Court Quashes Tax Attachment on Bona Fide Purchasers' Land, Citing Invalid Proc…

Full News

Court Quashes Tax Attachment on Bona Fide Purchasers' Land, Citing Invalid Proceedings

Court Quashes Tax Attachment on Bona Fide Purchasers' Land, Citing Invalid Proceedings

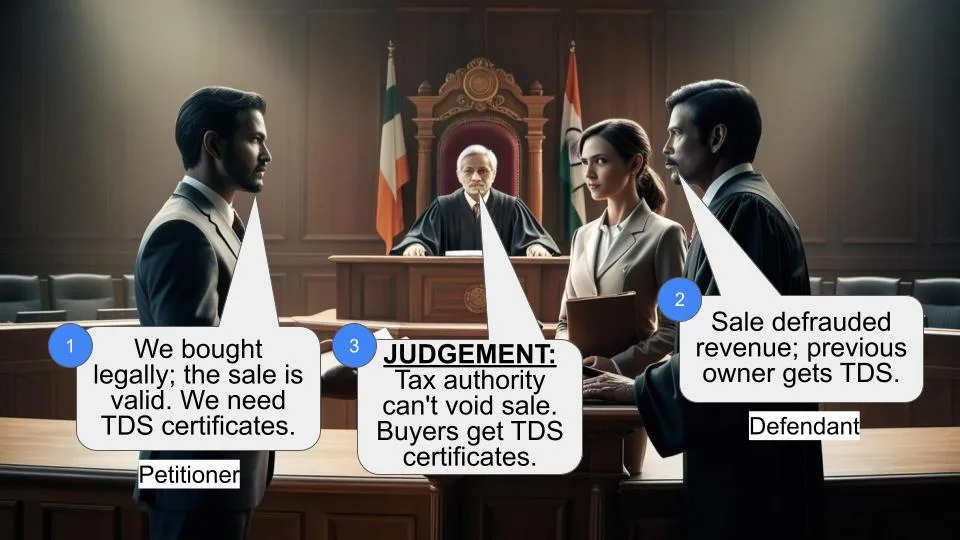

This case involves petitioners who purchased land from Ram Niwas, who had previously bought it from Chandrawali with an Income Tax clearance certificate. The Income Tax Department later tried to attach this land for Chandrawali's tax arrears. The court ruled in favor of the petitioners, quashing the attachment order and the proceedings under Section 281(1) (of Income Tax Act, 1961).

Get the full picture - access the original judgement of the court order here

Case Name:

Smt. Sushila & Ors. Vs Union of India & Ors. (High Court of Punjab & Haryana)

CWP No.16812 of 2006

Date: 24th January 2008

Key Takeaways:

1. Income Tax Officers cannot declare property transfers void under Section 281 (of Income Tax Act, 1961).

2. Bona fide purchasers are protected if they buy property with proper clearance and without notice of pending proceedings.

3. The Income Tax Department must pursue civil remedies to challenge property transfers they believe are fraudulent.

Issue:

Can the Income Tax Department attach and declare void a property transfer made with prior permission and an Income Tax clearance certificate, when the property is now owned by bona fide purchasers?

Facts:

1. Chandrawali sold land to Ram Niwas on 22.7.1999 with an Income Tax clearance certificate.

2. The petitioners later purchased this land from Ram Niwas.

3. The Income Tax Department initiated proceedings under Section 281(1) (of Income Tax Act, 1961) and issued an attachment order on 7.6.2004 against the petitioners' land.

4. The Department claimed Chandrawali had pending tax liabilities and the transfer was fraudulent.

5. The petitioners challenged this action through a writ petition.

Arguments:

Petitioners:

- They were bona fide purchasers who bought the land after due diligence.

- The sale was made with the Income Tax Department's permission via a clearance certificate.

- The Income Tax Officer has no power to declare transfers void under Section 281 (of Income Tax Act, 1961).

Income Tax Department:

- There's no estoppel against statute, and the transfer is void as per records.

- The clearance certificate doesn't validate the transfer under Section 281 (of Income Tax Act, 1961).

- Proceedings under Section 148 (of Income Tax Act, 1961) were pending against Chandrawali before the sale.

Key Legal Precedents:

1. Sancheti Leasing Company Ltd. and another vs. Income Tax Officer and another 246 ITR 814 (Madras High Court):

Income Tax Officers lack the power to declare transfers void.

2. R. Vijay Kumar vs. Asstt. Commissioner of Income Tax (1999) 190 ITR 245 (Madras High Court):

Section 230A (of Income Tax Act, 1961) permission indicates no pending proceedings, precluding Section 281 (of Income Tax Act, 1961) proceedings.

Judgement:

The court ruled in favor of the petitioners:

1. Quashed the proceedings under Section 281(1) (of Income Tax Act, 1961) and the attachment order dated 7.6.2004.

2. Held that the Income Tax Officer had no power to declare the sale void.

3. Noted that the Department's rights could only be decided by a civil court.

4. Left it open for the Department to pursue remedies if they succeed in their pending civil suit.

FAQs:

Q1: What protection does an Income Tax clearance certificate offer to property buyers?

A1: It indicates no pending tax liabilities at the time of sale and can protect bona fide purchasers from future attachment orders.

Q2: Can the Income Tax Department still pursue recovery of taxes in this case?

A2: Yes, but only if they succeed in their pending civil suit to declare the original sale deed as null and void.

Q3: What's the significance of Section 281 (of Income Tax Act, 1961) in this case?

A3: It deals with certain transfers being void, but the court clarified that Income Tax Officers can't unilaterally declare transfers void under this section.

Q4: How does this judgment affect future property transactions?

A4: It emphasizes the importance of obtaining proper clearances and conducting due diligence for property buyers, while also limiting the powers of Income Tax Officers in declaring transfers void.

Q5: What should taxpayers do if they receive similar attachment orders?

A5: They should consider legal remedies, such as filing a writ petition, especially if they are bona fide purchasers with proper documentation.

1. By way of the present writ petition the petitioners seek the quashing of proceedings under Section 281(1) (of Income Tax Act, 1961) (hereinafter referred to as the ‘Act’) and the consequential act i.e. attachment order dated 7.6.2004 (Annexure P-1) passed by respondent No.3 under Rule 48 of the second Schedule to the Income Tax Act, 1961 alleging the same as illegal and arbitrary on the part of the respondents.

2. As per the averments made in the writ petition, the petitioners took the property on 99 years' lease from one Ram Niwas s/o Sh. Ram Chander son of Lachhman, resident of Mohalla Sainian, Hisar Tehsil and Distt. Hisar who had purchased this property from one Chandrawali widow of late Shri Nand Ram, resident of Mohalla Sainian near Saini Athai, Hisar. In pursuance of the registered lease deed and with a view to get permanent and perpetual title over the said property three sale deeds were executed in favour of the petitioners on 4.3.2003, 4.3.2003 and 13.6.2003 for the aforementioned property at a price of Rs.4.5. lacs per acre.

3. It is the case of the petitioners that at the time of buying the aforementioned property they had made enquiries from the office of the Registrar and had verified the antecedents and purchased the property by paying all the statutory dues of stamp duty etc. It is also the case of the petitioners that in order to get the finance and to further check the clear title of the property, the petitioners had also seen the Income Tax Clearance Certificate issued on 22.7.1999 by the Income Tax Department, Hisar under Section 230A(i) (of Income Tax Act, 1961) before the Sub Registrar, Hisar permitting the registration of the sale deed of the land in question by Smt. Chandrawali to Sh. Ram Niwas. The Income Tax Clearance Certificate was a pre-requisite of the law for the execution of the sale deed by Smt. Chandrawali in favour of Sh. Ram Niwas. This Income Tax Clearance Certificate contained the full identity of the seller Smt. Chandrawali, her address as well as full particulars of the buyer Ram Niwas and complete description of the land required to be sold and also the rate and the sale price of the land in question. Thus, the sale deed of the land in question of Smt. Chandrawali to Sh. Ram Niwas was executed with the permission of the Income Tax Department, Hisar and was registered at Serial No.2934 dated 22.7.1999. Mutation was also sanctioned by the Revenue Department in favour of Ram Niwas vide order dated 7.7.2000 by the Assistant Collector, Grade II, Hisar. Thus, the petitioners found that the title of Ram Niwas was free from all encumbrances, marketable, undisputed and thereafter, the petitioners bought the land with the help of loans sanctioned and provided by The Haryana State Cooperative Agricultural and Rural Development Bank, Hisar.

4. It is further the case of the petitioners that they were shocked to know on 3.8.2004 that the aforementioned property of the petitioners had been attached in terms of the order dated 7.6.2004 (Annexure P-1) issued by the Tax Recovery Officer, Income Tax Department, Hisar to the Tehsildar, Hisar by invoking the provisions of Section 281 (of Income Tax Act, 1961). Vide this order the Tax Recovery Officer, Income Tax Department, Hisar has also intimated the Tehsildar Hisar that the transfer of land dated 22.7.1999 is null and void and the present owners be not allowed to part with their possession over the properties. It is the case of the petitioners that on coming to know about the attachment order Annexure P-1 they immediately submitted the representation dated 11.8.2004 to the respondents-authorities for setting aside the said order dated 7.6.2004 vide which the land of the petitioners has been attached and further for removal of the attachment of this land from the provisions of Section 281 (of Income Tax Act, 1961). In the said representation, the petitioners have clearly stated that they are the bona fide purchasers of the land in question for adequate consideration and without notice and further that before buying the land in question they had examined the original sale deeds and Income Tax Clearance Certificate dated 22.7.1999 issued by the Department in favour of Sh. Ram Niwas and found it to be in order. It was also stated by the petitioners that there is no tax liability against them and the Income Tax Department is estopped by its own act and conduct from passing the impugned order, firstly because they did not pass any order for provisional attachment of the land in question before initiating the alleged proceedings for assessment of Income Tax liability of Smt. Chandrawali as provided under Section 281(B) (of Income Tax Act, 1961) and secondly, because the Department itself issued the Income Tax Clearance Certificate on 22.7.1999 to Smt. Chandrawali and permitted her to sell the land in question to Ram Niwas. It is also stated by the counsel for the petitioners that the proviso to Section 281 (of Income Tax Act, 1961) covers the case of the petitioners as the land in question was purchased for adequate consideration and without notice of the pendency of proceedings against Chandrawali and with the previous permission of Assessing Officer. The petitioners have further alleged that they have received no reply in pursuance of their representation dated 11.8.2004 submitted to the respondents-authorities and instead the respondent-Department filed a civil suit in the Civil Court, Hisar against the petitioners for declaration to the effect that the Department is entitled to attach and sell the agricultural land for the recovery of demand of income tax assessed against Nand Ram deceased and Smt. Chandrawali who is the legal heir/representative as these sales and lease are void, illegal, fraudulent and the same have been made to defraud the Tax Recovery Officer and as such there is no binding effect on the rights of the respondents for the purpose of recovery of demand of Income Tax assessed under the Income Tax Act, 1961 by way attachment and the sale of the property till the satisfaction of all the dues, therefore, all the transfers made by Smt. Chandrawali be declared void.

5. Since the petitioners are aggrieved of the initiation of proceedings under Section 281 (of Income Tax Act, 1961) and the order of attachment thus, they have filed the present writ petition.

6. The respondents have contested the writ petition by filing written statement stating therein that the there is no estoppel against the statute as the transfer of agricultural land in question is void as is borne out from the record and moreover issuance of Income Tax Clearance Certificate under Section 230 (of Income Tax Act, 1961) A of the Act does not make the transfer as valid in terms of provisions of Section 281 (of Income Tax Act, 1961). The writ petition has also been contested on the ground that it suffers from the vice of concealment of facts as the proceedings under Section 148 (of Income Tax Act, 1961) against Smt. Chandrawali were pending before the sale was effected and later on assessment was finalised against her for different assessment years which has become final and the total outstanding demand against Smt. Chandrawali as per record is at Rs.1,60,48,610/- which has not been paid and this fact alone was sufficient to oust the petitioners. The Department has also relied upon the statement of Smt. Chandrawali which was recorded on 23.8.2002 in which she has stated that she is an illiterate lady and after the death of her husband on 20.1.1999 some people had fraudulently got the said land transferred in their favour without making any payment. Thus, it has been stated by the respondents-authorities that the Tax Recovery Officer invoked the provisions of Section 281 (of Income Tax Act, 1961) and declared the transfer of land as null and void and issued an order of attachment of immovable property of Smt. Chandrawali vide notice dated 14.7.2003 prohibiting and restraining the further transfer of properties and later on an order of attachment dated 7.6.2004 in respect of the said land was also issued to Tehsildar, Hisar requesting him not to allow the present owner of the properties to part with the possession of these properties as the transfer/sale dated 22.7.1999 has been treated as null and void. It has been admitted that the Department has filed a Civil Suit in the Civil Court at Hisar for declaring the sale of immovable property made on 22.7.1999 by Smt. Chandrawali in favour of Ram Niwas as void and the same is pending and therefore the Tax Recovery Officer/Income Tax Officer is entitled to attach and sell the agriculture land which has been fraudulently transferred vide sale deed dated 22.7.1999 by Smt. Chandrawali as the so- called transfer made to defraud the tax recovery.

7. The petitioners have filed replication controverting the plea taken by the respondent-Department on facts and law by stating that the order of attachment issued by the respondent- Department wherein the authorities have acted beyond powers vested in them by law, affecting the petitioners was passed on 7.6.2004 and therefore the writ petition has been filed within the period of limitation. The plea of concealment of facts as taken by the respondent-Department was also contested by stating that no proceedings under Section 148 (of Income Tax Act, 1961) was ever initiated against the petitioners and the same were allegedly started against Smt. Chandrawali who had sold the property to Ram Niwas from whom the property has been purchased by the petitioners.

8. We have heard learned counsel for the parties and perused the record.

9. Mr. Akshay Bhan, learned counsel for the petitioners, has vehemently argued that the Income Tax Officer is not vested with the powers to declare any such transaction of sale as void under any of the provision of Income Tax Act much less in terms of Section 281 (of Income Tax Act, 1961) of the Income Tax, 1961. Thus, the action of the Income Tax Officer treating the transfer of land in question by Smt. Chandrawali to Ram Niwas as void and then to attach the same cannot be sustained in law as the Assessing Authority was not vested with such powers. For this contention, counsel for the petitioners has relied upon the judgement of the Madras High Court reported as Sancheti Leasing Company Ltd. and another vs. Income Tax Officer and another 246 ITR 814. Learned counsel has also argued that the provisions of Section 230 (of Income Tax Act, 1961) A of the Act cannot be divorced from the provisions of Section 281 (of Income Tax Act, 1961) as Section 230 (of Income Tax Act, 1961) A of the Act is more a safeguard vis-a-vis Section 281 (of Income Tax Act, 1961) and this is specifically so in the case of the petitioners, inasmuch as the permission granted under Section 230A (of Income Tax Act, 1961) shows that no proceedings were pending on that day and therefore, no proceedings under Section 281 (of Income Tax Act, 1961) would lie as held by the Madras High Court in the case of R. Vijay Kumar vs. Asstt.

Commissioner of Income Tax (1999) 190 ITR 245. It has been also argued by Mr. Akshay Bhan, counsel for the petitioner that the Department has already filed a civil suit declaring the sale deed dated 22.7.1999 executed by Smt. Chandrawali in favour of Ram Niwas as null and void which is pending and the title or rights of the Department qua the petitioners can only be decided in the said civil suit. Thus, in view of this fact alone the proceedings initiated by the respondent-Department under Section 281 (of Income Tax Act, 1961) and issuance of notice Annexure P-1 cannot be sustained.

10. On the other hand, Mr. Yogesh Putney, learned counsel for the revenue, has defended the action of the respondent-Department.

11. We find considerable force in the arguments raised by counsel for the petitioners. A perusal of Annexure P-3 i.e. Income Tax Clearance Certificate issued by the Department in favour of Smt. Chandrawali for the sale of land in question to Sh. Ram Niwas (i.e. from whom the petitioners have purchased the land in question) clearly indicates that no liability was outstanding against Smt. Chandrawali on the date of issuance of the said Income Tax Clearance Certificate. It is also not contested by the Department that the petitioners are the bona fide purchasers of the land in dispute. They have purchased the land for a consideration and after making due enquiry about the clear title of the vendor. Section 281 (of Income Tax Act, 1961) sub- section (1) provides that if during the pendency of any proceeding under this Act or after the completion thereof, but before the service of notice under Rule 2 (of Income Tax Rules, 1962) of the Second schedule, any assessee creates a charge on or parts with the possession of, any of his assets in favour of any other person, such charge or transfer shall be void as against any claim in respect of any tax or any other sum payable by the assessee as a result of the completion of the said proceeding. Proviso to Section 281(1) (of Income Tax Act, 1961) provides that any such transaction as mentioned under Section 281(1) (of Income Tax Act, 1961) shall not be void if it is made for adequate consideration and without notice of the pendency of the said proceedings or as the case may be, without notice of such tax or other sum payable by the assessee or with the previous permission of the Assessing Officer. In the present case also, on 22.7.1999, when Smt. Chandrawali transferred the land in question to Sh. Ram Niwas no tax liability was pending against her and prior to that, only a notice under Section 148 (of Income Tax Act, 1961) for assessment proceedings was issued to her and moreover the said sale deed was executed with the permission of the Assessing Officer. Moreover, the Department could not produce any material to show that the sale/transfer of land in question to Sh. Ram Niwas (predecessor-in-interest of the petitioners) was not for adequate consideration as neither the vendee nor the assessee had any notice of the pendency of such proceedings or of tax liability on the part of Smt. Chandrawali to the Department at the time of the transfer in question for which the prior permission of the Assessing Officer was also obtained by taking Income Tax Clearance Certificate. It is clear from the Income Tax Clearance Certificate dated 22.7.1999 in which full description of the property in question was given and it has been specifically mentioned that no tax liability was pending against the seller. There is no provision under the Income Tax Act under which the Income Tax Officer can declare the sale/transfer of land in question to the petitioner as void and such rights of the department qua the petitioners can only be decided by a competent Court of civil jurisdiction and admittedly, the civil suit filed by the Department for declaring the sale deed dated 22.7.1999 by Smt. Chandrawali in favour of Sh. Ram Niwas (predecessor in-interest of the petitioners) is still pending and the Civil Court is seized of the matter .

12. In view of these facts, the initiation of proceedings by the respondent-Department under Section 281(1) (of Income Tax Act, 1961) and issuance of attachment certificate of land in question vide Annexure P-1 against the petitioners is bad in law. Hence, the proceedings under Section 281(1) (of Income Tax Act, 1961) and attachment certificate dated 7.6.2004 (Annexure P-1) issued against the petitioners are hereby quashed. However, it will be open to the Department to pursue its remedy, if any, against the land in question of the petitioners for recovery of alleged tax against Smt. Chandrawali, in case the Department succeeds in the Civil Suit filed for declaring the sale deed dated 22.7.1999 as null and void.

13. With these observations, the present writ petition is allowed.

(RAKESH KUMAR GARG)

JUDGE

(SATISH KUMAR MITTAL)

JUDGE

January 24, 2008

×

Similar Ripples

Questions

Court Quashes Tax Attachment on Bona Fide Purchasers' Land, Citing Invalid Proceedings

Write your CommentSimilar Posts

Generic

- Reportdata/4956.pdf