Bombay ITAT allows trader’s appeal, directs AO to restrict additions to GP rate…

Full News

Bombay ITAT allows trader’s appeal, directs AO to restrict additions to GP rate difference on disputed purchases.

Bombay ITAT allows trader’s appeal, directs AO to restrict additions to GP rate difference on disputed purcha…

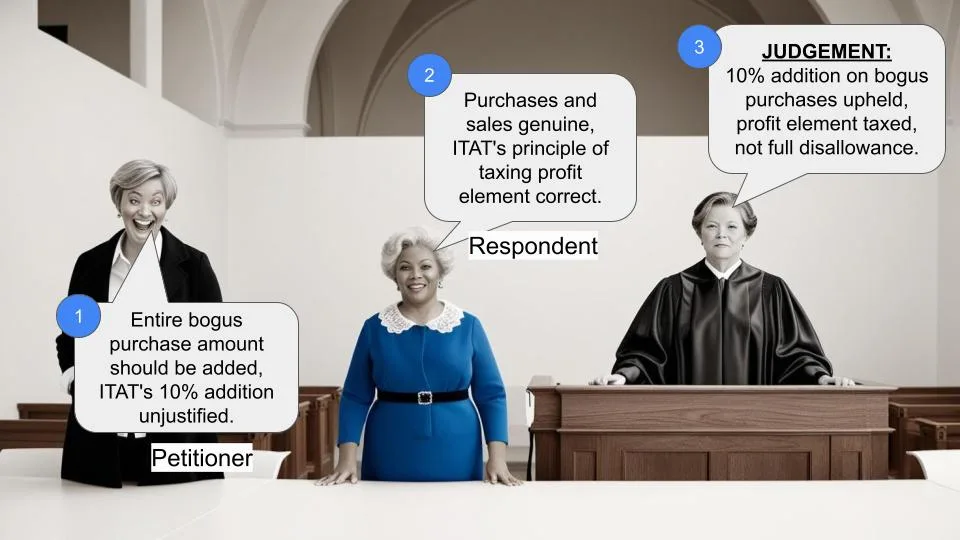

The case involves appeals filed by an assessee, a trader of ferrous and non-ferrous metals, against the CIT(A)’s order confirming the AO’s ad-hoc disallowance of 12.5% of trading purchases from alleged hawala parties. The ITAT set aside the CIT(A)’s order and directed the AO to restrict additions to the extent of bringing the GP rate on disputed purchases at the same rate as other genuine purchases, following the Bombay High Court’s decision in Mohommad Haji Adam & Co & Ors.

Case Name:

Shri Dilip Kumar Sumermal Kanungo vs. ITO 19(1)(4) (ITAT Mumbai)

Key Takeaways:

- The ITAT followed the Bombay High Court’s decision in Mohommad Haji Adam & Co & Ors, which held that purchases cannot be rejected without disturbing the sales in case of a trader.

- The ITAT directed the AO to restrict additions to the extent of bringing the GP rate on disputed purchases at the same rate as other genuine purchases.

- The decision emphasizes the principle that additions should be limited to the difference in GP rates when sales are accepted by the revenue.

Issue:

Whether the CIT(A) was correct in confirming the AO’s ad-hoc disallowance of 12.5% of trading purchases from alleged hawala parties, or whether the additions should be restricted to the extent of bringing the GP rate on disputed purchases at the same rate as other genuine purchases.

Facts:

The assessee, a trader of ferrous and non-ferrous metals, filed returns for AY 2009-10 and AY 2011-12.

The AO received information from the Sales Tax Department that the assessee had obtained bogus purchase bills from 8 parties.

Notices issued to those parties were returned unserved, and the assessee failed to produce them for examination.

The AO estimated profit at 12.5% of the disputed purchases and brought it to tax.

The CIT(A) confirmed the AO’s addition, distinguishing the case from Mohommad Haji Adam & Co & Ors.

Arguments:

Assessee’s Argument: The judgment in Mohommad Haji Adam & Co & Ors is applicable, and the CIT(A) should have followed it. Purchases cannot be rejected without disturbing the sales in case of a trader.

Revenue’s Argument: The estimation of 12.5% by the AO and confirmation by the CIT(A) is correct. The CIT(A) rightly distinguished the case from Mohommad Haji Adam & Co & Ors.

Key Legal Precedents:

Mohommad Haji Adam & Co & Ors (2019) 104 CCH 0391 (Bombay High Court) N.K. Industries Ltd. v. DCIT (Tax Appeal No. 240 of 2003, Gujarat High Court)

Judgement:

The ITAT set aside the CIT(A)’s order and directed the AO to restrict additions to the extent of bringing the GP rate on disputed purchases at the same rate as other genuine purchases, following the Bombay High Court’s decision in Mohommad Haji Adam & Co & Ors.

The ITAT found the facts in the instant case similar to the cited precedent, where the High Court held that purchases cannot be rejected without disturbing the sales in case of a trader.

FAQs:

Q1. What is the significance of the Bombay High Court’s decision in Mohommad Haji Adam & Co & Ors?

A1. The Bombay High Court held that purchases cannot be rejected without disturbing the sales in case of a trader. Additions should be limited to the extent of bringing the GP rate on disputed purchases at the same rate as other genuine purchases.

Q2. Why did the ITAT set aside the CIT(A)’s order?

A2. The ITAT found the facts in the instant case similar to the Mohommad Haji Adam & Co & Ors case and followed the Bombay High Court’s decision, which held that additions should be restricted to the difference in GP rates when sales are accepted by the revenue.

Q3. What was the ITAT’s direction to the AO?

A3. The ITAT directed the AO to restrict additions to the extent of bringing the GP rate on disputed purchases at the same rate as other genuine purchases.

Q4. What is the implication of this decision for traders?

A4. This decision reinforces the principle that when sales are accepted by the revenue, additions should be limited to the difference in GP rates on disputed purchases, rather than rejecting the entire purchases.

Q5. Does this decision have any impact on the legal principles established in N.K. Industries Ltd. v. DCIT?

A5. The ITAT did not explicitly discuss the impact on the N.K. Industries Ltd. case, but it followed the Bombay High Court’s decision, which distinguished the facts from the Gujarat High Court’s decision in N.K. Industries Ltd.

1. The captioned appeals filed by the assessee are directed against the order of the order of the Commissioner of Income Tax (Appeals)-5, Mumbai [in short ‘CIT(A)’] and arise out of the assessment completed u/s 143(3) (of Income Tax Act, 1961) r.w.s. 147 (of Income Tax Act, 1961), (the ‘Act’). For the sake of convenience, as common issues are involved, we are proceeding to dispose off these appeals by a consolidated order. Facts being identical, we begin with the AY 2009-10.

2. The ground of appeal filed by the assessee reads as under:

“That the Id. C.I.T (Appeals) has erred in confirming the ad-hoc disallowance made by the A.O. at Rs.15,51,341/- being 12.5% of trading purchases of Rs.1,24,10,733/- from the alleged hawala parties, treating the same as non-genuine merely on the basis of information received from Sales Tax Department of Government of Maharashtra without bringing any contrary evidence on record or doing any own worthwhile independent investigation and also without properly appreciating the facts of the case and law and also various documentary evidences and details furnished and also cogent explanation offered on record. Being the alleged disallowance made by A.O. &

confirmed by Id. C.I.T. (Appeals) wrong on facts and bad in law therefore same may kindly be deleted.”

3. Briefly stated, the facts of the case are that the assessee filed his return of income for the assessment year (AY) 2009-10 on 30.03.2010 declaring total income of Rs.4,49,838/-. Here the assessee is a reseller of ferrous and non- ferrous metals. The Assessing Officer (AO) completed the assessment u/s 143(3) (of Income Tax Act, 1961) on 30.12.2011 determining the income at Rs.4,75,249/-. On receipt of information from the Sales Tax Department, Government of Maharashtra that the assessee had obtained bogus purchase bills amounting to Rs.1,24,10,733/- from 8 parties, the AO issued notice u/s 148 (of Income Tax Act, 1961) for reopening the assessment. During the course of re-assessment proceedings, the AO issued notice u/s 133(6) (of Income Tax Act, 1961) to the said parties to verify the genuineness of the purchases.

However, those notices were returned un-served by the postal authorities with the remark “left”, “not traceable”, “not known” etc. Thereafter, the AO asked the assessee to produce those parties for examination. However, the assessee failed to do so. Having examined the details filed by the assessee, the AO noted that the assessee could not file important documents such as delivery challans, transport receipts, goods-inward register maintained in the godown. Considering the above facts, the AO estimated the profit @ 12.5% of the disputed purchases of Rs.1,24,10,733/- and accordingly brought to tax Rs.15,51,341/-.

4. In appeal, the Ld. CIT(A) vide order dated 27.05.2019 confirmed the above addition made by the AO by observing that :

“8.4.8. From the facts available on records, it is observed that in the present case also the AO has neither disbelieved the purchases nor the corresponding sales/works made. The AO has held that the impugned purchases were not made from above referred dealers/parties but from somewhere else/ open market. The facts and circumstances of the present case are similar to that of facts adjudicated by the Hon'ble Gujarat High Court and Hon'ble ITAT, Mumbai in above referred cases. Since, the action of the AO is in conformity with above referred decisions, no fault can be found with the action of the AO in disallowing 12.5% of such purchases. Hence, the impugned disallowance of Rs.15,51,341/- is confirmed.”

5. Before us, the Ld. counsel for the assessee submits that in the facts and

circumstances of the case, the judgment of the Hon’ble Bombay High Court in the case of Pr. CIT v. Mohommad Haji Adam & Co & Ors (2019) 104 CCH 0391 is applicable and the Ld. CIT(A) should have followed it, when it was cited before him during the course of appeal hearing.

On the other hand, the Ld. Departmental Representative (DR) supports the estimation of 12.5% done by the AO and then confirmed by the Ld. CIT(A). Further, it is stated by him that considering the facts of the present case, the Ld. CIT(A) has rightly distinguished the decision in Mohommad Haji Adam & Co & Ors (supra).

6. We have heard the rival submissions and perused the relevant materials on record. The Ld. CIT(A) has distinguished the present case of the assessee from Mohommad Haji Adam & Co & Ors (supra) (hereafter “that case”) on the ground that (i) in that case, the assessee was a trader in cotton and man-made fabrics on retails as well as semi wholesale basis and mainly dealt in suiting and shirting materials, whereas in the present case, the appellant is engaged in trading of ferrous and non-ferrous metals, (ii) in that case, it is observed that though during the course of survey operations u/s 133A (of Income Tax Act, 1961), bogus/hawala/suspicious parties concerned therein in their statement had admitted that they are engaged in issuing bogus/ hawala bills, but subsequently, all the three parties concerned therein had filed affidavits stating that as far as assessee is concerned they had actually made sales ; whereas in the present case, the AO in the assessment order has given a factual finding that in order to verify the genuineness of the transaction, notices u/s 133(6) (of Income Tax Act, 1961) were issued to the said parties at the address provided by the assessee, however, said notices could not be served and returned back un-served by the postal authorities with the remarks “left”, “not traceable” “not known” etc. and

(iii) in that case, the Bombay High Court while dismissing all appeals has held that “in these circumstances, no question of law, therefore arises”; hence, the order of the Tribunal, in the facts and circumstances of that case has been confirmed and no question of law arises.

6.1 At this moment, let us narrate at length the decision in Mohommad Haji Adam & Co & Ors (supra). In that case, during the course of survey operations in the case of entities from whom the assessee had claimed to have made purchases, the Department collected information suggesting that such purchases were not genuine. The AO noticed that the assessee had shown

purchases of fabrics worth Rs.29.41 lakhs from three group concerns, namely

M/s Manoj Mills, M/s Astha Silk Industries and M/s Shri Ram Sales and Synthetics. On the basis of statement recorded during such survey operations, the AO concluded that the selling parties were engaged only in supplying the bogus bills, that the goods in question were never supplied to the assessee, and therefore, the purchases were bogus. He, therefore, added the entire sum in the hands of the assessee as its additional income. The assessee carried the matter in appeal before the CIT(A), who accepted the factum of purchases being bogus.

However, he compared the purchases and sales statements of the assessee and

observed that the Department had accepted the sale, and therefore, there was

no reason to reject the purchases, because without purchases there cannot be sales. He, therefore, held that under these circumstances the AO was not correct in adding the entire amount of purchases as the assessee’s income. He, therefore, deleted the addition refreshing it to 10% of the purchase amount. He also directed the AO to make addition to the extent of difference between the gross profit rate as per the books of accounts on undisputed purchases and gross profit on sales relating to the purchases made from the said three parties. The assessee carried the matter before the Tribunal. The Revenue also carried the issue before the Tribunal. The Tribunal allowed the appeal of the assessee partly and dismissed that of the Revenue. The Tribunal noted that the CIT(A) had not given any reasons for retaining 10% of the purchases by way of ad-hoc additions. The Tribunal, therefore, deleted such additions, but retained the portion of the order of the CIT(A) to that extent he permitted the AO to tax the assessee on the basis of difference in the GP rates. In further appeal before the Hon’ble Bombay High Court, the Revenue referred to the decision of the Division Bench of the Hon’ble Gujarat High Court in the case of N.K. Industries Ltd. v. DCIT in Tax Appeal No. 240 of 2003 and connected appeals decided on 20.06.2016 and also pointed out that the SLP against such decision was dismissed by the Hon’ble Supreme Court. The Hon’ble Bombay High Court held :

“8. In the present case, as noted above, the assessee was a trader of fabrics. The A.O. found three entities who were indulging in bogus billing activities. A.O. found that the purchases made by the assessee from these entities were bogus. This being a finding of fact, we have proceeded on such basis. Despite this, the question arises whether the Revenue is correct in contending that the entire purchase amount should be added by way of assessee's additional income or the assessee is correct in contending that such logic cannot be applied. The finding of the CIT(A) and the Tribunal would suggest that the department had not disputed the assessee's sales. There was no discrepancy between the purchases shown by the assessee and the

sales declared. That being the position, the Tribunal was correct in coming to the conclusion that the purchases cannot be rejected without disturbing the sales in case of a trader. The Tribunal, therefore, correctly restricted the additions limited to the extent of bringing the G.P. rate on purchases at the same rate of other genuine purchases. The decision of the Gujarat High Court in the case of N.K. Industries (supra) cannot be applied without reference to the facts. In fact in paragraph 8 of the same Judgment the Court held and observed as under-

“So far as the question regarding addition of Rs.3,70,78,125/- as gross profit on sales of Rs.37.08 Crores made by the Assessing Officer despite the fact that the said sales had admittedly been recorded in the regular books during Financial Year 1997-98 is concerned, we are of the view that the assessee cannot be punished since sale price is accepted by the revenue. Therefore, even if 6 % gross profit is taken into account, the corresponding cost price is required to be deducted and tax cannot be levied on the same price. We have to reduce the selling price accordingly as a result of which profit comes to 5.66 %. Therefore, considering 5.66 % of Rs.3,70,78,125/- which comes to Rs.20,98,621.88 we think it fit to direct the revenue to add Rs.20,98,621.88 as gross profit and make necessary deductions accordingly. Accordingly, the said question is answered partially in favour of the assessee and partially in favour of the revenue.”

6.2 In Mohommad Haji Adam & Co & Ors (supra), to put it simply, the AO found three entities who were indulging in bogus billing activities, the AO found that the purchases made by the assessee from these entities were bogus. The finding of the CIT(A) and the Tribunal would suggest that the Department had not disputed the assessee's sales. There was no discrepancy between the purchases shown by the assessee and the sales declared. That being the position, the Tribunal was correct in coming to the conclusion that the purchases cannot be rejected without disturbing the sales in case of a trader. The Tribunal, therefore, correctly restricted the additions limited to the extent of bringing the GP rate on purchases at the same rate of other genuine purchases. The Hon’ble Bombay High Court held that “no purchases can be rejected without disturbing the sales in case of a trader thus, additions limited to the extent of brining the GP rate on purchases at the same rate of other genuine purchases”.

We find that the facts in the instant case are similar to the above decision. Following the same, we set aside the order of the Ld. CIT(A) and direct the AO to restrict the additions limited to the extent of bringing the G.P. rate on disputed purchases at the same rate of other genuine purchases.

Facts being identical, our decision for the AY 2009-10 applies mutatis

mutandis to AY 2011-12.

7. In the result, the appeals are allowed for statistical purposes.

Order pronounced in the open Court on 16/03/2021.

Sd/- Sd/-

(VIKAS AWASTHY) (N.K. PRADHAN)

JUDICIAL MEMBER ACCOUNTANT MEMBER

×

Similar Ripples

Questions

Bombay ITAT allows trader’s appeal, directs AO to restrict additions to GP rate difference on disputed purchases.

Write your CommentSimilar Posts

Generic

- Reportdata/6661.pdf