Court Halts Tax Assessment on Co-op Societies Pending Supreme Court Decision

Full News

Court Halts Tax Assessment on Co-op Societies Pending Supreme Court Decision

Court Halts Tax Assessment on Co-op Societies Pending Supreme Court Decision

This case involves Primary Agricultural Co-operative Societies challenging assessment orders for the 2016-17 tax year. The High Court directed the Revenue Department to keep the assessment orders in abeyance until the Supreme Court decides on a related Special Leave Petition (SLP) concerning deductions under Section 80P (of Income Tax Act, 1961).

Get the full picture - access the original judgement of the court order here

Case Name

K.4442 Pethampalayam Primary Agricultural Cooperative Credit Society Ltd. & Anr Vs Income Tax Officer (High Court of Madras)

W.P.Nos.1608 and 769 of 2019 and W.M.P.Nos.1785, 1786, 842 & 843 of 2019

Date: 06 September 2019

Key Takeaways

1. The High Court's decision provides temporary relief to co-operative societies regarding tax assessments.

2. The case highlights the ongoing dispute over the applicability of Section 80P (of Income Tax Act, 1961) deductions to co-operative societies.

3. The judgment emphasizes the importance of awaiting higher court decisions in similar matters before proceeding with assessments.

Issue

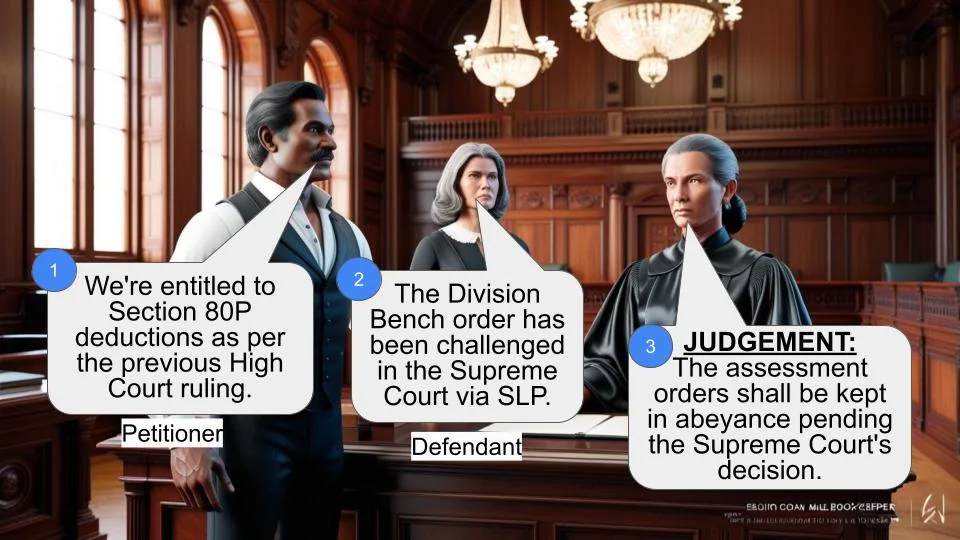

Are Primary Agricultural Co-operative Societies entitled to deduction under Section 80P (of Income Tax Act, 1961), and should the assessment orders be kept in abeyance pending the Supreme Court's decision on this matter?

Facts

1. The petitioners are Primary Agricultural Co-operative Societies

2. The Income Tax Officer passed assessment orders for the 2016-17 tax year, assessing tax payable by the societies

3. A Division Bench of the High Court had previously ruled in favor of the societies regarding Section 80P (of Income Tax Act, 1961) deductions

4. The Revenue Department challenged this decision in the Supreme Court through an SLP (No. 11745/2019)

Arguments

Petitioners' Arguments:

- The co-operative societies are entitled to deduction under Section 80P (of Income Tax Act, 1961)

- They rely on a previous Division Bench judgment of the High Court supporting their claim

Revenue's Arguments:

- The Division Bench order has been challenged in the Supreme Court

- Similar cases have been kept in abeyance by the High Court pending the Supreme Court's decision

Key Legal Precedents

1. Division Bench judgment in Tax Case Appeal Nos. 484 to 487 & 490 of 2016 dated 02.08.2016, which held that the exemption under Section 80P(4) (of Income Tax Act, 1961), is applicable to Credit Societies

2. High Court order in W.P.Nos.2552 of 2019 etc. dated 27.06.2019, where similar issues were kept in abeyance pending the Supreme Court decision

Judgement

The High Court disposed of the writ petitions with the following directions:

1. The Revenue Department shall keep the impugned assessment orders in abeyance until the disposal of the SLP by the Supreme Court

2. Both parties are free to pursue their remedies/actions, subject to the outcome of the SLP

3. No costs were awarded

FAQs

Q1: What is the main issue in this case?

A1: The main issue is whether Primary Agricultural Co-operative Societies are entitled to deduction under Section 80P (of Income Tax Act, 1961), and whether the assessment orders should be kept on hold pending a Supreme Court decision.

Q2: Why did the High Court decide to keep the assessment orders in abeyance?

A2: The High Court decided to keep the assessment orders in abeyance because a similar issue is pending before the Supreme Court in an SLP. This ensures that the final decision of the Supreme Court can be applied to these cases without causing undue hardship to the parties involved.

Q3: What happens if the Supreme Court rules in favor of the Revenue Department?

A3: If the Supreme Court rules in favor of the Revenue Department, the impugned assessment orders will be revived, and the law will take its course. The petitioners will still have the right to raise objections and defenses against the assessment notices

Q4: What if the Supreme Court rules in favor of the co-operative societies?

A4: If the Supreme Court rules in favor of the co-operative societies or refuses to interfere with the High Court's orders, the impugned assessment notices will be set aside without further reference to the High Court

Q5: Does this judgment affect other tax-related issues for these co-operative societies?

A5: No, this judgment specifically pertains to the benefit under Section 80P (of Income Tax Act, 1961). The Revenue Department is not precluded from proceeding against the petitioners on other tax-related issues in a manner known to law.

1. In both these writ petitions, the order of assessment is put to challenge by the respective writ petitioners.

2. Heard both sides.

3. The petitioners are Primary Agricultural Co-operative Societies.

In respect of the assessment year 2016-17, the assessing officer passed the orders of assessment thereby assessing the tax payable by the petitioners' society and making consequential demand notice as well.

4. The main contention of the writ petitioners is that the Co- operative Society is entitled to deduction under Section 80(P) (of Income Tax Act, 1961) and therefore, the order of assessment cannot be sustained. In support of their contentions, the petitioners sought to rely upon the common judgment made by the Division Bench of this Court in Tax Case Appeal Nos. 484 to 487 & 490 of 2016 dated 02.08.2016, wherein the Division Bench observed that the exemption spelt out in Section 80P(4) (of Income Tax Act, 1961), is applicable to the Credit Society.

5. However, the learned Standing Counsel for the respondents submitted that the said order of the Division Bench is put to challenge before the Apex Court by way of Special Leave Petition and the same is still pending consideration in SLP(C) No.11745/2019. He also invited this Court's attention to the order passed in W.P.Nos.2552 of 2019 etc. dated 27.06.2019 arising out of similar issue, wherein this Court disposed of those writ petitions by issuing a direction to the Revenue to keep the impugned proceedings therein in abeyance until disposal of the SLP filed by the Revenue before the Apex Court against the order of the Division Bench dated 02.08.2016, also with further directions. Therefore, it is submitted that the same order can be passed in these matters also.

6. Learned counsel for the respondents is not having any objection in passing the same order, since the similar writ petitions are disposed of on 27.06.2019 as stated supra.

7. The issue involved in this case is as to whether the petitioners' Society is entitled to deduction under Section 80(P) (of Income Tax Act, 1961). There is no dispute to the fact that the Division Bench of this Court has answered on such question in favour of the Society. However, it is stated that the said order of the Division Bench is put to challenge before the Apex Court where the matter is pending in SLP(C) No.11745/2019. In a batch of cases arising out of a same issue, the learned Judge of this Court passed an order on 27.06.2018 as follows:

4. In the light of the aforesaid undisputed position, the following order is passed:

a) All the 33 impugned notices will be kept in abeyance and there will be no further proceedings pursuant to the same until disposal of the Special Leave Petitions said to have been filed by respondent / Revenue in Hon'ble Supreme Court against the aforementioned orders of Hon'ble Division Bench of this Court particularly orders dated 02.08.2016 in Tax Case Appeal Nos.484-487 and 490 of 2016.

b) Subject to the outcome of the aforesaid Special Leave Petitions, i.e., if the Special Leave Petitions are in favour of the Revenue, the impugned orders will stand revived and law will take its course. If this scenario unfolds, it is open to the writ petitioner assessee to take all objections and defences available to section 148 (of Income Tax Act, 1961) notice including calling for reasons and limitation.

c) If the Special Leave Petitions end in favour of assessees and if the aforesaid Hon'ble Division Bench orders are confirmed or if the Hon'ble Supreme Court refuses to interfere with the orders of the High Court, all the 33 impugned notices will stand set aside without further reference to this Court.

d) Though obvious it is made clear that this order pertains to benefit under Section 80P (of Income Tax Act, 1961) qua writ petitioners covered by Hon'ble Division Bench orders against which Revenue submits that SLPs have been filed before Hon'ble Supreme Court and therefore, this order will not preclude Revenue from proceeding against writ petitioners in a manner known to law with regard to other issues, if any.

5. With the aforesaid directions, all the 33 writ petitions are disposed of and there will be no order as to costs. Consequently, connected miscellaneous petitions are closed.

8. Considering the above stated facts and circumstances, these Writ Petitions are disposed of as follows:

(a) The respondents shall keep the impugned assessment orders in abeyance till the disposal of the above S.L.P. by the Apex Court.

(b) It is open to either party to work out their remedy/action, subject to the outcome of the aforesaid S.L.P.

No costs. Consequently, connected miscellaneous petitions are closed.

×

Questions

Court Halts Tax Assessment on Co-op Societies Pending Supreme Court Decision

Write your CommentSimilar Posts

Generic

- Reportdata/4793.pdf