Court Upholds Deduction for Late ESI and PF Contributions, Citing Retrospective…

Full News

Court Upholds Deduction for Late ESI and PF Contributions, Citing Retrospective Effect

Court Upholds Deduction for Late ESI and PF Contributions, Citing Retrospective Effect

This case involves an appeal by the Commissioner of Income Tax against M/s Hemla Embroidery Mills P. Ltd. regarding the deductibility of late payments of ESI and Provident Fund contributions. The High Court of Punjab & Haryana dismissed the appeal, affirming that such contributions are deductible if paid before filing the income tax return, even if paid after the due date under the respective acts.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax vs Hemla Embroidery Mills P. Ltd.(High Court of Punjab & Haryana)

ITA No. 16 of 2009

Date: 27th September 2012

Key Takeaways:

1. The Second Proviso to Section 43B (of Income Tax Act, 1961), omitted by Finance Act 2003, was clarificatory and operates retrospectively.

2. Employers can claim deductions for ESI and PF contributions if paid before filing the income tax return, even if paid after the due date under the respective acts.

3. This judgment aligns with the Supreme Court's decision in Commissioner of Income Tax v. Alom Extrusions Ltd. [2009] 319 ITR 306 (SC).

Issue:

Whether the Income Tax Appellate Tribunal (ITAT) was correct in allowing deductions for late payments of employees' and employer's contributions to Provident Fund and ESI, when such payments were made after the due dates under the respective acts but before filing the income tax return?

Facts:

- The case pertains to the assessment year 2003-04.

- The assessee (Hemla Embroidery Mills P. Ltd.) filed its return on 27.11.2003, declaring nil income after setting off losses.

- The Assessing Officer completed the assessment on 20.3.2006, determining a total income of ₹24,11,200/-.

- The assessee appealed to the Commissioner of Income Tax (Appeals), who partly allowed the appeal.

- The revenue then appealed to the Income Tax Appellate Tribunal, which dismissed the appeal.

- The revenue finally appealed to the High Court under Section 260A (of Income Tax Act, 1961).

Arguments:

Revenue's arguments:

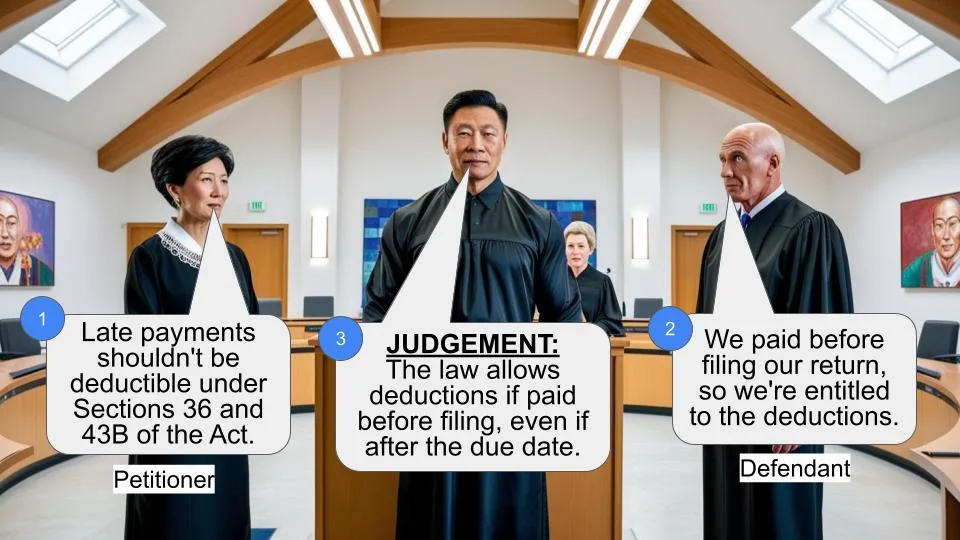

1. Late payments of employees' contributions to PF should not be allowed as deductions under Section 2(24)(x) (of Income Tax Act, 1961) read with Section 36(1)(va) (of Income Tax Act, 1961).

2. Late payments of employer's contributions should not be allowed as deductions under the second proviso to Section 43B (of Income Tax Act, 1961) read with Section 36(1)(iv) (of Income Tax Act, 1961).

3. The ITAT's decision contradicts its own earlier order and judgments from other High Courts.

Assessee's arguments (implied):

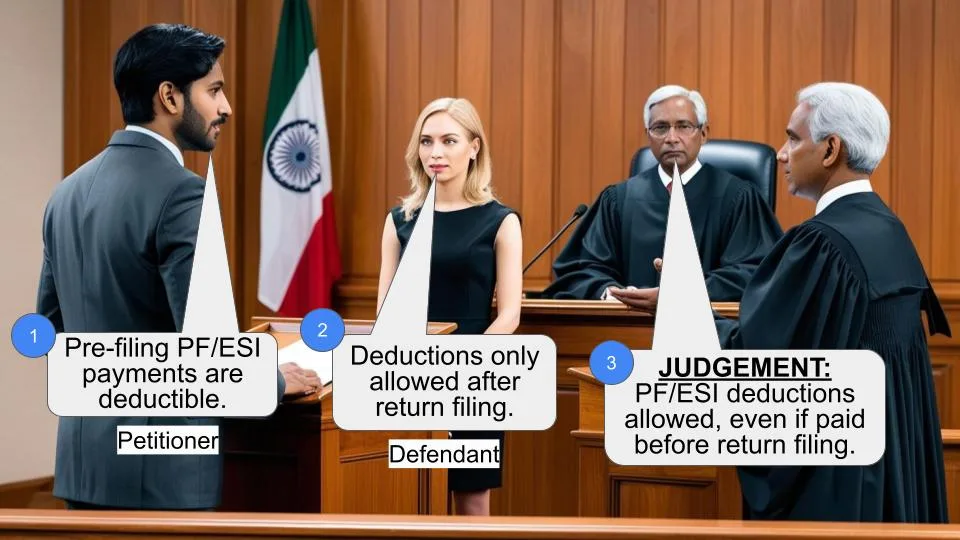

The payments were made before filing the income tax return and should be allowed as deductions.

Key Legal Precedents:

1. Commissioner of Income Tax v. Alom Extrusions Ltd. [2009] 319 ITR 306 (SC)

2. The Commissioner of Income Tax, Patiala v. M/s Rai Agro Industries Ltd. Sangrur (Income Tax Appeal No. 663 of 2005)

Judgement:

The High Court dismissed the revenue's appeal, holding that:

1. The issue is settled by the Supreme Court judgment in Alom Extrusions Ltd. and the High Court's own decision in Rai Agro Industries Ltd.

2. The Second Proviso to Section 43B (of Income Tax Act, 1961), omitted by Finance Act 2003 with effect from 1.4.2004, was clarificatory and operates retrospectively.

3. The assessee is entitled to deductions for employer and employee contributions to ESI and PF if deposited before filing the return under Section 139(1) (of Income Tax Act, 1961).

FAQs:

Q1: What was the main issue in this case?

A1: The main issue was whether late payments of PF and ESI contributions could be claimed as deductions if paid before filing the income tax return.

Q2: How did the court's decision affect taxpayers?

A2: The decision benefits taxpayers by allowing them to claim deductions for PF and ESI contributions even if paid after the due date, as long as they're paid before filing the income tax return.

Q3: What is the significance of the "retrospective" application mentioned in the judgment?

A3: It means that the clarification applies to past tax years as well, not just from the date of the amendment.

Q4: Does this judgment apply only to Punjab & Haryana?

A4: While this specific judgment is from the Punjab & Haryana High Court, it cites a Supreme Court decision, which is applicable throughout India.

Q5: What sections of the Income Tax Act were central to this case?

A5: Sections 43B, 36(1)(va), and 36(1)(iv) of the Income Tax Act were key to this case.

1. This order shall dispose of ITA No. 16 and 18 of 2009 as according to the learned counsel for the appellant, the issues involved in both the appeals are identical. For brevity, the facts are being extracted from ITA No. 16 of 2009.

2. This appeal has been preferred by the revenue under Section 260A (of Income Tax Act, 1961) (in short “the Act”) against the order dated 10.7.2008 passed by the Income Tax Appellate Tribunal, Delhi Bench “C”, New Delhi (hereinafter referred to as “the Tribunal) in ITA No. 4250/D/2007, for the assessment year 2003-04, claiming the following substantial question of law:-

I. Whether, on the facts and circumstances of the case, the Hon'ble ITAT was right in law in upholding the order of the Ld. CIT(A) in deleting the addition of Rs.7,46,296/- made by the AO u/s 2(24)(x) (of Income Tax Act, 1961) read with Section 36(1)(va) (of Income Tax Act, 1961) on account of late payment of employees' contribution to Provident Fund without appreciating the fact that the payments were made beyond the due dates?

II. Whether on the facts and in the circumstances of the case, the Hon'ble ITAT was right in law in upholding the order of the Ld. CIT(A) in deleting the addition of Rs.8,32,776/- made by the Assessing Officer on account of late payment of employer's contribution in terms of second proviso to section 43B (of Income Tax Act, 1961) read with section 36(1)(iv) (of Income Tax Act, 1961) in contravention of the decisions of Hon'ble Kerala High Court in the case of CIT Vs. GTN Textiles Ltd. (269-ITR-282), CIT Vs. Jai Ram and Sons (269-ITR-285), CIT Vs. Common Wealth Trust (P) Ltd. (269-ITR-290) and CIT Vs. South India Corporation Ltd. (242-ITR-114)?

III. Whether on the facts and in the circumstances of the case, the Hon'ble ITAT was right in law in upholding the order of the Ld. CIT(A) in deleting the additions made on account of late payments to provident fund, when it has itself held in its order passed by ITAT, 'H' Bench, New Delhi in ITA No. 2090/Del/2005 in the case of M/s SSP Ltd., 19-DLF Indl. Area-II, Faridabad for the Asstt. Year 2001-02 by relying upon the judgment of the Hon'ble Madras High Court in the case of CIT Vs. Synergy Financial Exchange Ltd. (205 CTR 481) that provident fund payment made after the due dates under the Provident Fund Act were not deductible in view of the second proviso to section 43B (of Income Tax Act, 1961), as it then was in force?

3. Briefly stated, the facts necessary for adjudication of the present appeal as narrated therein are that the assessee filed its return on 27.11.2003 declaring nil income after setting off the losses. The assessment in this case was completed vide order dated 20.3.2006 (Annexure A-1) by the Assessing Officer at a total income of ` 24,11,200/-. Feeling aggrieved, the assessee filed an appeal before the Commissioner of Income Tax (Appeals) [in short “the CIT(A)”]. The CIT(A) vide order dated 14.8.2007 (Annexure A-2) partly allowed the appeal. Against the order of the CIT(A), the revenue filed an appeal before the Tribunal. The Tribunal vide order dated 10.7.2008 (Annexure A-3) dismissed the appeal. Hence the present appeal by the revenue.

4. We have heard the learned counsel for the appellant.

5. Learned counsel for the appellant could not dispute that the issue raised herein finally stands settled by the Apex Court judgment in Commissioner of Income Tax v. Alom Extrusions Ltd. [2009] 319 ITR 306 (SC) and this Court in Income Tax Appeal No. 663 of 2005 (The Commissioner of Income Tax, Patiala v. M/s Rai Agro Industries Ltd. Sangrur), decided on 30.11.2010 wherein it has been held that Second Proviso to Section 43B (of Income Tax Act, 1961) omitted by Finance Act, 2003 with effect from 1.4.2004 was clarificatory in nature and was to operate retrospectively. Once that is so, in the present case, the respondent-assessee was entitled to deduction in respect of employer and employee's contribution to ESI and Provident Fund as the same had been deposited prior to the filing of the return under Section 139(1) (of Income Tax Act, 1961).

6. In view of the above, the substantial questions of law are answered against the revenue and in favour of the assessee. Consequently, the appeals are dismissed.

(AJAY KUMAR MITTAL)

JUDGE

(G.S. SANDHAWALIA)

JUDGE

September 27, 2012

IN THE HIGH COURT OF PUNJAB & HARYANA AT CHANDIGARH

ITA No. 18 of 2009

Date of Decision: 27.9.2012

Commissioner of Income Tax, Faridabad

Appellant.

Versus M/s UT Star Com. Inc Respondent.

CORAM:- HON'BLE MR. JUSTICE AJAY KUMAR MITTAL.

HON'BLE MR. JUSTICE G.S. SANDHAWALIA.

PRESENT: Mr. Tajender K. Joshi, Advocate for the appellant.

None for the respondent.

AJAY KUMAR MITTAL, J.

For orders, see ITA No. 16 of 2009 [Commissioner of

Income Tax, Faridabad v. M/s Hemla Embroidery Mills (P) Ltd].

(AJAY KUMAR MITTAL)

JUDGE

(G.S. SANDHAWALIA)

JUDGE

September 27, 2012

×

Similar Ripples

Questions

Court Upholds Deduction for Late ESI and PF Contributions, Citing Retrospective Effect

Write your CommentSimilar Posts

Generic

- Reportdata/5404.pdf