Court Condones Delay in Tax Return Filing Due to Genuine Hardship

Full News

Court Condones Delay in Tax Return Filing Due to Genuine Hardship

Court Condones Delay in Tax Return Filing Due to Genuine Hardship

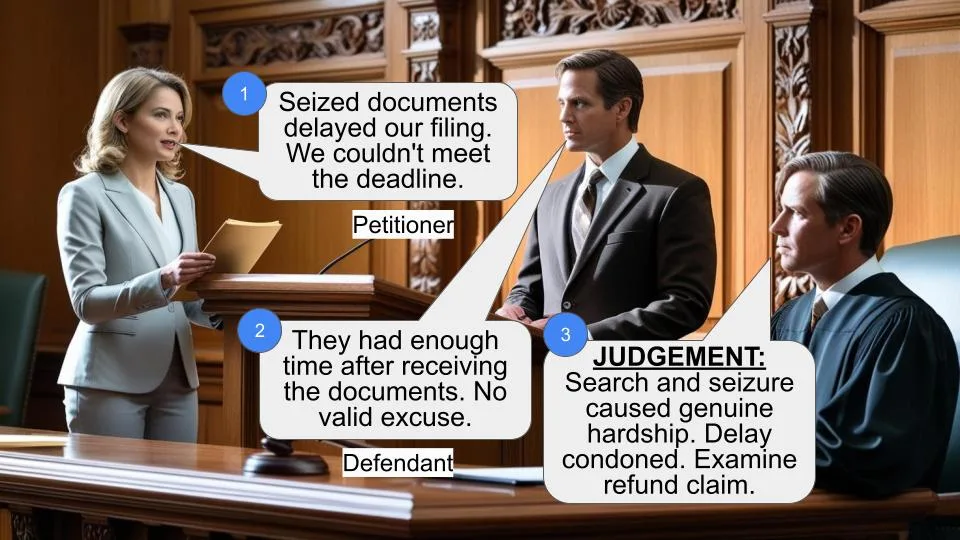

This case involves Dilip Buildcon Ltd., a public limited company, challenging an order that rejected their application to condone a delay in filing their income tax return. The company faced difficulties due to a search and seizure operation by tax authorities. The High Court ultimately allowed the petition, quashing the earlier order and directing the tax authority to examine the company's refund claim on merits.

Get the full picture - access the original judgement of the court order here

Case Name:

Dilip Buildcon Ltd. vs Union of India (High Court of Madhya Pradesh)

Writ Petition No.21190/2015

Date: 30th June 2016

Key Takeaways:

1. The court interpreted "genuine hardship" in Section 119(2)(b) (of Income Tax Act, 1961) liberally.

2. Circumstances beyond a taxpayer's control can justify delay in filing returns.

3. The magnitude of business operations and complexity of accounts are relevant factors in considering delay.

4. Courts can intervene if tax authorities fail to consider all relevant factors in condonation applications.

Issue:

Should the delay in filing the income tax return be condoned under Section 119(2)(b) (of Income Tax Act, 1961), due to genuine hardship faced by the assessee?

Facts:

1. Dilip Buildcon Ltd. is engaged in infrastructure development.

2. Search and seizure operations were conducted on the company and its group concerns on June 20-21, 2012.

3. Thousands of documents, including books of accounts and hard disks, were seized.

4. The company received the seized documents in installments, with the final set received on October 21, 2013.

5. The due date for filing the return was November 30, 2013.

6. The company filed its return on March 31, 2014, disclosing a total income of Rs.2,65,57,04,226/- and claiming a refund of Rs.2,08,73,620/-.

7. The company applied for condonation of delay under Section 119(2)(b) (of Income Tax Act, 1961), which was rejected by the tax authority.

Arguments:

Petitioner (Dilip Buildcon Ltd.):

- The delay was bonafide and only four months long.

- It was impossible to file the return by the due date due to the volume of seized documents.

- The company had a history of filing returns regularly in previous years.

Respondent (Tax Authority):

- The company received the required documents within time and was obligated to file the return by the due date.

- The company failed to properly explain the reason for the delay.

Key Legal Precedents:

1. Sitaldas K. Motwani vs. Director General of Income Tax (International Taxation), New Delhi [2010] 323 ITR 223 (Bombay)

2. Artist Tree (P.) Ltd. v. Central Board of Direct Tax [2014] 369 ITR691 (Bombay)

3. B.M. Malani v. Commissioner of Income Tax, [2008] 306 ITR (SC)

These cases established that "genuine hardship" should be interpreted liberally and that substantial justice should prevail over technical considerations.

Judgement:

The High Court allowed the petition, finding that:

1. There was genuine hardship to the petitioner in not filing the return within time.

2. The magnitude of the company's accounts and the complexity of the search and seizure operation justified the delay.

3. It was unreasonable to expect the company to complete the process within one month of receiving the final set of documents.

4. The delay of four months in filing the return for the assessment year 2013-14 should be condoned.

The court quashed the impugned order and directed the tax authority to examine the company's refund claim on merits within three months.

FAQs:

1. Q: What is Section 119(2)(b) (of Income Tax Act, 1961)?

A: It gives power to the tax authorities to admit applications or claims for exemptions, deductions, or refunds after the expiry of the specified period to avoid genuine hardship.

2. Q: How did the court interpret "genuine hardship"?

A: The court interpreted it liberally, considering factors like the complexity of the case, volume of documents involved, and circumstances beyond the taxpayer's control.

3. Q: Does this judgment set a precedent for all late tax filings?

A: While it provides guidance, each case would still be judged on its own merits and circumstances.

4. Q: What should taxpayers learn from this case?

A: If facing genuine difficulties in filing returns on time, they should document the reasons clearly and apply for condonation of delay, explaining the hardships faced.

5. Q: Can the tax authority still reject the company's refund claim?

A: Yes, the court only directed the authority to examine the claim on merits. The refund will depend on the company's eligibility as per tax laws.

1. Petitioner has filed this petition against the order Annexure P/7 dated 09.06.2015, by which the application of the petitioner filed under Section 119(2)(b) (of Income Tax Act, 1961) has been rejected.

2. The petitioner is a public limited company incorporated under the provisions of Companies Act, 1956. It is engaged in the business of infrastructure development i.e. construction of roads, bridges, residential houses and commercial complexes. Search proceedings under Section 132 (of Income Tax Act, 1961) (hereinafter called as â the Act of 1961) were carried out in the case of the petitioner and its group companies on 20.06.2012 and 21.06.2012. In the aforesaid proceedings, books of accounts, hard disk, other relevant documents and certain loose papers concerning to the petitioner company and group companies were seized. The petitioner company applied for photocopies of the documents seized by the department to enable the petitioner company to file income tax return. The petitioner company received seized documents and materials on 03.09.2012, 27.02.2013 and 21.10.2013. Thereafter, it filed the income tax return for the assessment year 2013-14 on 31.03.2014. The due date for filing the return was 30.11.2013.

3. Because the petitioner did not file the return within time and it was filed belatedly, the claim under Section 80IA (of Income Tax Act, 1961) was not allowed to the petitioner due to express provision contained in Section 80AC (of Income Tax Act, 1961). The petitioner pleaded that because it did not file return within time, hence, refund of an amount of Rs.2,08,73,620/- was not given to the petitioner. The petitioner filed an application under Section 119(2)(b) (of Income Tax Act, 1961) before the appropriate authority i.e. Central Board of Direct Taxes to condone the delay and admit application of the petitioner for refund. That application has been dismissed vide impugned order.

4. The petitioner in the petition pleaded that there was bonafide delay on the part of the petitioner. The delay was of four months in filing the return because seized documents were made available to the petitioner on 21.10.2013. The petitioner reconciled all the documents and it was not possible for the petitioner to file the return on due dated i.e. 31.11.2013. Thereafter, the petitioner filed return on 31.03.2014. The petitioner further pleaded that it had filed the return regularly in previous time. There was no delay in filing return. The respondents in reply pleaded that the petitioner had received the required documents which were seized by the authorities during search operation within time. It was the obligation of the petitioner to file the return within time. Hence, the petitioner is not eligible to condone the delay.

5. Learned counsel appearing on behalf of the petitioner has submitted that there was no mistake on the part of the petitioner in filing the return belatedly for the assessment year 2013-14. There was a delay of four months. Section 119(2)(b) (of Income Tax Act, 1961) gives power to the Board (C.B.D.T.) to condone the delay to avoid genuine hardship. The Board has not applied its mind properly in arriving on a conclusion that the petitioner is not eligible to condone the delay of four months. In support of his contentions, learned counsel relied on the following judgments :

1) Sitaldas K. Motwani vs. Director General of Income Tax (International Taxation), New Delhi [2010] 323 ITR 223 (Bombay).

2) Artist Tree (P.) Ltd. v. Central Board of Direct Tax [2014] 369 ITR691 (Bombay).

3) B.M. Malani v. Commissioner of Inocome Tax, [2008] 306 ITR (SC).

4) R. Seshammal v. Income Tax Officer, [1999] 237 ITR 185 (Madras).

5) All Gujarat Federation of Tax Consultants v. Central Board of Direct Taxes [2015] 378 ITR 160 (Gujarat).

6. Learned Standing Counsel appearing for the revenue has contended that the petitioner had received the copies of the assessed documents well within time. It was obligatory on the part of the petitioner to file the return within due date. The petitioner has not explained properly that what was

the reason for delay. The petitioner cannot get benefit of its own wrong. The authority has considered the case of the petitioner and passed appropriate order.

Hence, there is no merit in this petition. In alternate, learned counsel for the revenue has submitted that the matter may be remanded back to the Board for fresh consideration. In support of his contentions, learned counsel relied on the following judgments :

1) Madhya Pradesh State Electricity Board vs. Union of India & another reported in (2011) 239 CTR 0087;

2) Deputy Commissioner of Income Tax and another vs. Vasco Sales and Marketing Corporation reported in (2015) 377 ITR 0318 (Ker);

3) T.V. Hameed & others vs. Union of India and another reported in (2012) 67 DTR 0123;

4) J.K. Synthetics vs. Central Board of Direct Taxes reported (2009) 19 DTR 0327 and

5) Tiam House Service Ltd. vs. Central Board of Direct Taxes & others reported in (2000)163 CTR 0022.

7. Section 119(2)(b) (of Income Tax Act, 1961) gives power to the Income Tax Authority to admit the claim for refund after expiry of the period specified in the Act. The relevant provision reads as under:

â119(2)(b). the Board may, if it considers it desirable or expedient so to do for avoiding genuine hardship in any case or class of cases, by general or special order, authorise any income-tax authority, not being a Commissioner (Appeals) to admit an application or claim for any exemption, deduction, refund or any other relief under this Act after the expiry of the period specified by or under this Act for making such application or claim and deal with the same on merits in accordance with law;â

The Statutory provision provides that the Board has power to admit the application after condoning the delay for avoiding genuine hardship in any case or class of cases. The word âgenuine hardshipâ has been interpreted by the different High Courts in various judgments in the context of Section 119(2)(b) (of Income Tax Act, 1961). A Division Bench of Bombay High Court in the matter of Sitaldas K. Motwani vs. Director General of Income Tax (International Taxation), New Delhi reported in [2010] 187 Taxman 44 (Bombay) has held as under in regard to genuine hardship:

15. The phrase âgenuine hardshipâ used in Section 119(2)(b) (of Income Tax Act, 1961) should have been construed liberally even when the petitioner has complied with all the conditions mentioned in Circular dated 12.10.1993. The Legislature has conferred the power to condone delay to enable the authorities to do substantive justice to the parties by disposing of the matters on merit. The expression âgenuineâ has received a liberal meaning in view of the law laid down by the Apex Court referred to hereinabove and while considering this aspect, the authorities are expected to bare in mind that ordinarily the applicant, applying for condonation of delay does not stand to benefit by lodging its claim late. Refusing to condone delay can result in a meritorious matter being thrown out at the very threshold and cause of justice being defeated. As against this, when delay is condoned the highest that can happen is that a cause would be decided on merits after hearing the parties. When substantial justice and technical considerations are pitted against each other, cause of substantial justice deserves to be preferred for the other side cannot claim to have vested right in injustice being done because of a non-deliberate delay. There is no presumption that delay is occasioned deliberately, or on account of culpable negligence, or on account of mala fides. A litigant does not stand to benefit by resorting to delay. In fact he runs a serious risk. The approach of the authorities should be justice-oriented so as to advance cause of justice. If refund is legitimately due to the applicant, mere delay should not defeat the claim of refund.

10. Again the Bombay High Court in the case of

Artist Tree (P.) Ltd. vs. Central Board of Direct Taxes reported in [2014] 52 taxman.com 152 (Bombay) has held as under in regard to genuine hardship:

â11. The expression âgenuine hardshipâ came up for consideration of the Supreme Court in case of B.M. Malani (supra), wherein, by reference to New Collins Concise English Dictionary, the Supreme Court accepted the position that âgenuineâ means not fake or counterfeit, real, not pretending (not bogus or merely a ruse). Further, a genuine hardship would, interalia, mean a genuine difficulty. The ingredients of genuine hardship must be determined keeping in view the dictionary meaning thereof and legal conspectus attending thereto. For the said purpose another well known principle, namely, that a person cannot take advantage of his own wrong, may also have to be borne in mind. Compulsion to pay any unjust dues per se would cause hardship. But a question as to whether the default in payment of the amount was due to circumstances beyond the control of assessee, also bears consideration.â

The Division Bench relied on the judgment of the Apex Court reported in B.R. Malani vs. CIT, [2008] 306 ITR 196/174 Taxman 363 (SC).

11. From the above cited judgments, the legal principle is that the word âgenuine hardshipâ used in Section 119(2)(b) (of Income Tax Act, 1961) is to be construed liberally and the expression âgenuineâ means not fake or counterfeit, real, not pretending (not bogus or merely a ruse). This is dictionary meaning of the word âgenuineâ. However, when the delay is deliberate or on account of culpable negligence or on account of mala fides, the authority can reject the application.

12. From the facts of the present case, it is clear that a search operation was carried out at the residence of members of the management of the company and the office of the company and its sister concerns. The authorities had seized thousands of loose papers, books of accounts of the company, hard disc and other relevant documents. The petitioner received seized material finally on 21.10.2013. The papers were thousands in numbers and entries were running on lacks. Documents, prior to the aforesaid date, were not in possession of the petitioner. Hence, the petitioner was not able to finalize the accounts and determine the tax liability. The search and seizure proceedings were conducted on 23 group concerns of the assessee. Within one month, it was not possible for the petitioner to file return because the petitioner in the return disclosed total income of Rs.2,65,57,04,226/-. Petitioner claimed refund of Rs.2,08,73,620/-. The business of the petitioner is quite huge. The seizure operations were carried out at headquarter of the petitioner company, residence of office bearers and near about 28 sister concerns. In these circumstances, looking to the magnitude of accounts, it is unreasonable to hold that the petitioner could have had completed the process within a period of one month after receiving the final set of documents on 21.10.2013. In our opinion, in the facts and circumstances of the case, there was âgenuine hardshipâ to the petitioner in not filing the return within time. Hence, it would be just and proper to condone the delay.

13. The arguments advanced by the learned counsel for the respondents/revenue that the matter be remanded back to the authority cannot be accepted because the authority (C.B.D.T.) has considered the merits of the case and thereafter, rejected the application. The judgments cited by learned counsel for the revenue are in the context of facts where no reasoned order was passed by the authority. In the present case, a well reasoned order has been passed. Hence, it would not be just and proper to remand the case back to the authority. Looking to the overall facts of the case, in our opinion, it is just and proper to condone the delay of four months in filing the return for the assessment year 2013-14.

14. Consequently, the petition is allowed. The impugned order Annexure P/7 dated 09.06.2015 is hereby quashed. The application filed by the petitioner under Section 119(2)(b) (of Income Tax Act, 1961) is hereby allowed. The competent authority is directed to examine the claim of the petitioner for refund on merits in accordance with law. If the petitioner is eligible for refund, the same be provided to the petitioner. The authority shall decide the claim of refund within a period of three months from the date of the receipt of the copy of the order.

15. No order as to costs.

(S.K. GANGELE )

JUDGE

(ASHOK KUMAR JOSHI )

JUDGE

×