Court Rules on Tax Deductions: Modernization Expenses Allowed, Agent Commission…

Full News

Court Rules on Tax Deductions: Modernization Expenses Allowed, Agent Commissions Disallowed

Court Rules on Tax Deductions: Modernization Expenses Allowed, Agent Commissions Disallowed

This case involves a dispute between the Commissioner of Income Tax and a textile company regarding various tax deductions for the Assessment Year 1983-84. The main issues revolved around debenture issue expenses, commission paid to Indian agents, municipal tax expenses, and the applicability of certain sections of the Income Tax Act. The Income Tax Appellate Tribunal had made decisions on these matters, which were then referred to the High Court for opinion.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax vs. Office of the Official Liquidator (High Court of Gujarat)

Income Tax Reference No.82 of 1996

Date: 11th February 2008

Key Takeaways:

1. Expenses related to modernization of existing plant and machinery are allowable as revenue expenditure.

2. Commission paid to Indian agents for export sales is not eligible for weighted deduction under Section 35B (of Income Tax Act, 1961).

3. Mere withdrawal of court cases and submitting disputes to arbitration does not amount to cessation of liability under Section 41 (of Income Tax Act, 1961).

4. Section 43B (of Income Tax Act, 1961) is not applicable for the Assessment Year 1983-84.

Issue:

The central issue was whether various expenses claimed by the assessee (textile company) were allowable as deductions under different sections of the Income Tax Act.

Facts:

- The case pertains to the Assessment Year 1983-84, with the relevant accounting period ending on 30.6.1982.

- The assessee is a limited company running a Textile Mill with a Rubber Division.

- The company claimed debenture issue expenses of Rs.18,18,429/- and legal expenses of Rs.10,043/- and Rs.13,500/- as revenue expenses.

- The company also claimed weighted deduction for commission paid to Indian agents for export sales.

- There was a dispute regarding municipal tax expenses of Rs.6,37,885/-.

- The company had withdrawn court cases challenging municipal tax liability and submitted the disputes to arbitration.

Arguments:

Assessee's arguments:

1. Debenture issue expenses were related to working capital and should be allowed as revenue expenditure.

2. Commission paid to Indian agents should be allowed as a weighted deduction under Section 35B (of Income Tax Act, 1961).

3. Withdrawal of court cases and submission to arbitration does not amount to cessation of liability under Section 41 (of Income Tax Act, 1961).

Revenue's arguments:

1. Debenture issue expenses should be amortized under Section 35D (of Income Tax Act, 1961).

2. Commission paid to Indian agents is not eligible for weighted deduction.

3. Withdrawal of court cases amounts to cessation of liability, making Section 41 (of Income Tax Act, 1961) applicable.

Key Legal Precedents:

1. India Cements Ltd. vs. Commissioner of Income-Tax, Madras (1966) 60 ITR 52 - Cited by the assessee to support the claim for debenture issue expenses as revenue expenditure.

2. Commissioner of Income Tax vs. Stepwell Industries Ltd & Ors. (1997) 228 ITR 171 - Used by the court to determine the applicability of Section 35B (of Income Tax Act, 1961) for commission paid to Indian agents.

Judgement:

1. The court ruled in favor of the assessee regarding debenture issue expenses, allowing them as revenue expenditure.

2. The court ruled against the assessee on the issue of commission paid to Indian agents, disallowing the weighted deduction under Section 35B (of Income Tax Act, 1961).

3. The court agreed with the Tribunal that Section 41 (of Income Tax Act, 1961) was not applicable to the municipal tax dispute, as there was no cessation of liability.

4. The court confirmed that Section 43B (of Income Tax Act, 1961) was not applicable for the Assessment Year 1983-84.

FAQs:

Q1: Why were the debenture issue expenses allowed as revenue expenditure?

A1: The expenses were incurred for working capital during modernization of existing plant and machinery, not for setting up a new unit or extending the industrial undertaking.

Q2: Why was the commission paid to Indian agents not eligible for weighted deduction?

A2: Based on the Supreme Court's decision in the Stepwell Industries case, such commission is not eligible unless the assessee can prove that the agents were promoting the assessee's specific goods or services abroad.

Q3: What is the significance of the ruling on municipal tax liability?

A3: It clarifies that merely withdrawing court cases and submitting to arbitration does not constitute cessation of liability under Section 41 (of Income Tax Act, 1961).

Q4: Why was Section 43B (of Income Tax Act, 1961) not applicable in this case?

A4: Section 43B (of Income Tax Act, 1961) came into effect from 1.4.1984, whereas this case pertained to the Assessment Year 1983-84.

Q5: What is the overall impact of this judgment?

A5: It provides clarity on the treatment of various expenses for tax purposes, particularly in cases of modernization and dispute resolution, and reinforces the importance of timing in the application of tax laws.

1. The Income Tax Appellate Tribunal, Ahmedabad Bench-A has referred the following five questions for the opinion of this Court under Sec. 256(1) (of Income Tax Act, 1961) (the Act) at the instance of the Commissioner of Income Tax.

1. Whether the Appellate Tribunal is right in law and on facts in deleting the disallowance of Rs. 18,18,429/- being the debenture issue expenses, wherein the CIT(A) had held that it is of a capital nature covered by Sec. 35D (of Income Tax Act, 1961) ?

2. Whether the Appellate Tribunal is right in law and on facts in allowing the weighted deduction regarding commission paid to Indian Agents to the extent of export sales?

3. Whether the Appellate Tribunal is right in law and on facts in deleting the addition of Rs. 6,37,885/- made by the way of adjustment entry in the municipal tax expenses account?

4. Whether the Appellate Tribunal is right in law and on facts in allowing deduction of legal expenses of Rs. 10,043/- and Rs. 13,500/- being expenses attributable to issue of debentures as revenue expenditure?

5. Whether the Appellate Tribunal is right in law and on facts in deleting disallowance of Rs. 1,48,358/- made u/s. 43B (of Income Tax Act, 1961) in respect of municipal tax and education cess?

2. The Assessment Year is 1983-84, while the relevant account period is year ended on 30.6.1982. The assesee is a limited company running a Textile Mill with a Rubber Division.

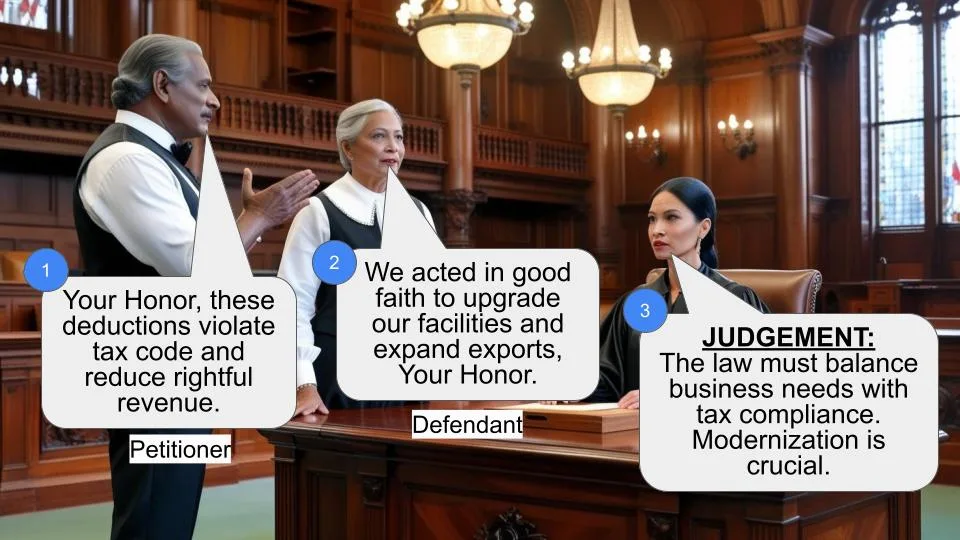

3. The assessee claimed debenture issue expenses of Rs. 18,18,429/-. Simultaneously, legal expenses of Rs. 10,043/- and Rs. 13,500/- being expenses attributable to issue of debentures were claimed as revenue expenses. These issues have been referred by way of questions Nos. 1 & 4 and hence they are taken up together. The case of the assessee was that the expenses were relatable to working capital and hence, being revenue expenditure, were allowable as a deduction in light of the Supreme Court decision in the case of India Cements Ltd. vs. Commissioner of Income-Tax, Madras, reported in (1966) 60 ITR 52. In the assessment order the claim was disallowed on the ground that the expenses in question were liable to be amortized in light of provisions of Sec. 35-D (of Income Tax Act, 1961). The Commissioner (Appeals) confirmed the disallowance. However, the Tribunal has allowed the deduction by referring to the decision of the Apex Court as well as sub-section (6) of Sec. 35-D (of Income Tax Act, 1961).

4. Mr. M.R. Bhatt learned Senior Counsel appearing on behalf of the applicant- Revenue submitted that taking into consideration the provisions of Sec. 35 (of Income Tax Act, 1961)- D(2)(c)(iv) of the Act, once the expenses related to or were in connection with issue of debentures of the assessee-company, the amount was allowable only to the extent of 1/10th under Sec. 35-D (of Income Tax Act, 1961) and balance was not allowable in the year under consideration. The learned advocate for respondent – assessee relied on order of the Tribunal.

5. Section 35-D (of Income Tax Act, 1961) stipulates under sub- section(1) of allowing only 1/10th of expenditure for each of the 10 successive previous years beginning with the previous year in which the business commences or, as the case may be, the previous year in which extension of Industrial Undertaking is completed or new Industrial Unit commences production or operation. Sub-section(2) of Sec. 35-D (of Income Tax Act, 1961) enumerates different kinds of expenditure which can be considered for the purpose of deduction under sub- sec.(1) of Sec. 35-D (of Income Tax Act, 1961). However, before the provisions can be applied to the case of an assessee it has to be shown that the expenditure in question has been incurred either (1) before commencement of business, or; (2) after the commencement of business, but in connection with extension of Industrial Undertaking or in connection with setting up a new Industrial Unit. In the facts of the present case, the Tribunal has recorded, and there is no dispute on this count, that the expenditure in question is for the purposes of working capital in course of modernisation of the existing plant and machinery.

Therefore, this is not a case which can fall within clause(i) of sub-section (1) of Section 35-D (of Income Tax Act, 1961), nor are the conditions stipulated by clause (ii) of sub-section (1) of Sec. 35-D (of Income Tax Act, 1961) fulfilled.

There is no finding that this expenditure was for extension of existing Industrial Undertaking or setting up a new unit after commencement of the business. A faint suggestion was made on behalf of the revenue that in absence of such a finding the question should not be answered and the matter be left open so as to be decided by the Tribunal in accordance with law. However, when one considers the finding of the Tribunal that the expenditure has been incurred during the course of a modernisation programme, there is no question of invoking provisions of Sec. 35-D (of Income Tax Act, 1961) and hence, it is not necessary to return the question unanswered.

6. In the facts and circumstances of the case, Questions Nos. 1 and 4 are answered in the affirmative, that is, in favour of assessee and against the revenue.

7. In so far as the question no. 2 is concerned, question itself indicates that commission was paid to Indian Agents based on the extent of export sales. The Tribunal has merely relied upon the assessee's own case for the Assessment Year 1974-75. However, Mr. Bhatt invited attention to the Apex Court's decision in the case of Commissioner of Income Tax vs. Stepwell Industries Ltd & Ors., reported in (1997)228 ITR 171 to point out that in similar circumstances commission paid to State Trading Corporation was held to be disallowable despite the fact that there were export sales in the said case.

The learned advocate for respondent – assessee has placed reliance on the fact that export sales has taken place and hence, according to the learned advocate the deduction was allowable under Section 35-B (of Income Tax Act, 1961) without any disallowance on this count.

8. The contention raised on behalf of assessee has been answered by the Apex Court in the following terms:

“If the State Trading Corporation incurs expenditure for an advertisement or publicity outside India, the assessee will not be entitled to any deduction unless the assessee can establish that the advertisement or publicity was being done outside India for and on behalf of the assessee and in respect of goods the assessee deals in or provides in the course of his business. Likewise, if the State Trading Corporation maintains a branch office or agency for the promotion of sale outside India, the assessee cannot claim any deduction on account of maintenance of such branch office or agency but if such branch office or agency is maintained by the assessee himself for the promotion of sale outside India of his goods, services or facilities, then the assessee will be entitled to a deduction under section 35B (of Income Tax Act, 1961).”

9. Applying the ratio of the Apex Court's decision in the case of Commissioner of Income Tax vs. Stepwell Industries Ltd & Ors. (supra), question no. 2 is answered in the negative, that is, in favour of Revenue and against the assessee.

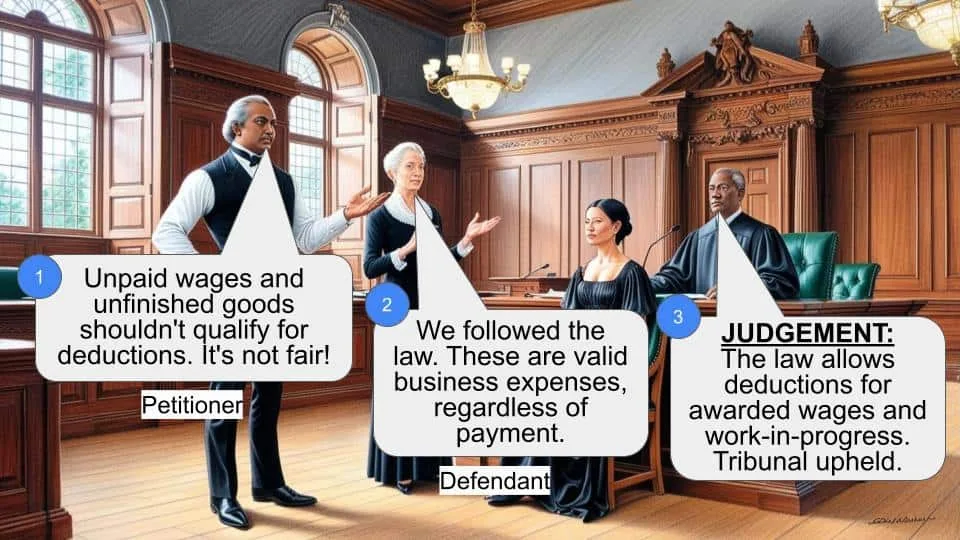

10. In so far as the question no. 3 is concerned, the facts recorded by the Tribunal show that deduction of Rs. 6,37,885/- was claimed on the basis of provision for Municipal Tax as per bills for Assessment Year 1974-75 to 1980-81. However, the assessee disputed the liability and filed various suits in the Civil Court. The suits came to be withdrawn and the matter was referred to Arbitration subject to the condition that 65% of outstanding liability be paid to the Municipal Corporation. In relation to the balance outstanding liability provisions of Sec. 41 (of Income Tax Act, 1961) were invoked by the Assessing Officer and confirmed by the CIT (Appeals). However, the Tribunal has held that provisions of Sec. 41 (of Income Tax Act, 1961) are not applicable.

11. On facts, it is apparent that the assessee disputed its liability qua the bills raised and such liability continued to exist, in the first instance during the pendency of Court cases and thereafter due to pendency of Arbitration proceedings. Mere withdrawal of Court cases and submitting the disputes to Arbitration would, in no case, amount to cessation of liability, which is the pre-requisite condition, for applying the provisions of Sec. 41 (of Income Tax Act, 1961). The Tribunal has rightly come to the conclusion that in absence of cessation of liability Sec. 41 (of Income Tax Act, 1961) cannot be made applicable.

12. Accordingly, question no. 3 is answered in affirmative, that is, in favour of the assessee and against the revenue.

13. In so far as question no. 5 is concerned, the same pertains to disallowance under sec. 43-B (of Income Tax Act, 1961) in relation to the Municipal Tax and Education Cess. Mr. Bhatt has very fairly pointed out that Sec. 43-B (of Income Tax Act, 1961) has been made applicable with effect from 1.4.1984 and hence cannot be made applicable for Assessment Year 1983-84. Hence, in absence of any infirmity in the impugned order of Tribunal, question no. 5 is answered in the affirmative, that is, in favour of assessee and against the revenue.

14. The Reference is answered accordingly in relation to all the five questions, and hence, stands disposed of with no order as to costs.

(D.A. MEHTA, J.)

(Z.K. SAIYED, J.)

×

Similar Ripples

Questions

Court Rules on Tax Deductions: Modernization Expenses Allowed, Agent Commissions Disallowed

Write your CommentSimilar Posts

Generic

- Reportdata/4831.pdf