Court Grants Relief in Tax Dispute: Assessee's Appeal to be Heard by CIT

Full News

Court Grants Relief in Tax Dispute: Assessee's Appeal to be Heard by CIT

Court Grants Relief in Tax Dispute: Assessee's Appeal to be Heard by CIT

A company (the petitioner) is challenging a decision made by the tax authorities. The main issue was that the tax office rejected the company's request for a stay on tax payment and even went ahead to freeze their bank accounts. The court stepped in and said, "Hold up! Let's give this another look." They've asked a higher tax authority to review the case quickly and make a fair decision.

Get the full picture - access the original judgement of the court order here

Case Name:

M/s Essjay Ericsson Private Limited Vs Commissioner of Income Tax, New Delhi & Ors. (High Court of Delhi)

W.P.(C) 1449/2020

Date: 7th February 2020

Key Takeaways:

1. The court is prioritizing fair process over immediate tax collection.

2. There's a clear message that tax authorities should consider stay applications carefully.

3. The judgment emphasizes the importance of reasoned orders in tax matters.

4. It shows the court's willingness to intervene in cases of potential injustice in tax proceedings.

Issue:

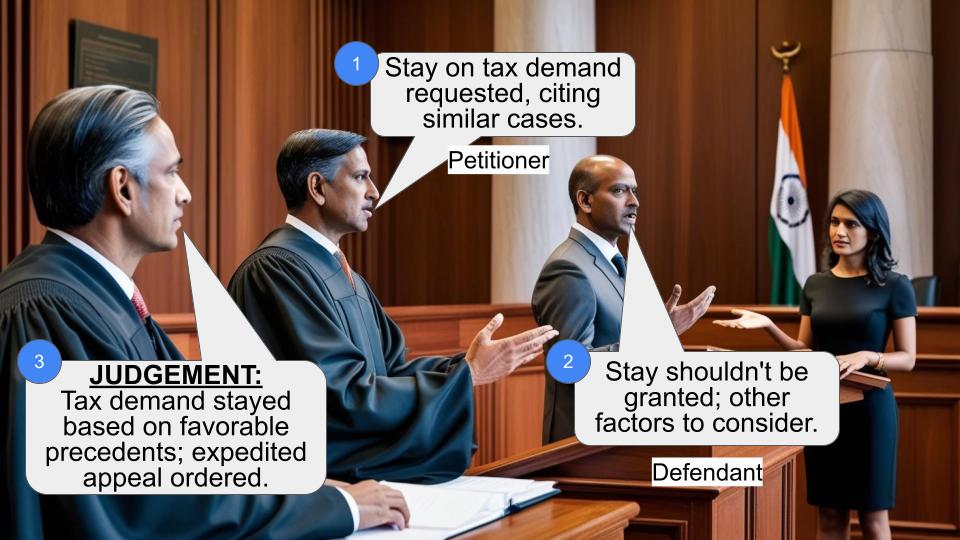

The main question here is: Should the petitioner's application for a stay on tax payment be reconsidered, and should their bank accounts be unfrozen pending this reconsideration?

Facts:

1. The petitioner (probably a company called Essjay Ericsson) had some tax issues.

2. They applied for a stay on tax payment under Section 220(6) (of Income Tax Act, 1961).

3. On January 23, 2020, the Assessing Officer said "Nope!" and rejected their application.

4. To make matters worse, the tax office went ahead and froze the company's bank accounts.

5. The company wasn't happy about this and took the matter to the High Court.

6. Meanwhile, they also had an appeal pending with the Commissioner of Income Tax (Appeals), or CIT(A) for short.

Arguments:

The petitioner's side:

- They're saying, "Hey, the Assessing Officer shouldn't have rejected our stay application so quickly."

- They're also arguing that freezing their bank accounts was unfair.

The tax department's side:

- We don't have their specific arguments, but they likely justified their actions based on tax laws and the need to collect dues.

Key Legal Precedents:

In this case, the court doesn't explicitly mention any previous cases. However, they're clearly applying principles of natural justice and fair hearing. The focus is on Section 220(6) (of Income Tax Act, 1961), which deals with stay applications on tax demands.

Judgement:

The court came down on the side of the petitioner. Here's what they decided:

1. They said, "Go ahead and file a stay application with the CIT(Appeals) right away."

2. They told the CIT(Appeals) to look at this application within two weeks.

3. Importantly, they said the CIT(Appeals) shouldn't be influenced by the Assessing Officer's earlier rejection.

4. If the CIT(Appeals) grants any relief, and if the tax office has taken more money than they should have, they need to give it back to the company.

5. The court emphasized that the CIT(Appeals) needs to give proper reasons for whatever they decide.

FAQs:

1. Q: Does this mean the company doesn't have to pay taxes?

A: Not necessarily. It just means they get another chance to argue why they shouldn't have to pay right now.

2. Q: Will the company get its money back?

A: If the CIT(Appeals) decides in their favor, yes, they could get some money back.

3. Q: How long will this process take?

A: The court has given a two-week deadline for the initial decision, but the overall process could take longer.

4. Q: What's the significance of this judgment?

A: It shows that courts are willing to step in to ensure fairness in tax proceedings, even at preliminary stages.

5. Q: Does this set a precedent for other cases?

A: While each case is unique, it does emphasize the importance of giving taxpayers a fair hearing before taking drastic actions like freezing bank accounts.

C.M. No. 5013/2020

Exemption allowed, subject to all just exceptions. The application stands disposed of.

Issue notice. Learned counsel for the respondents accepts notice. We have heard learned counsels and proceed to dispose of the petition at this stage itself. No counter-affidavit is called for in view of the order that we propose to pass.

The grievance of the petitioner is with regard to the rejection of the petitioner’s application under Section 220(6) (of Income Tax Act, 1961) by the Assessing Officer vide order dated 23.01.2020 and the consequent attachment of the bank accounts of the petitioner. We are informed that the petitioner’s appeal is already pending before the CIT (Appeals).

We permit the petitioner to immediately file the stay application before the CIT (Appeals). The CIT (Appeals) shall consider the same and pass an order thereon within two weeks without being influenced by the order dated 23.01.2020 passed by the Assessing Officer on the stay application under Section 220(6) (of Income Tax Act, 1961). The bank accounts of the petitioner already stand attached and the amounts recovered. In case, the CIT (Appeals) grants relief after hearing the assessee, to the extent that any amount may have been recovered in excess of the amount in respect of which stay is not granted, the same shall be restituted to the petitioner by the respondent.

It goes without saying that CIT (Appeals) shall pass a reasoned order on the stay application filed by the assesse.

The petition stands disposed of in the aforesaid terms.

Order dasti under the signatures of the Court Master.

VIPIN SANGHI, J

SANJEEV NARULA, J

FEBRUARY 07, 2020

N.Khanna

×

Questions

Court Grants Relief in Tax Dispute: Assessee's Appeal to be Heard by CIT

Write your CommentSimilar Posts

Generic

- Reportdata/6291.pdf