Court Allows R&D Approval Despite Late Filing, Citing Technical Glitches

Full News

Court Allows R&D Approval Despite Late Filing, Citing Technical Glitches

Court Allows R&D Approval Despite Late Filing, Citing Technical Glitches

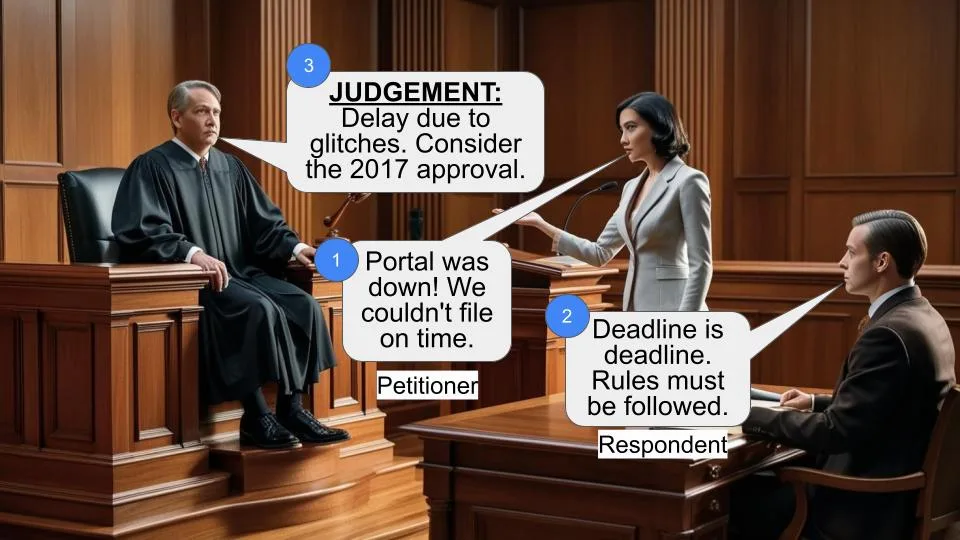

This case involves Hawkins Cookers Ltd. (the petitioner) challenging an order by the Department of Scientific and Industrial Research (DSIR, the respondent) that approved their Research and Development facility under Section 35(2AB) (of Income Tax Act, 1961) only from 01.04.2018, instead of 01.04.2017 as requested. The court ultimately sided with the petitioner, allowing them to seek approval for the earlier date despite the late filing of their application.

Get the full picture - access the original judgement of the court order here

Case Name:

Hawkins Cookers Ltd. vs Union of India (High Court of Delhi)

W.P.(C) 9586/2019

Date: 27th February 2020

Key Takeaways:

1. Technical issues with government portals can be valid grounds for late submissions.

2. Courts may prioritize substantive justice over procedural technicalities.

3. Government agencies should consider condonation of delay in cases involving technical glitches.

4. The rights of parties shouldn't be compromised due to inefficient software systems.

Issue:

Should the petitioner's Research and Development facility be approved under Section 35(2AB) (of Income Tax Act, 1961) from 01.04.2017, despite submitting Form 3CK after the deadline due to technical issues with the online portal?

Facts:

1. The petitioner, Hawkins Cookers Ltd., sought approval for their R&D facility under Section 35(2AB) (of Income Tax Act, 1961) from 01.04.2017.

2. The respondent, DSIR, approved the facility only from 01.04.2018.

3. The reason for not approving from 01.04.2017 was that the petitioner submitted Form 3CK on 27.04.2018, after the 31.03.2018 deadline.

4. The petitioner claimed that the online portal for submission was not functioning from 08.03.2018 to at least 25.04.2018.

5. The petitioner's Vice-Chairman & CEO, required to sign the physical form, was out of India from 08.03.2018 till 25.04.2018.

6. The respondent did not specifically deny the allegation about the non-functioning portal in their counter-affidavit.

Arguments:

Petitioner:

1. The delay in filing Form 3CK was not intentional due to the non-functional online portal.

2. Physical submission was delayed because the required signatory was out of the country.

3. The delay of 27 days should have been condoned given the circumstances.

Respondent:

1. As per Guidelines, the application (Form 3CK) should have been filed by 31.03.2018 for approval from 01.04.2017.

2. Physical copies of the application forms were being accepted.

Key Legal Precedents:

1. Vision Distribution Pvt. Ltd. vs. Commissioner, State Goods & Services Tax & Ors. (WP(C) No.8317/2019): The court observed that "The rights of the parties cannot be subjugated to the poor and inefficient software systems adopted by the Respondents."

2. Apollo Tyres Ltd., Kochi vs. Union of India (WP(C) No.13338/2009): This judgment was cited by the respondent to support their stance on the application deadline.

Judgement:

1. The court sided with the petitioner, allowing them to seek approval from 01.04.2017.

2. The respondent was directed to consider the petitioner's request to condone the delay and grant approval for the financial year 2017-18.

3. The petitioner was allowed to make a representation to the respondent, which must be considered within four weeks of receipt.

4. The court emphasized that the mere absence of a provision for condoning delay should not be grounds for rejecting the representation.

FAQs:

1. Q: Why did the court side with the petitioner despite the late submission?

A: The court considered the technical issues with the online portal and the absence of a specific denial from the respondent about these issues.

2. Q: What implications does this judgment have for future cases?

A: It suggests that courts may be willing to consider technical difficulties as valid reasons for late submissions, especially when government portals are involved.

3. Q: Does this mean all late submissions will be accepted if there are technical issues?

A: Not necessarily. Each case would likely be judged on its own merits, considering the specific circumstances and evidence provided.

4. Q: What should companies do if they face similar technical issues with government portals?

A: They should document the issues, attempt to submit through alternative means if possible, and be prepared to explain the situation if challenged.

5. Q: How might this judgment impact government agencies' policies?

A: It may encourage agencies to improve their online systems and to be more flexible in considering reasons for delays, especially those related to technical issues.

1. This petition has been filed by the petitioner challenging the order dated 16.04.2019 issued by the respondent whereby the Research and Development facility of the petitioner, for the purpose of Section 35(2AB) (of Income Tax Act, 1961), 1961, has been approved only with effect from 01.04.2018.

2. It is the claim of the petitioner that the same should have been approved with effect from 01.04.2017. 3. The ground for not approving the facility of the petitioner with effect from 01.04.2017 is that the petitioner had submitted Form 3CK only on 27.04.2018.

4. Relying upon Clause 5(i) of the Guidelines for approval in Form 3CM under Section 35(2AB) (of Income Tax Act, 1961), 1961, the respondent contends that the application seeking approval in Form 3CK should have been filed on or before 31.03.2018 for the approval to be granted from 01.04.2017. Reliance in this regard is made on the judgment dated 20.04.2010 passed by the Division Bench of this Court in WP(C) No.13338/2009, titled Apollo Tyres Ltd., Kochi vs. Union of India.

5. On the other hand, the learned counsel for the petitioner submits that Clause 6 of the Guidelines requires the application (Form 3CK) to be submitted online. The petitioner further asserts that the online portal of the respondent was not functioning between the period 08.03.2018 to at least 25.04.2018, when the application was submitted by the petitioner in the physical form. The said submission is made in Ground XI and XII of the petition, which are reproduced here in under:

“XI. Because the delay in filing Form 3CK was not intentional, for online portal of DSIR was not functional and during the period 8.3.2018 to 25.4.2018, Petitioner’s Vice-Chairman & Chief Executive Officer was out of India on a business promotion trip-to promote exports. Affidavit of Mr.Jayanta Kumar Chakrabarti, Senior Vice President, Research & Development, of the Petitioner is annexed herewith and marked as Annexure P-10.XII. Because Form 3CK could not be filed online as stipulated in the guidelines of DSIR because of technical glitch in DSIR portal. After repeated attempts to file online and not able to do so, hard copy was filed on April 27, 2018. Hard copy of Form 3CK was filed immediately on return of Vice Chairman & CEO from a business trip abroad as the said Form 3CK had to be signed by the Head of the organisation as stipulated in guidelines of DSIR. In the circumstances, DSIR ought to have condoned the delay of 27 days.”

6. In reply to the above averments, the respondent in its counter affidavit has not specifically denied the allegation of the petitioner with respect to the portal of the respondent not working, however, has submitted that even the physical copies of the application forms were being accepted by the respondent.

7. The petitioner in answer asserts that in accordance with Clause 8 of the Guidelines, Form 3CK, in the physical form, could have been submitted only under the signatures of the Managing Director. As the Managing Director of the petitioner was not available in India from 08.03.2018 till 25.04.2018, the Form 3CK could be submitted with the respondent in the physical form only on 27.04.2018. 8. I have considered the submissions made by the learned counsels for the parties.

9. As noted hereinabove, the submission of the petitioner that the portal of the respondent was not working from 08.03.2018, has not been specifically denied by the respondent in its counter affidavit. This Court in its judgment dated 12.12.2019 passed in WP(C) No.8317/2019, titled Vision Distribution Pvt. Ltd. vs. Commissioner, State Goods & Services Tax & Ors., though in relation to the Goods and Service Tax regime, has observed as under:

“The rights of the parties cannot be subjugated to the poor and inefficient software systems adopted by the Respondents. The software systems adopted by the Respondents have to be in tune with the law, and not vice verse. The system limitations cannot be a justification to deny the relief, to which the Petitioner is legally entitled. We, therefore, reject the hyper technical objections sought to be raised by the Respondents – to the effect, that no refund can be granted, because the system did not reflect any credit lying in the ITC ledger of the Petitioner for the months of July and August, 2017. If that is so, it is entirely the Respondents making. In fact, to permit the Respondents to get away with such an argument would be putting premium on inefficiency. We therefore, reject the submission.”

10. Clause 6 of the Guidelines prescribes that the application that is Form 3CK needs to be submitted online. It seems that only because the portal of the respondent was not working, the respondents decided to accept the application even in physical form, however, for reasons mentioned hereinabove, the petitioner could not submit the application in physical form in time. At the same time, the petitioner cannot be denied the grant of the approval under Section 35(2AB) (of Income Tax Act, 1961) on such hyper technical ground.

11. In view of the above, on the petitioner satisfying the respondent of the reasons for non-submission of Form 3CK in physical form with the respondent on or before 31.03.2018, the respondent shall consider the request of the petitioner to condone the delay and grant approval to the petitioner under Section 35(2AB) (of Income Tax Act, 1961) for the financial year 2017-18. The petitioner in this regard shall be entitled to make a representation to the respondent, which shall be considered by the respondent within four weeks of receipt of such representation. Mere absence of a provision for condoning such delay, shall not be a ground for rejecting the representation of the petitioner inasmuch as it is not denied that the portal of the respondent was not functioning from 08.03.2018.

12. The petition is disposed of with the above directions.

×

Questions

Court Allows R&D Approval Despite Late Filing, Citing Technical Glitches

Write your CommentSimilar Posts

Generic

- Reportdata/6277.pdf