Court Remands Tax Deduction Case for Fresh Examination of Evidence

Full News

Court Remands Tax Deduction Case for Fresh Examination of Evidence

Court Remands Tax Deduction Case for Fresh Examination of Evidence

This case involves Guru Angad Dev Veterinary Agricultural Science University (GADVASU) appealing against income tax authorities' decision regarding tax deduction at source (TDS). The High Court remanded the matter back to the Assessing Officer for a fresh examination of new evidence.

Get the full picture - access the original judgement of the court order here

Case Name:

Guru Angad Dev Veterinary Agricultural Science University vs Commissioner of Income Tax (High Court of Punjab & Haryana)

ITA No. 347 of 2011 (O&M)

Date: 10th February 2016

Key Takeaways:

1. The court emphasized the importance of examining all relevant evidence before making a tax-related decision.

2. The case highlights the complexity of TDS obligations in contractual relationships.

3. The judgment demonstrates the court's willingness to allow for reconsideration when new evidence is presented.

Issue

Was the Income Tax Appellate Tribunal justified in upholding the lower authorities' orders that GADVASU was liable for not deducting tax at source under Section 194C (of Income Tax Act, 1961)?

Facts

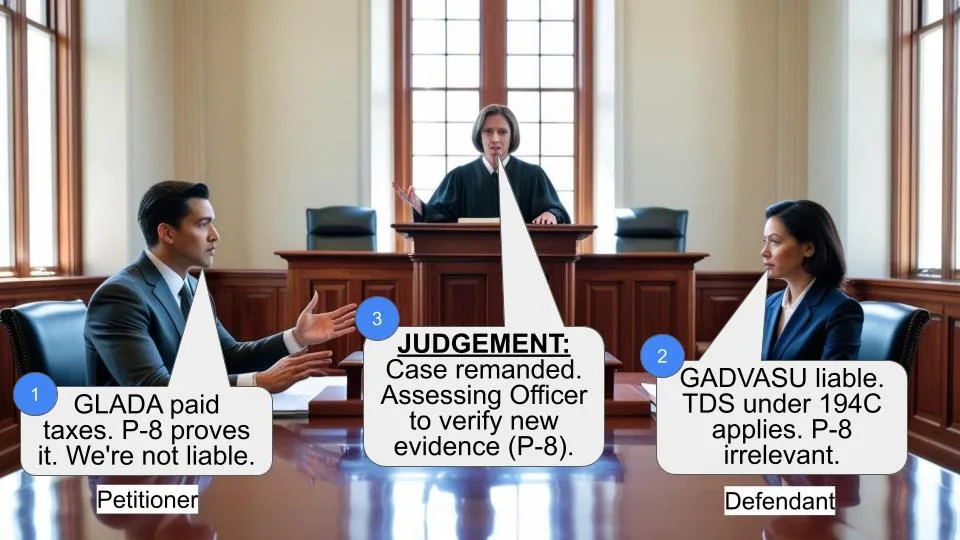

1. GADVASU (our appellant) entered into a Memorandum of Understanding (MOU) with the Greater Ludhiana Area Development Authority (GLADA) on March 24, 2007.

2. The MOU was for GLADA to supervise a building project at the University Campus.

3. GADVASU gave an interest-bearing advance to GLADA.

4. The agreement stated that GLADA would deduct tax at source when paying contractors.

5. On December 3, 2009, the tax department conducted a TDS inspection.

6. They issued a show cause notice to GADVASU about why TDS wasn't deducted on payments to GLADA.

7. The Income Tax Officer created a demand of ₹29,46,570 (including interest) against GADVASU.

8. GADVASU appealed, but both the CIT(A) and the Tribunal dismissed their appeals.

9. Now, GADVASU has approached the High Court with this appeal.

Arguments

GADVASU's side:

1. The interest-bearing advance to GLADA wasn't a payment for work, so Section 194C (of Income Tax Act, 1961) doesn't apply.

2. GLADA was a supervising agency, not a contractor.

3. GLADA deducted tax when paying contractors, as per the MOU.

4. They presented a new certificate (Annexure P-8) from GLADA confirming tax payments.

Tax Department's side:

1. The MOU used the word 'contract', making GADVASU liable under Section 194C (of Income Tax Act, 1961).

2. GADVASU should have deducted TDS when paying GLADA.

Key Legal Precedents

The appellant cited three important cases:

1. Hindustan Coca-Cola Beverage (P) Ltd. v. Commissioner of Income Tax (2007) 293 ITR 226 (SC)

2. Children's Education Society v. Deputy Commissioner of Income Tax (TDS) (2009) 319 ITR 409 (Kar.)

3. Commissioner of Income Tax v. The Chief Electoral Officer, Chandigarh, ITR No. 183 of 1999 decided on 23.11.2010

These cases suggest that if the new evidence (Annexure P-8) is found to be correct, GADVASU might not be liable for the tax.

Judgement

The High Court decided to:

1. Set aside the previous orders by the Assessing Officer, CIT(A), and Tribunal.

2. Remand the matter back to the Assessing Officer.

3. Direct the Assessing Officer to examine the veracity of Annexure P-8.

4. Instruct the Assessing Officer to decide the issue afresh based on this examination.

The court emphasized that this decision doesn't express any opinion on the merits of the case.

FAQs

1. Q: What is the significance of Annexure P-8?

A: It's a certificate from GLADA confirming that they paid taxes on the interest received from GADVASU and deducted TDS when paying contractors.

2. Q: Why did the court remand the case instead of deciding it?

A: The court wanted the Assessing Officer to verify the new evidence (Annexure P-8) before making a decision.

3. Q: What is Section 194C (of Income Tax Act, 1961)?

A: It deals with TDS on payments to contractors for carrying out any work.

4. Q: Does this judgment mean GADVASU won the case?

A: Not necessarily. It means they get another chance to present their case with the new evidence.

5. Q: What happens next in this case?

A: The Assessing Officer will examine Annexure P-8 and make a fresh decision based on all the evidence.

1. Photocopy of Annexure P-8 filed along with CM No. 3127-CII of 2016 is taken on record subject to all just exceptions. CM stands disposed of accordingly.

2. This order shall dispose of two appeals bearing ITA Nos. 347 and 348 of 2011 as according to learned counsel for the parties, the issues involved therein are identical. For brevity, the facts are being extracted from ITA No. 347 of 2011.

3. This appeal has been preferred by the assessee under Section 260A (of Income Tax Act, 1961) (in short “the Act”) against the order dated 27.4.2011 (Annexure A-3) passed by the Income Tax Appellate Tribunal, Chandigarh Bench “B”, Chandigarh (hereinafter referred to as “the Tribunal”) in ITA No. 1453/CHANDI/2010, for the assessment year 2009-10. The appeals were admitted by this Court vide order dated 13.8.2012 for consideration of the substantial questions of law as mentioned in para 12 of the appeals which are as under:-

1. Whether on the facts and in the circumstances of the case, the learned Tribunal is justified in upholding the orders of the authorities below ignoring that interest bearing advance cannot be treated as payment for carrying out any work so as to attract Section 194C (of Income Tax Act, 1961), particularly when interest of 43.46 lacs has accrued to the appellant on the advance of 6.97 crores, as per Annexure A-7?

2. Whether the ITAT is justified in confirming the order of authorities below holding the appellant as liable u/s 194C (of Income Tax Act, 1961) by being swayed by the word 'contract' mentioned in the MOU instead of observing the real intention of the MOU and thereby treating the supervising agency i.e. GLADA as a contractor who was actually a specialized agency of the government to be paid for supervising the work as an arm of the appellant, and to make payments to the contractors subject to deduction of tax at source on behalf of the appellant, as per clause 1(f) of the MOU, Annexure A-4, which has duly been deducted as per Annexure A-6?

3. Whether the ITAT is justified in confirming the order of authorities below holding the appellant as liable u/s 194C (of Income Tax Act, 1961) despite the fact that the appellant was not at all required to deduct the tax at source on payment of interest bearing advance to GLADA which is not an expenditure on 'carrying our any work' and when any payment was made out of the said advance for 'carrying out the work' tax was duly deducted at, Annexure A-6?

4. Put shortly, the facts necessary for adjudication of the instant appeal as narrated therein may be noticed. The appellant/assessee entered into Memorandum of Understanding (MOU) on 24.3.2007 (Annexure A-4) with Punjab Urban Development Authority presently known as Greater Ludhiana Area Development Authority (GLADA), Ludhiana for supervision of the building project at the University Campus on behalf of the appellant. The project was initiated in the year 2007 and as per clause 3 of the MOU, interest bearing advance was forwarded by the appellant to the GLADA with a clear understanding that when any payment is made to the contractors executing the work, the GLADA will deduct the tax at source and the tax as per certificate dated 5.8.2010 (Annexure A-5) has been deducted by the GLADA. On 3.12.2009, a TDS inspection was carried out by the revenue. A show cause notice dated 31.12.2009 was issued to the assessee to explain as to why TDS on amount of 11,67,79,805/-, 1,26,000/- and ` 2,74,000/- was not deducted under Section 194C (of Income Tax Act, 1961) at the time of issuance of cheques to GLADA and as to why interest under Section 201(1A) (of Income Tax Act, 1961) be not charged. The Income Tax Officer, TDS-II, Ludhaia vide order dated 15.2.2010 (Annexure A-1) passed under Section 201(1) (of Income Tax Act, 1961) created demand of 29,46,570/- including interest of 2,67,870/- under Section 201(1A) (of Income Tax Act, 1961). The assessee filed an appeal against the order, Annexure A-1, before the Commissioner of Income Tax (Appeals) [for brevity “the CIT(A)”]. The CIT(A) vide order dated 15.10.2010 (Annexure A-2) upheld the order, Annexure A-1, and dismissed the appeal. Feeling dissatisfied, the assessee filed an appeal before the Tribunal who vide order dated 27.4.2011 (Annexure A-3) dismissed the appeal. Hence, the instant appeals.

5. Learned counsel for the appellant-assessee relied upon the certificate dated 5.9.2012 (Annexure P-8) issued by GLADA, confirming that the interest on payments received from Guru Angad Dev Veterinary & Animal Sciences University (GADVASU) for deposit works of GADVASU during the financial years 2007-08 and 2008-09 relevant to the assessment years 2008-09 and 2009-10, respectively have been added in the income of the GLADA and the income tax due on such interest amount has been paid. It has further been certified that TDS has been deducted and deposited wherever applicable on payments made to the contractors in lieu of GADVASU work executed/done.

6. It was urged by learned counsel for the appellant that the matter is required to be remitted to the Assessing Officer to ascertain the veracity of factual matrix contained in Annexure P-8 and in case it is found to be correct, then in view of the judgments of the Supreme Court in Hindustan Coca-Cola Beverage (P) Ltd. v. Commissioner of Income Tax (2007) 293 ITR 226 (SC); Karnataka High Court in Children's Education Society v. Deputy Commissioner of Income Tax (TDS) (2009) 319 ITR 409 (Kar.) and of this Court in Commissioner of Income Tax v. The Chief Electoral Officer, Chandigarh, ITR No. 183 of 1999 decided on 23.11.2010, no tax liability could be created or sustained against the assessee for non-deduction of tax at source.

7. On the other hand, learned counsel for the revenue supported the orders passed by the authorities below and prayed for dismissal of the appeals.

8. We have heard learned counsel for the parties and find substance in the submission of learned counsel for the appellant.

9. In view of the submission of learned counsel for the parties, it is considered appropriate that the matter is referred back to the Assessing Officer to examine and verify the factual matrix as urged by learned counsel for the appellant. Accordingly, the impugned orders passed by the Assessing Officer (Annexure A-1), the CIT(A) (Annexure A-2) and the Tribunal (Annexure A-3) are set aside. The matters are remanded to the Assessing Officer for examining the veracity of Annexure P-8 and decide the issue afresh in accordance with law. Needless to say that nothing observed hereinbefore shall be taken to be expression of opinion on the merits of the controversy.

(AJAY KUMAR MITTAL)

JUDGE

February 10, 2016 (RAJ RAHUL GARG)

gbs JUDGE

×

Similar Ripples

Questions

Court Remands Tax Deduction Case for Fresh Examination of Evidence

Write your CommentSimilar Posts

Generic

- Reportdata/3107.pdf