Court Remands Case for Fresh Adjudication on Tax Exemption Approval

Full News

Court Remands Case for Fresh Adjudication on Tax Exemption Approval

Court Remands Case for Fresh Adjudication on Tax Exemption Approval

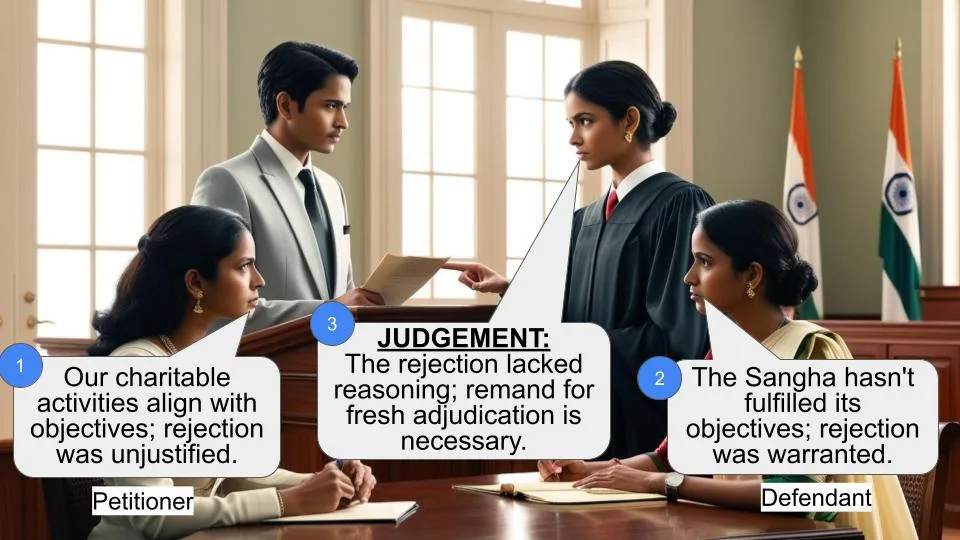

The case involves the Sri Narayana Guru Prasaditha Sangha and the Commissioner of Income Tax. The dispute centers around the rejection of the Sangha's application for the continuance of tax exemption approval under Section 80G (of Income Tax Act, 1961). The court found that the rejection lacked sufficient reasoning and remanded the case for fresh adjudication.

Get the full picture - access the original judgement of the court order here

Case Name:

Sri Narayana Guru Prasaditha Sangha vs. Commissioner of Income Tax (High Court of Karnataka)

ITA No. 687 of 2009

Date: 14th July 2015

Key Takeaways:

- The court emphasized the need for a detailed and reasoned order when rejecting applications for tax exemptions.

- The case highlights the importance of examining whether the activities of a trust fulfill its charitable objectives.

- The decision underscores the procedural requirements under Rule 11AA (of Income Tax Rules, 1962) for granting approval under Section 80G (of Income Tax Act, 1961).

Issue

Was the rejection of the Sangha's application for continuance of tax exemption under Section 80G (of Income Tax Act, 1961) justified?

Facts

- The Sri Narayana Guru Prasaditha Sangha, a registered society, had previously been granted tax exemption under Section 80G (of Income Tax Act, 1961).

- The Sangha applied for the continuance of this approval, which was proposed to be rejected by the Commissioner.

- The rejection was based on the alleged failure to fulfill the charitable objectives of the trust.

Arguments

- For the Sangha: The Sangha argued that the rejection was unjustified as it had undertaken activities like constructing a community hall and providing medical treatment, which aligned with its charitable objectives.

- For the Commissioner: The Commissioner contended that the Sangha had not carried out its objectives adequately, justifying the rejection of the application.

Key Legal Precedents

- Section 80G (of Income Tax Act, 1961): Governs the approval for tax exemptions for charitable institutions.

- Rule 11AA (of Income Tax Rules, 1962): Outlines the procedural requirements for granting approval under Section 80G (of Income Tax Act, 1961), including the need for a reasoned order when rejecting applications.

Judgement

The court set aside the previous orders rejecting the Sangha's application due to a lack of detailed reasoning. It remanded the case back to the Commissioner for fresh adjudication, instructing that the application be examined on its merits and in accordance with the law.

FAQs

Q1: What was the main reason for the court's decision?

A1: The court found that the rejection of the application lacked sufficient reasoning and did not adequately consider the Sangha's activities.

Q2: What does this mean for the Sangha?

A2: The Sangha's application will be reconsidered by the Commissioner, who must provide a detailed and reasoned decision.

Q3: How does this case impact other charitable institutions?

A3: It reinforces the need for detailed reasoning in decisions regarding tax exemption approvals, ensuring that charitable activities are properly evaluated.

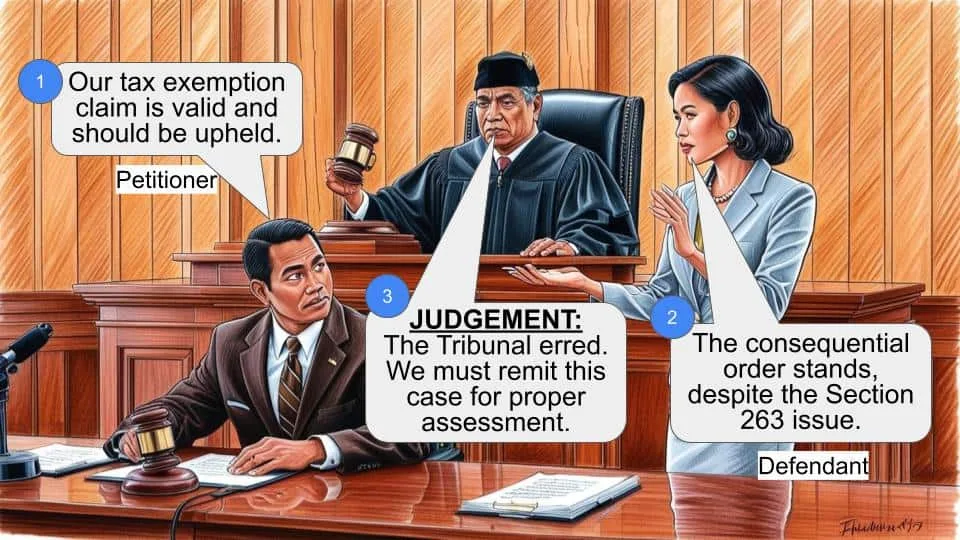

1. Assessee has filed this appeal challenging the correctness and legality of the order passed by Income Tax Appellate Tribunal, Bangalore Bench ‘B’,

Bangalore dated 29.05.2009 in ITA No.4/Bang/2009 whereunder appeal filed by the assessee questioning the order of Commissioner for Income Tax, Mangalore

who had rejected the assessee’s application filed under Section 80G (of Income Tax Act, 1961) (for short ‘Act’) came to be affirmed.

2. Appellant (hereinafter referred to as ‘assessee’) is a society registered under the Karnataka Societies Registration Act, 1960. It was granted

registration under Section 12A (of Income Tax Act, 1961) and also approval under Section 80G(5)(vi) (of Income Tax Act, 1961) with effect from 17.02.2004 to 31.03.2005. Thereafter, continuation

of the approval granted under Section 80G(5)(vi) (of Income Tax Act, 1961) was granted with effect from 01.04.2005 to 31.03.2008. On an application made for continuance

of approval on 06.03.2008, it was proposed to be rejected by the respondent and as such, notice came to be issued which was duly replied by the assessee. Thereafter, application for continuance of recognition came to be rejected by the respondent. Assessee unsuccessfully challenged the same before Tribunal and as such, present appeal has been presented to this Court.

3. We have heard the arguments of Smt.

Jineetha Chatterjee, learned Advocate appearing on

behalf of Sri S Parthasarathy for appellant – assessee

and Sri E.I.Sanmathi, learned Advocate appearing for

Respondent – Revenue.

4. It is the contention of Smt Jineetha

Chatterjee , learned Advocate appearing for the

appellant - assessee that respondent was not justified

in rejecting the application for continuance of

recognition granted to appellant under Section

80G(5)(vi) of the Act without examining as to whether

aims and objects of the assessee – society had been

fulfilled and charitable object with which it was

formed has been achieved or not and as such, she

contends that order of the Commissioner is

erroneous. She would also contend that

Commissioner as well as Tribunal erred in not

considering the fact that assessee – Trust had not

carried on any activity which was hit by proviso to

Section 2(15) (of Income Tax Act, 1961) and reply given to the

respondent indicated that donations which had been

received by the assessee had been utilised for the

purpose envisaged under the objects of the Trust and

its fulfillment. Non-consideration of said vital

evidence available on record by the respondent has

resulted in miscarriage in the administration of

justice. Hence, she prays for answering the

substantial questions of law formulated in the appeal

memorandum in favour of the assessee and against

the revenue.

5. Per contra, Sri E.I.Sanmathi, learned

Advocate appearing for the revenue would support

the orders passed by the authorities and contends

that assessee – Trust having obtained registration

under Section 12A (of Income Tax Act, 1961) on 17.02.2004, had not

carried out the object for which Trust was established

even after lapse of four years and as such, rejection of

renewal is just and proper and as such, he prays for

dismissing the appeal by answering the substantial

questions of law in favour of the revenue.

6. This Court, vide order dated 21.10.2009

has admitted the appeal to consider the following

substantial question of law:

“(a) Whether the Tribunal was

justified in alleging that, mere

construction of a building for the

purpose of carrying out of

activities for the advancement of

any objects of general public

utility like providing venue for

public meeting to promote unity

of brotherhood would not

constitute charitable activity to

deny continuance of approval

under Section 80G(5)(vi) (of Income Tax Act, 1961) of the

Act?

(b) When Appellant has granted

registration under Section 12A (of Income Tax Act, 1961)

and also approval under Section

80G (5)(vi) of the Act and

continuance for such approval in

preceding years under similar

circumstances then, whether

Tribunal was justified in

upholding the denial of

continuance of approval

subsequently under Section

80G(5)(vi) of the Act?

(c) Whether construction of a

building to enable carrying out

Appellant’s objects can be held as

in adequate for grant of

continuance of approval under

Section 80G(5)(vi) (of Income Tax Act, 1961) when

such continuance was required

for carrying out of activity

concerning advancement of object

of general public utility as

provided under Section 2(15) (of Income Tax Act, 1961)?

(d) Whether the proviso to Section

2(15) of the Act would apply to

justify the denial of continuance

of approval under Section

80G(5)(vi) of the Act when the

construction of building for

carrying out of the object of the

Society was under progress?”

7. Having heard the learned Advocates

appearing for parties and on perusal of the records, it

would emerge that assessee –Trust was granted

registration under Section 12A (of Income Tax Act, 1961) and also

approval under Section 80G(5)(vi) (of Income Tax Act, 1961) on

17.02.2004 upto 31.03.2005. Same was continued

with effect from 01.04.2005 and upto 31.03.2008 by

order dated 04.10.2005 (Annexure-E) and thereafter

assessee sought for continuance of the approval

granted under Section 80G(5)(vi) (of Income Tax Act, 1961) by

submitting an application on 06.03.2008.

Respondent issued a show cause notice to the

assessee proposing to reject the application. Same

was resisted to by the assessee by filing detailed

objection, copy of which has been made available by

the learned Advocate appearing for the assessee

during the course of arguments. Subsequently, the

Commissioner vide order dated 28.11.2008

(Annexure-G) rejected the application for

continuation of the recognition.

8. Perusal of the said order dated

28.11.2008 which is at Annexure-G would indicate

that there is neither consideration of objections filed

by the assessee for rejecting the application of

assessee nor the respondent has examined as to

whether the conditions laid down in clause (vi) of

sub-section (5) of Section 80G (of Income Tax Act, 1961) is either

fulfilled or not fulfilled, for rejecting the application

for renewal. Assessee had carried said order of

rejection in appeal before the Tribunal by filing an

appeal and even the appellate Tribunal after

considering the grounds urged by the assessee has

held that rejection order is justifiable. Perusal of the

order of Tribunal dated 29.05.2009 would also

indicate that there are no reasons forthcoming as to

why order of rejection is sustained, except making a

passing reference to the fact that construction of the

building by the assessee would by itself not

constitute granting of relief for the poor or it would be

sufficient to hold such activity would amount

charitable purpose. It is not in dispute that

registration granted to the respondent-assessee

under Section 12A (of Income Tax Act, 1961) is in force or vogue as

on date and the Commissioner while examining the

application for approval of an institution or fund

under Section 80G (of Income Tax Act, 1961) is required to comply

with Rule 11AA (of Income Tax Rules, 1962), which

reads as under:

“Requirements for approval of an

institution or fund under Section

80G.

11AA. (1) The application for approval

of any institution or fund under clause

(vi) of sub-section (5) of Section 80G (of Income Tax Act, 1961)

shall be in Form No.10G and shall be

made in triplicate.

(2) The application shall be

accompanied by the following

documents, namely;-

(i) Copy of registration

granted under Section 12A (of Income Tax Act, 1961)

or copy of notification

issued under Section

10(23) or 10(23C);

(ii) Notes on activities of

institution or fund since its

inception or during the last

three years, whichever is

less;

(iii) Copies of accounts of the

institutions or fund since

its inception or during the

last three years, whichever

is less.

(3) The Commissioner may call for

such further documents or

information from the institution

or fund or cause such inquiries

to be made as he may deem

necessary in order to satisfy

himself about the genuineness of

the activities of such institution

or fund.

(4) Where the Commissioner is

satisfied that all the conditions

laid down in clauses (i) to (v) of

sub-section (5) of section 80G (of Income Tax Act, 1961) are

fulfilled by the institution or

fund, he shall record such

satisfaction in writing and grant

approval to the institution or

fund specifying the assessment

year or years for which the

approval is valid.

(5) Where the Commissioner is

satisfied that one or more of the

conditions laid down in clauses (i)

to (v) of sub-section (5) of Section

80G are not fulfilled, he shall

reject the application for

approval, after recording the

reasons for such rejection in

writing:

Provided that no order of

rejection of an application shall

be passed without giving the

institution or fund an

opportunity of being heard.

(6) The time limit within which the

Commissioner shall pass an

order either granting the approval

or rejecting the application shall

not exceed six months from the

date on which such application

was made:

Provided that in computing the

period of six months, any time

taken by the applicant in not

complying with the directions of

the Commissioner under sub-rule

(3) shall be excluded. “

9. Perusal of the above Rule would indicate

that an applicant is required to indicate in the

application about activities of the institution or fund

collected since its inception or during the last three

years whichever is less including furnishing of

Registration Certificate obtained under Section 12A (of Income Tax Act, 1961)

and copies of its accounts since inception or last

three years, whichever is less and in the event of

Commissioner not being satisfied with the details

furnished by the applicant, he is empowered under

sub-rule (3) of Rule 11AA (of Income Tax Rules, 1962) to call for

further documents or information from the institution

or fund or cause such enquiry as he deems necessary

in order to satisfy himself the activities of the

institution or fund is genuine. After calling for such

information or details or particulars, if the

Commissioner is satisfied that all the conditions laid

down under clauses (i) to (v) to sub-section (5) of

Section 80G (of Income Tax Act, 1961) are fulfilled, he would issue approval as

otherwise, he would reject the application for

approval by recording reasons for such rejection and

communicate the same to the applicant.

10. At the cost of repetition, it requires to be

noticed that order of rejection of renewal of

recognition dated 28.11.2008 – Annexure-G is bereft

of reasons. On the ground of order of rejection being

not a speaking order which has been affirmed by the

Tribunal in a perfunctory manner, we are of the

considered view that both the orders cannot be

sustained and are liable to be set aside. In view of

the fact that objections came to be filed by the

assessee – applicant to the rejection proposed by

respondent indicating that it had taken steps to fulfill

the objects of the Trust by not only constructing

‘Samudaya Bhavana’ but also medical treatment said

to have been given by its ‘Mumbai Samithi’ apart

from distribution of books to the needy, are all

aspects which was required to be examined by

respondent and said exercise having not been

undertaken, we are of the considered view that

matter requires to be remitted to the respondent for

being adjudicated afresh. Hence, by setting aside

order dated 28.11.2008 passed by the respondent

and order dated 29.05.2009 passed by the Tribunal,

matter is being remitted to the respondent for

adjudication afresh. It is needless to state that

respondent would be at liberty to examine the

application afresh on merits and in accordance with

law.

11. In that view of the matter, substantial

questions of law as obtained in the facts and

circumstances of the case are required to be

answered in favour of the appellant – assessee.

Hence, we proceed to pass the following order:

(1) Appeal is hereby allowed by

answering substantial questions of

law in favour of the assessee –

applicant (on facts).

(2) Matter is remitted back to the

Commissioner of Income Tax,

Mangalore for being adjudicated

afresh and he would be at liberty to

pass orders on merits and in

accordance with law without being

influenced by the observations made

in the earlier order which came to be

affirmed by the Tribunal.

(3) Costs made easy.

Sd/-

JUDGE

Sd/-

JUDGE

×

Similar Ripples

Questions

Court Remands Case for Fresh Adjudication on Tax Exemption Approval

Write your CommentSimilar Posts

Generic

- Reportdata/3632.pdf