Court Upholds Tax Deduction Requirement for Interest Payments, Rejecting Govern…

Full News

Court Upholds Tax Deduction Requirement for Interest Payments, Rejecting Government Exemption Claim

Court Upholds Tax Deduction Requirement for Interest Payments, Rejecting Government Exemption Claim

The Punjab High Court dismissed an appeal by the Council for Citrus & Agri Juicing in Punjab against an Income Tax Appellate Tribunal order. The case centered on whether the appellant was required to deduct tax at source for interest payments, which they claimed were exempt as payments to the government. The court upheld the tax authorities' decision, ruling that the appellant failed to prove the payments qualified for exemption under Section 196(i) (of Income Tax Act, 1961).

Get the full picture - access the original judgement of the court order here.

Case Name:

Council for Citrus & Agri Juicing in Punjab vs Commissioner of Income Tax (TDS) (High Court of Punjab and Harayana)

ITA No. 338 of 2015 (O&M)

Key Takeaways:

1. The court affirmed that tax deduction at source (TDS) is required for interest payments unless clearly proven to be made to the government.

2. Self-serving certificates and meeting minutes are insufficient to prove government ownership of funds.

3. The case highlights the importance of maintaining clear documentation for claiming tax exemptions.

Issue:

Whether the interest payments made by the appellant were exempt from tax deduction at source under Section 196(i) (of Income Tax Act, 1961) as payments to the government?

Facts:

- The Income Tax Officer issued a show cause notice to the assessee for short deduction of tax at source for the financial year 2007-08 (assessment year 2008-09).

- The Assessing Officer created a total demand of Rs. 13,64,006/-, including Rs. 9,21,626/- for short deduction of tax at source and Rs. 4,42,380/- as interest.

- The assessee had made a provision for interest of Rs. 48 lacs in its books of account without deducting TDS.

- The Punjab Agro Industrial Corporation (PAIC) had not shown the interest income in their books of account.

- The assessee claimed that the loan was from a corpus fund created by the government, and thus the interest was payable to the government.

Arguments:

- The assessee argued that the interest paid was to the government as envisaged under Section 196(i) (of Income Tax Act, 1961), and therefore no tax deduction at source was required.

- The assessee relied on Annexures A-4 and A-5 to support their claim that the interest was paid to the government as the corpus fund was created by the government.

- The tax authorities contended that there was no documentary evidence to prove that the loan was raised from the government and that the interest was payable to the government.

Key Legal Precedents:

- Section 196(i) (of Income Tax Act, 1961), which states that no deduction of tax shall be made from sums payable to the government by way of interest or dividend in respect of securities or shares owned by it or in which it has full beneficial interest.

- The case of Hindustan Coca-Cola was mentioned but deemed not applicable to the assessee's situation.

Judgement:

- The High Court dismissed the appeal, finding no substantial question of law arising from the case.

- The court upheld the Tribunal's decision that there was insufficient evidence to prove the loan was raised from the government and that the interest was payable to the government.

- The court found that Annexure A-4 (a certificate from PAIC) was a self-serving document without corroboration, and Annexure A-5 (minutes of a Corpus Fund Committee meeting) did not advance the appellant's case.

- The court concluded that the interest paid by the appellant did not fall under Section 196(i) (of Income Tax Act, 1961) and was therefore subject to tax deduction at source.

FAQs:

Q1: What is Section 196(i) (of Income Tax Act, 1961)?

A1: Section 196(i) (of Income Tax Act, 1961) exempts from tax deduction sums payable to the government as interest or dividend on securities or shares owned by it or in which it has full beneficial interest.

Q2: Why was the assessee's claim for exemption rejected?

A2: The assessee failed to provide sufficient documentary evidence to prove that the loan was from the government and that the interest was payable to the government.

Q3: What kind of evidence would have been acceptable to prove government ownership?

A3: While not explicitly stated, the court's reasoning suggests that official government records or audited financial statements showing the loan and interest as government assets would have been more persuasive than self-issued certificates or meeting minutes.

Q4: What are the implications of this judgment for other organizations claiming similar exemptions?

A4: Organizations claiming exemptions under Section 196(i) (of Income Tax Act, 1961) should ensure they have robust documentation clearly demonstrating government ownership or beneficial interest in the funds involved.

Q5: Did the court make any decision regarding the interest rate for the tax demand?

A5: Yes, the court directed the Assessing Officer to verify whether the applicable interest rate should be 10.30% or 11.33%.

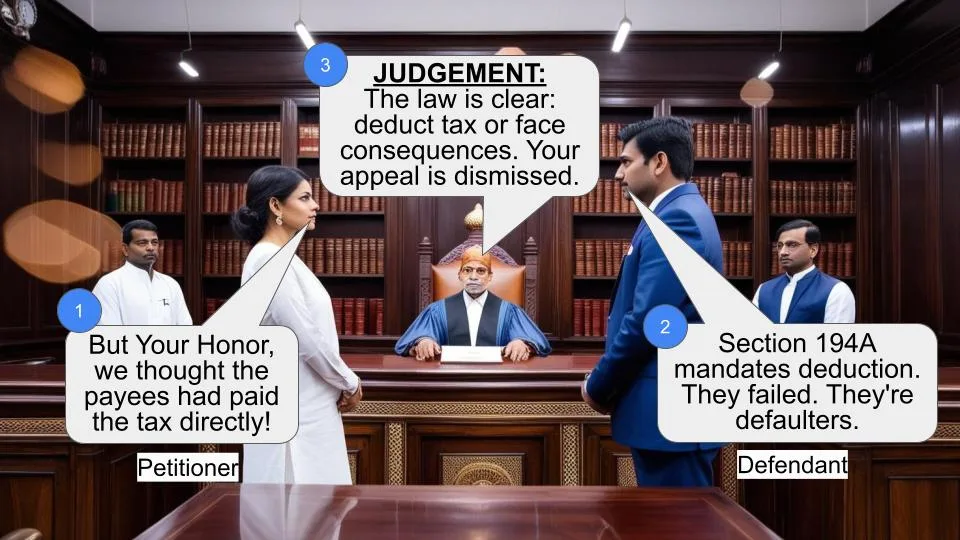

1. This appeal has been preferred by the assessee under Section 260A (of Income Tax Act, 1961) (in short “the Act”) against the order dated 17.3.2015 (Annexure A-3) passed by the Income Tax Appellate Tribunal, Amritsar Bench, Amritsar (hereinafter referred to as “the Tribunal”) in ITA No. 30/ASR/2014, for the assessment year 2008-09, claiming the following substantial questions of law:-

i) Whether the Tribunal erred on facts and in law in dismissing the appeal of the appellant on the ground that the assessee-appellant has failed to prove the loan amount being raised from the State Government and the interest is payable to the Government and as such the issue is covered under Section 196(i) (of Income Tax Act, 1961)?

ii) Whether the Tribunal was justified in dismissing the appeal of the assessee on the ground that no evidence has been produced on record that the loan amount belongs to the State Government and neither the interest nor the principal has ever been paid by the appellant?

2. A few facts necessary for adjudication of the instant appeal as narrated therein may be noticed. The Income Tax Officer (TDS)-II, Chandigarh has received information that the assessee has neither deducted or short deducted tax at source under Sections 194A (of Income Tax Act, 1961), 194C (of Income Tax Act, 1961), 194I (of Income Tax Act, 1961) and 194J (of Income Tax Act, 1961) amounting to Rs, 9,21,626/- for the financial year 2007-08 relating to the assessment year 2008-09 and he passed on the same to the Income Tax Officer (TDS)-I, Jalandhar for necessary action. The Income Tax Officer (TDS)-I, Jalandhar issued a show cause notice dated 21.3.2012 to the assessee for verification of the compliance of TDS/TCS provisions. The Assessing Officer vide order dated 27.3.2012 (Annexure P-1) passed under Sections 201(1) (of Income Tax Act, 1961)/201(1A) of the Act raised a demand of Rs, 13,64,006/- including interest. Feeling aggrieved, the

assessee filed an appeal before the Commissioner of Income Tax (Appeals) [for brevity “the CIT(A)”]. The CIT(A) vide order dated 8.11.2013 (Annexure A-2) partly allowed the appeal. Still dissatisfied, the assessee challenged the orders, Annexures A-1 and A-2 before the Tribunal, who vide order dated 17.3.2015 (Annexure A-3) upheld the order of the CIT(A) and dismissed the appeal. Hence, the present appeal.

3. Learned counsel for the assessee submitted that the authorities below were in error in declining the benefit as was available under Section 196(i) (of Income Tax Act, 1961). It was urged that the interest paid by the assessee was to the Government as envisaged thereunder and, therefore, no tax deduction at source was required to be made. Learned counsel referred to Annexures A-4 and A-5 to contend that it clearly shows that the interest was paid to the Government as the corpus fund was created by the Government.

4. After hearing learned counsel for the appellant-assessee, we do not find any merit in the appeal.

5. Section 196(i) (of Income Tax Act, 1961) reads as under:-

“196. Notwithstanding anything contained in the foregoing provisions of this Chapter, no deduction of tax shall be made by any person from any sums payable to-

(i) the Government, or

(ii) to (iv) XX XX XX

where such sum is payable to it by way of interest or dividend in respect of any securities or shares owned by it or in which it has full beneficial interest, or any other income accruing or arising to it.”

6. A plain reading of the said section shows that there would be no deduction of tax from the sums which are paid or payable to the Government by way of interest or dividend in respect of any securities or shares owned by it or in which it has full beneficial interest, or any other income accruing or arising to it.

7. A show cause notice dated 26.3.2012 was issued to the assessee for short deduction of tax at source and accordingly the Assessing Officer vide order dated 27.3.2012 (Annexure A-1) created a total demand of ` 13,64,006/- including ` 9,21,626/- for short deduction of tax at source under Section 201(1) (of Income Tax Act, 1961) and ` 4,42,380/- on account of interest under Section 201(1A) (of Income Tax Act, 1961). The CIT(A) recorded that the assessee had made a provision for the interest of ` 48 lacs in its books of account where no TDS was deducted even after the financial year was over. It was also recorded that the Punjab Agro Industrial Corporation (PAIC) has also not shown the interest income in their books of account. The CIT(A) concluded that the Assessing Officer was right in creating demand of ` 5,43,840/- along with interest for not deducting TDS. The Tribunal while affirming the findings of the CIT(A) held that there was no documentary evidence to the effect that the loan has been raised by the assessee from the Government and the interest thereon was payable to the Government. However, the Tribunal sent the matter back to the Assessing Officer for determination of rate of TDS application, i.e. @ 10.30% or 11.33%. The relevant findings recorded by the Tribunal read thus:-

“8. We have heard the rival contentions and perused the facts of the case. There is no documentary evidence placed on record by the ld. counsel for the assessee that the loan has been raised from the Government and interest is payable to the Government and therefore, the submission made before the ld. CIT(A) and before us cannot help the assessee to cover the issue u/s 196(i) (of Income Tax Act, 1961). It has also been conceded before the ld. CIT(A) that Punjab Agro Food Grains Corpn. Ltd. has also not declared the said interest income in their books of account and therefore, judicial pronouncement in the case of Hindustan Coca-Cola will not be available to the assessee as held by the ld. CIT(A). The relevant findings of ld. CIT(A) at page 18 are reproduced for the sake of convenience as under:-

“It has been submitted by the assessee that the Punjab Agro Food Grains Corporation Limited has provided loan/funds of Rs.6 crores to the assessee on which no interest was ever paid by the assessee. It has also been submitted that the assessee has also not provided any interest on the loan of Rs.6 crores in the books of account/balance sheet. When asked the assessee to substantiate its claim, it has been fairly conceded by the Ld. ARs of the assessee that the assessee has provided for the interest of Rs.48 lakhs in the books and no TDS was deducted as the financial year was already over. It has also been conceded during the appellate proceedings that PAIC has also not shown the interest income in their books of account as their income meaning thereby that the benefit of the judicial pronouncement in the case of Hindustan Coca-Cola will also not be available to the assessee. In these facts and in the circumstances of the case, I am of the opinion that the AO is justified in creating demand of Rs.5,43,840/- along with interest in the case of the assessee for not deducting TDS as per provisions of section 194 (of Income Tax Act, 1961). In the result, ground of appeal no.2 taken by the assessee is dismissed.”

9. In the facts and circumstances of the case, we find no infirmity in the order of the ld. CIT(A), who has rightly held the assessee in default u/s 201(1) (of Income Tax Act, 1961) and 201 (1A) of the Act. We find no infirmity in the order of the ld. CIT(A) subject to the rate of interest which the assessee in ground No.3 has agitated should have been 10.30% instead of 11.33%. The AO is directed to verify the rate of interest as per law whether it is

10.30% or 11.33%. Accordingly, the matter is set- aside to the file of the AO only to the extent of determination of rate of TDS applicable i.e. @ 10.30% or 11.33%. Hence, ground no.2 of the assessee is dismissed and ground no.3 is set aside to the file of the AO to determine the rate of interest applicable in the light of our direction hereinabove. Ground No.4 is also dismissed in view of our finding and finding of the ld. CIT(A).” 8. Learned counsel for the assessee was unable to show from the perusal of Annexures A-4 and A-5 appended along with the appeal that the payment of interest was made to the Government except to repeat that the corpus fund was created by the Government from which the loan was advanced to the appellant. A perusal of Annexure A-4 shows that it is a certificate issued by the PAIC that the corpus fund belong to the State Government of Punjab and an income arising out of it belonged to the Government of Punjab. Annexure A-4 is a self-serving certificate issued without any corroboration from any supporting material.

Annexure A-5 also does not advance the case of the appellant as it is the minutes of meeting of Corpus Fund Committee only. Thus, it cannot be said that the interest paid by the appellant was to the Government and would fall under Section 196(i) (of Income Tax Act, 1961).

9. In view of the above, no substantial question of law arises in this appeal. Consequently, finding no merit in the instant appeal, the same is hereby dismissed.

10. There is a delay of 2 days in filing the appeal. CM No. 19282-CII of 2015 has been filed for condonation of 2 days' delay in filing the appeal. Since the appeal has been dismissed on merits, no further orders are required to be passed in the application for condonation of delay in filing the appeal and the same is disposed of as such.

(AJAY KUMAR MITTAL) JUDGE

October 9, 2015 (RAMENDRA JAIN) gbs JUDGE

×

Similar Ripples

Questions

Court Upholds Tax Deduction Requirement for Interest Payments, Rejecting Government Exemption Claim

Write your CommentSimilar Posts

Generic

- Reportdata/3389.pdf