Court Rules Oil Wells as Plant, Eligible for Higher Depreciation Rate

Full News

Court Rules Oil Wells as Plant, Eligible for Higher Depreciation Rate

Court Rules Oil Wells as Plant, Eligible for Higher Depreciation Rate

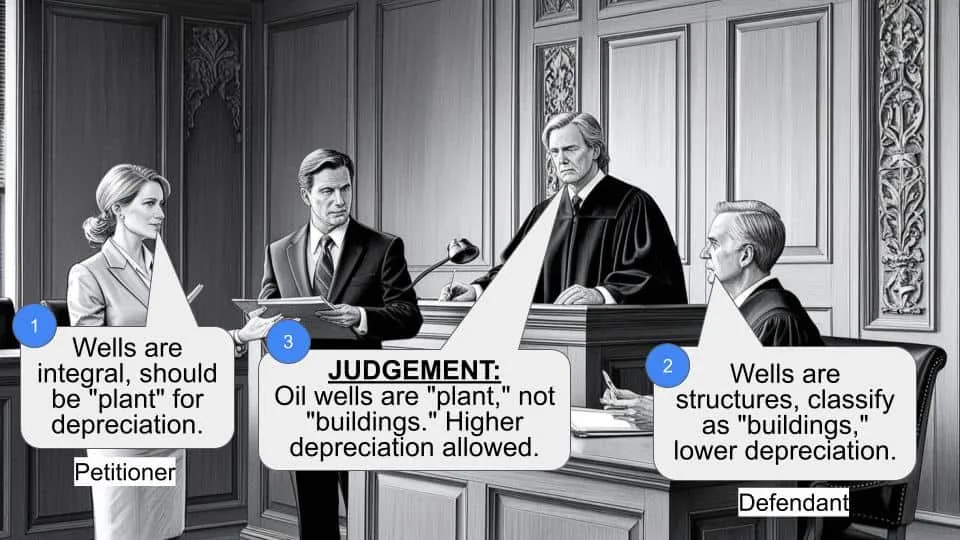

This case involves Niko Resources Ltd. (the assessee) challenging a decision by the Income Tax Appellate Tribunal regarding the classification of gas oil wells for depreciation purposes. The High Court ruled in favor of the assessee, holding that oil wells should be considered as "plant" rather than "buildings," thus eligible for a higher depreciation rate.

Get the full picture - access the original judgement of the court order here

Case Name:

Niko Resources Ltd. Vs Assistant Commissioner of Income Tax (High Court of Gujarat)

Tax Appeal No. 1193 of 2009

Date: 20th July 2016

Key Takeaways:

1. Oil wells can be classified as "plant" for income tax purposes.

2. The functional test is crucial in determining whether something qualifies as a plant.

3. This decision may have significant implications for companies in the oil and gas sector regarding their tax calculations.

Issue:

Whether gas oil wells should be classified as "plant" or "building" for the purpose of calculating depreciation under Section 32 (of Income Tax Act, 1961)?

Facts:

- Niko Resources Ltd. is engaged in oil and gas exploration.

- The company claimed depreciation on gas oil wells as "plant."

- The Income Tax Appellate Tribunal ruled that the wells should be treated as "buildings," allowing only 10% depreciation.

- The assessee appealed this decision to the High Court.

Arguments:

Assessee's Arguments:

- Oil wells are integral to the business and should be considered "plant."

- Previous court decisions have classified similar structures as "plant."

- The functional test should be applied to determine classification.

Department's Arguments:

- Wells are not machinery but structures, thus should be classified as "buildings."

- No machine is installed below ground in a gas well.

- The well is merely a passage to reach the oil/gas reservoir.

Key Legal Precedents:

1. Scientific Engg. House (P.) Ltd. v Commissioner of Income-tax [1986] 157 ITR 86 (SC)

2. Commissioner of Income-tax v. Dr. B. Venkata Rao [2000] 243 ITR 81 (SC)

3. Assistant Commissioner of Income-tax v. Victory Aqua Farm Ltd. [2015] 379 ITR 335 (SC)

4. Commissioner of Income-tax v. Oil India Ltd. [1992] 198 ITR 701 (Calcutta)

These cases established the importance of the functional test in determining whether an item qualifies as "plant" for tax purposes.

Judgement:

The High Court ruled in favor of the assessee, holding that:

1. The oil wells should be considered as "plant" rather than "buildings."

2. The reasoning adopted by the Tribunal was incorrect.

3. The view taken by the CIT (Appeals) was restored, and the Tribunal's findings were reversed.

FAQs:

1. Q: What is the significance of classifying oil wells as "plant" instead of "buildings"?

A: Classification as "plant" typically allows for a higher depreciation rate, which can lead to significant tax savings for oil and gas companies.

2. Q: What is the "functional test" mentioned in the judgment?

A: The functional test examines how an item is used in a business to determine if it qualifies as "plant." If it's an essential tool or apparatus for carrying out the business, it's more likely to be considered "plant."

3. Q: Does this judgment apply to all types of wells?

A: While the judgment specifically addresses oil and gas wells, its reasoning might be applied to similar structures in other industries. However, each case would need to be evaluated on its specific facts.

4. Q: How might this decision impact the oil and gas industry?

A: This decision could lead to significant tax savings for companies in the oil and gas sector, potentially affecting their financial planning and reporting.

5. Q: Can the tax department appeal this decision?

A: Yes, the department could potentially appeal this decision to the Supreme Court if they believe there are grounds to challenge the High Court's interpretation.

1. By way of this Appeal, the Appellant– assessee has challenged the judgment and order dated 19.03.2008 of the Income Tax Appellate Tribunal, Ahmedabad “C” Bench in ITA No.408/Ahd./2007 for the Assessment Year : 1998-1999 whereby the Tribunal reversed the findings of the CIT (Appeals) and confirmed the assessment order of the Assessing Officer.

2. While admitting the matter on 11.01.2010, the following substantial question of law was framed by the Court for consideration :-

“(i) Whether, in the facts and under the circumstances of the case the Income Tax Appellate Tribunal was right in law in treating the mineral oil wells as Buildings for the purpose of applying rate of depreciation under Section 32 (of Income Tax Act, 1961)?”

3. Learned Senior Counsel for the appellant – assessee Mr. S.N. Soparkar has submitted that the Tribunal has erred in restricting the alternate claim of depreciation made by the assessee without prejudice to its principal claim under Section 42 (of Income Tax Act, 1961). It is further submitted that the Tribunal has erred in restricting the claim of depreciation only @ 10% against 100% allowed by CIT(Appeals) by treating the oil wells as buildings. It is next contended that the Tribunal has erred in not appreciating that the mineral oil wells can never be equated with the buildings and therefore its action of applying the rate of depreciation of buildings to the mineral oil wells is illegal and cannot be sustained in law.

3.1. Learned Senior Counsel Mr. S.N. Soparkar has taken us to the orders of the Assessing Officer, CIT (Appeals) and the Tribunal and has contended that building a well forms a mandatory part for drilling of the oil and therefore, the same was constructed and this aspect has not been considered.

3.2. Learned Senior Counsel for the appellant has relied on the decision of the Hon'ble Supreme Court in the case of Scientific Engg. House (P.) Ltd. v Commissioner of Income-tax reported in [1986] 157 ITR 86 (SC) and more particularly on paragraphs 10, 11 and 12 which reads as under :-

“10. The next question is whether the acquisition of such a capital asset is depreciable asset or not? Under section 32 (of Income Tax Act, 1961) depreciation allowance is, subject to the provisions of section 34 (of Income Tax Act, 1961), permissible only in respect of certain assets specified therein, namely, buildings, machinery, plant and furniture owned by the assessee and used for the purpose of business while section 43(3) (of Income Tax Act, 1961) defines 'plant' in very wide terms saying "plant includes ships, vehicles, books, scientific apparatus and surgical equipments used for the purpose of the business". The question is whether technical know-how in the shape of drawings, designs, charts, plans, processing data and other literature falls within the definition of 'plant'.

11. The Counsel for the assessee urged that the expression 'plant' should be given a very wide meaning and reference was made to a number of decisions for the purpose of showing how quite a variety of articles, objects or things have been held to be 'plant'. But it is unnecessary to deal with all those cases and a reference to three or four decisions, in our view, would suffice. The classic definition of 'plant' was given by Lindley, L.J. in Yarmouth v. France, [1887] 19 Q.B.D. 647, a case in which it was decided that a cart-horse was plant within the meaning of section 1(1) of Employers' Liability Act, 1880. The relevant passage occurring at page 658 of the Report runs thus :-

"There is no definition of plant in the Act: but, in its ordinary sense, it includes whatever apparatus is used by a business man for carrying on his business - not his stock-in-trade which he buys or makes for sale; but all goods and chattels, fixed or movable, live or dead, which he keeps for permanent employment in his business”

In other words, plant would include any article or object fixed or movable, live or dead, used by businessman for carrying on his business and it is not necessarily confined to an apparatus which is used for mechanical operations or processes or is employed in mechanical or industrial business. In order to qualify as plant the article must have some degree of durability, as for instance, in Hinton v. Maden & Ireland Ltd., 39 I.T.R. 357 (of Income Tax Rules, 1962), knives and lasts having an average life of three years used in manufacturing shoes were held to be plant. In C.I.T. Andhra Pradesh v. Taj Mahal Hotel, 82 I.T.R. 44 (of Income Tax Rules, 1962), the respondent, which ran a hotel installed sanitary and pipeline fittings in one of its branches in respect whereof it claimed development rebate and the question was whether the sanitary and pipe- line fittings installed fell within the definition of plant given in sec. 10(5) of the 1922 Act which was similar to the definition given in Sec. 43(3) (of Income Tax Act, 1961) and this Court after approving the definition of plant given by Lindley L.J. in Yarmouth v. France as expounded in Jarrold v. John Good and sons Limited, 1962, 40 T.C. 681 C.A. , held that sanitary and pipe-line fittings fell within the definition of plant.

12. In Inland Revenue Commissioner v. Barly Curle & Co. Ltd., 76 I.T.R. 62 (of Income Tax Rules, 1962), the House of Lords held that a dry dock since it fulfilled the function of a plant must be held to be a plant. Lord Reid considered the part which a dry dock played in the assessee company's operations and observed :

“It seems to me that every part of this dry dock plays an essential part....The whole of the dock is I think, the means by which, or plant with which, the operation is performed.”

Lord Guest indicated a functional test in these words :

In order to decide whether a particular subject is an 'apparatus' it seems obvious that an enquiry has to be made as to what operation it performs. The functional test is, therefore, essential at any rate as a preliminary...”-

In other words the test would be: Does the article fulfil the function of a plant in the assessee's trading activity Is it a tool of his trade with which he carries on his business? If the answer is in the affirmative it will be a plant.”

3.3. Reliance is also placed on the decision of the Hon'ble Supreme Court in the case of Commissioner of Income-tax v. Dr. B. Venkata Rao reported in [2000] 243 ITR 81 (SC) and paragraphs 2 and 3 of this decision reads as under :-

“2. The assessee is a medical practitioner. The assessee is a medical practitioner. He runs a nursing home. In respect of the building in which the nursing home is run, the assessee claimed, for the asst. yr. 1983-84, that it was a "plant". His contention was rejected by the ITO and by the CIT(A). The Tribunal found to the contrary.

Applying the functional test, it held that the nursing home was a plant. The High Court affirmed that view. It said that a building used as a nursing home is not comparable with an ordinary building having regard to the number of persons using it, the manner of its use and the purpose for which it is used. The building was used not only to house patients and nurse them, but also to treat them, for which various kinds of equipment and instruments were installed.

3. The most apposite decision in this context is that delivered by the Allahabad High Court in S.K. Tulsi & Sons vs. CIT (1990) 90 CTR (All) 99 : (1991) 187 ITR 685 (All) : TC 29R.638. Reference was made to an earlier judgment, where also the functional test approved by this Court in several decisions was applied. It was held that if it was found that the building or structure constituted an apparatus or a tool of the taxpayer by means of which business activities were carried on, it amounted to a "plant"; but where the structure played no part in the carrying on of these activities but merely constituted a place wherein they were carried on, the building could not be regarded as a plant.”

3.4. In addition, learned Senior Counsel for the appellant has referred to the decision of the Hon'ble Supreme Court in the case of Assistant Commissioner of Income-tax v. Victory Aqua Farm Ltd. reported in [2015] 379 ITR 335 (SC) wherein Paragraphs 4 and 6 are reproduced hereunder :-

4. It is not in dispute that if these ponds are ‘plants’, then they are eligible for depreciation at the rates applicable to plant and machinery and case would be covered by the provisions of Section 32 (of Income Tax Act, 1961). It is not even necessary to deal with this aspect in detail with reference to the various judgments, inasmuch as judgment of this Court in Commissioner of Income Tax, Karnataka v. Karnataka Power Corporation [2002(9) SCC 571] clinches the issue. Therein the Court has taken into consideration the earlier judgments on which some reliance was placed by the learned counsel for the Revenue and are suitably dealt with. The relevant portion of the said judgment reads as under:

“5. It was the case of the assessee that it was entitled to investment allowance as applicable to a plant in respect of its power generating station building. In a note filed before the Commissioner (Appeals) it stated that it had included for the purpose the value of its Potential Transformer Foundation. Cable Duct System, Outdoor Yard Structures and Tail Race Channel. It explained that the process of generation started from letting in water from the reservoir into the pen-stocks and ducts which were the water conductor system into the turbines. Once electricity had been produced by generation, it had to be conducted, as it was not possible to store the same, and the process of generation continued until the electricity was led to the transmission tower. The water that was used for rotation of the turbines had to be removed and this was done through the Tail Race Channel. For stepping up the electricity, transformers were used in the outdoor yard. The conduction of the electricity was through conductors held in ducts, called the Cable Duct System, which were specifically designed for the purpose. The case of the assessee, therefore, was that all these were part of the special engineering works that were an essential part of a generating plant and, therefore, it was entitled to have the same treated as a plant for the purposes of investment allowance. The Commissioner accepted the correctness of the assessee’s case. He held that it was clear that the generating station buildings had to be treated as a plant for the purposes of investment allowance. These buildings could not be separated from the machinery and the machinery could not be worked without such special construction. He, therefore, allowed investment, allowance on the generating station, building, as claimed. The Tribunal affirmed this finding, as, as, indeed did the High Court.

6. We, therefore, have before us a finding of fact recorded by the fact finding authority that the generating station building is an integral part of the assessee’s generating system.

7. Our attention has been drawn by learned Counsel for the Revenue to the judgment of this Court in Commissioner of Income Tax v. Anand Theatres 224 I.T.R. 192 (of Income Tax Rules, 1962). He submits that, in that judgment, this Court has held that, except in exceptional cases, the building in which the plant is situated must be distinguished from the plant and that, therefore, the assessee’s generating station building was not to be treated as a plant for the purposes of investment allowance.

8. It is difficult to read the judgment in the case of Anand Theatres so broadly. The question before the court was whether a building that was used as a hotel or a cinema theatre could be given depreciation on the basis that it was a “plant” and it was in relation to that question that the court considered a host of authorities of this country and England and came to the conclusion that a building which was used as a hotel or cinema theatre could not be given depreciation on the basis that it was a plant. We must add that the Court said, “To differentiate a building for grant of additional depreciation by holding it to be a plant in one case where a building is specially designed and constructed with some special features to attract the customers and the building not so constructed but used for the same purpose, namely, as a hotel or theatre would be unreasonable.”

This observation is, in our view, limited to buildings that are used for the purposes of hotels or cinema theatres and will not always apply otherwise. The question, basically, is a question of fact, and where it is found as a fact that a building has been so planned and constructed as to serve an assessee’s special technical requirements, it will qualify to be treated as a plant for the purposes of investment allowance.

9. In the instant case, there is a finding by the fact finding authority that the assessee’s generating station building is so constructed as to be an integral part of its generating system. It must, therefore, be held that it is a “plant” and entitled to investment allowance accordingly. The third question is answered in the affirmative and in favour of the assessee.”

6. We find that the judgment dated 14.10.2004 rightly rests this case on ‘functional test’ and since the ponds were specially designed for rearing/breeding of the prawns, they have to be treated as tools of the business of the assessee and the depreciation was admissible on these ponds. We, thus, decide the question in favour of the assessee and as a consequence, appeals of the Revenue are dismissed and that of the assessee are allowed.”

3.5. Further, reliance is placed on the decision of the High Court of Calcutta in the case of Commissioner of Income- tax v. Oil India Ltd. reported in [1992] 198 ITR 701 (Calcutta) and relevant part of the said decision is reproduced as under :-

“Question No. 6 is whether the Tribunal was justified in holding that the oil wells constituted plant for the purpose of the allowance of development rebate. The Tribunal has found that the assessee claimed drilling expenditure of Rs. 2,72,94,678 and claimed development rebate at 25 per cent. of the said amount at Rs. 68,83,670. The Income- tax Officer did not allow the claim on the ground that the whole of the expenditure claimed by the assessee has been allowed to it. The Commissioner of Income-tax (Appeals), relying on several decisions, stated that the well was not plant and, therefore, the assessee was not entitled for development rebate.

The Tribunal pointed out that oil well is an apparatus used by the assessee for the purpose of deriving income from crude oil after drilling the well. Under the circumstances, the well is a plant of the assessee used for its business of exploration of crude oil.

In fact, the assessee relied upon the Circular of the Department being No. 582-25/605 J. M. dated January 23, 1926. The said circular categorically lays down that wells and pipes are plant.

The Supreme Court decision in the case of Scientific Engineering House P. Ltd. v. CIT was relied upon by Dr. Pal.

The Supreme Court, in the said judgment, has quoted with approval from the decision reported in Yarmouth v. France [1887J 19 QBD 647 that " there is no definition of plant in the Act : but in its ordinary sense, it includes whatever apparatus is used by a businessman for carrying on his business,--not his stock-in-trade which he buys or makes for sale ; but all goods and chattels, fixed or movable, live or dead, which be keeps for permanent employment in his business ".

The same view has been taken by the House of Lords in Hinton v. Maden and Ireland Ltd. [1959] 38 TC 391, 417 and 424.

In Income-tax Reference No. 260 of 1987 (Tribeni Tissues Ltd. v. CIT , the Division Bench of this court presided over by Ajit Kumar Sengupta J., held that tube-well is a plant entitled to investment allowance. It has been further decided that a well dug for the purpose of carrying on business is a plant both for the purposes of depreciation and for development rebate. In this connection, we take note of the following decisions :

(1) CJT v. Warner Hindustan Ltd. .

(2) CIT v. Warner Hindustan Ltd.

. In the case of CIT v. Hindusthan Motors Ltd. , the expenditure was allowed under Clause 12(ii) of the second supplemental agreement and not as a revenue expenditure.

Development rebate is allowable under Section 33 (of Income Tax Act, 1961) over and above the recoupment of the total cost of machinery by way of depreciation allowance. The allowance under Section 33 (of Income Tax Act, 1961) is obviously given to provide an incentive for industrial expansion. It has no connection with depreciation allowance, which is an yearly feature. Accordingly, question No. 6 is answered in the affirmative and in favour of the assessee.”

It is also pointed out that as per the Depreciation Table of the Income Tax Rules, 2016, item No.(c), i.e. oil wells are not covered in clauses (a) and (b) of category (xii) – Mineral oil concerns.

4. Learned Counsel for the respondent - Department Mr. Nitin K. Mehta has drawn the attention of this Court to the Assessment Order of the Assessing Officer and the relevant paragraph of the order is reproduced herein below :-

“(5.1) It is essential to examine the alternative claim of the assessee that it is eligible to 100% depreciation on the entire items of expenses claimed u/s. 42 (of Income Tax Act, 1961). Reliance was placed on entry 111(3) (ix)(b) of the appendix 1 of the Income Tax Rules 1962.

The said entry of Income Tax rules reads as under :

111. MACHINERY AND PLANT (ix) Mineral oil concerns :

(b) Plant used in field | operations (below ground), | but not including kerbside | 100 pumps including underground | tanks and fittings used in | filed operations (distribution)| by mineral oil concerns | A perusal of above would reveal that entry (ix)(b) deals with plant used in filed operation (distribution) by mineral oil concern. Thus, to qualify for this entry following conditions have to be satisfied.

◦ It should be a plant.

◦ It is used in field operation (below ground).

◦ It belongs to a mineral oil concern.

It is necessary to understand assessee's operation before deciding the depreciation rates for the wells used by the assessee. It is necessary to understand the process of drilling and exploration activities for a gas well. Before drilling a well, geographical and geophysical surveys are conducted and probable site for well is decided. At the time of drilling the well, drilling fluid or drilling mud is constantly circulated round the well board. When the drilling is completed, casing pipe is lowered in the well to ensure the safe control of production, to prevent water entering in well bore and to keep rock formations from 'sloughing' into wellbore. Valves, chokes and fittings controlling the explored gas are installed at wellhead, which is known as 'Christmas tree'.

Stated briefly, there is a well, dug after drilling and there is a casing lowered in the well. Assessee has incurred expenses on drilling, cost of casing and cost of lowering the casing. The assessee has claimed 100% depreciation on all costs.

(5.2) Now, the question is whether a well constitutes a plant? Is there any plant below ground?

No machine is installed below ground in the case of a gas well. Gas flows to the wellbore under its own pressure. As a result, gas well is equipped only with chokes and valves to control the flow through the well head into a pipeline. Below the ground only casing – tubular steel pipe connected by threads and couplings – lines the total length of the wellbore to ensure the safe control of production, to prevent water entering in wellbore and to keep rock formations from 'sloughing' into wellbore.”

4.1. Learned Counsel for the respondent has also relied on the findings of the Tribunal and relevant part of the same are as under :-

“57. Applying these functional tests, a well may be the producing apparatus with which the business of oil and gas extraction business is carried on and hence could be a 'plant' within the meaning of Section 43(3) (of Income Tax Act, 1961). This view is also supported by decisions where a well and a tube well have been held to be plant. These are i) CIT vs. Oil India 198 ITR 701 (Cal) holding the oil well as a plant, it being an apparatus used by the assessee for the purpose of deriving income from crude oil after drilling the well; ii) Siemens India Limited vs. CIT 217 ITR 622 (Bom) holding a tube well in connection with setting up of a electroplating plant shop, a plant for a concern engaged in the manufacture of equipment for the generation and distribution of electricity, x-ray equipment and other electrical equipment; iii) CIT vs. Hindustan Motors Limited 170 ITR 431 (Cal) holding that tube well used by the assessee for drawing water to be used I production constituted a plant for an assessee manufacturing automobile ancillaries used in its own business of manufacturing cars; iv) CIT vs. Taj Mahal Hotel 82 ITR 44 (SC) holding pipelines and sanitary fittings to be a plant for a hotel because of a wide definition u/s 43(3) (of Income Tax Act, 1961) and based on the functional test; v) the decision of Calcutta High Court in the case of Tribeni Tissues Ltd. v. CIT (Cal) 190 ITR 487, holding that tube well is an apparatus with equipment necessary for drawing water from subterranean sources where water is used for production was a plant; and vi) CIT v. Warner Hindustan Ltd. 117 ITR 15 (AP) and 117 ITR 68 (AP), wherein a well even in a pharmaceutical factory was held to be in the nature of a plant and not a building. The decision of Gujarat High Court in the case of Shree Digvijay Woolen Mills Ltd. Vs. CIT, 204 ITR 398 (Guj) relied upon the ld. CIT-DR was not whether tube well is a plant but it held that the expenditure on tube well is a capital expenditure. It held that even if it did not result in the creation of an asset, it would not cease to be an expenditure of the nature of capital.

65. The assessee dug the well and put steel pipes therein to reach the reservoirs of oil and natural gas. It is thus a passage created by the assessee to reach reservoir. The well is to protect, cover and put a structure around the space drilled from which mineral oil or gas is obtained. The cost is of digging and laying steel pipeline and is the expenditure claimed as cost of the plant but the cost of apparatus which is used to extract oil and natural gas is separately booked under the head machinery. This also gives an impression that the gas oil wells are not plant. It is but a setting through which the assessee extracted oil and gases, and therefore a part of the building within the extended meaning of the term building given in the Appendix 1 to IT Rules. The depreciation would be allowed thereon %10 a building.”

3. Facts and circumstances being similar we holding that the oil well is not a plant but a building by respectfully following that order in this year as well. We accordingly reverse the order of CIT(A) and restore that of the AO on this issue.”

4.2. Learned Counsel for the respondent has further relied on the decision of the Delhi High Court in the case of R.C. Chemical Industries v. Commissioner of Income-tax, New Delhi reported in [1982] 134 ITR 330 wherein the question was whether that building was a “plant” and qualified for development rebate under Section of the Act. The Court held that the building could not qualify as a “plant” for the purpose of development rebate.

4.3. Further reference is made to the decision of the Gauhati High Court int eh case of Nowrangroy Metal Pvt. Ltd. v. Joint Commissioner of Income-tax (Assessment) reported in [2003] 262 ITR 231 wherein the facts of the case, it was held that the building in question was plant and therefore the assessee was entitled to the higher rate of depreciation.

5. We have heard learned Counsel appearing for the respective parties. In light of the decision of the Hon'ble Supreme Court in the case of Scientific Engg. House (P.) Ltd. v Commissioner of Income-tax (supra), we are of the view that the reasoning which was adopted by the Tribunal holding that the well would not form a part of the plant and machinery for drilling of oil is not correct. In that view of the matter, the view taken by CIT (Appeals) is restored and the findings of the Tribunal are reversed. Hence, the issue raised in this Appeal is answered in favour of the assessee and against the Department. The Appeal stands disposed of accordingly.

Sd/-

(K.S. JHAVERI, J.)

Sd/-

(G.R. UDHWANI, J.)

×