Court Sides with Revenue on Depreciation and Toll Road Classification

Full News

Court Sides with Revenue on Depreciation and Toll Road Classification

Court Sides with Revenue on Depreciation and Toll Road Classification

This case involves an appeal by the Commissioner of Income Tax against West Gujarat Expressway Ltd. The main issues were about granting depreciation on assets not owned by the respondent and classifying toll roads as plant and machinery. The court ruled in favor of the Revenue (tax authorities) on both questions.

Get the full picture - access the original judgement of the court order here

Case Name

Commissioner of Income Tax vs. West Gujarat Expressway Ltd. (High Court of Bombay)

Income Tax Appeal No. 2190 of 2013

Date: 5th April 2016

Key Takeaways

- The court ruled against allowing depreciation on assets not owned by the assessee.

- Toll roads were determined not to be classified as plant and machinery for tax purposes.

- This decision aligns with a previous case (Income Tax Appeal No.2357 of 2013) on the same issues.

Issue

The central legal questions in this case were:

- Can depreciation be granted on assets not owned by the respondent under Section 32 (of Income Tax Act, 1961)?

- Should toll roads be treated as plant and machinery for tax purposes according to Rule 5 (of Income Tax Rules, 1962)?

Facts

- This appeal (we don’t have the exact number) was heard alongside Income Tax Appeal No.2357 of 2013.

- The case relates to the Assessment Year 2008-09.

- The Tribunal (a lower court) had previously made a decision that the Revenue (tax authorities) disagreed with.

- The Tribunal’s decision for this case followed its order for the Assessment Year 2007-08, which was challenged in the other appeal (No.2357 of 2013).

Arguments

Unfortunately, the connected document doesn’t provide detailed arguments from each side. However, we can infer that:

- The Revenue (appellant) argued that:

- Depreciation shouldn’t be allowed on assets not owned by the respondent.

- Toll roads shouldn’t be classified as plant and machinery for tax purposes.

2. The Respondent (West Gujarat Expressway Ltd.) likely argued the opposite:

- They should be granted depreciation on the assets in question.

- Toll roads should be considered plant and machinery for tax benefits.

Key Legal Precedents

The main precedent mentioned in this case is the court’s decision in Income Tax Appeal No.2357 of 2013. This earlier case dealt with the same issues for a different assessment year (2007-08). The court followed the reasoning from that case in making its decision here.

Judgement

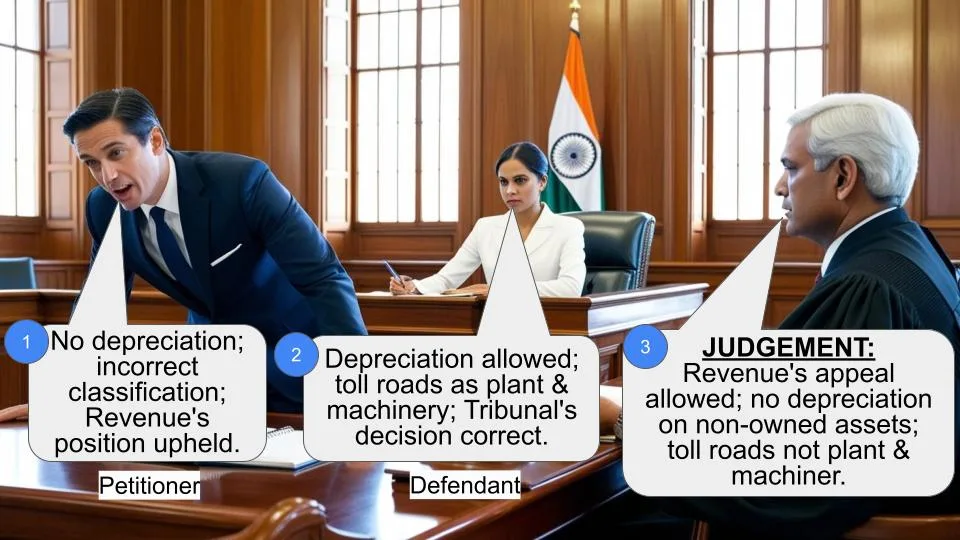

- The court answered both questions in favor of the Revenue (appellant) and against the Respondent (assessee).

- They decided that:

- The Tribunal was wrong in directing the Assessing Officer to grant depreciation on assets not owned by the Respondent.

- The Tribunal was incorrect in treating toll roads as plant and machinery.

3. The appeal was disposed of based on these decisions.

4. No order was made regarding costs.

FAQs

Q: What does this decision mean for West Gujarat Expressway Ltd.?

A: It means they likely won’t be able to claim depreciation on certain assets and won’t get tax benefits from classifying toll roads as plant and machinery.

Q: Why did the court refer to another case (Appeal No.2357 of 2013)?

A: That case dealt with the same issues for a different tax year. Courts often rely on previous decisions to maintain consistency in their rulings.

Q: What’s the significance of Section 32 (of Income Tax Act, 1961)?

A: Section 32 (of Income Tax Act, 1961) deals with depreciation in tax calculations. The court’s decision suggests a strict interpretation of this section, only allowing depreciation on owned assets.

Q: How might this decision affect other companies in similar situations?

A: Other companies with similar tax structures or those operating toll roads might need to reassess their tax strategies based on this ruling.

Q: Can West Gujarat Expressway Ltd. appeal this decision?

A: While the document doesn’t mention it, generally, decisions from High Courts can be appealed to the Supreme Court if there’s a substantial question of law involved.

1. This Appeal was heard along with Income Tax Appeal No.2357 of 2013. The impugned order dated 21st March, 2013 for A.Y. 200809 of the Tribunal follows its order rendered for A.Y. 200708 which was a subject matter of challenge before this Court in Income Tax Appeal No.2357 of 2013.

2. In the above view, only the following two questions of law are pressed by the Revenue for our consideration:

“(i) Whether on the facts and in the circumstances of the case and in law, the Tribunal was right in directing the AO to grant depreciation on assets not owned by the Respondent that goes against provisions of Section 32 (of Income Tax Act, 1961)?

(ii) Whether on the facts and in the circumstances of the case and in law, the Tribunal was right in its decision of treating toll roads as plant and machinery, when this is not as per rule 5 of New Appendix I of the I.T. Rules?”

3. We have today by a separate speaking order in Income Tax Appeal No.2357 of 2013, disposed of the two substantial questions of law raised for our consideration by answering them in the negative i.e. in favour of the AppellantRevenue and against the RespondentAssessee. Thus following the same in this Appeal we answer the identical questions raised in this Appeal in the negative i.e. in favour of the AppellantRevenue and against the RespondentAssessee.

4. The Appeal is disposed of in the above terms. No order as to costs.

(A. K. MENON, J.) (M. S. SANKLECHA, J.)

×

Similar Ripples

Questions

Court Sides with Revenue on Depreciation and Toll Road Classification

Write your CommentSimilar Posts

Generic

- Reportdata/2933.pdf