Court Remands Case on Land Acquisition Costs in Company Amalgamation

Full News

Court Remands Case on Land Acquisition Costs in Company Amalgamation

Court Remands Case on Land Acquisition Costs in Company Amalgamation

This case involves Commonwealth Trust (India) Ltd. and the Commissioner of Income Tax. The dispute centers around the taxation of compensation received by the company for land acquired by the government. The court set aside previous orders and remanded the case for fresh consideration, emphasizing the need to examine the terms of the amalgamation scheme.

Get the full picture - access the original judgement of the court order here

Case Name:

Commonwealth Trust (India) Ltd. Vs Commissioner of Income Tax (High Court of Kerala)

ITA. No. 170 of 2000(M)

Date: 8th April 2008

Key Takeaways:

1. Acquisition of property through amalgamation may involve consideration in the form of share allotment.

2. The value of shares allotted can constitute the value of property acquired during amalgamation.

3. Courts should carefully examine the terms of amalgamation schemes approved by High Courts.

4. If cost of acquisition is based on a specific date (1.1.1974), the Tribunal's fixed value should be adopted to avoid further litigation.

Issue:

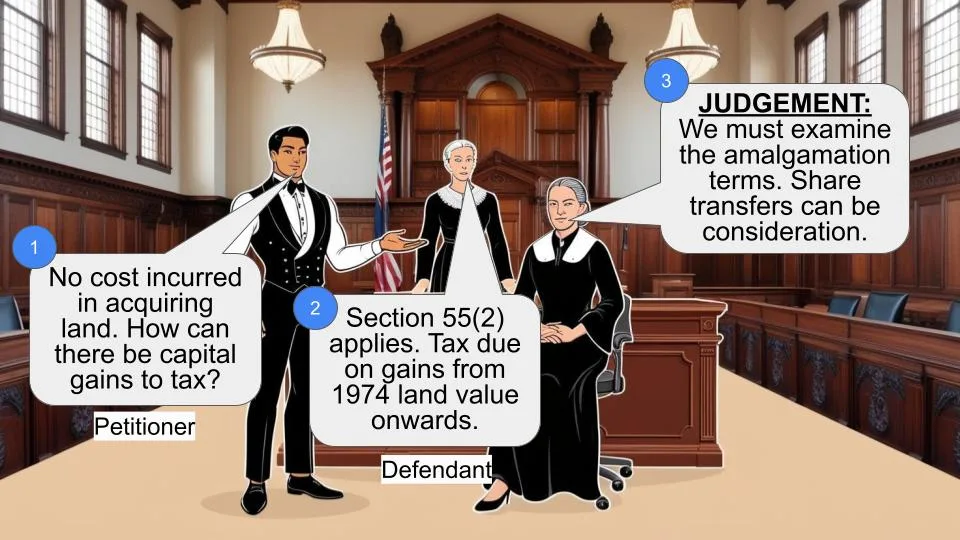

Does the acquisition of land by a company through a scheme of amalgamation involve a cost of acquisition, making the compensation received on subsequent government acquisition of that land chargeable under capital gains?

Facts:

1. The land in question originally belonged to Basel Mission Trading Co., which was declared enemy property during World War I and taken over by the British Government.

2. The British Government transferred the property to a U.K. company named Commonwealth Trust Limited.

3. In 1977, the High Court approved a scheme of amalgamation, transferring the properties to the petitioner, an Indian company.

4. During the assessment years 1990-91 and 1991-92, the Government of Kerala acquired some of this land and paid compensation.

5. The company didn't offer the compensation for assessment under capital gains, claiming it hadn't spent any amount on acquisition.

Arguments:

Appellant's Argument:

- The land was acquired without payment, so there was no cost of acquisition, and thus no capital gain arises.

Revenue's Argument:

- By virtue of Section 55(2) (of Income Tax Act, 1961), the appellant is liable to pay tax on capital gains by adopting the land's value as of 1.1.1974.

Key Legal Precedents:

While specific case laws aren't mentioned in the provided context, the judgment refers to "various court decisions including that of the Supreme Court" supporting the contention that capital gain doesn't arise where there's no cost involved in property acquisition.

Judgement:

1. The court set aside the orders of the Tribunal and lower authorities.

2. The case was remanded to the Assessing Officer for fresh consideration.

3. The court found that the assumption of no consideration in property acquisition was incorrect.

4. The amalgamation scheme involved share transfers, which constitutes consideration.

5. The Assessing Officer must verify the terms of amalgamation approved by the High Court.

6. If cost of acquisition is adopted as the value on 1.1.1974, the Tribunal's fixed value should be used to avoid further litigation.

FAQs:

Q1: Why did the court remand the case?

A1: The court remanded the case because the previous orders were based on an incorrect assumption that there was no consideration in the property acquisition during amalgamation. The court wants the Assessing Officer to examine the actual terms of the amalgamation scheme.

Q2: What constitutes the consideration in this case?

A2: The consideration is in the form of shares transferred to the shareholders of the foreign company from which the property was transferred to the petitioner company under the amalgamation scheme.

Q3: How does share allotment relate to property value in amalgamation?

A3: Share capital is a liability of the company to shareholders. Therefore, the value of shares allotted constitutes the value of the property acquired by the company during amalgamation.

Q4: What should the Assessing Officer do now?

A4: The Assessing Officer should verify the terms of amalgamation approved by the High Court, give the assessee an opportunity for a hearing, and then make a fresh consideration of the case.

Q5: What if the cost of acquisition is based on the 1.1.1974 value?

A5: If the cost of acquisition is adopted as the value on 1.1.1974, the value fixed by the Tribunal should be used to avoid another round of litigation on this ground.

The connected appeals filed by the appellant arise from order of the Tribunal upholding levy of capital gains on land acquired from the appellant by the Government during the previous years relevant for the assessment years 1990-91 and 1991-92. The land acquired originally belonged to Basel Mission Trading Co. which was declared as an enemy property during the first world war and taken over by the British Government. The British Government thereafter transferred the property to a U.K. Company by name Commonwealth Trust Limited. The property in the form of land and buildings remained that of British company until 1977. However, in the year 1977 the High Court approved a scheme of amalgamation where under the landed properties of the British company namely, the amalgamating company was transferred to the petitioner which is an Indian company. During the previous years relevant for assessment years 1990-91 and 1991-92, Government of Kerala acquired some extent of land from the company and paid compensation. The company did not offer the compensation received for assessment under the head "capital gains" for the reason that it had not spent any amount towards cost of acquisition. Even though the factual position was not controverted, the officer assessed capital gains on the compensation amount which is upheld by the first appellate authority and the Tribunal, against which these appeals are filed.

2. Sri.P.Balachandran, Senior counsel appearing for the appellant contended that the land in respect of which compensation for acquisition was received, originally belonged to Basel Mission which was acquired by the British Company as enemy property. Thereafter the property was transferred to British company and in turn to the assessee-company under the scheme of acquisition and since no payment was made for acquisition of land, there was no cost of acquisition and so much so, capital gain does not arise. He has relied on various court decisions including that of the Supreme Court in support of his contention that capital gain does not arise in a case where there is no cost involved in the acquisition of property. Senior counsel for the Revenue on the other hand contended that by virtue of Section 55(2) (of Income Tax Act, 1961), the appellant is liable to pay tax on the capital gains by adopting the value of the land as on 1.1.1974. We do not think we should answer the question on the facts based on which decision was rendered by all the authorities including the Tribunal because we are of the view that the assumption by all the authorities that there was no consideration in the acquisition of property by the assessee is incorrect. In fact some of the documents produced in court pertain to amalgamation. We find that the scheme of amalgamation approved by the High Court involved transfer of shares to the shareholders of the foreign company from which the property was transferred to the petitioner under scheme of amalgamation approved by the High Court. In other words, if shares were transferred to the shareholders of the foreign company, then the transfer of property to the appellant-company is against consideration in the form of value of shares allotted to the shareholders of the amalgamating company. Share capital is a liability of the company to the shareholders and so much so, value of shares allotted constitute value of the property acquired by the company in the course of amalgamation. So much so, we are of the view that the acquisition of property in the course of amalgamation involved payment of consideration, though in the form of allotment of fully paid shares to the shareholders of the amalgamating company. If this is the position, then the assessee will not be entitled to contend that the acquisition of land by them in the course of amalgamation did not involve any cost to them. Since orders are based on wrong assumption of facts and without examining the nature and content of the scheme of amalgamation approved by the High Court under which the property vested in the assessee-company, we set aside the orders of the Tribunal and that of lower authorities and remand the matter to the Assessing Officer for fresh consideration after verifying the terms of amalgamation approved by the High Court and after giving an opportunity of hearing to the assessee. However, we make it clear that if cost of acquisition is adopted as the value as on 1.1.1974, then the value fixed by the Tribunal shall be adopted for the sake of finality so that another round of litigation is avoided on this ground.

C.N.RAMACHANDRAN NAIR

Judge T.R.RAMACHANDRAN NAIR Judge

×

Similar Ripples

Questions

Court Remands Case on Land Acquisition Costs in Company Amalgamation

Write your CommentSimilar Posts

Generic

- Reportdata/4674.pdf