Full News

Imported Goods confiscated? These 15 Court Decisions Could Be Your Lifeline!

Imported Goods confiscated? These 15 Court Decisions Could Be Your Lifeline!

What if you find yourself in a situation where you've imported restricted goods without a license? Or your import lands at an unauthorized port? These are not just hypotheticals, but real situations that could land you in a sea of legal complications. Similarly, imagine a scenario where customs revalues your imported goods relying on NIDB data. This could throw your financial calculations off balance and leave you scrambling to make sense of the new valuation. And what about high sea purchases made on forged documents? This could potentially lead to serious legal trouble and damage your business reputation. Or consider a situation where your CHA licensed employee decides to open his own CHA agency. This could lead to conflicts of interest and potential legal disputes. And let's not forget about the possibility of customs reclassifying your exempt imported goods under a non-exempt category. This could result in unexpected duties and taxes, impacting your bottom line. These are just a few of the many scenarios you could face in the complex world of imports and customs. So, keep this guide handy. It's filled with valuable insights and legal precedents that can help you navigate these challenging situations.

Article #31402: Upholding penalties for importing old clothing without a valid license and dismissing Revenue's enhancement request, the Tribunal reinforced the strict interpretation of licensing requirements for restricted goods.(Please right click me to read in full)

Article #31415: Overturning the confiscation of rough diamonds based on a re-determined value, the Tribunal upheld the validity of the Kimberley Process Certificate, underscoring the need for adherence to international regulations. (Please right click me to read in full)

Article 31406: The Tribunal dismissed the Revenue's appeal for enhancing redemption fine @ 19.5% and penalties @ 7.8% of the assessed value on the import of old clothing without a valid license.(Please right click me to read in full)

Article #31408: In a case involving technical violations by a Customs House Agent, the Tribunal quashed penalties because a procedural lapse by the Revenue authorities resulted in violation and the appellants had acted in good faith.(Please right click me to read in full)

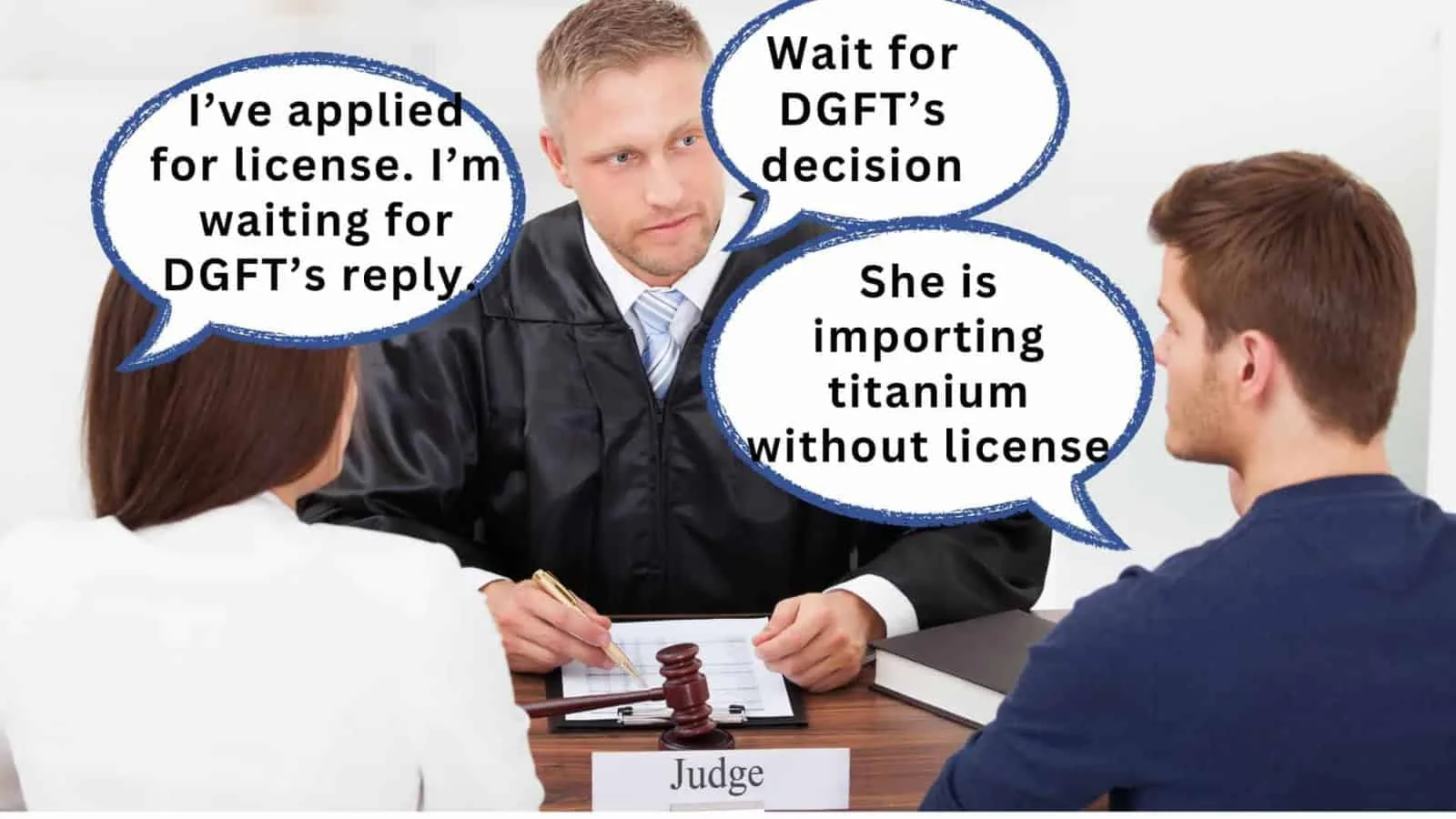

Article #31409: Remanding a case involving the import of restricted titanium powder, the Tribunal instructed the authorities to await the importer's pending license application, showcasing a nuanced approach to facilitating compliance.(Please right click me to read in full)

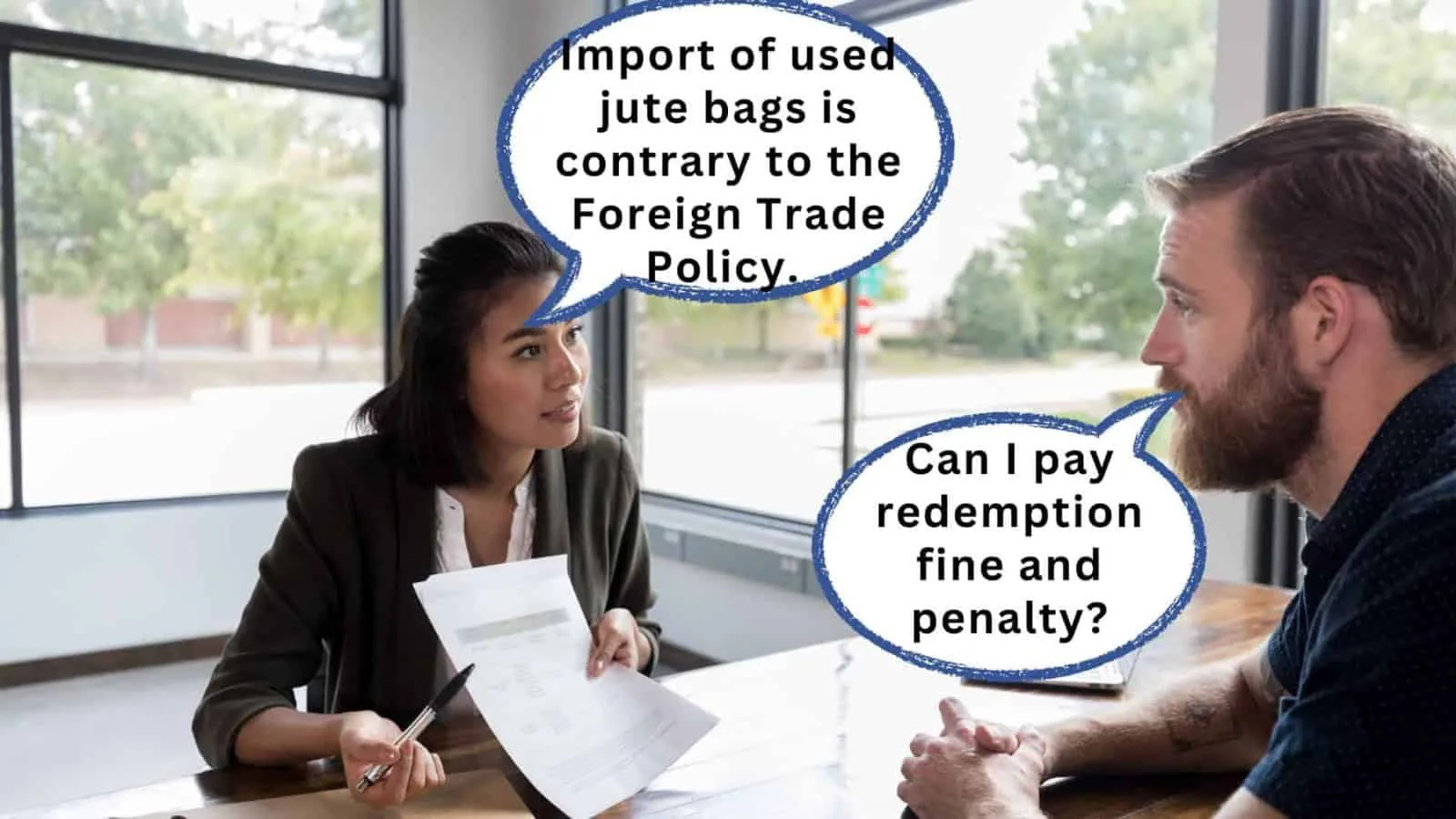

Article #31310: In a nuanced ruling, the Customs Tribunal upheld the penalty for restriction on importing used jute bags while reducing the redemption fine, highlighting that the redemption fine cannot exceed the market value of the goods less the duty payable. (Please right click me to read in full)

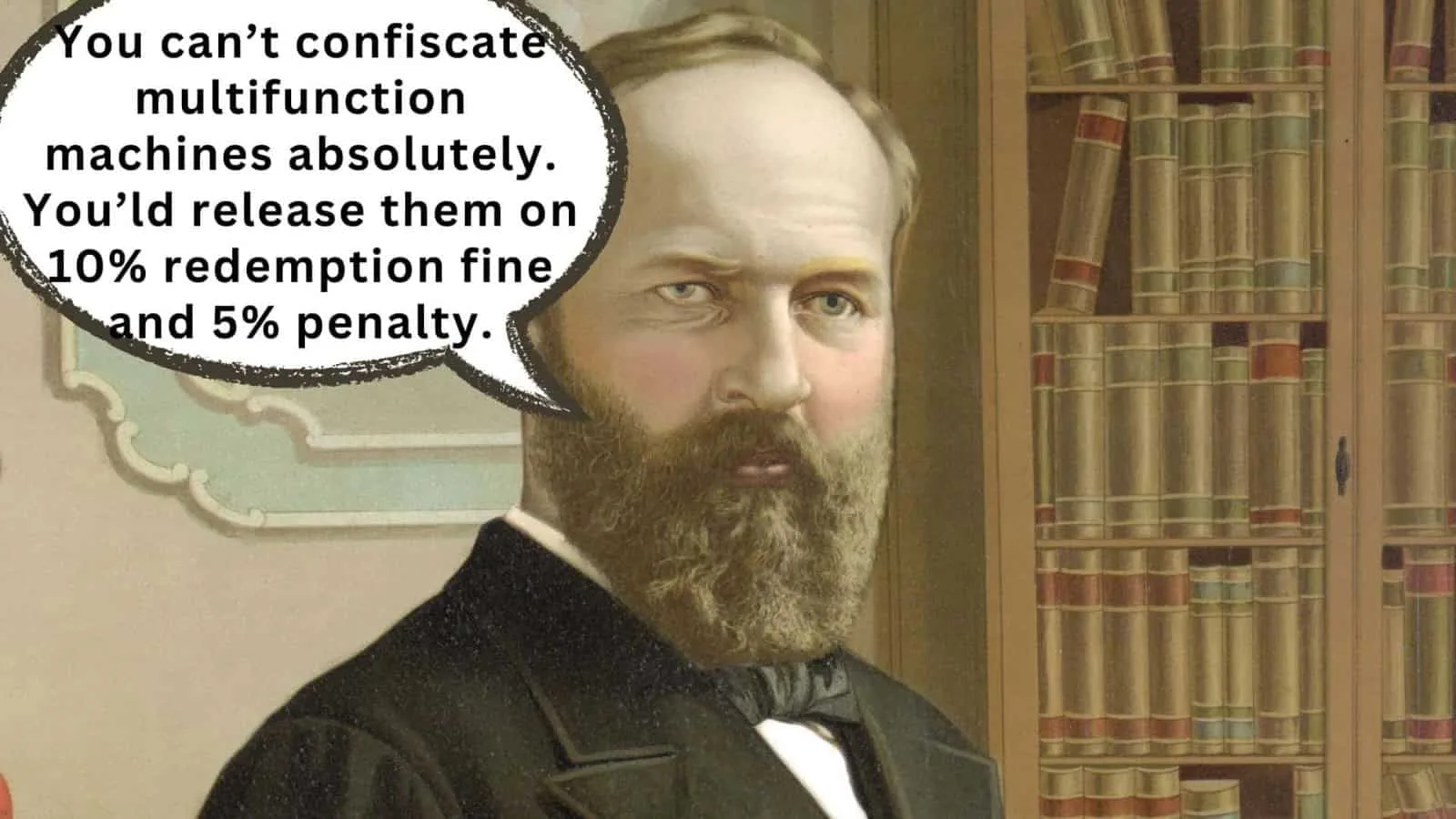

Article #31405: The Tribunal reduced the redemption fine and penalty for importing used multifunction machines, striking a balance between deterrence and proportionality in enforcement actions.(Please right click me to read in full)

Article #31407: In a nuanced ruling, the Tribunal allowed the import of deodorants in a not authorised port by imposing a penalty for a port violation, demonstrating a balanced approach to trade facilitation and regulatory enforcement. (Please right click me to read in full)

Article #819: The Supreme Court set aside a duty demand not pursuant to a show cause notice and adjudication, emphasizing the importance of due process in customs proceedings. (Please right click me to read in full)

Article #2604: The Tribunal allowed the reprocessing and clearance of imported food items failing quality standards, subject to payment of fines and conformity to prescribed standards, showcasing a pragmatic approach to trade facilitation. (Please right click me to read in full)

Article #31414: Imposing penalties for forged phytosanitary certificates and by ordering re-export of such imported kiwi fruits, the Tribunal highlighted the severe consequences of submitting fraudulent documentation in customs clearance. (Please right click me to read in full)

Article #31413: Quashing confiscation and penalties for false duty exemption claims, the Tribunal emphasized the need for due process and evidence of willful mis-statement or suppression of facts. (Please right click me to read in full)

Article #31410: The High Court ordered the release of a foreign national's seized currency after deducting fines and penalties, upholding the principles of due process and proportionality in enforcement actions. (Please right click me to read in full)

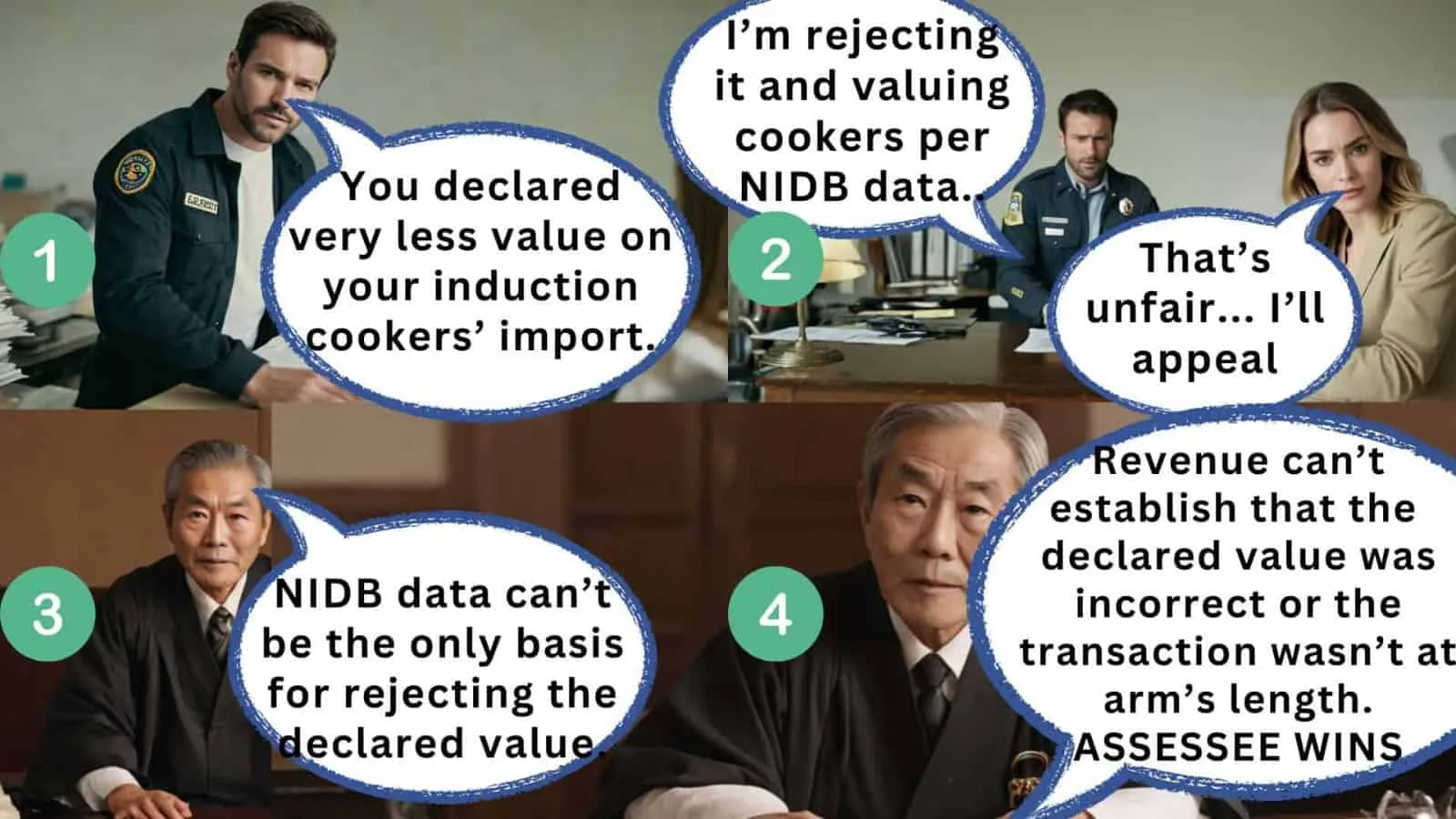

Article #31403: Overturning the re-valuation of imported induction cookers, the Tribunal upheld the declared value, setting guidelines on the use of contemporaneous data and chartered engineers' reports in valuation disputes. (Please right click me to read in full)

Article #31424: The Tribunal upheld the re-assessment of duty for current imports but set aside demands for past imports without evidence of willful mis-statement or suppression of facts, clarifying the application of the extended period of limitation. (Please right click me to read in full)

Article #31416: The Tribunal set aside the impugned orders of the Commissioner (Appeals) and allowed the department’s appeals, holding that when the importer had voluntarily accepted the enhanced value determined by customs without any protest, the department was not required to pass a speaking order justifying the enhancement. The accepted enhanced value became the declared transaction value.(Please right click me to read in full)

×