Court Remands Case for Reconsideration of Assessee's Denial in Income Tax Dispu…

Full News

Court Remands Case for Reconsideration of Assessee's Denial in Income Tax Dispute

Court Remands Case for Reconsideration of Assessee's Denial in Income Tax Dispute

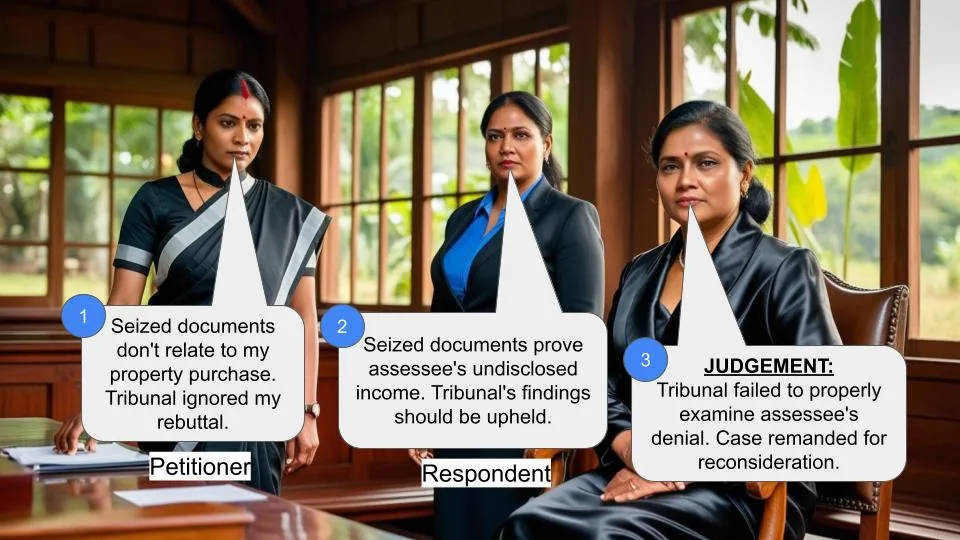

In this case, Jaswant Singh (the assessee) appealed against an Income Tax Tribunal's decision regarding undisclosed income. The High Court found that the Tribunal had not properly examined the assessee's rebuttal of presumptions made against him. As a result, the Court remanded the case back to the Tribunal for reconsideration.

Get the full picture - access the original judgement of the court order here.

Case Name:

Jaswant Singh vs Assistant Commissioner of Income Tax (High Court of Allahabad)

Income Tax Appeal No. 200 of 2010

Key Takeaways

1. The importance of thoroughly examining an assessee's rebuttal in tax cases.

2. The court's willingness to remand cases when lower authorities fail to consider crucial aspects.

3. The significance of timing in relating seized documents to specific transactions.

Issue

Did the Income Tax Tribunal properly consider the assessee's rebuttal against the presumption of undisclosed income based on seized document

Facts

- A search and seizure operation was conducted at the assessee's residence on 4.6.2002.

- Loose sheets (marked as LP-10) were seized during the operation.

- The tax department linked these sheets to a property purchase in Tilak Nagar, Kanpur, registered on 17.5.2002.

- The assessing authority concluded there was undisclosed income based on these documents.

- The assessee denied that the loose sheets were related to the property transaction.

Arguments

Assessee's Arguments:

- The notings in LP-10 were rough estimates and incorrect.

- The property was registered in May 2001, so calculations from 2002 couldn't relate to it.

- The presumptions were based on conjecture, not evidence.

Tax Department's Arguments:

- The loose sheets related to the Tilak Nagar property transaction.

- The assessee failed to explain the nature of various entries in the documents.

Key Legal Precedents

No specific legal precedents were cited in this judgment.

Judgement

The High Court found that:

1. The assessee had denied the connection between the loose sheets and the property transaction.

2. The Tribunal failed to examine this denial properly.

3. The matter should be remanded to the Tribunal for reconsideration.

The Court ordered the Tribunal to reconsider "whether or not the assessee had in fact denied LP-10 as relating to the property purchased at Tilak Nagar, Kanpur Nagar?"

FAQs

Q1: What was the main issue in this case?

A1: The main issue was whether the Tribunal properly considered the assessee's denial of the connection between seized documents and a property transaction.

Q2: Why did the High Court remand the case?

A2: The Court remanded the case because the Tribunal had not examined the assessee's rebuttal of the presumptions made against him.

Q3: What specific question did the Court ask the Tribunal to reconsider?

A3: The Court asked the Tribunal to reconsider whether the assessee had indeed denied that LP-10 related to the property purchased at Tilak Nagar, Kanpur Nagar.

Q4: What is the significance of this judgment?

A4: This judgment emphasizes the importance of thoroughly examining an assessee's rebuttal in tax cases and the court's willingness to remand cases when lower authorities fail to consider crucial aspects

Q5: What timeframe did the Court set for the Tribunal to reconsider the case

A5: The Court ordered the Tribunal to decide the matter within three months from the date of production of a certified copy of the order.

Heard Shri S.D. Singh, learned Senior Counsel assisted by Shri Archi Agrawal, learned counsel for the appellant and Shri Shubham Agrawal, learned counsel for the department.

This appeal has been filed by the assessee under Section 260-A (of Income Tax Act, 1961), 1961 against the order passed by the Tribunal dated 30.10.2009 for the blocked period ending 4th of June 2002.

The questions of law sought to be answered by the order of this Court dated 5.5.2014 reads as hereunder:

"(i) Whether, the finding in respect of on-money alleged to have been paid by the appellant and Sri Kamal Raheja is based on any cogent material and evidence on record?

The facts of the case are that a search and seizure operation was conducted at the residence of the assessee on 4.6.2002 and some documents were seized from the premises which included some loose sheets.

While examining these loose sheets which was marked as LP-10 the department sought to correlate the same documents to a property purchased by the assessee at Tilak Nagar, Kanpur between him and one Shri Kamal Raheja. The registration of which was done on 17.5.2002. The assessing authority sought to correlate these loose sheets to the transaction between him and Shri Kamal Raheja on the basis of scribbling on the loose sheets marked as LP-10 and came to the conclusion that some undisclosed income and undisclosed investments were there which had not been shown by the assessee.

The assessing authority records in his assessment order dated 18.6.2004 which reads as hereunder:

"9.8. Reply was subsequently filed on 15.06.2004. It was argued that the notings in annexure LP-10 were rough estimates, which were incorrect. It was further argued that the cut figures have to be taken as cut. It was stated that the property was finally registered in May 2001 and thus the calculation which seem to be of 2002 could not relate to any amount paid on account of purchase of property. It was further routinely argued that details of property/ on money were nowhere recorded in the entire LP and entire presumption is based on conjectures and surmises and not on any evidence found during search. This paper was stated to be dump. Regarding amount of surplus of Rs.39,500/- it was stated that it seemed to be rough working and assessee was estimating what he would earned or saved.

The Commissioner of Income Tax also came to the conclusion that the loose papers related to the Tilak Nagar, Kanpur property and made an addition against the assessee. The Tribunal too has recorded a finding which is contained in paragraph 17 of the Tribunal's order which reads as hereunder:

"17. After careful consideration of rival submissions, we are of the opinion that so far as details in the alleged papers under reference which have been reproduced by the CIT (A) in para 31 of her order are concerned, the assessee has not disputed that the same did not relate to transactions carried by him or with respect to transactions in which the assessee was involved and having not disputed this fact it was incumbent upon him to explain the nature of various entries. Simply submitting that the details were of May, 2002 whereas the property had been registered in 2001, in our opinion, was not sufficient to discard the revenue's case. It is quite possible that extra money may have been paid after the registration or if it was not for that property, it may have been against some other transaction/ property. The onus put on the assessee, in our opinion, was not discharged and therefore, we are unable to interfere with the order of the CIT (A), which is confirmed."

Upon reading of the three orders passed by the authorities below it becomes abundantly clear that the assessee had infact denied the loose sheets and had nothing to do with the transaction that was completed on 17.5.2001 The search had been made after one year. Apart from one figure which the authorities had tried to relate to the transaction by saying that it has two zeroes less of an amount of Rs.2,64,73,000/-. No other figure seems to be matched with the cost of registration which was rupees 23 lacs and odd. The authorities below have tried to say that it related to the property because it could be presumed to reach an amount of Rs.26 lacs.

The Tribunal opines that simply submitting the details were of May, 2002 whereas the property had been registered in 2001 was not sufficient to discard the revenue case.

On the contrary we are of the opinion that once the assessee had rebutted the presumption which had been drawn against the assessee and also in view of the fact that the assessing officer records that the assessee denied that loose sheets related to the previous transactions, such a finding could have been made by the Tribunal. The Tribunal has not examined this aspect of the matter at all.

The matter is, therefore, remanded to the Tribunal to reconsider this aspect of the matter i.e. whether or not the assessee had infact denied LP-10 as relating to the property purchased at Tilak Nagar, Kanpur Nagar?

The matter on remand may be decided within a period of three months from the date of a production of a certified copy of the order before it. A certified copy of the order may be produced before the authority concerned within next three weeks. The question is, therefore, decided in the above terms.

The appeal stands disposed of.

Order Date :- 21.12.2016

×

Similar Ripples

Questions

Court Remands Case for Reconsideration of Assessee's Denial in Income Tax Dispute

Write your CommentSimilar Posts

Generic

- Reportdata/11427-HC.pdf