Court Quashes Reassessment Order Due to Procedural Lapse and Time Bar

Full News

Court Quashes Reassessment Order Due to Procedural Lapse and Time Bar

Court Quashes Reassessment Order Due to Procedural Lapse and Time Bar

In this case, the court addressed the issue of whether the reassessment of a taxpayer's income was valid when the mandatory procedure for handling objections was not followed and the reassessment was initiated after the statutory time limit. The court ruled in favor of the taxpayer, quashing the reassessment order due to procedural lapses and the expiration of the four-year time limit.

Get the full picture - access the original judgement of the court order here.

Case Name:

Gujarat Eco Textile Park Ltd. Vs Assistant Commissioner of Income Tax (High Court of Gujarat)

Special Civil Application No. 18622 of 2014

Key Takeaways

- The court emphasized the importance of following mandatory procedures before proceeding with reassessment.

- The reassessment was quashed because the objections raised by the taxpayer were not considered.

- The action for reassessment was also barred by the four-year limitation period as per the first proviso to Section 147 (of Income Tax Act, 1961).

- The court reinforced that any reassessment initiated after the statutory period without proper grounds is without jurisdiction.

Issue

Did the reassessment of the taxpayer's income violate procedural requirements and the statutory time limit under Section 147 (of Income Tax Act, 1961)?

Facts

- The taxpayer filed a return of income for the assessment year 2008-2009 on May 11, 2008.

- The initial assessment was completed on November 29, 2010, under Section 143(3) (of Income Tax Act, 1961).

- On October 14, 2013, a notice was issued under Section 147 (of Income Tax Act, 1961) for reopening the assessment.

- The taxpayer responded and requested the reasons for reopening, which were provided on October 25, 2013.

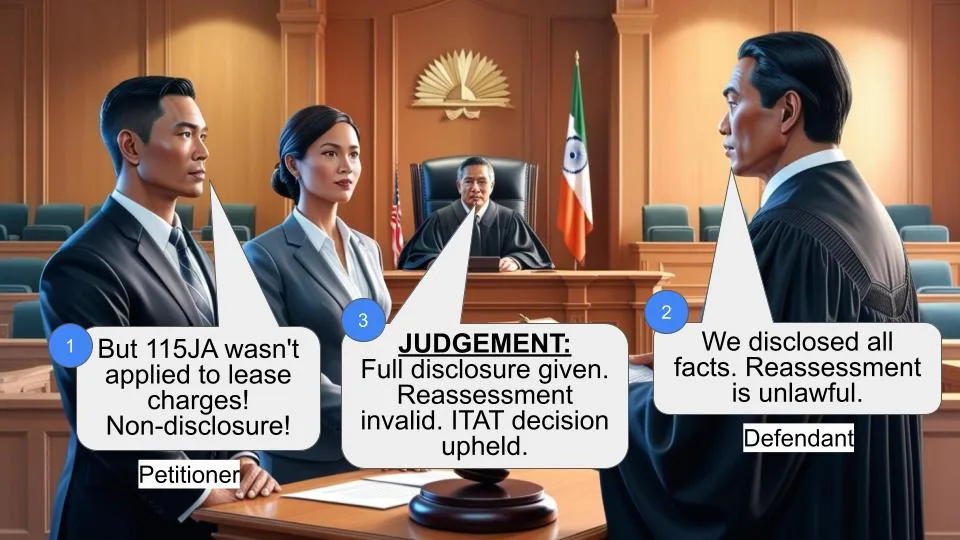

- The taxpayer filed objections on October 20, 2014, but the assessing officer proceeded with reassessment without addressing these objections.

- The reassessment order was passed on October 31, 2014, leading to the current petition.

Arguments

Petitioner (Taxpayer)

- Argued that the reassessment was barred by the four-year limitation period under the first proviso to Section 147 (of Income Tax Act, 1961).

- Claimed that all relevant facts were disclosed during the original assessment, and there was no failure to disclose material facts.

- Cited the case of General Motors India (P) Ltd. vs. Deputy Commissioner of Income Tax, where similar procedural lapses led to the quashing of reassessment orders.

Respondent (Revenue)

- Admitted that the objections were not disposed of before proceeding with reassessment.

- Argued that the reassessment was based on the non-admissibility of depreciation claimed by the taxpayer.

Key Legal Precedents

- General Motors India (P) Ltd. vs. Deputy Commissioner of Income Tax:

This case established that if objections to reassessment are not addressed, the reassessment process is invalid.

- Section 147 (of Income Tax Act, 1961):

Allows for reassessment if income has escaped assessment, but includes a proviso that bars reassessment after four years unless there was a failure to disclose material facts.

Judgement

The court quashed the reassessment order, ruling that:

- The reassessment was initiated without addressing the taxpayer's objections, violating mandatory procedural requirements.

- The reassessment was barred by the four-year limitation period as all relevant facts were disclosed during the original assessment.

- The action for reassessment was without jurisdiction and could not stand in the eye of the law.

FAQs

Q1. What was the main issue in this case?

A1. The main issue was whether the reassessment of the taxpayer's income was valid when the mandatory procedure for handling objections was not followed and the reassessment was initiated after the statutory time limit.

Q2. Why was the reassessment order quashed?

A2. The reassessment order was quashed because the objections raised by the taxpayer were not considered, and the reassessment was initiated after the four-year limitation period, making it without jurisdiction.

Q3. What is the significance of the four-year limitation period under Section 147 (of Income Tax Act, 1961)?

A3. The four-year limitation period under Section 147 (of Income Tax Act, 1961) bars reassessment after four years from the end of the relevant assessment year unless there was a failure to disclose material facts necessary for the assessment.

Q4. How does this case impact future reassessment proceedings?

A4. This case reinforces the importance of following mandatory procedures and respecting statutory time limits in reassessment proceedings. Failure to do so can render the reassessment invalid.

1. Rule. Mr.Mehta, learned counsel waives service of notice of Rule. With the consent of the learned counsel appearing for both the sides, the petition is finally heard.

2. The short facts of the case appear to be that on 11.05.2008, the petitioner filed return of income for the A.Y. of 2008-2009. The scrutiny of the return had taken place and vide order dated 29.11.2010, the assessment order was passed under Section 143(3) (of Income Tax Act, 1961) (hereinafter referred to as the ‘Act’). Thereafter, on 14.10.2013, notice was issued under Section 147 (of Income Tax Act, 1961). The petitioner replied to the notice vide letter dated 17.10.2013 demanding, inter alia, the reasons recorded. It appears that thereafter, vide communication dated 25.10.2013, the reasons were supplied to the petitioner. The petitioner filed objections vide letter dated 20.10.2014. The concerned officer, without considering the objections and without disposal of the objections filed by the petitioner against reasons recorded, proceeded for reassessment and ultimately, vide order dated 31.10.2014, reassessment order has been passed (Annexure-H). Under the circumstances, the present petition before this Court.

3. We have heard Mr.Vora, learned counsel appearing for the petitioner and Mr.Sudhir Mehta, learned counsel appearing for the respondent.

4. The learned counsel for the petitioner relied upon the decision of this Court in case of General Motors India (P) Ltd. V/s. Deputy Commissioner of Income Tax reported in (2013)354 ITR 244 (Guj) and contended that the case of the petitioner is directly covered by the said decision inasmuch as, after the reasons were supplied to the petitioner, the objections were filed by the petitioner but, such objections were not considered nor disposed of. It was submitted that the A.O. proceeded for reassessment and the reassessment order has been passed. He submitted that similar were the fact situations in the decision of this Court in case of General Motors India (P) Ltd. (supra) and, therefore, the impugned order of reassessment may be quashed by this Court.

5. The learned counsel for the petitioner also contended that in any case, notice under Section 147 (of Income Tax Act, 1961) for reopening of the assessment dated 14.10.2013 (Annexure - C) was barred by the first proviso to Section 147 (of Income Tax Act, 1961) since the period of 4 years from the end of the relevant A.Y. had expired. He contended that reopening of assessment was not on the ground that full and true material facts were not disclosed but the only ground was that the depreciation was not admissible as claimed by the Assessee and in spite of the same, such was made admissible and there was omission in the earlier assessment made. He, therefore, submitted that the action can be said as barred by first proviso to Section 147 (of Income Tax Act, 1961).

6. Whereas, Mr.Mehta, learned counsel appearing for the respondent admitted that the objections were not disposed of before proceeding for reassessment. He is not in a position to dispute that the ground of notice under Section 147 (of Income Tax Act, 1961) read with the reasons recorded shows that it was on account of non-admissibility of the depreciation, the assessment was proposed to be reopened. The learned counsel for the revenue is not in a position to dispute the facts disclosed for the claim of depreciation but he submitted that such depreciation was not admissible as per the statutory provision and hence, it was made as basis for reopening of the assessment. Mr.Mehta, learned counsel is not in a position to show that whether any true and correct facts were not disclosed which lead to reopening of the assessment, even for claim of depreciation.

7. We may record that this Court today, in Special Civil Application No.18004 of 2014, had an occasion to consider the question of bar operating to the action under Section 147 (of Income Tax Act, 1961) and it was observed thus:-

“1. Rule. Mr. Mehta, learned Standing Counsel, waives notice of Rule. The matter is finally heard with the consent of the learned advocates appearing for both the sides.

2. The only question which may arise for consideration in the present matter is “Whether the bar of four years provided by first proviso of section 147 (of Income Tax Act, 1961) can be made applicable to the facts of the present case or not?

3. The relevant facts are that as per the petitioner, for the assessment year 20082009, the scrutiny was made under section 143(3) (of Income Tax Act, 1961) (hereinafter referred to as the “Act”) and the petitioner submitted detailed letter on various points connected with the return of income tax filed under section 139 (of Income Tax Act, 1961). On 18.11.2010, during the course of regular assessment, in reply to the notice under section 142(1) (of Income Tax Act, 1961), the Chartered Accountant of the petitioner, vide letter, had submitted various documents including the audit report and the details about the salary of the partners. On 28.12.2010, the assessing officer passed a scrutiny assessment order under section 143(3) (of Income Tax Act, 1961) and while passing the said order, the survey made on 22.08.2008 and other relevant aspects were considered and the order was passed.

4. On 17.01.2014, the assessing officer issued notice under section 148 (of Income Tax Act, 1961) informing the petitioner that the income has escaped assessment for the assessment year 20082009 and vide letter dated 01.04.2014, the respondent provided reasons recorded for reopening of the assessment. On 17.06.2014, the petitioner filed objections against the reasons and it was contended inter alia that full disclosure was made including the points on the basis of which the assessment is sought to be reopened and the period of limitation of four years expired was also contended by way of objection. On 10.10.2014 the respondent passed the order, whereby the objections filed by the petitioner were disposed of and the notice for reopening of the assessment was maintained. Under the circumstances, the present petition before this Court.

5. We have heard Mr.J.P. Shah, learned counsel appearing with M.J.Shah for the petitioner and Mr. Sudhir Mehta, for the respondent Revenue.

6. As such, apart from the aspect as to whether income escaped assessment, we find that one of the major point which may go to the root of the matter is the bar operating on the power of Revenue to reopen the assessment after the expiry of the period of four years from the end of the relevant assessment year. Section 147 (of Income Tax Act, 1961) upto first proviso which is relevant for the purpose of this petition reads as under:

“147. Income escaping assessment. If the Assessing Officer has reason to believe that any income chargeable to tax has escaped assessment for any assessment year, he may, subject to the provisions of sections 148 to 153, assess or reassess such income and also any other income chargeable to tax which has escaped assessment and which comes to his notice subsequently in the course of the proceedings under this section, or recompute the loss or the depreciation allowance or any other allowance, as the case may be, for the assessment year concerned (hereafter in this section and in sections 148 to 153 referred to as the relevant assessment year) : Provided that where an assessment under subsection (3) of section 143 (of Income Tax Act, 1961) or this section has been made for the relevant assessment year, no action shall be taken under this section after the expiry of four years from the end of the relevant assessment year, unless any income chargeable to tax has escaped assessment for such assessment year by reason of the failure on the part of the assessee to make a return under section 139 (of Income Tax Act, 1961) or in response to a notice issued under subsection (1) of section 142 (of Income Tax Act, 1961) or section 148 (of Income Tax Act, 1961) or to disclose fully and truly all material facts necessary for his assessment, for that assessment year”

7. Section 147 (of Income Tax Act, 1961) enables the AO to reopen the assessment subject to the provisions of sections 148 to 153 of the Act, but the first proviso to the very section 147 (of Income Tax Act, 1961) provides that no action shall be taken under this section (147) after the expiry of the period of four years from the end of the relevant assessment year, unless any income chargeable to tax has escaped assessment for such assessment year by the reason of failure on the part of assessee to disclose full and truly all material facts necessary for assessment for the respective assessment year.

8. The aforesaid shows that unless the case falls in the exceptional category of “failure to disclose fully and truly all material facts necessary for the assessment”, the action after the expiry of four years for reopening of the assessment is not permissible. As we are not required to examine other contingencies of failure, we do not deal with the same.

9. As per the learned counsel Mr.Shah for the petitioner, full and true disclosure of all material facts relevant to the reasons which is the ground for reassessment were disclosed before the AO at the time when the scrutiny of the assessment had taken place. He submitted that not only that but the audit report was also produced which included the remuneration to the partners from the disclosed item of Rs.74,90,834/and during the course of the assessment, this aspect is deemed to have been considered and the assessment order was passed. He submitted that once the petitioner succeeds to satisfy that full and true disclosures were made of the relevant material and thereafter, if the assessment order is passed, the bar of four years would apply. Apart from the aforesaid contention, as per Mr.Shah, it cannot be said that the income escaped the assessment and therefore section 147 (of Income Tax Act, 1961) cannot be invoked by the Department.

10. Whereas, Mr. Mehta, learned counsel appearing for respondent is not in a position to dispute the factual aspect that the true disclosure was made by the assessee for the remuneration paid to the partners and computed while computing the business income. He is also unable to dispute that the audit report showing the aforesaid details were produced.

11. In view of the above, we find no reason to believe that true and full disclosure was not made by the assessee to come out from the bar of four years as provided by first proviso to section 147 (of Income Tax Act, 1961). Once the bar operates upon the power by express statutory provision, the action can be said as without jurisdiction. If the action of issuance of notice is without jurisdiction, it would be a case for interference under Article 226 of the Constitution.

12. In view of the above, we find that the impugned action under section 147 (of Income Tax Act, 1961) and consequently issuance of notice under section 148(AnnexureE) (of Income Tax Act, 1961) including disposal of the objection dated 10.10.2014 (AnnexureI) may not stand in the eye of law. Hence, they are quashed and set aside.

13. The petition is allowed to the aforesaid extent. Rule made absolute accordingly. Considering the facts and circumstances, no order as to costs.”

8. In our view, when even as per the respondent, all the relevant facts were disclosed and produced at the time of earlier assessment pertaining to the claim of depreciation and when there is no ground for non-discloser of true and correct relevant material, bar of 4 years, as per first proviso to Section 147 (of Income Tax Act, 1961), would apply and the action under Section 147 (of Income Tax Act, 1961) for reopening of the assessment could be said as without jurisdiction and the action cannot stand in the eye of law.

9. Apart from above, there is considerable force in the contention of the learned counsel for the petitioner that in the similar fact situation, this Court in the case of General Motors India (P) Ltd. (supra) has found that if the objections are not decided to the reasons for opening of reassessment and the department has proceeded for reassessment, the assessee would be well within his right to invoke the jurisdiction of this Court under Article 226 of the Constitution. As the mandatory procedure is not followed for disposal of the objection before proceeding with reassessment, initiation of the action as well as the subsequent order for reassessment would be required to be quashed.

10. In view of the above, examining the matter in either way, we find that the action for reopening of assessment under Section 147 (of Income Tax Act, 1961) was barred and even the action for non- disposal of objection and subsequent order, which is impugned in the present petition, would also be required to be quashed and set aside. Hence, they are quashed and set aside.

11. The petition is allowed to the aforesaid extent. Rule is made absolute. Considering the facts and circumstances, no order as to costs.

(JAYANT PATEL, J.)

(S.H.VORA, J.)

×

Similar Ripples

Questions

Court Quashes Reassessment Order Due to Procedural Lapse and Time Bar

Write your CommentSimilar Posts

Generic

- Reportdata/4086.pdf