Full News

Please allow me fulfilling your dream of owning that beautiful park facing the corner home with shining marble flooring, with oil painted doors...

Please allow me fulfilling your dream of owning that beautiful park facing the corner home with shining marbl…

Please let me help you buy that luxurious roof-open car you saw in that fabulous car showroom which immediately stole your heart and raised a desire to go on a long weekend drive with your lovely family or your other substantial one... in just 3 steps.

Pull out your calculator... may be that old casio one or on your smart phone... doesn't matter...

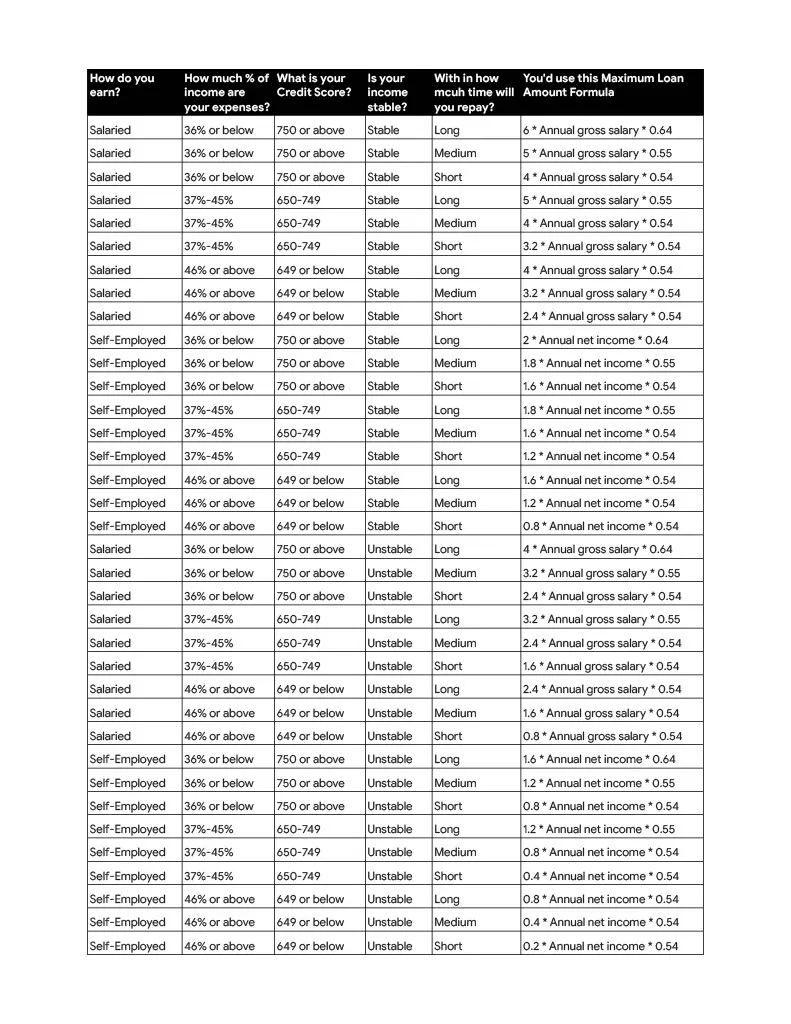

Watch the below table to locate the category you fall in...and the formula in the last column...

Punch your figures in the calculator and VOILA you can get this much of loan... Is it sufficient to buy your dreams...

Yes? or No?

If no, then think of someone close... who will let you his (her) name as a co-borrower... Add his(her) figures...

Sufficient? Yes...

Go...Run...Rush to your banker.. tell him you want a loan to buy your dreams...

Here's the table...

You may say in a nutshell that:

- Salaried employees in India can typically get a home loan amount up to 6 times their annual gross salary.

- Self-employed individuals and professionals can typically get a home loan amount up to 2-3 times their annual net income or up to 80% of the property value, whichever is lower.

- The age of the borrower plays an important role in determining home loan eligibility.

- The RBI has capped the LTV ratio for home loans at 90% for loans of up to Rs 30 lakh, 80% for loans of above Rs 30 lakh and up to Rs 75 lakh and 75% for loans above Rs 75 lakh.

For example,

A salaried employee with an annual gross salary of Rs. 10 lakh, 35 years old and has a good credit score, can be eligible for a home loan amount of up to Rs. 60 lakh. However, the RBI's LTV ratio caps the loan amount at Rs. 45 lakh. This means that the borrower would need to make a down payment of Rs. 5 lakh.

If the borrower were self-employed, they would likely be eligible for a lower home loan amount. For example, if their annual net income is Rs. 5 lakh, they would be eligible for a home loan amount of up to Rs. 15 lakh. However, the LTV ratio would still cap the loan amount at Rs. 12 lakh. This means that the borrower would need to make a down payment of Rs. 38 lakh.

Before you read further, let me make a disclaimer - "The article here is aiming to provide general insights into loan eligibility and criteria. It serves as a starting point for further exploration and is not intended as professional financial advice. Individuals should consult with experts for personalized information based on their specific financial situations.

Now, here are the factors that determine how much home loan you can get against your salary:

- Your age: Lenders typically consider the age of the applicant when calculating the loan amount. The older you are, the lower the loan amount you will be eligible for.

- Your income: The amount of your income is one of the most important factors that lenders consider when calculating your loan eligibility. The higher your income, the higher the loan amount you will be eligible for.

- Your existing debt: Lenders will also consider your existing debt obligations when calculating your loan eligibility. The more debt you have, the lower the loan amount you will be eligible for.

- Your credit score: Your credit score is a reflection of your credit history. Lenders use your credit score to assess your risk as a borrower. The higher your credit score, the higher the loan amount you will be eligible for.

- The value of the property: The value of the property you are buying is also a factor that lenders consider when calculating your loan eligibility. The higher the value of the property, the higher the loan amount you will be eligible for.

Here are some tips for increasing your home loan eligibility:

- Increase your income: One of the best ways to increase your home loan eligibility is to increase your income. This can be done by getting a raise at your current job, getting a second job, or starting your own business.

- Pay down your debt: Another way to increase your home loan eligibility is to pay down your debt. This will free up more of your monthly income to be used for your home loan EMIs.

- Improve your credit score: A good credit score will make you a more attractive borrower to lenders. You can improve your credit score by paying your bills on time, keeping your credit utilization low, and avoiding late payments and defaults.

- Choose a property with a lower value: If you are buying a property with a lower value, you will be eligible for a higher loan amount.

By following these tips, you can increase your home loan eligibility and get the financing you need to buy your dream home.

×