Court Allows Deductions for PF and ESI Contributions Made Before Tax Return Fil…

Full News

Court Allows Deductions for PF and ESI Contributions Made Before Tax Return Filing

Court Allows Deductions for PF and ESI Contributions Made Before Tax Return Filing

This case involves an income tax appeal filed by the department against a judgment passed by the Income Tax Appellate Tribunal (ITAT) for the assessment year 1993-94. The main issue was whether the assessee (taxpayer) could claim deductions for Provident Fund (PF) and Employees' State Insurance (ESI) contributions made before filing their tax return. The court ruled in favor of the assessee, allowing these deductions.

Get the full picture - access the original judgement of the court order here

Case Name

Commissioner of Income Tax and Another vs. Dhampur Sugar Mills Ltd.(High Court of Allahabad)

Income Tax Appeal No. 564 of 2007

Date: 18th November 2016

Key Takeaways

1. Employers can claim deductions for PF and ESI contributions made before filing their tax return under section 139(1) (of Income Tax Act, 1961).

2. The 2003 amendment to the Income Tax Act is to be applied retrospectively from April 1, 1988.

3. This judgment aligns with previous Supreme Court and High Court decisions on similar issues.

Issue

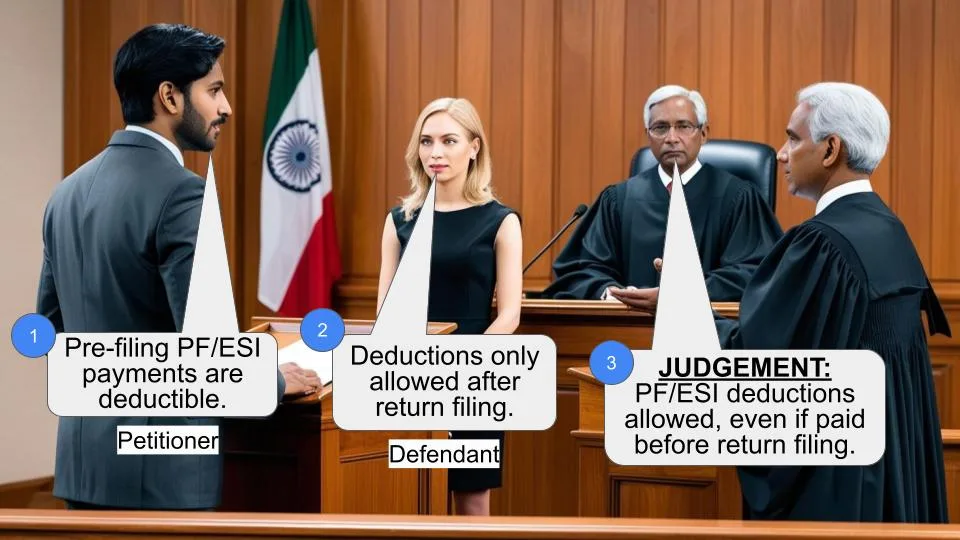

Is the assessee entitled to claim deductions for employers' and employees' contributions towards Employees' State Insurance and Provident Fund deposited prior to filing the tax return under section 139(1) (of Income Tax Act, 1961)?

Facts

1. The case relates to the assessment year 1993-94.

2. The assessee (Dhampur Sugar Mills Ltd.) made contributions to PF and ESI before filing their tax return.

3. The Assessing Officer (AO) initially disallowed these deductions, which was confirmed by the Commissioner of Income Tax (Appeals).

4. The Income Tax Appellate Tribunal (ITAT) allowed the deductions in favor of the assessee.

5. The department filed an appeal against the ITAT's decision in the High Court.

Arguments

Department's Argument:

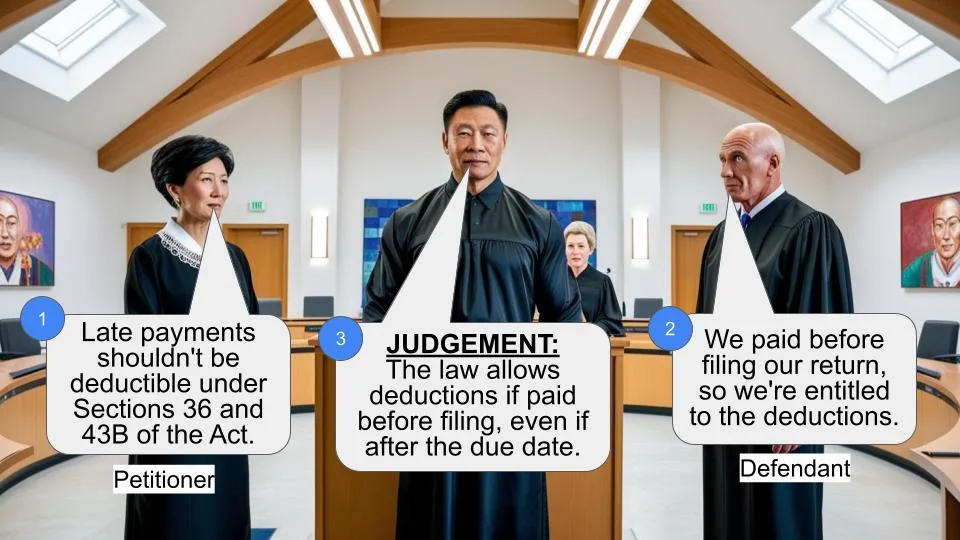

The department likely argued that the contributions should not be allowed as deductions based on the provisions of section 2(24)(x) (of Income Tax Act, 1961) read with section 36(1)(va) (of Income Tax Act, 1961).

Assessee's Argument:

The assessee argued that the contributions were made before the due date and before filing the tax return, and therefore should be allowed as deductions.

Key Legal Precedents

1. Commissioner of Income Tax vs. Alom Extrusions Ltd. (2009) 319 ITR 306 (SC): The Supreme Court held that the 2003 amendment to the Income Tax Act should be applied retrospectively from April 1, 1988, allowing the benefit of making PF payments before filing the return.

2. Commissioner of Income Tax vs. Mark Auto Industries Ltd. (2013) 358 ITR 43 (P&H): The Punjab and Haryana High Court followed the Supreme Court's decision and allowed deductions for PF and ESI contributions made before filing the return under section 139(1) (of Income Tax Act, 1961).

Judgment

The court ruled in favor of the assessee, allowing the deductions for PF and ESI contributions made before filing the tax return. The court based its decision on the following:

1. The Supreme Court's decision in the Alom Extrusions Ltd. case, which applied the 2003 amendment retrospectively.

2. The Punjab and Haryana High Court's decision in the Mark Auto Industries Ltd. case, which followed the Supreme Court's ruling.

3. The ITAT's view that the deduction should be allowed because the contributions were made before the due date and before filing the return.

The court decided question no. 3 (regarding the PF contributions) in favor of the assessee and against the department.

FAQs

Q1: What is the significance of this judgment?

A1: This judgment reinforces the principle that employers can claim deductions for PF and ESI contributions made before filing their tax return, even for earlier assessment years.

Q2: Does this judgment apply only to the specific assessment year mentioned?

A2: While the case deals with the assessment year 1993-94, the principle established applies more broadly due to the retrospective application of the 2003 amendment.

Q3: What should employers do in light of this judgment?

A3: Employers should ensure they make their PF and ESI contributions before filing their tax returns to be eligible for deductions. However, it's always best to consult with a tax professional for specific advice.

Q4: How does this judgment affect past assessments?

A4: This judgment may provide grounds for reassessment of past cases where similar deductions were disallowed. However, taxpayers should consult with tax experts to understand the implications for their specific situations.

Q5: Are there any limitations to claiming these deductions?

A5: While the judgment allows for these deductions, they must still be made before filing the tax return under section 139(1) (of Income Tax Act, 1961). Other statutory requirements and deadlines may also apply.

We have heard Sri Krishna Agarwal learned counsel counsel for the department and learned Senior Advocate Sri R.R. Agrawal assisted by Sri Suvash Agrawal learned counsel for the respondent assessee.

This income tax appeal has been filed under section 260A (of Income Tax Act, 1961) filed by the department against the judgment and order dated 29.9.2006 passed by the I.T.A.T. for the assessment year 1993-94.

As many as 14 questions have been referred to are the questions which have been answered by the decision of this court in Income Tax Appeal no.461 of 2007 except the question no.3 which reads as hereinunder:

"3. Whether on the facts and in the circumstances of the case, the Tribunal is justified in law in deleting a sum of Rs.9,79,228/- and Rs.8,81,669/- being employees' and employers contribution of PF which was disallowed by A.O. and confirmed by CIT (A) in view of legal provisions of section 2(24)(x) (of Income Tax Act, 1961) read with section 36(1)(va) (of Income Tax Act, 1961)?" This question has also been answered by the Apex Court in the case of Commissioner of Income Tax Versus Alom Extrusions Ltd. reported in 2009 (319) ITR 306 (SC) wherein the Apex Court took a view that the amendment made in the Act, 2003 was to be read as having retrospective effect from 1.4.1988 and therefore the benefit of making payment of the Provident Fund before filing of the return was allowed to the assessee.

This decision of the Apex Court has also been followed by the Punjab and Haryana High Court in the case of Commissioner of Income Tax versus Mark Auto Industries Ltd. reported in (2013) 358 ITR 43 (P&H) wherein the Punjab and Haryana High Court has also took a view that the assessee would be entitled to deductions in respect of employers and employees contributions towards the Employees State Insurance and Provident Fund deposited prior to the filing of return under section 139(1) (of Income Tax Act, 1961).

The tribunal in the present case has also taken a view that the deduction was to be allowed to the assessee because the contribution to the provident fund was deposited by the assessee before the due date and before filing of the return. Such being the circumstances on facts and in law, the question no.3 is decided in favour of the assessee and against the department.

So far as the remaining questions referred to in the appeal are concerned, Sri Krishna Agarwal learned counsel for the department has submitted that questions i.e. 1, 2, and 4 to 14 are answered by various appeals decided by this court. He states that whereas the question nos.1, 4, 7, 8, 9, 10 and, 14, referred in the present appeal have already been answered in I.T.A. no.461 of 2007 decided on 16.12.2013 in question no.4, 6, 2, 3, 7, 1 and 2 respectively.

He also states that the question nos.2, 11 and 12 in the appeal are answered while answering question no.3 referred to in I.T.A. no.334 of 2008 decided on 16.12.2013.

He further submits that the question no.5 referred to the in appeal is answered in I.T.A no.612 of 2007 decided on 16.12.2013 in question no.3 and the question no.6 in the appeal is answered in I.T.A no.220 of 2014 decided on 5.11.2014 in question no.2. He further states that the question no.13 referred to in the appeal is answered in I.T.A no.334 of 2008 decided on 16.12.2013 in question no.6.

The Court is also provided with a chart in respect of the remaining questions which have been decided by this court in previous appeals. They will abide by the decision of this court passed in the appeal filed on behalf of the department and of the same assessee respectively.

The appeal is disposed of as above. No costs. The questions referred to are answered accordingly.

Order Date :- 18.11.2016

×

Similar Ripples

Questions

Court Allows Deductions for PF and ESI Contributions Made Before Tax Return Filing

Write your CommentSimilar Posts

Generic

- Reportdata/2275_Wf4KFrL.pdf