Court Allows Depreciation on Unused Plant & Machinery, Overturning Tax Tribunal…

Full News

Court Allows Depreciation on Unused Plant & Machinery, Overturning Tax Tribunal's Decision

Court Allows Depreciation on Unused Plant & Machinery, Overturning Tax Tribunal's Decision

This is interesting case where a detergent manufacturing company claimed depreciation on their plant and machinery, even though they weren't actively manufacturing that year. The tax authorities initially denied this claim, but the High Court eventually ruled in favor of the company. It's a bit of a rollercoaster ride through the tax appeal system.

Get the full picture - access the original judgement of the court order here

Case Name:

Nirma Credit and Capital Ltd. Vs Assistant Commissioner of Income Tax (High Court of Gujarat)

Tax Appeal No. 1203, 1204 and 1205 of 2006

Date: 28th June 2016

Key Takeaways:

1. Once a factory building is put to use, you can't restrict depreciation by saying only part of it was used.

2. For a block of assets, you don't need to use every single item to claim depreciation on the whole block.

3. The court emphasized that it's not necessary for all items in plant and machinery to be used simultaneously to qualify for depreciation.

Issue:

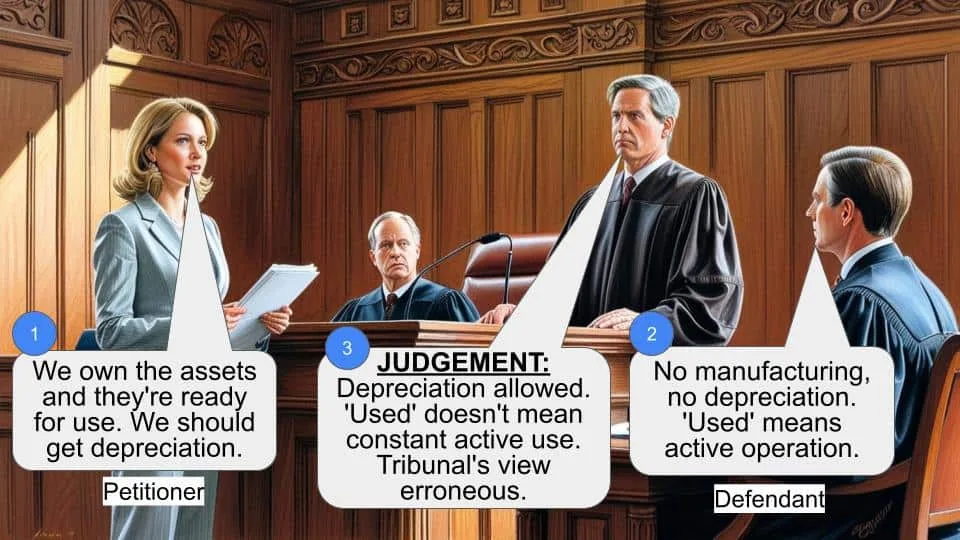

The main question here was: Can a company claim depreciation on plant and machinery when it's not actively manufacturing during the tax year?

Facts:

We've got this company, Nirma Credit and Capital Ltd., that makes detergents. During the year in question, they weren't actually manufacturing anything. But they still claimed depreciation on their plant and machinery from the previous year. The Assessing Officer said, "Nope, can't do that," and disallowed the depreciation. The company wasn't happy, so they appealed to the Commissioner of Income Tax (Appeals), who partially allowed it. Then the Revenue department wasn't satisfied, so they took it to the Income Tax Appellate Tribunal, who sided with the Revenue. Finally, it landed up in the High Court.

Arguments:

The company's side: They argued that once assets are used for business, you don't need to use every single item in the plant and machinery at the same time to claim depreciation.

The Revenue's side: They said, "Hold up! The word 'used' in Section 32 (of Income Tax Act, 1961) means the asset needs to be actually used, not just ready for use." They argued that there was no evidence the assets were actually put to use.

Key Legal Precedents:

1. Commissioner of Income-tax v. Sonal Gum Industries, [2010] 322 ITR 542 (Guj): This case established that you can't restrict depreciation on a building by saying only part of it was used.

2. An unreported decision in Tax Appeal No. 429/2007 dated 18.12.2014 by the same court was also cited.

3. The Revenue cited Dineshkumar Gulabchand Agrawal v. Commissioner of Income-tax and another, [2004] 267 ITR 768 and Deputy Commissioner of Income-tax v. Yellamma Dasappa Hospital, [2007] 290 ITR 353 (Karn) to support their argument.

Judgement:

The High Court sided with the company. They said, "Look, once you've put the factory building to use, you can't just say 'only this part was used' to limit depreciation." They also pointed out that for a block of assets, you can't cherry-pick items for depreciation. The court emphasized that as long as the assets are used for business, you don't need to use every single item in plant and machinery at the same time to claim depreciation. They felt the Tribunal made a big mistake in not allowing the depreciation.

FAQs:

1. Q: Does this mean companies can claim depreciation on all assets even if they're not actively manufacturing?

A: Not exactly. The assets still need to be used for business purposes, but they don't all need to be used simultaneously.

2. Q: How does this affect the concept of 'block of assets' in taxation?

A: It reinforces the idea that a 'block of assets' is treated as a whole for depreciation purposes, rather than considering each item separately.

3. Q: What's the practical implication for businesses?

A: This decision provides more flexibility for businesses in claiming depreciation, especially during periods of reduced activity.

4. Q: Does this apply to all types of businesses or just manufacturing?

A: While this case was about a manufacturing company, the principle could potentially apply to other types of businesses too.

5. Q: How does this align with the concept of 'ready to use' in depreciation claims?

A: The judgment seems to favor a broader interpretation of 'use', focusing on whether assets are employed in the business rather than their constant active use.

1. Tax Appeal Nos.1203/2006 to 1205/2006 under Section 260A (of Income Tax Act, 1961) of the Income tax Act, 1961 are filed against the common order dated 19.05.2006 passed by the Income Tax Appellate Tribunal in ITA Nos.18, 2515 & 2516/Ahd/2000 raising the following substantial question of law:

“Whether, on the facts and in the circumstances of the case, the Tribunal was justified in law in holding that the assessee was not entitled to depreciation on plant and machinery not put to use during the year under consideration ?”

1.1 Tax Appeal No.71/2009 is filed against the order dated 13.06.2008 passed by the Income Tax Appellate Tribunal in ITA No.2455/Ahd/2000 raising the following substantial question of law:

“Whether on facts the Tribunal's finding and conclusion of upholding the disallowance of Rs.32,81,666/ towards claim of depreciation is `vitiated' on facts and sustainable in law on interpretation of Section 32 (of Income Tax Act, 1961) ?”

1.2 As the appeals involve identical questions on law and were ordered to be heard together, they are decided by this common judgment. For the purpose of this judgment, Tax Appeal No.1203/2006 is taken as the lead matter.

2. Briefly stated, the assessee company is engaged in the business of manufacture of detergents. During the year under consideration, manufacturing activity was not carried out by the assessee. Therefore, the assessee claimed depreciation on the block of Plant & Machinery from the earlier year. However, the Assessing Officer passed the assessment order on 05.01.1998 disallowing the depreciation. Against the said order, the assessee preferred appeal before the CIT(A). The CIT(A) partly allowed the appeal vide order dated 04.10.1999. Being dissatisfied with the same, the Revenue filed appeals before the Tribunal. However, all the appeals filed by the Revenue were dismissed. Hence, these Tax Appeals.

3. When the matters were called out in the first round, learned Standing Counsel Mr. Nitin Mehta was not present. Therefore, the matters were keptback. When the matters were called out again in the second round, Mr. Nitin Mehta was not present. Therefore, a request was made to learned counsel Mr. Sudhir Mehta to assist the Court in these matters, which he agreed. Therefore, the matters were heard and decided on merits.

4. We have heard learned Senior Advocate Mr. S.N. Soparkar for the assessee in Tax Appeal Nos.1203/2006 to 1205/2006, learned counsel Mr. B.D. Karia for the assessee in Tax Appeal No.71/2009 and learned counsel Mr. Sudhir Mehta for the Revenue.

5. Learned counsel appearing on behalf of the assessee submitted that the authorities below as also the Tribunal did not allow deduction mainly on the ground that the assets for which depreciation was claimed, was not put to actual use for the year under consideration or that a part of the assets were not installed for undertaking the manufacturing process. It was submitted that the reasoning adopted by the Tribunal is erroneous since it is not necessary that all assets falling within plant and machinery have to be simultaneously used for being entitled to depreciation once it is found that the assets are used for business.

6. In support of the submission, learned Senior Advocate placed reliance upon a judgment of this Court rendered in the case of Commissioner of Incometax v. Sonal Gum Industries, [2010] 322 ITR 542 (Guj), wherein, it has been held that once that factory building is put to use, it is not possible to restrict the depreciation on the said building by stating that only a portion thereof had been put to use. Similarly, in relation to the block of assets, it is not possible to seggregate items falling within the block for the purposes of granting depreciation or restricting the claim thereof and once it is found that the assets are used for business, it is not necessary that all the items falling within plant and machinery have to be simultaneously used for being entitled to depreciation. Reliance was also placed on an unreported decision of this Court passed in Tax Appeal No. 429/2007 dated 18.12.2014.

7. Mr. Sudhir Mehta, learned counsel for the Revenue, supported the impugned order of the Tribunal and the authorities below and submitted that the word “used” in section 32 (of Income Tax Act, 1961) denotes that the asset has been actually used and not that it is merely ready for use. In the instant case, there was nothing to show that the asset had been actually put to use. Therefore, the authorities below and the Tribunal were justified in disallowing the depreciation.

7.1 In support of his submission, learned counsel Mr. Sudhir Mehta placed reliance upon the decision of Bombay High Court rendered in the case of Dineshkumar Gulabchand Agrawal v. Commissioner of Incometax and another, [2004] 267 ITR 768 and of the Karnataka High Court rendered in Deputy Commissioner of Incometax v. Yellamma Dasappa Hospital, [2007] 290 ITR 353 (Karn).

8. The record reveals that the reason assigned by the Assessing Officer for rejecting the depreciation is that the assessee had stopped the manufacturing activity and therefore, the question of use of machinery does not arise. However, the CIT(A) reversed the findings of the Assessing Officer on the premise that individual items included in the block are not to be considered separately for the purposes of granting depreciation in light of the amended provisions. We do not find any legal infirmity in the aforesaid view adopted by the first appellate authority since the assessment order itself reveals that it is not the case of Assessing Officer that the assets were not put to use at all. Once the factory building is put to use, it is not possible to restrict the depreciation on the said building by stating that only a portion thereof has been put to use. Similarly, in relation to block of assets, it is not possible to segregate items falling within the block for the purposes of granting depreciation or restricting the claim thereof. Once it is found that the assets are used for business, it is not necessary that all the items falling within plant and machinery have to be simultaneously used for being entitled to depreciation.

9. In view of the above discussion, we hold that the Tribunal committed serious error in law in disallowing the depreciation. Thus, the question raised in these appeals are answered in the negative, i.e. in favour of the assessee and against the Revenue. The appeals stand disposed of accordingly. No order as to costs.

(K.S.JHAVERI, J.)

(G.R.UDHWANI, J.)

×

Similar Ripples

Questions

Court Allows Depreciation on Unused Plant & Machinery, Overturning Tax Tribunal's Decision

Write your CommentSimilar Posts

Generic

- Reportdata/2717.pdf