purposes and is being regularly assessed to income

tax. An application was submitted in Form 56D under Section 10(23C)(vi) (of Income Tax Act, 1961)

of the Act read with Rule 2CA (of Income Tax Rules, 1962) seeking exemption from payment of income

tax as per requirements and it also filed the audited balance sheets for the

last 3 years plus the trust deed. Certain information was asked for and a

detailed reply was filed clarifying each and every issue and an opportunity

of hearing was afforded by respondent no. 1, who rejected the claim on

untenable grounds.

In the written statement filed on behalf of the respondents, plea

taken was that the education institution is to exist “solely for educational

purposes” and if the institution existed for other purposes, the exemption

could not be granted and reliance was placed upon the provisions of Section

10(23C)(vi) of the Act and the observations made by the Division Bench of

this Court in Pine Grove International Charitable Trust vs. Union of India

and others, (2010) 327 ITR 73 (P & H). The said order was accordingly

justified that even if one of the objects enables the institute to undertake

commercial activities, entitlement for approval under the provisions of the

Act would not be there.

The petitioner-Trust also filed replication that a supplementary

trust deed had been executed and the objecting words “and any other

business as decided by the trustees” had been deleted. The said fact had

also been noticed in a subsequent assessment made on 21.12.2012

(Annexure P-9).

Counsel for the petitioner has thus submitted that merely

because there was a clause in the trust deed which provided that the Trust

could carry on other business would not mean that there was an absolute bar

for consideration of the benefit under Section 10(23C)(vi) (of Income Tax Act, 1961) once

the predominant purpose and objects of the trust were charitable in nature.

It is accordingly submitted that in view of the observations of the Division

Bench in Pine Grove's case (supra), which had been further upheld by the

Apex Court in Queen's Educational Society vs. CIT, (2015) 372 ITR 699,

the respondent no. 1 was not justified in rejecting the case.

Counsel for the Department, on the other hand, contended that

the order was justified and within the ambit of the provisions of the Act and once the Trust was having other objectives which were not related to the

charitable purposes, no fault could be found in the decision of respondent

no. 1. The objectionable clause which was part of the trust deed was clause

(i) which provided that one of the objects of the trust was “to carry on other business as decided by the trustees”. On the strength of the said clause, as noticed above, the impugned order has been passed against the petitioner-trust on the strength of the provisions that the trust did not exist solely for educational purposes.

To appreciate the controversy in question, it would be

necessary to examine the provisions of Section 10(23C)(vi) (of Income Tax Act, 1961)

which provides that in computing the total income of the previous year of

any person, income falling within any of the specified clauses is not to be

included which is received on behalf of any educational institution existing

solely for educational purposes and not for purposes of profit than those

mentioned in sub-clause (iiiab) or sub-clause (iiiad) of Section 10(23C) (of Income Tax Act, 1961) of

the Act. The relevant provisions read thus:-

“10. In computing the total income of a

previous year of any person, any income falling within

any of the following clauses shall not be included-

(23C) any income received by any person on behalf of-

(iiiab) any university or other educational

institution existing solely for educational purposes and

not for purposes of profit , which is wholly or

substantially financed by the Government; or

(iiiad) any university or other educational

institution existing solely for educational purposes and

not for purposes of profit if the aggregate annual

receipts of such university or educational institution do

not exceed the amount of annual receipts as may be

prescribed; or

(vi) any university or other educational

institution existing solely for educational purposes and

not for purposes of profit,other than those mentioned in

subclause(iiiab) of sub-clause(iiiad) and which may be

approved by the prescribed authority;”

The said provisions were discussed in a threadbare manner by

the Division Bench of this Court in Pine Grove's case (supra) wherein,

exemption granted had been withdrawn on the ground that the educational

institutions being run were for generating profits and did not exist solely for educational purpose. While issuing show cause notice, the authorities had placed reliance upon the judgment of the Uttrakhand High Court in CIT vs. Queen's Educational Society, (2009) 318 ITR 160. The Division Bench

framed the following substantial questions of law:-

“(A) Whether an educational institution would

cease to exist 'solely' for educational purposes and not

for purposes of profit merely because it has generated

surplus income over a period of 4/5 years after meeting

its expenditure?

(B) Whether the amount spent on

acquiring/constructing capital assets wholly and

exclusively becomes part of the total income or it

becomes entitled to exemption under Section 10(23C) (of Income Tax Act, 1961)

(vi)of the Act?

(C) Whether an institution registered as a

Society under the Societies Registration Act,1860,loses

its character as an educational institution, eligible to

apply for exemption under Section 10(23C)(vi) (of Income Tax Act, 1961)of the

Act?”

Question no. (A) as to whether the education institution cease

to exist solely for educational purposes was answered in favour of the

institutions by holding that the predominant object of the activity is to be

taken into consideration. Reliance was placed upon the judgments of the

Apex Court in Aditanar Educational Institution vs. Additional

Commissioner of Income Tax, 1997 (224) ITR 310; American Hotel and

Lodging Association Educational Institute v. CBDT, (2008) 301 ITR 86;

CIT (Addl.) vs. Surat Art Silk Cloth Manufacturers Association, 1980

(121) ITR 1 (SC) and the view in Queen's Educational Society's case

(supra) was specifically not accepted. It was held that where the

educational institutions which are registered, the society would retain their character as such and they would be eligible to apply for exemption. The relevant observations read thus:-

“(1) It is obligatory on the part of the Chief

Commissioner of Income Tax or the Director, which are

the prescribed authorities, to comply with proviso

thirteen (un-numbered). Accordingly, it has to be

ascertained whether the educational institution has

been applying its profit wholly and exclusively to the

object for which the institution is established. Merely

because an institution has earned profit would not be

deciding factor to conclude that the educational

institution exists for profit.

(2) The provisions of Section 10(23C)(vi) (of Income Tax Act, 1961) of the

Act are analogues to the erstwhile Section 10(22) (of Income Tax Act, 1961) of the

Act, as has been laid down by Hon’ble the Supreme

Court in the case of American Hotel and Lodging

Association (supra). To decide the entitlement of an

institution for exemption under Section 10(23C)(vi) (of Income Tax Act, 1961) of

the Act, the test of predominant object of the activity

has to be applied by posing the question whether it

exists solely for education and not to earn profit [See 5-

Judges Constitution Bench judgment in the case of

Surat Art Silk Cloth Manufacturers Association

(supra)]. It has to be borne in mind that merely because

profits have resulted from the activity of imparting

education would not result in change of character of

the institution that it exists solely for educational

purpose. A workable solution has been provided by

Hon’ble the Supreme Court in para 33 of its judgment

in American Hotel and Lodging Association’s case

(supra). Thus, on an application made by an institution,

the prescribed authority can grant approval subject to

such terms and conditions as it may deems fit provided

that they are not in conflict with the provisions of the

Act. The parameters of earning profit beyond 15% and

its investment wholly for educational purposes may be

expressly stipulated as per the statutory requirement.

Thereafter the Assessing Authority may ensure

compliance of those conditions. The cases where

exemption has been granted earlier and the

assessments are complete with the finding that there is

no contravention of the statutory provisions, need not

be reopened. However, after grant of approval if it

comes to the notice of the prescribed authority that the

conditions on which approval was given, have been

violated or the circumstances mentioned in 13th proviso

exists, then by following the procedure envisaged in 13th

proviso, the prescribed authority can withdraw the

approval.

(3) The capital expenditure wholly and

exclusively to the objects of education is entitled to

exemption and would not constitute part of the total

income.

(4) The educational institutions, which are

registered as a Society, would continue to retain their

character as such and would be eligible to apply for

exemption under Section 10(23C)(vi) (of Income Tax Act, 1961). [See

para 8.7 of the judgment – Aditanar Educational

Institution case (supra)].

Accordingly, the orders passed withdrawing the exemptions

were quashed with liberty to pass fresh orders.

The said view has been specifically approved by the Apex

Court in Queen's Educational Society's case (supra) and the judgment of the

Uttrakhand High Court has been reversed.

The Apex Court has accordingly discussed the predominant

objects of the educational institution and whether it exists solely for

educational purposes and not for the purposes of profit. Accordingly,

conclusion was arrived at that merely because some profit arises from the

activity which was the predominant object, it would not mean that the

charitable character of the purpose of setting of the institution would be lost.

The predominant object test was to applied which was the promotion of

education and the principles were laid down as under:-

“(1) Where an educational institution carries

on the activity of education primarily for educating

persons, the fact that it makes a surplus does not lead

to the conclusion that it ceases to exist solely for

educational purposes and becomes an institution for the

purpose of making profit.

(2) The predominant object test must be

applied - the purpose of education should not be

submerged by a profit making motive.

(3) A distinction must be drawn between the

making of a surplus and an institution being carried on

"for profit". No inference arises that merely because

imparting education results in making a profit, it

becomes an activity for profit.

(4) If after meeting expenditure, a surplus

arises incidentally from the activity carried on by the

educational institution, it will not be cease to be one

existing solely for educational purposes.

(5) The ultimate test is whether on an overall

view of the matter in the concerned assessment year the

object is to make profit as opposed to educating

persons.”

It is also pertinent to note that while relying upon the earlier

judgments of the Apex Court namely American Hotel and Lodging

Association (supra) and keeping in view the provisos of the sections in

mind especially 13th proviso which provided that after giving a reasonable

opportunity, the approval granted to the trust could be withdrawn if it is

found that the activities are not genuine or in accordance with any of the

conditions, there could be a conditional approval subject to the monitoring.

The relevant observations read thus:-

“25. We approve the judgments of the Punjab

and Haryana, Delhi and Bombay High Courts. Since

we have set aside the judgment of the Uttarakhand

High Court and since the Chief CIT's orders cancelling

exemption which were set aside by the Punjab and

Haryana High Court were passed almost solely upon

the law declared by the Uttarakhand High Court, it is

clear that these orders cannot stand. Consequently,

Revenue's appeals from the Punjab and Haryana High

Court's judgment dated 29.1.2010 and the judgments

following it are dismissed. We reiterate that the correct

tests which have been culled out in the three Supreme

Court judgments stated above, namely, Surat Art Silk

Cloth, Aditanar, and American Hotel and Lodging,

would all apply to determine whether an educational

institution exists solely for educational purposes and

not for purposes of profit. In addition, we hasten to add

that the 13th proviso to Section 10(23C) (of Income Tax Act, 1961) is of great

importance in that assessing authorities must

continuously monitor from assessment year to

assessment year whether such institutions continue to

apply their income and invest or deposit their funds in

accordance with the law laid down. Further, it is of

great importance that the activities of such institutions

be looked at carefully. If they are not genuine, or are

not being carried out in accordance with all or any of

the conditions subject to which approval has been

given, such approval and exemption must forthwith be

withdrawn. All these cases are disposed of making it

clear that revenue is at liberty to pass fresh orders if

such necessity is felt after taking into consideration the

various provisions of law contained in Section 10(23C) (of Income Tax Act, 1961)

read with Section 11 (of Income Tax Act, 1961).”

In the present case, under the second proviso, the authority was

to call for documents including audited annual accounts from the trust and

in order to satisfy itself about the genuineness of the activities of the trust, the inquiries had to be made. The objects of the petitioner-trust read thus:-

“2. OBJECTS OF THE TRUST

(a) To spread education and for achieving the

said object to establish, maintain, run, develop and

improve, extend, grant donations in cash and kind and

assist in the establishment, running, development,

improvement and extension of schools, colleges,

workshop, industrial and technical schools, institutions

for the promotion of agriculture, hostels for the benefit

of needy students, maintain agriculture farms for the

benefit of the poor.

(b) To establish, maintain or acquire library

or libraries for the benefit of the students community.

(c) To institute and award scholarships in

India for the study, research and apprenticeship for all

or any of the aforesaid educational purpose.

(d) To establish, maintain, run, develop,

improve, extend, grant donations for and to aid and

assist in the establishment maintenance, running,

development, improvement and extension of hospitals,

clinics, XRay plants, dispensaries, maternity houses,

recreating centres and all similar institutions as will

afford treatment to alleviate human sufferings.

(e) To conduct feeding to poor generally give

food and raiment to the poor, needy and disabled

persons and to afford relief to people in distress due to

natural calamities, accident, earthquake, flood,

famine,. Epidemic orphanages and welfare

institutions.

(f) To carry on community development

programmes for the upliftment of the economically

weaker sections of the society and construct and

develop community centres or halls for carrying on

such activities.

(g) To provide food, shelter, clothing, medical

care and education for the needy.

(h) To provide assistant to best players and

also to promote various sports by organizing

tournaments in the interest of the Public.

(i) To carry out other business as decided by

the Trustees.”

It is not disputed that the school as such is also affiliated with

the Central Board of Secondary Education, New Delhi and has also been

granted registration under Section 12-A (of Income Tax Act, 1961) w.e.f. 15.07.1997. Merely because

one of the clauses of the trust deed provided that the trust would carry on

other business as decided by the trustees would not per se dis-entitle it from being considered for registration under Section 10(23C)(vi) (of Income Tax Act, 1961). The reasoning that the Trust had intentions to carry out the business and the said institute was not existing solely for educational purposes would amount to giving a very narrow meaning to the section and the predominant object test was to be applied. As noticed above, it was not that respondent no. 1 came to the conclusion that the Trust was doing some other business and the said business was generating substantial amounts which would over ride the main objects of the trust which have been reproduced above which pertain mainly to the cause of education. Keeping in view the principles which have been discussed regarding the words 'solely for educational purposes and of generating profit', we are of the opinion that in the absence of any such finding that the trust was doing business, the application could not have been rejected only on this ground that one of the clauses in the objects provided such right to the trust. The prescribed authority could have made it conditional by holding that if any such business is carried out, the registration granted is liable to be cancelled. The principles laid down by the Apex Court in American Hotel and Lodging Association's case (supra) can thus be also applied in the circumstances. The said principles read thus:-

“33. Having analysed the provisos to Section 10 (of Income Tax Act, 1961)

(23C)(vi) one finds that there is a difference between

stipulation of conditions and compliance thereof. The

threshold conditions are actual existence of an

educational institution and approval of the prescribed

authority for which every applicant has to move an

application in the standardized form in terms of the

first proviso. It is only if the pre-requisite condition of

actual existence of the educational institution is

fulfilled that the question of compliance of

requirements in the provisos would arise. We find merit

in the contention advanced on behalf of the appellant

that the third proviso contains monitoring

conditions/requirements like application, accumulation,

deployment of income in specified assets whose

compliance depends on events that have not taken place

on the date of the application for initial approval.

34. To make the section with the proviso

workable we are of the view that the Monitoring

Conditions in the third proviso like

application/utilization of income, pattern of investments

to be made etc. could be stipulated as conditions by the

PA subject to which approval could be granted. For

example, in marginal cases like the present case, where

appellant-Institute was given exemption up to financial

year ending 31.3.1998 (assessment year 1998-99) and

where an application is made on 7.4.1999, within seven

days of the new dispensation coming into force, the PA

can grant approval subject to such terms and

conditions as it deems fit provided they are not in

conflict with the provisions of the 1961 Act (including

the abovementioned monitoring conditions). While

imposing stipulations subject to which approval is

granted, the PA may insist on certain percentage of

accounting Income to be utilized/applied for imparting

education in India. While making such stipulations, the

PA has to examine the activities in India which the

applicant has undertaken in its Constitution, MoUs.

and Agreement with Government of India/National

Council. In this case, broadly the activities undertaken

by the appellant are - conducting classical education

by providing course materials, designing courses,

conducting exams, granting diplomas, supervising

exams, all under the terms of an Agreement entered

into with Institutions of the Government of India.

Similarly, the PA may grant approvals on such terms

and conditions as it deems fit in case where the Institute

applies for initial approval for the first time. The PA

must give an opportunity to the applicant-institute to

comply with the monitoring conditions which have been

stipulated for the first time by the third proviso.

Therefore, cases where earlier the applicant has

obtained exemption(s), as in this case, need not be re-

opened on the ground that the third proviso has not

been complied with. However, after grant of approval,

if it is brought to the notice of the PA that conditions on

which approval was given are breached or that

circumstances mentioned in the thirteenth proviso

exists then the PA can withdraw the approval earlier

given by following the procedure mentioned in that

proviso. The view we have taken, namely, that the PA

can stipulate conditions subject to which approval may

be granted finds support from sub-clause (ii)(B) in the

thirteenth proviso.”

Accordingly, we are of the view that the impugned order cannot

be justified solely on the ground that in view of a clause which provided

that the Trust could run a business, it would be debarred as such from

registration on the ground that it was not existing solely for educational

purposes. That merely a conferment of power to do business would not

debar the right for consideration to the trust without any finding being

recorded that the predominant object of the Trust was to do business. Thus,

respondent no. 1 misdirected itself by rejecting the application on this

ground without coming to any conclusion that the trust was carrying on any

other activity as per clause (i). It is also a matter of fact, as noticed, now that the trust has already also deleted the objectionable clause and which has also been noticed in the subsequent assessment made in the assessment order dated 21.12.2012 for the year 2010-11.

Accordingly, the writ petition is allowed and the impugned

order dated 17.09.2012 (Annexure P-5) is quashed. The competent

authority shall decide the said application afresh keeping in view the

observations made hereinabove.

(S.J. VAZIFDAR)

ACTING CHIEF JUSTICE

(G.S. SANDHAWALIA)

JUDGE

06.07.2015

×

Similar Ripples

Questions

Trust’s Business Clause Doesn’t Bar Educational Exemption

Write your CommentSimilar Posts

Generic

- Reportdata/3644.pdf