Court Upholds Deduction for Scientific Research Company, Limits Assessing Offic…

Full News

Court Upholds Deduction for Scientific Research Company, Limits Assessing Officer's Power

Court Upholds Deduction for Scientific Research Company, Limits Assessing Officer's Power

This case involves an appeal by the revenue department against Quintiles Research (India) Private Limited regarding a tax deduction claim under Section 80-IB(8A) (of Income Tax Act, 1961) for the Assessment Year 2008-09. The High Court dismissed the appeal, ruling in favor of the assessee (Quintiles Research) and upholding the decision of the Income Tax Appellate Tribunal.

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs Quintiles Research (India) Private Limited (High Court of Karnataka)

ITA No.282 of 2014

Date: 14th October 2020

Key Takeaways:

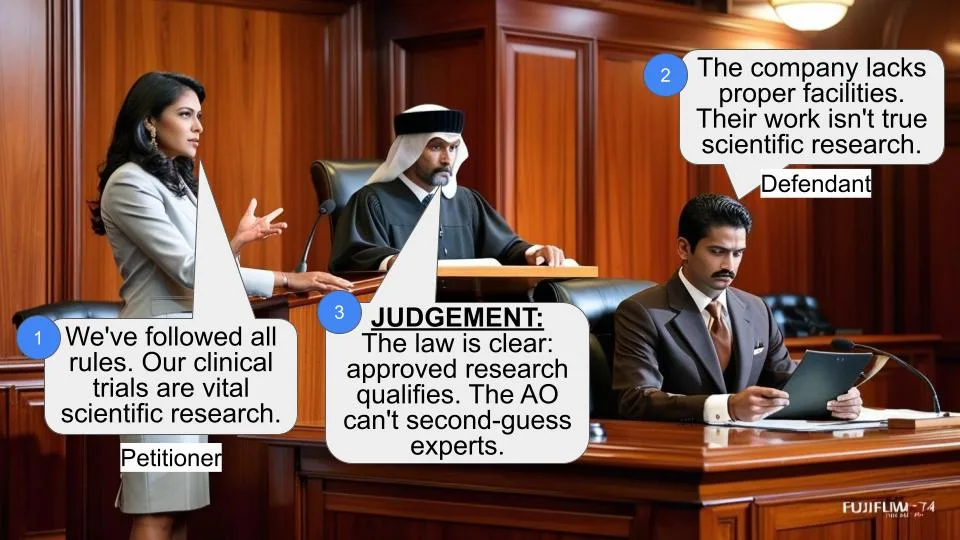

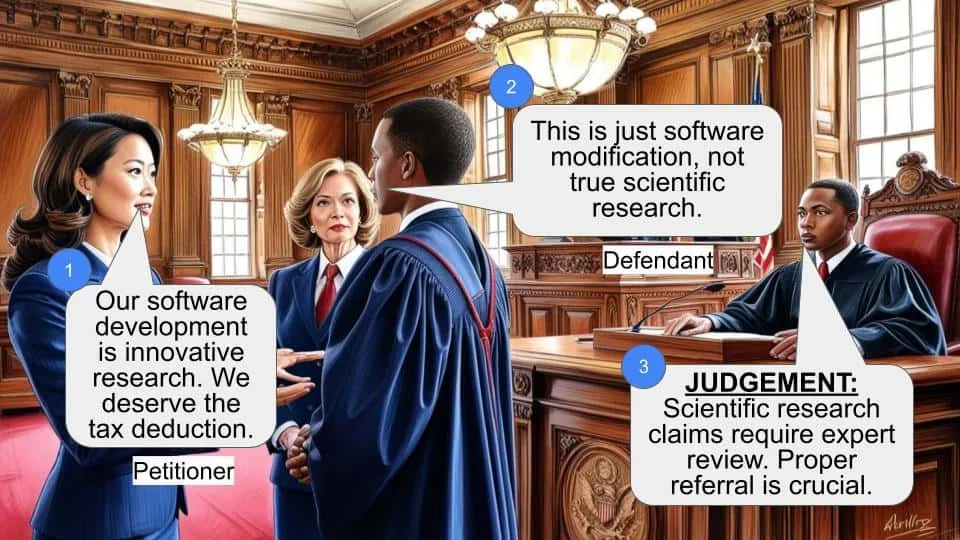

1. Once approval is granted by the prescribed authority for deduction under Section 80-IB(8A) (of Income Tax Act, 1961), the Assessing Officer cannot re-examine the fulfillment of conditions.

2. The prescribed authority (Secretary, Department of Scientific and Industrial Research) is the expert body to assess compliance with scientific research requirements.

3. Clinical trials fall within the scope of "scientific research" for tax deduction purposes.

Issue:

Whether the Income Tax Appellate Tribunal was correct in holding that only the prescribed authority, and not the Assessing Officer, can examine the conditions of Rule 18DA(8A) (of Income Tax Rules, 1962) for allowing deduction under Section 80-IB(8A) (of Income Tax Act, 1961)?

Facts:

1. Quintiles Research (India) Private Limited is engaged in pharmaceutical research and development and clinical research.

2. For the Assessment Year 2008-09, the company claimed a deduction of Rs. 31,32,49,090/- under Section 80-IB(8A) (of Income Tax Act, 1961).

3. The Assessing Officer disallowed the claim, stating that the company was not undertaking scientific research and development on its own.

4. The company appealed to the Dispute Resolution Panel, which rejected their objections.

5. The Income Tax Appellate Tribunal allowed the company's appeal, setting aside the Assessing Officer's order.

Arguments:

Revenue's Arguments:

1. The assessee lacks adequate infrastructure for scientific research and development.

2. The company's activities don't qualify as scientific research and development under Rule 18DA(1)(c) (of Income Tax Rules, 1962).

3. The Assessing Officer is competent to verify compliance with Rule 18DA (of Income Tax Rules, 1962) conditions.

Assessee's Arguments:

1. The company has been granted approval, which has been renewed multiple times.

2. Clinical trials fall within the definition of "scientific research".

3. Once approval is granted by the prescribed authority, the Assessing Officer cannot re-examine the conditions.

Key Legal Precedents:

1. 'PRINCIPAL COMMISSIONER OF INCOME-TAX-1 VS. B.A.RESEARCH INDIA LTD.', (2016) 70 TAXMANN.COM 268 (GUJARAT)

2. 'TEJAS NETWORKS LTD. VS. DEPUTY COMMISSIONER OF INCOME-TAX, CIRCLE 12(4), BENGALURU', (2015) 60 TAXMANN.COM 309 (KARNATAKA)

3. 'GESTETNER DUPLICATORS PVT. LTD. VS. COMMISSIONER OF INCOME-TAX', (1979) 1 TAXMAN 1 (SC)

4. 'COMMISSONER OF INCOME-TAX VS. PARRYS (EASTERN) (P.) LTD.', (1989) 42 TAXMANN 62 (BOM)

Judgement:

The High Court dismissed the revenue's appeal, ruling in favor of Quintiles Research. Key points of the judgment:

1. Once approval is granted by the prescribed authority under Rule 18D (of Income Tax Rules, 1962), it's not open for the Assessing Officer to re-examine the fulfillment of conditions in Rule 18DA (of Income Tax Rules, 1962).

2. The prescribed authority is a specialized body with expertise in scientific research and development.

3. The Tribunal correctly held that any violation of Rule 18DA (of Income Tax Rules, 1962) conditions can only be examined by the prescribed authority, not the Assessing Officer.

FAQs:

1. Q: What is Section 80-IB(8A) (of Income Tax Act, 1961)?

A: It provides a 100% tax deduction for companies carrying out scientific research and development, subject to certain conditions.

2. Q: Who is the prescribed authority for approving companies under this section?

A: The Secretary, Department of Scientific and Industrial Research, Ministry of Science and Technology, Government of India.

3. Q: Can the Assessing Officer challenge the prescribed authority's approval?

A: No, the court ruled that once approval is granted, the Assessing Officer cannot re-examine the fulfillment of conditions.

4. Q: Does clinical research qualify as scientific research under this section?

A: Yes, the court affirmed that clinical trials fall within the scope of "scientific research" for tax deduction purposes.

5. Q: How long is the approval valid for?

A: Initially for three years, with the possibility of extension for another three years, up to a total of ten consecutive assessment years.

This appeal under Section 260A (of Income Tax Act, 1961) (hereinafter referred to as the Act for short) has been preferred by the revenue. The subject matter of the appeal pertains to the Assessment year 2008-09. The appeal was admitted by a bench of this Court vide order dated 09.06.2015 on the following substantial question of law:

Whether, on the facts and in the circumstances of the case, the Tribunal is right in law in holding that the conditions of Rule 18DA(8A) (of Income Tax Rules, 1962) can be looked into only by the prescribed authority and not by the Assessing Officer, whereas the said Rule prescribes the conditions necessary for allowing deduction under Section 80IB (of Income Tax Act, 1961)-8A of the Income Tax Act and the Assessing Officer is well within his jurisdiction to accept or reject the same based on the conformity adhered to by the assessee?

2. In order to appreciate the factual context, in which the aforesaid substantial question of law arises for our consideration in this appeal, reference to a few facts is necessary. The assessee is a company, which is engaged in the pharmaceutical research and development as well as clinical research for pharmacy products. The assessee filed the return of income for the Assessment Year 2008-09 and claimed deduction of Rs.31,32,49,090/- under Section 80-IB(8A) (of Income Tax Act, 1961). The Assessing Officer vide order dated 15.10.2012, inter alia by taking into account the Work Orders dated 31.08.2006 and 13.11.2007 inter alia held that assessee is not undertaking any scientific research and development on its own as specified under Rule 18DA(1)(c) (of Income Tax Rules, 1962). It was further held that assessee has not been able to sell any output / prototype till date and undertakes the activities as specified in the agreement and transfer the data / information to the customer who in turn may use the same to develop a technology product / patent and the assessee itself is not engaged in Scientific, Research & Development activities leading to development / improvement/ transfer of technology. Thus, it was held that the assessee does not meet the prescribed conditions under Rule 80-IB(8A) (of Income Tax Rules, 1962). Accordingly, the claim of the assessee for deduction under the aforesaid provision was disallowed.

3. Being aggrieved, the assessee approached the Dispute Resolution Panel. The Dispute Resolution Panel vide order dated 03.09.2012 rejected the objections of the assessee. Being aggrieved, the assessee approached the Income Tax Appellate Tribunal (hereinafter referred to as 'the Tribunal' for short). The Tribunal by an order dated 21.02.2014 allowed the appeal preferred by the assessee and set aside the order of the Assessing Officer and remitted the question of determination of the question of Arm’s Length Price (ALP) to the Transfer Pricing Officer (TPO) for fresh consideration. In the result, the appeal was partly allowed. In the aforesaid factual background, this appeal has been filed.

4. Learned counsel for the revenue while inviting the attention of this court to provisions of Section 80-IB(8A) (of Income Tax Act, 1961) as well as Rule 18DA(1)(c) (of Income Tax Rules, 1962) and submitted that the assessee is not entitled to deduction under the aforesaid provision as the assessee does not have adequate infrastructure such as laboratory facility, qualified manpower, scale of facilities and prototype development facilities for undertaking scientific research and development of its own. It is further submitted that without establishing laboratory facilities and necessary instruments / equipments it is not possible for the assessee to engage in scientific research and development. It is also pointed out that infrastructure facility referred to by the assessee in Bangalore, Mumbai and Ahmedabad is only an office space and not a facility that supports scientific research and development activity. It is contended that the assessee has entered into agreement with various hospitals to utilize their facilities / infrastructure and the phrase used in Rule 18DA(1)(c) (of Income Tax Rules, 1962) is of its own and not on its own. It is also submitted that the assessee has not obtained prior permission of the prescribed authority to sell and prototype of output, if any, from its laboratories or pilot plans and therefore, condition contained in Rule 18DA(2) (of Income Tax Rules, 1962) is not complied with. It is also pointed out with reference to the agreement entered into by the assessee that the assessee’s responsibilities under the agreement were to deal with regulatory authorities, preparation of protocol, study materials and identification of laboratory / investigation sites etc. and aforesaid services cannot be equated with undertaking scientific research and development of its own in terms of Rule 18DA(1)(c) (of Income Tax Rules, 1962). Our attention has also been invited to Clause 17 of the Agreement and it is pointed out that the provisions of the agreement clearly indicate that the assessee was not undertaking any scientific research and development of its own as specified in Rule 18DA(1)(c) (of Income Tax Rules, 1962) and Sub-Rule (2) of Rule 18D (of Income Tax Rules, 1962). Reference has also been made to Section 43(4) (of Income Tax Act, 1961), and it has been contended that scientific research connotes any activity for extension of knowledge in the fields of natural or applied sciences and the assessee is not contributing to expansion of such knowledge through its activities and earnings of the assessee are more in the nature of job charges and therefore, assessee is not entitled for deduction.

5. It is also argued that Tribunal has failed to appreciate that the assessee was not engaged exclusively in scientific research and development activities and only provided certain services based on the requirement of the client and there was no output generated which is owned or in respect of which assessee can exercise rights. It is also contended that Tribunal failed to appreciate that assessee does not develop, improve or transfer technology owned by it and therefore, conditions mentioned in Rule 18DA(1)(e) (of Income Tax Rules, 1962) are not satisfied. Our attention has also been invited to Memorandum explaining the provisions of Section 80-IB(8A) (of Income Tax Act, 1961) introduced by Finance (No.2) Bill, 1996 which specifically states that deduction has to be allowed to an undertaking carrying out scientific research and development but in the instant case, from the material on record, it is evident that the assessee was dealing with regulatory authorities, preparation of protocol and study materials, identification of laboratory / investigation sites etc. It is also urged that Tribunal ignored the findings of the assessing authority and Dispute Resolution Panel with regard to clauses in the agreement. It is also submitted that Assessing Officer is competent to ascertain whether conditions mentioned in Rule 18DA (of Income Tax Rules, 1962) are complied with or not. Alternatively, it is submitted that the Tribunal should have directed the assessing authority to send a report to prescribed authority for reporting violation and the prescribed authority after examining the issue of violation, could have taken appropriate action and the assessing authority could have passed a final order of assessment in the light of the action, which may have been taken by the prescribed authority. It is also urged that exemption notification of clause should be strictly construed. In support of aforesaid submissions, reliance has been placed on decision of Supreme Court in ‘COMMISSIONER OF CUSTOMS (IMPORT) MUMBAI VS. DILIP KUMAR AND CO.’, (2018) 68 GST 239 as well as a decision of this court in ‘COMMISSIONER OF INCOME TAX AND ANOTHER VS. MANIPAL ACADEMY OF HIGHER EDUCATION’, 357 ITR 114.

6. On the other hand, learned Senior counsel for the assessee while inviting our attention to provisions of Section 80-IB(8A) (of Income Tax Act, 1961) submitted that admittedly, conditions mentioned in Clauses (i) to (iii) are complied with and the dispute is only with regard to compliance with conditions mentioned in Clause (iv). Reference has also been made to Rule 18D (of Income Tax Rules, 1962) and Rule 18DA (of Income Tax Rules, 1962), which deals with prescribed authority for approval of companies carrying on scientific research and development and prescribed conditions for deduction under Sub-Section (8)(a) of Section 80-IB (of Income Tax Act, 1961) respectively. It is also submitted that the claim under Section 80-IB(8A) (of Income Tax Act, 1961) is allowed upto 2007-08 which is evident from para 24 of the order passed by the Tribunal. It is also pointed out that renewal has been granted to the assessee in the year 2006, 2009 and 2012 as well. Reference has also been made to findings recorded by the Tribunal and it is pointed out that admittedly, the assessee has been granted approval, which has been renewed from time to time. It is also pointed out that no substantial question of law has been framed with regard to findings recorded by the Tribunal in paragraphs 27, 28 and 30 of the order and the substantial question of law has been framed only with regard to finding recorded by the Tribunal in paragraph 81 of the judgment. It is also urged that clinical trials fall within the expression ‘scientific research’ and the finding recorded by the Tribunal is based on meticulous appreciation of evidence on record. It is also argued that once the approval has been granted by the prescribed authority, it is not open for the Assessing Authority to examine whether or not the conditions have been fulfilled by the assessee. It is urged that the issue that the substantial question of law involved in this appeal is no longer res integra and has been answered by High Court of Gujarat in ‘PRINCIPAL COMMISSIONER OF INCOME-TAX-1 VS. B.A.RESEARCH INDIA LTD.’,

(2016) 70 TAXMANN.COM 268 (GUJARAT). In support of aforesaid submissions, reliance has been placed on decisions in ‘TEJAS NETWORKS LTD. VS. DEPUTY COMMISSIONER OF INCOME-TAX, CIRCLE 12(4), BENGALURU’, (2015) 60 TAXMANN.COM 309 (KARNATAKA), ‘GESTETNER DUPLICATORS PVT. LTD. VS. COMMISSIONER OF INCOME-TAX’, (1979) 1 TAXMAN 1 (SC) and ‘COMMISSONER OF INCOME-TAX VS. PARRYS (EASTERN) (P.) LTD.’, (1989) 42 TAXMANN 62 (BOM).

7. We have considered the submissions made by learned counsel for the parties and have perused the record. Section 80-IB (of Income Tax Act, 1961) provides for deduction in respect of profits and gains from certain industrial undertakings other than infrastructure development undertakings. Before proceeding further, we may take note of the relevant statutory provisions viz., Section 80-IB(8A) (of Income Tax Act, 1961), Rule 18D (of Income Tax Rules, 1962) and Rule 18DA (of Income Tax Rules, 1962), which read as under:

Section 80-IB(8A)(8A) (of Income Tax Act, 1961)The amount of deduction in the case of any company carrying on scientific research and development shall be hundred per cent of the profits and gains of such business for a period of ten consecutive assessment years, beginning from the initial assessment year, if such company—

(i) is registered in India;

(ii) has its main object the scientific and industrial research and development;

(iii) is for the time being approved by the prescribed authority at any time after the 31st day of March, 2000 but before the 1st day of April, 2007;

(iv) fulfils such other conditions as may be prescribed.

From perusal of the aforesaid provision, it is evident that the case of a company falling on scientific research and development, there would be 100% deduction of the profits and gains of such business for a period of 10 consecutive Assessment Years subject to the condition that the company satisfied the conditions enumerated in sub-Section (8A) of Section 80-IB (of Income Tax Act, 1961).

Rule 18D (of Income Tax Rules, 1962)

Rule 18D(1) (of Income Tax Rules, 1962) For the purposes of sub- section (8A) of section 80-IB (of Income Tax Act, 1961), the prescribed authority shall be the Secretary, Department of Scientific and Industrial Research, Ministry of Science and Technology, Government of India.

(2) The prescribed authority shall initially grant approval to a company carrying on scientific research and development for a period of three assessment years and subject to satisfactory performance of that company on periodic review extend the said approval for a further period of three assessment years so that the total period of approval is for ten consecutive assessment years, beginning from the initial assessment year.

Sub-Rule (1) of Rule 18D (of Income Tax Rules, 1962) specifies the prescribed authority, whereas, sub-Rule (2) of Rule 18D (of Income Tax Rules, 1962) provides that prescribed authority shall initially grant approval to a company for a period of 3 Assessment Years and subject to satisfaction of the satisfactory performance of the company, on period review, extend the approval for a period of three Assessment Years so that total period of approval is for 10 consecutive Assessment Years beginning from initial Assessment Year.

Rule 18DA (of Income Tax Rules, 1962)

18DA. (1) Any company carrying on scientific research and development shall be eligible for deduction specified in sub-section (8A) of section 80-IB (of Income Tax Act, 1961), if such company—

(a) is registered in India;

(b) has its main object the scientific and industrial research and development;

(c) has adequate infrastructure such as laboratory facilities, qualified manpower, scale-up facilities and prototype development facilities for undertaking scientific research and development of its own;

(d) has a well formulated research and development programme comprising of time bound research and development projects with proper mechanism for selection and review of the projects or programme;

(e) is engaged exclusively in scientific research and development activities leading to technology development, improvement of technology and transfer of technology developed by themselves;

(f) submits the annual return alongwith statement of accounts and annual report within eight months after the close of each accounting year to the prescribed authority.

(2) Every company which is approved under sub-rule (2) of rule 18D (of Income Tax Rules, 1962) shall—

(a) sell any prototype or output, if any, from its laboratories or pilot plants with the prior permission of the prescribed authority;

(b) intimate the change, if any, in its memorandum of association and articles of association relating to its main objects and forward the altered copy of its memorandum of association and articles of association to the prescribed authority;

(c) apply for extension of the approval at least three months before expiry of the approval already granted by the prescribed authority;

(d) have a system of monitoring the cost of research and development projects.

(3) If, at any stage, it is found that—

(a) the approval granted to the company referred to in sub-rule (2) of rule 18D (of Income Tax Rules, 1962) is to avoid payment of taxes by its group companies or companies related to its directors or majority of its shareholders;

(b) any provisions of the Act or the rules have been violated, the prescribed authority specified may withdraw the approval so granted.

(4) Every company referred to in sub-rule (1) shall make an application to the prescribed authority for the purposes of obtaining approval.

(5) Every application referred to in sub- rule (4) shall be accompanied by—

(a) memorandum of association and articles of association incorporating all amendments duly certified by the company secretary or managing director of the company;

(b) annual report of the company for the last three years, if available;

(c) photocopies of the memorandum of understanding relating to all on- going and future sponsored research projects or programmes.

(6) The prescribed authority may call for any information or document which may be necessary for consideration of the grant of approval under sub-rule (2) of rule 18D (of Income Tax Rules, 1962).

(7) The prescribed authority shall grant approval within four months from the date of receipt of the application :

Provided that where the approval is not granted, the decision of the said authority shall be communicated to the applicant within the said period of four months :

Provided further that no approval shall be refused unless the applicant has been given an opportunity of being heard.

8. From a conjoint reading of Rule 18D (of Income Tax Rules, 1962) and Rule 18DA (of Income Tax Rules, 1962), it is axiomatic that it is for the prescribed authority to examine the nature of research and scientific development proposed to be or being carried out by the company who seeks approval or extension of approval. Once under sub-rule (2) approval is granted which enures for a period of three years, it can be extended only on satisfactory performance of the company, which has to be assessed on periodic review by the prescribed authority. The prescribed authority is also empowered to call for such information or documents, which may be found necessary for consideration of application for grant of approval. Even during the currency of approval granted by the prescribed authority, the company has to satisfy several conditions in terms of Rule 18DA(2) (of Income Tax Rules, 1962). The prescribed authority is also empowered to withdraw the approval. Thus, the statutory scheme of the Rules mandates the prescribed authority to be a body, which can minutely examine the highly technical and scientific requirements in case of a company. Therefore, once the prescribed authority grants approval and such approval holds the field, it would not be open to the Assessing Officer or any other revenue authority to sit in appeal over such approval certificate and re-examine the issue of fulfillment of conditions mentioned in Sub-Rule (1) of Rule 18DA (of Income Tax Rules, 1962). The prescribed authority is a specialized body having expertise in the field of scientific research and development and the requirements being extremely complex, scientific requirements have therefore, being rightly placed in the hands of the expert body. There appears to be no plausible reason as to why Assessing Officer should be allowed to sit in appeal over the decision of a body, which is prescribed under the Rules. In this connection, reference may be made to Section 85C (of Income Tax Act, 1961) also, which deals with deduction of tax on royalties etc. received from certain foreign companies. The assessee in order to claim the benefit of deduction under Section 85C (of Income Tax Act, 1961) was required to obtain approval of the Central Government in respect of an agreement and once the approval is granted by the Central Government, and Central Government satisfies itself that the other company is a foreign company and the services required to be furnished by the assessee to the other company were technical services, the authorities under the Act ought to have proceeded accordingly. The aforesaid view was taken by High Court of Bombay in Parry’s (Eastern) (P.) Ltd. supra. Thus, once the approval is granted by prescribed authority and such approval is valid, it would be no longer be open to the Assessing Officer to verify the satisfaction of the conditions prescribed under Rule 18DA (of Income Tax Rules, 1962) in order to refuse deduction under Sub-Section (8A) of Section 80-IB (of Income Tax Act, 1961).

9. The Tribunal, in the instant case, has examined the issue on merits and has held that Rules clearly contemplate even sponsored research program and the entire receipts of the assessee are from contract research and not of own research. It has further been held that any issue with regard to violation of conditions mentioned in Rule 18DA (of Income Tax Rules, 1962) can be looked into only by the prescribed authority and therefore, the Assessing Officer erred in disallowing the deduction. The Tribunal has rightly held that issue with regard to violation of conditions mentioned in Rule 18DA (of Income Tax Rules, 1962) can be looked into only by the prescribed authority and not by the Assessing Officer. Admittedly, the approval was granted to the assessee, which was renewed from time to time, therefore, the question of remand does not arise in the facts of the case. We are in respectful agreement with the view taken by the High Court of Gujarat in case of B.A.RESEARCH INDIA LTD supra.

In view of preceding analysis, the substantial question of law framed by a bench of this court is answered against the revenue and in favour of the assessee. In the result, appeal fails and is hereby dismissed.

Sd/-

JUDGE

Sd/-

JUDGE

×

Similar Ripples

Questions

Court Upholds Deduction for Scientific Research Company, Limits Assessing Officer's Power

Write your CommentSimilar Posts

Generic

- Reportdata/6165.pdf