Full News

Court Denies Appeal Due to Excessive Delay in Refiling, Citing Lack of Due Diligence

Court Denies Appeal Due to Excessive Delay in Refiling, Citing Lack of Due Diligence

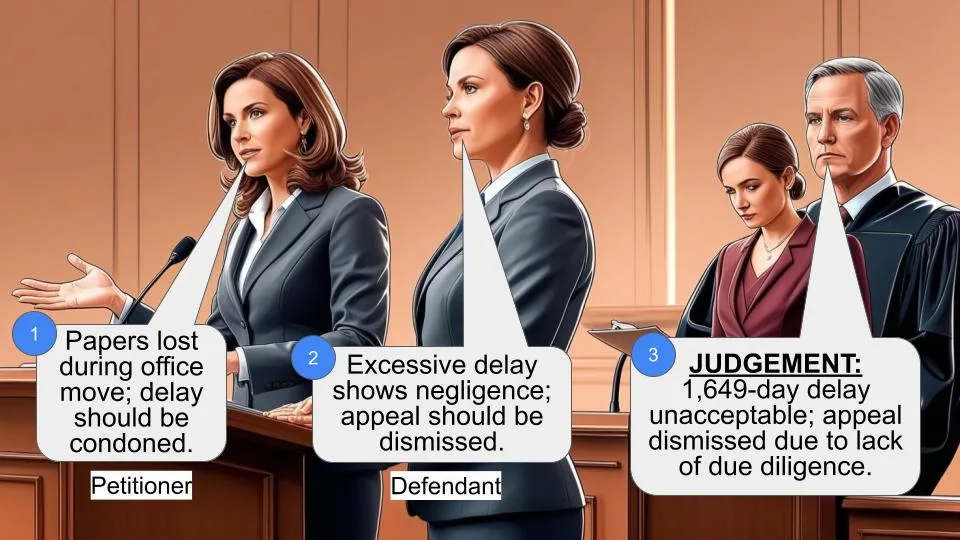

This case is all about a company called Rane (Madras) Ltd. that tried to file an appeal against an Income Tax Officer’s decision. The big issue was that they took way too long (1,649 days!) to refile some paperwork, and the court wasn’t having it. They basically said, “Sorry, but that’s just too long to wait without a good reason,” and dismissed the appeal.

Get the full picture - access the original judgement of the court order here

Case Name:

Rane (Madras) Ltd. vs Income Tax Officer (High Court of Madras)

Tax Case(Appeal).Sr.No.91371 of 2010 and CMP No.8551 of 2016

Date: 10th June 2016

Key Takeaways:

- Courts take timely filing of appeals seriously.

- Lack of due diligence in filing appeals can be seen as gross negligence.

- Enormous delays without valid explanations are likely to be rejected.

- Courts balance justice for both parties, not just the one seeking delay condonation.

- Proper record-keeping and prompt action in legal matters are crucial.

Issue:

The main question here was: Should the court condone (or forgive) a delay of 1,649 days in refiling appeal papers when the explanation provided is simply that the papers were lost and couldn’t be traced?

Facts:

- Rane (Madras) Ltd. filed an appeal against an order from the Income Tax Officer.

- The appeal papers were returned on November 22, 2010, to fix some defects.

- They were supposed to refile by December 2, 2010.

- But guess what? They only refiled on June 8, 2015 - that’s 1,649 days late!

- Their excuse? They said the papers got mixed up when their lawyer’s office moved and couldn’t be found until recently.

Arguments:

Rane (Madras) Ltd.'s side:

- They argued that the delay should be condoned because the appeal papers were lost during their lawyer’s office relocation.

- They claimed they only recently found the papers.

The court’s perspective:

- The explanation provided was too simplistic and unsatisfactory.

- The enormous delay of 1,649 days requires a more stringent scrutiny.

- The appellant showed a lack of diligence in pursuing their appeal.

Key Legal Precedents:

The court relied on some important previous cases:

- H. Dohil Constructions Company Private Limited v. Nahar Exports Limited and Another (2015) 1 Supreme Court Cases 680

- This case emphasized the need for due diligence in filing appeals and that enormous delays without valid explanations can be seen as gross negligence.

2. Esha Bhattacharjee v. Raghunathpur Nafar Academy (2013) 12 SCC 649

- This case laid out several principles for considering delay condonation applications, including:

- a) No presumption of deliberate delay, but gross negligence should be noted.

- b) Lack of good faith is significant.

- c) Courts should weigh the balance of justice for both parties.

3. Tamilnadu Mercantile Bank Ltd. v. Appellate Authority (1990) 1 LLN 457

- This case was also considered in forming the principles for delay condonation.

Judgement:

In the end, the court said, “Nope, we’re not buying it.” They refused to condone the delay of 1,649 days in refiling the appeal papers. The court felt that:

- The reasons given weren’t satisfactory.

- The appellant (Rane Madras Ltd.) hadn’t been diligent in pursuing their appeal.

- The inaction was obvious.

- So, they dismissed both the petition to condone the delay (CMP No.8551 of 2016) and the main appeal (TCA Sr.No.91371 of 2010) right at the start.

FAQs:

Q: Why was the court so strict about the delay?

A: Courts take timely filing seriously to ensure justice isn’t delayed. They expect parties to show due diligence, especially in important matters like tax appeals.

Q: Could a better explanation have changed the outcome?

A: Possibly. If Rane (Madras) Ltd. had provided a more detailed, convincing explanation with evidence of their efforts to locate the papers, the court might have been more sympathetic.

Q: What lesson can other companies learn from this case?

A: Always be prompt with legal filings, keep good records, and if delays occur, provide thorough, honest explanations with evidence of your efforts to comply.

Q: Does this mean courts never allow delays?

A: Not at all. Courts can condone delays, but they need valid, well-explained reasons, especially for lengthy delays like in this case.

Q: What could Rane (Madras) Ltd. have done differently?

A: They could have been more proactive in tracking their appeal, maintained better records, and perhaps filed for an extension earlier when they realized the papers were missing.

1. The Miscellaneous Petition is to condone the delay of 1649 days in representing the tax case appeal. Supporting the case for delay in representation of 1649 days, petitioner has only contended that while the office of the learned counsel was shifted, Tax Case Appeal bundles were mixed up and could not be traced. Bundles were traced out only now.

2. Perusal of the affidavit shows that the appeal papers were returned on 22.11.2010 to comply with certain defects and that the same ought to have been represented on or before 02.12.2010, but, represented only on 08.06.2015. While setting out the principles of law to be followed, in the matter of considering the applications filed for condonation, in a recent decision in H.Dohil Constructions Company Private Limited V. Nahar Exports Limited and Another, reported in 2015 (1) Supreme Court Cases 680, the Hon'ble Supreme Court, after considering the Hon'ble Division Bench judgment of this Court in Tamilnadu Mercantile Bank Ltd., Vs. Appellate Authority, reported in (1990) 1 LLN 457 and decision of the Hon'ble Supreme Court in Esha Bhattacharjee v. Raghunathpur Nafar Academy, reported in (2013) 12 SCC 649, at paragraph Nos.23 and 24, held as follows:

“23. We may also usefully refer to the recent decision of this Court in Esha Bhattacharjee [Esha Bhattacharjee v. Raghunathpur Nafar Academy, reported in (2013) 12 SCC 649], where several principles were culled out to be kept in Principles (iv), (v), (viii), (ix) and (x) of para 21 can be usefully referred to, which read as under: (SCCpp.658-59)

“21.4(iv) No presumption can be attached to deliberate causation of delay but, gross negligence on the part of the counsel or litigant is to be taken note of.

21.5. (v) Lack of bona fides imputable to a party seeking condonation of delay is a significant and relevant fact.

21.8. (viii) There is a distinction between inordinate delay and a delay of short duration or few days, for to the former doctrine of prejudice is attracted whereas to the latter it may not be attracted. That apart, the first one warrants strict approach whereas the second calls for a liberal delineation.

21.9 (ix) The conduct, behaviour and attitude of a party relating to its inaction or negligence are relevant factors to be taken into consideration. It is so as the fundamental principle is that the courts are required to weight the scale of balance of justice in respect of both parties and the said principle cannot be given a total go-by in the name of liberal approach.

21.10. (x) If the explanation offered is concocted or the grounds urged in the application are fanciful, the courts should be vigilant not to expose the other side unnecessarily to face such a litigation.

24. When we apply those principles to the case on hand, it has to be stated that the failure of the Respondents in not showing due diligence in filing of the appeals and the enormous time taken in the refiling can only be construed, in the absence of any valid explanation, as gross negligence and lacks in bonafides as displayed on the part of the Respondents. Further, when the Respondents have not come forward with proper details as regards the date when the papers were returned for refiling, the non-furnishing of satisfactory reasons for not refiling of papers in time and the failure to pay the Court fee at the time of the filing of appeal papers on 06.09.2007, the reasons which prevented the Respondents from not paying the Court fee along with the appeal papers and the failure to furnish the details as to who was their counsel who was previously entrusted with the filing of the appeals cumulatively considered, disclose that there was total lack of bonafides in its approach. It also requires to be stated that in the case on hand, not refiling the appeal papers within the time prescribed and by allowing the delay to the extent of nearly 1727 days, definitely calls for a stringent scrutiny and cannot be accepted as having been explained without proper reasons. As has been laid down by this Court, Courts are required to weigh the scale of balance of justice in respect of both parties and the same principle cannot be given a go-by under the guise of liberal approach even if it pertains to refiling. The filing of an application for condoning the delay of 1727 days in the matter of refiling without disclosing reasons, much less satisfactory reasons only results in the Respondents not deserving any indulgence by the Court in the matter of condonation of delay. The Respondents had filed the suit for specific performance and when the trial Court found that the claim for specific performance based on the agreement was correct but exercised its discretion not to grant the relief for specific performance but grant only a payment of damages and the Respondents were really keen to get the decree for specific performance by filing the appeals, they should have shown utmost diligence and come forward with justifiable reasons when an enormous delay of five years was involved in getting its appeals registered.”

In the above reported case, the Apex Court also considered the aspect of delay in refiling of the appeal and on the facts and circumstances of the case,observed that it was without disclosing the reasons, much less satisfactory reasons. In H.Dohil constructions case, it was a delay of 1727 days in refiling.

3. Reverting to the case on hand, the number of days of delay in refiling is 1649. Reasons assigned are simpliciter that papers were lost and could not be traced. Appellant who had taken up to the cause of adjudicating the correctness of the order in I.T.A.No.106/Chny/2009 dated 11.06.2010, has not been diligent in pursuing the appeal. Inaction is per se apparent. Reasons assigned are not satisfactory. Having regard to the principles set out supra, we are not inclined to condone the delay of 1649 days in representing the appeal papers. Hence, the condone delay petition viz. CMP No.8551 of 2016 is dismissed. Consequently, TCA Sr.No.91371 of 2010 is also dismissed at SR stage itself. No costs.

[S.M.K., J.] [D.K.K., J.]

10.06.2016

Index: Yes/No

Internet: Yes/No

To

The Income Tax Officer, Company Circle, Chennai - 600 034.

S.MANIKUMAR, J.,

and

D.KRISHNAKUMAR, J.,

×

Similar Ripples

Questions

Court Denies Appeal Due to Excessive Delay in Refiling, Citing Lack of Due Diligence

Write your CommentSimilar Posts

Generic

- Reportdata/2778.pdf