Court allows TDS claim despite technical error in PAN, dismisses revenue's appe…

Full News

Court allows TDS claim despite technical error in PAN, dismisses revenue's appeal.

Court allows TDS claim despite technical error in PAN, dismisses revenue's appeal.

The case involves a dispute over a TDS claim of ₹1,20,73,097 by the assessee, M/s Relcom, which was initially denied by the revenue on technical grounds. The court ruled in favor of the assessee, allowing the TDS claim despite the error in the PAN mentioned in the TDS certificate, as the benefit was not availed by the sister company, M/s REPL.

Get the full picture - access the original judgement of the court order here.

Case Name:

Commissioner of Income Tax vs. Relcom (High Court of Delhi)

ITA 26/2015

Key Takeaways

- The court allowed the TDS claim of ₹1,20,73,097 by the assessee, M/s Relcom, despite a technical error in the PAN mentioned in the TDS certificate.

- The court emphasized that procedural technicalities should not hamper the cause of justice.

- The decision was influenced by the fact that the sister company, M/s REPL, did not object to the TDS claim and had not availed the benefit.

- The court referenced Rule 37BA (of Income Tax Rules, 1962), and the case of CIT v. Bhooratnam to support its decision.

Issue

Whether the assessee, M/s Relcom, was entitled to the TDS claim of ₹1,20,73,097 without offering the corresponding income of ₹19,08,20,903 to taxation, given the error in the PAN mentioned in the TDS certificate.

Facts

- The assessee, M/s Relcom, derived income from the business of erection, commissioning, and installation of towers.

- The assessee filed its returns for the relevant assessment year, declaring total receipts of ₹6,20,99,368 but claimed TDS of ₹1,20,73,097.

- The discrepancy arose because a vendor mistakenly mentioned the assessee's PAN in the TDS certificate instead of the sister company, M/s REPL.

- The Assessing Officer (AO) rejected the TDS claim based on Section 199 (of Income Tax Act, 1961), stating that the TDS credit should be allowed to the person from whose income the deduction was made.

- The CIT(A) and ITAT allowed the TDS claim, noting that the benefit was not availed by M/s REPL and both companies belonged to the same group.

Arguments

- Revenue's Argument:

The revenue argued that the TDS claim should be disallowed as the deduction was made in respect of M/s REPL's income, not the assessee's. They relied on Section 199 (of Income Tax Act, 1961).

- Assessee's Argument:

The assessee argued that the benefit of the TDS claim was not availed by M/s REPL and that the error in the PAN should not result in the denial of the TDS claim.

Key Legal Precedents

- CIT v. Bhooratnam (2013) 357 ITR 196 (AP):

The court held that credit for TDS certificates cannot be denied to the assessee while assessing the contract receipts mentioned in the certificates as income of the assessee.

- Sardar Amarjit Singh Kalra v. Pramod Gupta, (2003) 3 SCC 272:

The court emphasized that procedure is the handmaid of justice and should not be used to hamper the cause of justice.

Judgement

The court dismissed the revenue's appeal and allowed the TDS claim of ₹1,20,73,097 by the assessee. The court reasoned that the procedural error in the PAN should not result in the denial of the TDS claim, especially since the benefit was not availed by the sister company, M/s REPL. The court emphasized that procedural technicalities should not hamper the cause of justice.

FAQs

Q1: Why was the TDS claim initially denied?

A1: The TDS claim was initially denied because the Assessing Officer (AO) argued that the TDS credit should be allowed to the person from whose income the deduction was made, and in this case, the deduction was made in respect of M/s REPL's income, not the assessee's.

Q2: What was the court's reasoning for allowing the TDS claim?

A2: The court allowed the TDS claim because the benefit was not availed by M/s REPL, and both companies belonged to the same group. The court emphasized that procedural technicalities should not hamper the cause of justice.

Q3: What legal precedents did the court rely on?

A3: The court relied on the case of CIT v. Bhooratnam (2013) 357 ITR 196 (AP) and the principle from Sardar Amarjit Singh Kalra v. Pramod Gupta, (2003) 3 SCC 272, which states that procedure is the handmaid of justice.

Q4: What is the significance of Rule 37BA (of Income Tax Rules, 1962), in this case?

A4: Rule 37BA (of Income Tax Rules, 1962) envisions the grant of TDS credit to entities other than the deductee. Although not directly applicable, it was referenced to demonstrate that TDS credit is not always given to the deductee.

Q5: What does this decision mean for the parties involved?

A5: The decision means that the assessee, M/s Relcom, is entitled to the TDS claim of ₹1,20,73,097, and the revenue's appeal is dismissed. This sets a precedent that procedural errors should not result in the denial of legitimate claims.

1. The revenue has filed the present appeal against the impugned order dated 15.07.2014 passed by the Income Tax Appellate Tribunal (hereinafter referred to as, “ITAT”) in ITA No.5979/DEL/2012, relating to the Assessment Year 2009-10. The question of law urged by the revenue in the instant appeal is:

“Whether in view of Section 199 (of Income Tax Act, 1961), the assessee was entitled to the TDS without offering the corresponding income i.e. total receipts of Rs.19,08,20,903/-to taxation by declaring it as total income?”

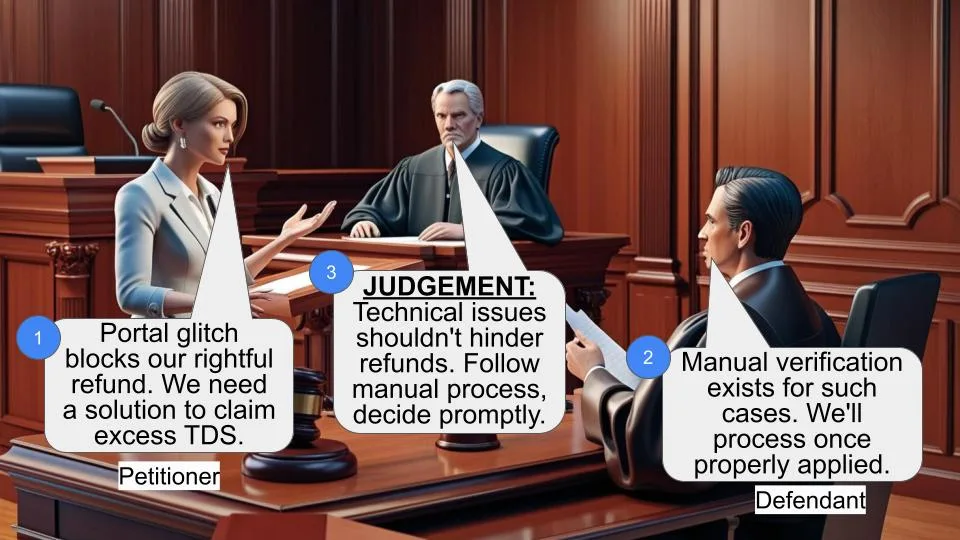

2. The facts involved in the present appeal are that during the year under consideration, the respondent (hereinafter referred to as, “the assessee”) derived income from the business of erection, commissioning and installation of towers on contract basis. It filed its returns for the relevant assessment year on 29.03.2010 and the returns were processed under Section 143(1) (of Income Tax Act, 1961) (hereafter referred to as, “the Act”).The Assessing Officer (AO) noticed that as per Form 26AS statement, though the total receipts declared by the assessee was 6,20,99,368/- (as opposed to 19,08,20,903/-), the TDS claimed was 1,20,73,097/-. The assessee's explanation for the discrepancy was that a vendor had billed M/s Relcom Engineering Pvt. Ltd. (“REPL”), its sister company, for the work but had mistakenly mentioned its (assessee’s) PAN in the TDS certificate, thus inadvertently crediting its TDS account in the 26AS statement, which is PAN based.

3. The assessee had claimed credit of all TDS certificates, including that related to M/s REPL but the income of this certificate was not reflected in the Profit and Loss Account. The total TDS claim made by the assessee was 1,20,73,097/- against a total of `19,08,20,903/- received. The assessee stated that the benefit of the TDS certificate mistakenly issued in its PAN name has not been availed by M/s REPL. The Assessing Officer (AO) rejected this claim relying on Section 199 (of Income Tax Act, 1961) and held that the TDS credit should be allowed to the person from whose income the deduction was made. Therefore, according to the AO, the assessee, instead of claiming the credit of the TDS which did not belong to it, should have approached the vendors for correction of their record. The AO held that since out of the total receipts of 19,08,20,903/-, the assessee received only 6,20,99,368/- (and the rest of the amount was received by Ms/ REPL), the TDS could be claimed only against the said amount of 6,20,99,368/-.

4. The assessee appealed against the AO’s order before the Commissioner of Income Tax (Appeals) (hereinafter referred to as, CIT(A)) who, by its order dated 20.09.2012, allowed the TDS claim. The CIT(A) noted that the assessee had categorically stated that the benefit of TDS claimed by it had not been availed by M/s REPL. Thus, the CIT(A) allowed assessee’s claim, on the ground that since the assessee had already paid the due taxes in M/s REPL (both companies being a part of the same group), it would be a travesty of justice to not allow the benefit of TDS to the assessee. The observations of CIT(A) are reproduced below:

“4.2 I have carefully considered the submissions made by the appellant and the assessment order framed by the AO and I am of the considered opinion that there is no technicality involved in the issue and it is purely a matter of applying little bit of common sense. It is clear from the narrations in the preceding paragraphs that there is an apparent mistake on the part of the vendor who has billed M/s. REPL for the work, but has mistakenly mentioned the PAN of M/s. Relcom in the TDS certificate. Thus, the credit of TDS has gone in the account of M/s. Relcom in the 26AS statement, which is PAN based. The appellant found it cumbersome to get fresh corrected certificates from the vendor and to approach the TDS division of the department for necessary rectification in the 26AS statement. Instead, the group decided that both the concerns belong to the same group and it would be easier to claim refund in M/s. Relcom and pay the due taxes in M/s. REPL. This is exactly what has transpired. Since, the appellant has already paid the due taxes in M/s. REPL, it would be a travesty of justice to not allow the benefit of TDS in M/s. Relcom. Therefore, the AO is directed to allow the benefit of TDS claim of the appellant as per the TDS certificates submitted by it...”

The ITAT, by its impugned order dated 15.07.2014, dismissed the revenue’s appeal against the order of the CIT(A).

5. The revenue in the present appeal has urged that the CIT(A) and the ITAT could not have allowed the entire TDS amount of ` 1,20,73,097/- claimed by the assessee as the deduction was not made in respect of the assessee’s income and it was, instead, made in respect of M/s REPL’s income. In support of this contention, the revenue relies on the provisions of Section 199 (of Income Tax Act, 1961). The revenue also contended that in the absence of the assessee offering the corresponding income, i.e. total receipts of 19,08,20,903/- for taxation by declaring total income, the assessee’s TDS claim could not have been allowed. Thus, the revenue submits, the defective TDS amount of 93,72,097/- should be disallowed and the only legitimate claim is that of 27,01,000/- against the declared total receipts of 6,20,99,368/-.

6. Having heard the submissions made on behalf of the revenue and after a perusal the orders passed by the CIT(A) and the ITAT, we are of opinion that the said orders do not call for any interference and were warranted and justified in the facts and circumstances of the case. Before we proceed to elaborate on our reasons for the same, a perusal of Section 199 (of Income Tax Act, 1961) is necessary. Section 199 (of Income Tax Act, 1961) reads as follows: “199. Credit for tax deducted.

(1) Any deduction made in accordance with the foregoing provisions of this Chapter and paid to the Central Government shall be treated as a payment of tax on behalf of the person from whose income the deduction was made, or of the owner of the security, or of the depositor or of the owner of property or of the unit-holder, or of the shareholder, as the case may be.

(2) Any sum referred to in sub-section (1A) of section 192 (of Income Tax Act, 1961) and paid to the Central Government shall be treated as the tax paid on behalf of the person in respect of whose income such payment of tax has been made.

(3) The Board may, for the purposes of giving credit in respect of tax deducted or tax paid in terms of the provisions of this Chapter, make such rules as may be necessary, including the rules for the purposes of giving credit to a person other than those referred to in sub-section (1) and sub-section (2) and also the assessment year for which such credit may be given.”

7. The revenue relies on the phrase “shall be treated as a payment of tax on behalf of the person from whose income the deduction was made” to contend that the assessee’s TDS claim cannot be based on the receipts of M/s REPL. However, the assessee fairly admitted throughout the proceedings for its TDS claim of ` 1,20,73,097/- that the benefit of such claim has not been availed by M/s. REPL. Therefore, the revenue, having assessed M/s REPL’s income in respect to such TDS claim cannot now deny the assessee’s claim on the mere technical ground that the income in respect of the said TDS claim was not that of the assessee, given that M/s Relcom (the assessee) and M/s REPL are sister concerns and M/s REPL has not raised any objection with regard to the assessee’s TDS claim of 1,20,73,097/-.

8. This Court’s reasoning is supported by a ruling of the Division Bench of the Andhra Pradesh High Court in CIT v. Bhooratnam, (2013) 357 ITR 196 (AP), where the Court noted as follows:

“In our view, the CIT (Appeals) and the Tribunal have rightly held that the assessee is entitled to the credit of the TDS mentioned in the TDS certificates issued by the contractor, whether the said certificate is issued in the name of the Joint Venture or in the name of a Director of the assessee company. They have considered the terms of the agreement dated 12-03- 2003 among the parties to the joint venture and held that credit for TDS certificates cannot be denied to the assessee while assessing the contract receipts mentioned in the said certificates as income of the assessee. The income shown in the TDS certificates has either to be taxed in the hands of the joint venture or in the hands of the individual co-joint venturer. As the joint venture has not filed return of income and claimed credit for TDS certificates and the TDS certificates have not been doubted, credit has to be granted to the TDS mentioned therein for the assessee.

The Revenue cannot be allowed to retain tax deducted at source without credit being available to anybody. If credit of tax is not allowed to the assessee, and the joint venture has not filed a return of income, then credit of the TDS cannot be taken by anybody. This is not the spirit and intention of law.”(emphasis supplied)

9. At this stage, it is also relevant to note the provisions of Rule 37BA (of Income Tax Rules, 1962), which envisions grant of TDS credit to entities other than the deductee (herein, M/s REPL). We must clarify that we are not oblivious of the fact that Rule 37BA (of Income Tax Rules, 1962) is not directly applicable in the facts of this case. The reliance placed on Rule 37BA (of Income Tax Rules, 1962) is merely to demonstrate that in not all circumstances is TDS credit given to the deductee.

10. This Court relies upon the well-settled dictum that procedure is the handmaid of justice, and it cannot be used to hamper the cause of justice [Sardar Amarjit Singh Kalra v. Pramod Gupta, (2003) 3 SCC 272]. Therefore, the revenue’s contention that the assessee, instead of claiming the entire TDS amount, ought to have sought a correction of the vendor’s mistake, would unnecessarily prolong the entire process of seeking refund based on TDS credit.

11. In light of the aforesaid reasons, the question of law framed is answered against the revenue and the appeal is accordingly dismissed.

S. RAVINDRA BHAT

(JUDGE)

R.K. GAUBA

(JUDGE)

JANUARY 16, 2015

×

Similar Ripples

Questions

Court allows TDS claim despite technical error in PAN, dismisses revenue's appeal.

Write your CommentSimilar Posts

Generic

- Reportdata/4121.pdf