Full News

Court Voids Tax Authority's Nullification of Property Transfer, Upholds Buyers' Rights

Court Voids Tax Authority's Nullification of Property Transfer, Upholds Buyers' Rights

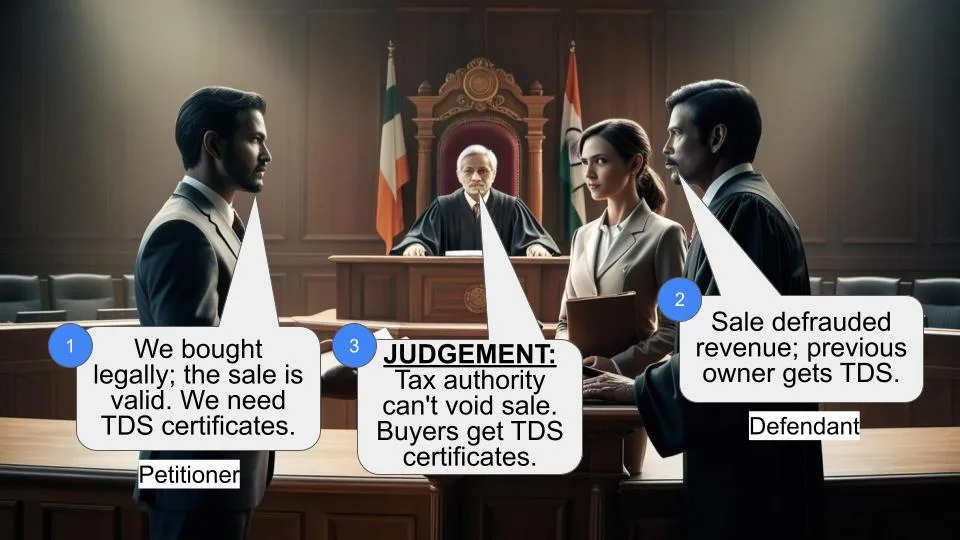

This case involves a dispute between property buyers (the petitioners) and tax authorities over the validity of a property transfer and the issuance of TDS (Tax Deducted at Source) certificates. The court ruled in favor of the buyers, declaring the tax authority's order nullifying the property transfer as illegal and directing the bank to issue TDS certificates to the buyers.

Get the full picture - access the original judgement of the court order here

Case Name:

Shamim Bano G. Rathi & Anr. Vs Oriental Bank of Commerce Ltd. & Ors. (High Court of Bombay)

Writ Petition No. 1969 of 2007

Date: 5th December 2007

Key Takeaways:

1. Tax authorities cannot unilaterally declare property transfers void under Section 281 (of Income Tax Act, 1961).

2. Only a competent civil court can declare a transfer fraudulent under Section 281 (of Income Tax Act, 1961).

3. TDS certificates should be issued to the current property owners, not the previous owners, even if there's an ongoing tax dispute.

Issue:

Can tax authorities declare a property transfer null and void under Section 281 (of Income Tax Act, 1961) without a civil court order, and who is entitled to receive TDS certificates in such situations?

Facts:

1. The petitioners purchased a property from Respondent No. 5 on July 30, 2002, through a registered deed of sale.

2. At the time of sale, there were pending income tax proceedings against Respondent No. 5.

3. Respondent No. 5 had taken a loan from Respondent No. 1 (Oriental Bank of Commerce) and mortgaged the property.

4. The tax authorities declared the sale deed null and void on September 21, 2004.

5. The bank continued to issue TDS certificates to Respondent No. 5 instead of the petitioners.

Arguments:

Petitioners:

- They were bona fide purchasers of the property.

- The tax authorities had no jurisdiction to declare the sale void.

- They were entitled to TDS certificates as the new property owners.

Tax Authorities:

- The transfer was made to defraud the revenue and should be declared void under Section 281 (of Income Tax Act, 1961).

Key Legal Precedents:

1. Tax Recovery Officer v. Gangadhar Viswanath Ranade (Decd.) (1998) 234 ITR 188 (SC): The Supreme Court held that the tax department must file a suit in a civil court to declare a transfer void under Section 281 (of Income Tax Act, 1961).

2. Ms. Ruchi Mehta & Ors. v. Union of India & Ors. (2007) 294 ITR 614 (Bom): The Bombay High Court affirmed that Section 281 (of Income Tax Act, 1961) doesn't provide any adjudicatory machinery, and proceedings must be taken before a competent civil court.

Judgement:

1. The court declared the tax authority's order nullifying the sale deed as illegal and without jurisdiction.

2. The petitioners were recognized as the rightful owners of the property until a competent civil court decides otherwise.

3. The bank (Respondent No. 1) was directed to rectify the TDS certificates and issue them in favor of the petitioners.

4. The court quashed the attachment order dated November 18, 2003, and subsequent demand notices.

5. The petitioners were given a six-month restriction on transferring or creating third-party rights on the property to allow the tax department to approach a civil court if needed.

FAQs:

1. Q: Why couldn't the tax authorities declare the sale void?

A: Only a competent civil court has the authority to declare a transfer fraudulent under Section 281 (of Income Tax Act, 1961).

2. Q: What happens to the TDS certificates issued to the previous owner?

A: The bank has been directed to rectify the TDS certificates and issue them in favor of the new owners (the petitioners).

3. Q: Can the tax department still challenge the property transfer?

A: Yes, but they must file a suit in a civil court to have the transfer declared void.

4. Q: What's the significance of the six-month restriction on the property?

A: It gives the tax department time to approach a civil court if they wish to challenge the transfer, while protecting the petitioners' ownership rights.

5. Q: How does this judgment impact similar cases?

A: It reinforces the principle that tax authorities cannot unilaterally void property transfers and emphasizes the importance of following proper legal procedures in such disputes.

1. Rule. Heard forthwith.

2. It is the case of the petitioners that by a registered deed of sale dated 30.7.2002 they purchased the premises from respondent no.5. Admittedly, there were proceedings pending under the Income Tax Act against respondent no.5 on that date. The order of attachment under Section 226(3) (of Income Tax Act, 1961) made on 19.6.2002 was lifted sometime in July-2002. Admittedly, on the date of the sale of the property there was no order of attachment. The order of attachment was subsequently passed on 22.10.2003.

3. Respondent no.5 had taken a loan from respondent no.1 and to secure the loan had created a mortgage in favour of respondent no.1. Respondent no.5 has also created leave and license in favour of respondent no.1. The license amounts were to be adjusted against the loan amount advanced by respondent no.1 to respondent no.5.

. Though the petitioners had served the notice of attornment on respondent no.5 and though the petitioners were showing the income received from respondent no.1 in their returns, respondent no.1 continued to issue TDS certificate in favour of respondent no.5. According to the respondent no.1 this was done considering the order passed by respondent no.3 under Section 226(3) (of Income Tax Act, 1961). Counsel for respondent no.1 however, states that they have no objection in issuing the TDS certificate in favour of the petitioners and accordingly to carry out rectification in the TDS certificate in favour of the petitioners. By October-2007 the loan amount payable by respondent no.5 in favour of respondent no.1 has been re-paid. The sale consideration in so far as sale deed between respondent no.1 and respondent no.5 apart from the consideration was also the liability under the mortgage. In other words, though the petitioners had become the owners of the property, the license fee received from respondent no.1 was to be adjusted against the loan dues of respondent no.5.

4. The petition as earlier filed in this Court was only in the matter of issuance of TDS certificate in the name of the petitioner. In the reply filed by respondent no.1 reference was made to letter dated 4.11.2004 by Tax Recovery officer Range 2(3) to Respondent no.1 wherein it was recorded that the sale of the property by agreement dated 30.7.2002 by respondent no.5 was declared to be null and void by the department by order dated 21.9.2004. Chamber summons was taken out for amendment of the petition and the petition was amended to include amongst other reliefs not to give effect to the orders dated 21.9.2004 and 18.11.2003.

5. The first question that we are called upon to consider is whether it was open for the assessing officer to declare the sale deed between respondent no.5 and the petitioners as null and void, considering section 281 (of Income Tax Act, 1961). In our opinion, the issue is no longer resintegra having been answered in the judgment of the Supreme Court in Tax Recovery Officer v.Gangadhar Viswanath Ranade (Decd.) reported in 234 ITR 188 where the Supreme Court held that if the department finds that a property of the assessee is transferred by him to a third party with the intention to defraud the Revenue, it will have to file a suit under rule 11(6) (of Income Tax Rules, 1962) to have the transfer declared void under section 281 (of Income Tax Act, 1961).

6. On behalf of Revenue, learned Counsel submits that there is distinction between the ratio of that judgment and the facts in issue in the present case as in the instant case it is the assessing officer who has declared the transfer to be null and void whereas in the case of Gangadhar V.Ranade (decd.) (supra) it was the tax officer who had done so. The judgment in Gangadhar V.Ranade (deceased) had come up for consideration before us in Ms.Ruchi Mehta & Ors. v. Union of India & Ors. reported in [2007] 294 ITR 614 (Bom). On considering the said judgment, we have taken a view that section 281 (of Income Tax Act, 1961) does not prescribe any adjudicatory machinery for deciding any question which may arise under it. In order to declare a transfer fraudulant under Section 281 (of Income Tax Act, 1961), appropriate proceedings have to be taken before the competent civil Court. The issue therefore, where the order was passed by the Tax recovery officer or A.O. is immaterial.

7. Learned Counsel for assessee further contends that they were bonafide purchasers and the sale cannot be said to be null and void. It is also contended that no opportunity was given to them before the said order was passed and considering the judgment of this Court (Ms.Ruchi Mehta & Ors.) (supra) the order must be set aside on that ground also. We need not answer these questions at this stage in view of the order to be passed.

. In so far as first contention, we are of the opinion that the order declaring the sale deed dated 30.7.2002 as null and void was an order without jurisdiction and consequently has to be set aside. The petitioners in the absence of any declaration continue to be the owners of the property, till such times a competent civil Court passes any appropriate order.

8. Let us come to next issue of the TDS certificate not being issued in the name of the petitioners. The learned Counsel points out that infact, the assessing officer had himself addressed a letter that the TDS certificate should be issued in favour of the petitioners by respondent no.1. The assessing officer accepted the return filed in the matter of rent but did not grant the benefit in the absence of TDS certificate. Thereafter a demand was made on the petitioners consequence to TDS certificate not being produced. Though the petitioners were owners of the property and were entitled for rent from respondent no.1, respondent no.1 on account of the service of notice by respondent nos.2 to 3 continued to issue the TDS certificate in favour of respondent no.5.

9. In our opinion, considering that the petitioners’ contention to be the owners of the property and the rent was payable by respondent no.1 to the petitioners, the TDS certificate has to be issued in favour of the petitioners as we have held that the order declaring the sale to be null and void is itself illegal and without authority of law. In other words, after the purchase of the property by the petitioners on 30.7.2002 respondent no.1 was bound to issue TDS certificate in favour of the petitioners. The respondent no.1 is therefore, directed to rectify the TDS certificate issued by respondent no.1 in favour of respondent no.5 and issue it in favour of the petitioners.

10. Considering this position, in our opinion, the demand made by respondent nos.2 to 3 on the petitioners would be without jurisdiction. It will however, be open for the petitioners to place this material before the competent officer and the competent officer will take such steps in law including withdrawal of the demand considering that the demand was made, as the TDS certificate was not produced by the petitioners. Hence, following order :- O R D E R

1. The sale deed dated 30.7.2002 in the absence of a declaration by a civil court that it is null and void and as observed by the Supreme Court in Tax Recovery Officer v. Gangadhar Viswanath Ranade (Decd.) is legal and valid ;

2. As the sale is legal and valid, respondent no.1 was bound to issue the TDS certificate in favour of the petitioners from 30.7.2002 onwards and thereafter. The respondent no.1 is therefore, directed to rectify the TDS certificate and accordingly, issue the same in the name of the petitioners herein ;

3. Consequently the order of attachment dated 18.11.2003 is quashed and set aside and as a consequence the A.O. is directed not to proceed on the basis of the demand notices dated 29.3.2006 and 27.11.2006. It will be open for the petitioners-assessees, based on the rectified TDS certificate to move the A.O. for re-call of the said demand notices ;

4. For a period of six months from today the petitioners will not transfer, alienate or create any third party rights in respect of the suit property to enable the department to move the civil Court and to take the appropriate orders therefrom.

5. Rule made absolute in the above terms.

(R.S.Mohite,J) (F.I.Rebello,J)

×

Similar Ripples

Questions

Court Voids Tax Authority's Nullification of Property Transfer, Upholds Buyers' Rights

Write your CommentSimilar Posts

Generic

- Reportdata/5108.pdf