Court Dismisses Appeal on Tax Penalty, Upholds Tribunal's Decision

Full News

Court Dismisses Appeal on Tax Penalty, Upholds Tribunal's Decision

Court Dismisses Appeal on Tax Penalty, Upholds Tribunal's Decision

This case involves an appeal by the Principal Commissioner of Income Tax against Atotech India Ltd. (formerly Max Atotech Limited) regarding a penalty imposed under Section 271(1)(c) (of Income Tax Act, 1961). The High Court dismissed the appeal, agreeing with the Income Tax Appellate Tribunal's decision to cancel the penalty of Rs.62,41,758/- imposed on the assessee.

Get the full picture - access the original judgement of the court order here

Case Name:

Principal Commissioner of Income Tax vs Atotech India Ltd.(High Court of Punjab & Haryana)

ITA-347-2015 (O&M)

Date: 30th November 2016

Key Takeaways:

1. Voluntary disclosure of changes in tax claims may prevent penalties.

2. Absence of financial implications can influence penalty decisions.

3. Courts may consider the intent behind tax claim changes when assessing penalties.

Issue:

Was the Income Tax Appellate Tribunal justified in cancelling the penalty imposed on Atotech India Ltd. under Section 271(1)(c) (of Income Tax Act, 1961)?

Facts:

1. Atotech India Ltd. (formerly Max Atotech Limited) filed a return for the assessment year 2004-2005.

2. Initially, the company sought to set off its income against brought forward business losses from earlier years.

3. During proceedings under Section 143 (of Income Tax Act, 1961), the company changed its claim via a letter dated 13.12.2006.

4. The new claim sought to set off the income against unabsorbed depreciation instead of business losses.

5. The tax effect in both scenarios was nil, with no future financial implications.

6. The Income Tax Department imposed a penalty of Rs. 62,41,758/- under Section 271(1)(c) (of Income Tax Act, 1961).

7. The Income Tax Appellate Tribunal cancelled this penalty.

8. The Principal Commissioner of Income Tax appealed against the Tribunal's decision.

Arguments:

Appellant (Principal Commissioner of Income Tax):

1. The Tribunal was not justified in cancelling the penalty.

2. Rejection of the assessee's patently wrong claim should amount to furnishing inaccurate particulars of income or concealment of income.

3. The assessee should be liable for penalty under Section 271(1)(c) (of Income Tax Act, 1961).

Respondent (Atotech India Ltd.):

1. The change in claim was based on a legal opinion from a reputable firm of Chartered Accountants.

2. The disclosure of the change was voluntary and not due to the notice under Section 143(2) (of Income Tax Act, 1961).

3. There was no financial implication or tax effect due to the change in claim.

Key Legal Precedents:

The judgment doesn't explicitly mention any specific legal precedents. However, it refers to Sections 143 and 271(1)(c) of the Income Tax Act, 1961.

Judgement:

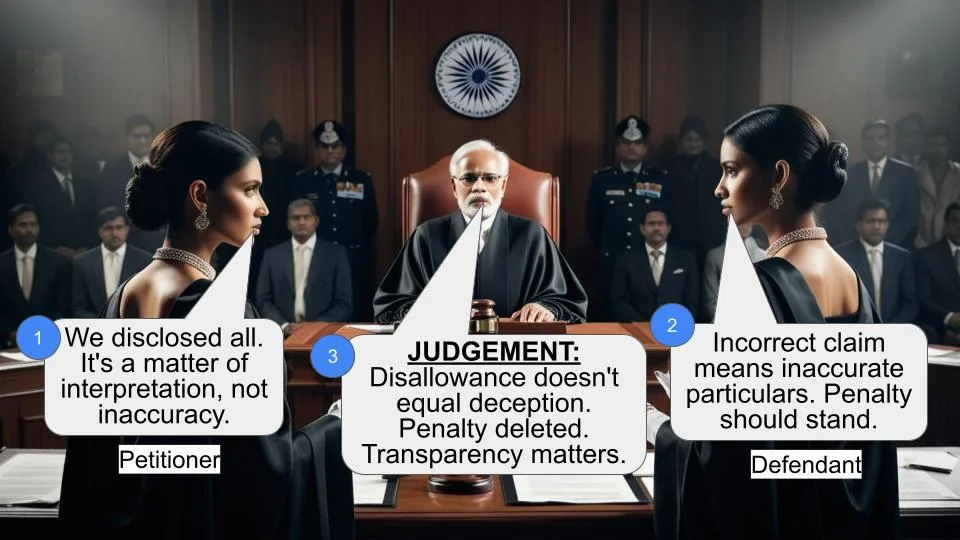

1. The High Court dismissed the appeal, agreeing with the Tribunal's decision.

2. The court found that the Tribunal's decision was neither perverse nor absurd.

3. The court noted that the change in claim was based on a legal opinion and found no evidence of malafides.

4. The voluntary nature of the disclosure and the absence of financial implications were considered significant factors.

5. The court concluded that no substantial question of law arose in this case.

FAQs:

1. Q: What was the main issue in this case?

A: The main issue was whether the assessee (Atotech India Ltd.) should be penalized for changing its tax claim from setting off income against brought forward business losses to unabsorbed depreciation.

2. Q: Why did the court dismiss the appeal?

A: The court found no substantial question of law in the case and agreed with the Tribunal's decision that the penalty was not justified, considering the voluntary disclosure and lack of financial implications.

3. Q: What factors influenced the court's decision?

A: The court considered the voluntary nature of the disclosure, the legal opinion obtained by the assessee, the absence of malafides, and the lack of financial implications due to the change in claim.

4. Q: What is Section 271(1)(c) (of Income Tax Act, 1961)?

A: This section deals with penalties for concealment of income or furnishing inaccurate particulars of income.

5. Q: Does this judgment set a precedent for similar cases?

A: While each case is unique, this judgment suggests that courts may consider factors such as voluntary disclosure, intent, and financial implications when assessing penalties in tax cases.

1. This is an appeal against the order of the Tribunal allowing the respondent/assessee’s appeal against the order of the CIT (Appeals) in respect of the assessment year 2004-2005.

2. According to the appellant, the following substantial questions of law arise:-

“1. Whether on the facts and in the circumstances of the case and in law, the Hon’ble Tribunal was justified in cancelling the penalty u/s 271(1)(c) (of Income Tax Act, 1961) of Rs. 62,41,758/-?

2. Whether on the facts and in the circumstances of the case and in law, the Hon’ble Tribunal was justified in holding that rejection of the patently wrong claim of the assessee of setting off of brought forward business loss in its return of income would not amount to furnishing of inaccurate particulars of income/concealment of income and would not be liable for penalty u/s 271(1)(c) (of Income Tax Act, 1961)?”

3. The question is whether the assessee is liable to penalty in view of its change of stand in respect of its return of income for the said assessment year.

4. The assessee was earlier known as Max Atotech Limited. It appears initially to have been a private limited company and was thereafter converted into a public limited company. For the assessment year 2004-2005, the assessee in its return of income sought to set off its income against the brought forward business losses of the earlier years. Proceedings under Section 143 (of Income Tax Act, 1961) (in short the Act) were initiated in the course of which the assessee by a letter dated 13.12.2006 claimed the above set off against another head, namely, of unabsorbed depreciation. Admittedly, the tax effect in either case is nil. Further, it is admitted that even if the respondent was permitted to claim the set off against the unabsorbed depreciation, it would have no financial implication for the future.

5. The decision of the Tribunal that the respondent ought not to be made liable for penalty cannot be said to be perverse or absurd.

6. The Tribunal noted that the respondent had claimed the set off of its business income of Rs. 1.85 crores against the brought forward business losses of the earlier years on the basis of a legal opinion received from a leading firm of Chartered Accountants dated 15.06.2001. The Tribunal found nothing clandestine in the manner in which the opinion was sought. In any event, even our attention was not invited to anything which suggests any malafides either in the obtaining of the opinion or otherwise. Further, the loss was allowed to be carried forward in the assessment year, namely, assessment year 2002-2003. Inter alia, in these circumstances, the Tribunal found as a matter of fact that the letter dated 13.12.2006 was voluntary and not merely because a notice had been issued under Section 143(2) (of Income Tax Act, 1961). This is a perception on the basis of the facts of the case and warrants no interference.

7. In these circumstances including in view of the fact that there is no financial implication on account of the change in the basis of the claim, no substantial question of law arises in this case.

8. The appeal is, therefore, dismissed.

9. In view thereof, it is not necessary to consider the cross objections filed by the respondent.

(S.J. VAZIFDAR)

CHIEF JUSTICE

(DEEPAK SIBAL)

JUDGE

30.11.2016

×