Full News

Court Upholds Dismissal of Appeal Due to 3389-Day Delay, Emphasizing Importance of Timely Filing

Court Upholds Dismissal of Appeal Due to 3389-Day Delay, Emphasizing Importance of Timely Filing

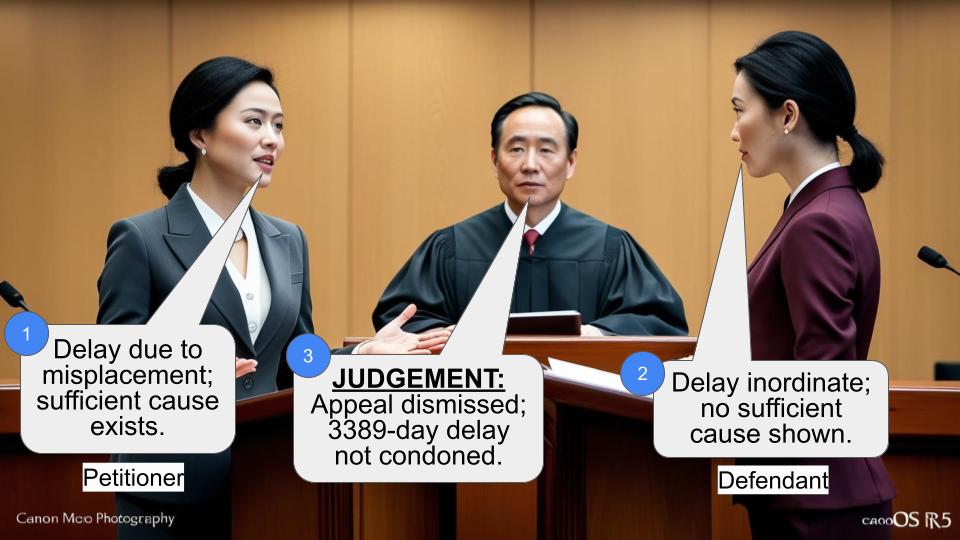

This case involves an appeal by B.J. Samson against the Assistant Commissioner of Income Tax. The appellant sought to challenge an order from the Commissioner of Income Tax (Appeals), but filed the appeal after a significant delay of 3389 days. The Income Tax Appellate Tribunal dismissed the appeal due to this delay, and the High Court upheld this decision.

Get the full picture - access the original judgement of the court order here

Case Name:

B.J. Samson vs Assistant Commissioner of Income Tax (High Court of Madras)

T.C.A.No.267 of 2016

Date: 7th June 2016

Key Takeaways:

- Courts take a serious view of inordinate delays in filing appeals.

- The burden is on the appellant to provide sufficient cause for delay.

- Negligence and lack of diligence are not considered valid reasons for condonation of delay.

- Courts balance the need for justice with the importance of timely legal proceedings.

Issue:

Should the court condone a delay of 3389 days in filing an appeal before the Income Tax Appellate Tribunal?

Facts:

- The appellant, B.J. Samson, received an adverse order from the Commissioner of Income Tax (Appeals) on 26.12.2005.

- The statutory time limit for filing an appeal before the Income Tax Appellate Tribunal is 60 days.

- The appellant filed the appeal after a delay of 3389 days.

- The appellant claimed that the order was received and misplaced by family members, and he was unaware of it due to financial problems and relocation to Mumbai.

- The Income Tax Appellate Tribunal dismissed the appeal, refusing to condone the delay.

Arguments:

Appellant’s arguments:

- The delay was due to misplacement of the order by family members.

- Financial problems and relocation to Mumbai contributed to the delay.

- The appellant was ignorant of income tax procedures.

Tax authorities’ arguments:

- The delay of 3389 days is inordinate and unexplained.

- The reasons provided are vague and general.

- The appellant showed lack of diligence in pursuing the case.

Key Legal Precedents:

- N. Balakrishnan v. M. Krishnamurthy (1998 (2) CTC 533)

- C. Subramaniam v. Tamil Nadu Housing Board (2000 (3) CTC 727)

- Esha Bhattacharjee v. Raghunathpur Nafar Academy (2013 (12) SCC 649)

- H. Dohil Constructions Company Private Limited v. Nahar Exports Limited (2015 (1) Supreme Court Cases 680)

These cases establish principles for condonation of delay, emphasizing the need for a liberal approach balanced with the need to prevent abuse of the legal process.

Judgement:

The High Court dismissed the appeal, upholding the Income Tax Appellate Tribunal’s decision. The court found that:

- The appellant failed to provide sufficient cause for the inordinate delay.

- The reasons given were vague and general.

- The appellant showed a lack of diligence in pursuing the case.

- The principles of law regarding condonation of delay were not satisfied.

FAQs:

Q: What is the time limit for filing an appeal before the Income Tax Appellate Tribunal?

A: The statutory time limit is 60 days from the date of receiving the order being appealed against.

Q: Can courts condone delays in filing appeals?

A: Yes, courts have the discretion to condone delays if sufficient cause is shown.

Q: What factors do courts consider when deciding whether to condone a delay?

A: Courts consider the length of delay, the reasons provided, the conduct of the party, and the potential prejudice to the other party.

Q: Does ignorance of law constitute a valid reason for delay?

A: Generally, ignorance of law is not considered a valid reason for condonation of delay.

Q: What lesson can be learned from this case?

A: It’s crucial to be diligent in legal matters and file appeals within the prescribed time limits. If there’s a delay, one must provide strong, specific reasons to justify it.

1. Challenge in this Tax Case Appeal, is to an order made by the Income Tax Appellate Tribunal in I.T.(SS)No.10/Mds/2015, dated 06.01.2016, by which, the Tribunal has declined to condone the delay of 3389 days in filing the appeal.

2. Short facts leading to the appeal are that during January' 2006, the order of the CIT(Appeals)-I, Chennai-34, dated 26.12.2005 was received in the absence of the appellant. Time provided for appeal is 60 days from the date of communication of the said order. Reasons assigned for condonation of delay are that the impugned order was received and misplaced by his family members,without knowing the consequences. Besides, he had several financial problems and therefore, he shifted his business to Mumbai, from 2006. Only after the receipt of the recovery notice from the Tax Recovery Officer-7, Chennai-34, dated 26.12.2014, he took steps, by consulting the Chartered Accountants, who had appeared on his behalf. Thereafter, appeal was filed under Section 158-BC (of Income Tax Act, 1961) r/w. 158-BD r/w.144 of the Income-Tax Act, 1961, with a delay of 3389 days in filing the same.

3. Adverting to the reasons assigned, the Income-Tax Appellate Tribunal, “C” Bench, Chennai, dated 06.01.2016, dismissed the appeal, as hereunder:

“The reason advanced by the assessee in its condonation petition for inordinate delay of 3389 days is very vague and too general and the reason advanced by the assessee cannot be considered as a reasonable one so as to condone the inordinate day of 3389 days. The approach of the assessee is casual and requires no sympathy from our end since the assessee has not shown good and sufficient reason to condone the delay. Accordingly by placing reliance on the order of the Third Member of the Co-ordinate Bench decision in the case of JCIT vs. Tractors & Farms Equipments Ltd [104 ITD 149], wherein it was observed as under:- The law assists those who are vigilant, not those who sleep over their rights. This principle is embodied in the dictum: vigilantibus non doemientibus jura subveniunt. The delay cannot be condoned simply because the appellant’s case is hard and calls for sympathy or merely out of benevolence to the party seeking relief. In granting the indulgence and condoning the delay, it must be proved beyond the shadow of doubt that the appellant was diligent and was not guilty of negligence, whatsoever. The sufficient cause within the contemplation of the limitation provisions must be a cause which is beyond the control of the party invoking the aid of the provisions. The cause for the delay in filing the appeal, which by due care and attention, could have been avoided, cannot be a sufficient cause within the meaning of the limitation provision. Where no negligence or inaction, or want of bonafides can be imputed to the appellant, a liberal construction of the provisions has to be made in order to advance substantial justice. Seekers of justice must come with clean hands.

Accordingly, we are inclined to dismiss the appeal of the assessee as unadmitted.

7. In the result, the appeal of the assessee in IT(SS)A No.10/Mds/2015 is dismissed.” 4. Though Mr.S.Sridhar, learned counsel appearing for the appellant assailed the correctness of the order of the Tribunal, contending inter alia that the Income-Tax Appellate Tribunal has failed to appreciate the issues raised, on merits and further contended that the Tribunal has failed to consider the decision of the Hon'ble Apex Court in Collector, Land Acquisition v. Mst.Katiji reported in (1987) 167 ITR 471 and further contended that the appellant was ignorant of the procedure, in the matter of assessment of income-tax, this Court is not inclined to accept the same.

5. Perusal of the order impugned shows that the Income Tax Appellate Tribunal, Chennai, while declining to accept the reasons, has relied on a decision in JCIT vs. Tractors & Farms Equipments Ltd reported in 104 ITD 149. Besides in the matter of condonation of delay, it is worthwhile to consider few decisions on the aspect, as follows:

(a) In N.Balakrishnan versus M.Krishnamurthy, reported in 1998 (2) CTC 5 33 , this Court held as follows:

"14. It must be remembered that in every case of delay there can be some lapse 'on the part of the litigant concerned. That alone is not enough to turn down his plea and to shut the door against him. If the explanation does not smack of mala fides or it is put-forth as part of a dilatory strategy the court must show utmost consideration to the suitor. But when there is reasonable ground to t hink that the delay was occasioned by the party delibera tely to gain time then the court should lean against acceptance of the explanation "

(b) In the Hon'ble Division Bench Judgment of our High Court, in C.Subramaniam versus Tamil Nadu Housing Board rep. by its Chairman And Managing Director, reported 2000 (3) CTC 727 = 2000 3 L.W. 938, the position has been stated, as hereunder.

“31. To turn up the legal position, (1) the work "sufficient cause" should receive liberal construction to do substantial justice; (2) what is "sufficient cause" is a question of fact in a given circumstances of the case; (3) it is axiomatic that condonation of delay is discretion of the Court; (4) length of delay is no matter, but acceptability of the explanation is the only criterion' (5) once the Court accepts the explanation as "sufficient", it is the result of positive exercise of discretion and normally the superior court should not disturb in such finding unless the discretion was exercised on wholly untenable or perverse; (6) The rules of limitation are not meant to destroy the rights of the parties but they are meant to see that the parties do not resort to dilatory tactics to seek their remedy promptly; (7) Unless a party shows that he/she is put to manifest injustice or hardship, the' discretion exercised by the lower Court is not liable to be revised; (8) If the explanation does not smack of mala fides or it is put forth as part of a dilatory strategy, the court must show utmost consideration to the suitor; (9). If the delay was occasioned by party deliberately to gain time, then the court should lean against acceptance of the explanation and while condoning the delay, the Court should not forget the opposite party altogether.”

(c) In Sundar Gnanaolivu rep. By his Power of Attorney Agent Mr.Rukini Vs. Rajendra Gnanavolivu rep. By his Power of Attorney Agent Veina Gnanavolivu, reported in 2003 (1) LW 585 (DB), after considering a catena of decisions, the Hon'ble Division Bench of this Court, at paragraph Nos.15 and 16, held as follows:

"15. On a conspectus reading of the above principles set out in the various judgments, it is well settled that a liberal approach should be extended while considering the application for condonation of delay. Sufficient caution has been exhibited to note that wherever there is lack of bona fides or attempt to hood- wink the Court by the party concerned who has come forward with an application for condonation of delay, in such cases, no indulgence should be shown by condoning the delay applied for. It is also clear to the effect that it is not the number of days of delay that matters, but the attitude of the party which caused the delay. In other words when the Court finds that the party who failed to approach the Court within the time stipulated comes forward with an explanation for condoning the delay, the Court if satisfied that the delay occasioned not due to the deliberate conduct of the party, but due to any other reason, then by sufficiently compensating the prejudice caused to the other side monetarily, the condonation of delay can be favourbly ordered. 16. As held by His Lordship Mr. Justice M. Srinivasan, as he then was, in the Division Bench Judgment reported in 1990 (1) LLN 457 (Tamil Nadu Mercantile Bank Ltd. Tuticorin versus Appellate Authority Under The Tamil Nadu Shops And Establishments Act, Madurai And Another), the rules prescribing the period of limitation have to be obeyed by the concerned party and in order to get over such period prescribed, sufficient explanation should be tendered. His Lordship was pleased to hold that question of limitation is not merely a technical consideration but based on principles of sound public policy as well as equity and that a litigant cannot be expected to have a Damocles' sword hanging over his head indefinitely for a period to be determined at the whims and fancies of the opponent.

(d) In Shanmugam Vs. Chokkalingam, reported in 2009 (5) CTC 48, this Court was called upon to test the correctness of the order dismissing the application, seeking condonation of the delay in filing an application, to set aside the exparte decree. The reason assigned in the supporting affidavit was that, he could not avail leave from employment and hence could not appear before the Court. He did not know about the passing of the exparte decree.

Only when he met his counsel, he came to know about the decree. After considering a catena of decisions, on the aspect as to how and in what circumstances, delay could be condoned or not and on the facts and circumstances, this Court held that there was no illegality in dismissing the application filed for condonation of 332 days in seeking to set aside the exparte decree. It is worthwhile to reproduce the decision relied on in Shanmugam's case:

"9. .... Before going into the merits of the case, it has become absolutely necessary for this Court to refer the Judgment of the Honourable Apex Court reported in MANU/SC/0573/1998 : 1998(7) SCC 123 in between N. Balakrishnan v. M. Krishnamurthy, which reads as under:

The primary function of a court is to adjudicate the dispute between the parties and to advance substantial justice. The time- limit fixed for approaching the Court in different situations is not because on the expiry of such time a bad cause would transform into a good cause. Rules of limitation are not meant to destroy the rights of parties. They are meant to see that parties do not resort to dilatory tactics, but seek their remedy promptly. The object of providing a legal remedy is to repair the damage caused by reason of legal injury. The law of limitation fixes a lifespan for such legal remedy for the redress of the legal injury so suffered. The law of limitation is thus founded on public policy. It is enshrined in the maxim interest reipublicae up sit finis litium (it is for the general welfare that a period be put to litigation). Rules of limitation are not meant to destroy the rights of the parties. They are meant to see that parties do not meant to dilatory tactics but seek their remedy promptly. The idea is that every legal remedy must be kept alive for a legislatively fixed period of time.

Condonation of delay is a matter of discretion of the Court. Section 5 of the Limitation Act does not say that such discretion can be exercised only if the delay is within a certain limit. Length of delay is no matter, acceptability of the explanation is the only criterion. Sometimes delay of the shortest range may be uncondonable due to a want of acceptable explanation whereas in certain other case, delay of a very long range can be condoned as the explanation thereof is satisfactory. In every case of delay, there can be some lapse on the part of the litigant concerned. That alone is not enough to turn down his plea and to shut the door against him. If the explanation does not smack of mala fides or it is not put forth as part of a dilatory strategy, the court must show utmost consideration to the suitor. But when there is reasonable ground to think that the delay was occasioned by the party deliberately to gain time, then the court should lean against acceptance of the explanation. A court knows that refusal to condone delay would result in foreclosing a suitor from putting forth his cause. There is no presumption that delay in approaching the court is always deliberate. The words 'sufficient cause" under Section 5 of the Limitation Act should receive a liberal construction so as to advance substantial justice.

10. Similarly, the judgment of this Court reported in 2002(3) CTC 13 in between Sankaralingam and Anr. v. V. Rahuraman would also enlighten this Court regarding the points to be pondered in a case of condonation of delay. The relevant portion would run as under:

This Court is inclined to point out the following facts and circumstances which would speak volume against the petitioners (i.e.)

(a) Negligence and inaction, that too wilful, has to be inferred from the facts and circumstances,

(b) Vagueness of the affidavit and contradiction between the affidavit and deposition before Court,

(c) Failure to place any materials before Court to substantiate the case, and

(d) Absence of arguable points and law in the defence.”

(e) In Kaliaperumal Vs. Parasuraman, reported in 2010 (1) TNCJ 61 (Mad), there was a Delay of 3351 days. The defence taken was that counsel did not inform about proceeding of case. Holding that no reason has been given by petitioner, as to why he himself had not contacted his counsel, this Court rejected the case of the petitioner.

(f) In Anthonysamy Vs. Loordhusamy, reported in 2012 (1) TNCJ 914 (Mad), there was a delay of 1486 days. The application for condonation was dismissed. The reason assigned was that the appeal was filed in time, but the papers were mistakenly handed over by the counsel to another client. On the facts and circumstances of the case, the Court below held that having taken note of the fact that the revision petitioner had participated in the final decree and also in the eviction petition, cannot plead ignorance of legal proceedings and accordingly, upheld the order of dismissal.

(g) In Esha Bhattacharjee v. Raghunathpur Nafar Academy reported in 2013 (12) SCC 649, the Hon'ble Supreme Court has culled out the principles applicable to an application for condonation of delay and the same are reproduced hereunder:

“i) There should be a liberal, pragmatic, justice-oriented, non- pedantic approach while dealing with an application for condonation of delay, for the courts are not supposed to legalise injustice but are obliged to remove injustice.

ii) The terms “sufficient cause” should be understood in their proper spirit, philosophy and purpose regard being had to the fact that these terms are basically elastic and are to be applied in proper perspective to the obtaining fact- situation.

iii) Substantial justice being paramount and pivotal the technical considerations should not be given undue and uncalled for emphasis.

iv) No presumption can be attached to deliberate causation of delay but, gross negligence on the part of the counsel or litigant is to be taken note of.

v) Lack of bona fides imputable to a party seeking condonation of delay is a significant and relevant fact.

vi) It is to be kept in mind that adherence to strict proof should not affect public justice and cause public mischief because the courts are required to be vigilant so that in the ultimate eventuate there is no real failure of justice.

vii) The concept of liberal approach has to encapsule the conception of reasonableness and it cannot be allowed a totally unfettered free play.

viii) There is a distinction between inordinate delay and a delay of short duration or few days, for to the former doctrine of prejudice is attracted whereas to the latter it may not be attracted. That apart, the first one warrants strict approach whereas the second calls for a liberal delineation.

ix) The conduct, behaviour and attitude of a party relating to its inaction or negligence are relevant factors to be taken into consideration. It is so as the fundamental principle is that the courts are required to weigh the scale of balance of justice in respect of both parties and the said principle cannot be given a total go by in the name of liberal approach.

x) If the explanation offered is concocted or the grounds urged in the application are fanciful, the courts should be vigilant not to expose the other side unnecessarily to face such a litigation.

xi) It is to be borne in mind that no one gets away with fraud, misrepresentation or interpolation by taking recourse to the technicalities of law of limitation.

xii) The entire gamut of facts are to be carefully scrutinized and the approach should be based on the paradigm of judicial discretion which is founded on objective reasoning and not on individual perception.

xiii) The State or a public body or an entity representing a collective cause should be given some acceptable latitude.”

(h) In H.Dohil Constructions Company Private Limited V. Nahar Exports Limited and Another, reported in 2015 (1) Supreme Court Cases 680, the Hon'ble Supreme Court, after considering Tamilnadu Mercantile Bank Ltd., Vs. Appellate Authority, reported in (1990) 1 LLN 457, a decision of this Court and decision of the Supreme Court in Esha Bhattacharjee v. Raghunathpur Nafar Academy, reported in (2013) 12 SCC 649 at paragraph Nos.23 and 24, held as follows:

“23. We may also usefully refer to the recent decision of this Court in Esha Bhattacharjee [Esha Bhattacharjee v. Raghunathpur Nafar Academy, reported in (2013) 12 SCC 649], where several principles were culled out to be kept in mind while dealing with such applications for condonation of delay. Principles (iv), (v), (viii), (ix) and (x) of para 21 can be usefully referred to, which read as under: (SCCpp.658-59)

“21.4(iv) No presumption can be attached to deliberate causation of delay but, gross negligence on the part of the counsel or litigant is to be taken note of.

21.5. (v) Lack of bona fides imputable to a party seeking condonation of delay is a significant and relevant fact.

21.8. (viii) There is a distinction between inordinate delay and a delay of short duration or few days, for to the former doctrine of prejudice is attracted whereas to the latter it may not be attracted. That apart, the first one warrants strict approach whereas the second calls for a liberal delineation.

21.9 (ix) The conduct, behaviour and attitude of a party relating to its inaction or negligence are relevant factors to be taken into consideration. It is so as the fundamental principle is that the courts are required to weight the scale of balance of justice in respect of both parties and the said principle cannot be given a total go-by in the name of liberal approach.

21.10. (x) If the explanation offered is concocted or the grounds urged in the application are fanciful, the courts should be vigilant not to expose the other side unnecessarily to face such a litigation.

24. When we apply those principles to the case on hand, it has to be stated that the failure of the Respondents in not showing due diligence in filing of the appeals and the enormous time taken in the refiling can only be construed, in the absence of any valid explanation, as gross negligence and lacks in bonafides as displayed on the part of the Respondents. Further, when the Respondents have not come forward with proper details as regards the date when the papers were returned for refiling, the non- furnishing of satisfactory reasons for not refiling of papers in time and the failure to pay the Court fee at the time of the filing of appeal papers on 06.09.2007, the reasons which prevented the Respondents from not paying the Court fee along with the appeal papers and the failure to furnish the details as to who was their counsel who was previously entrusted with the filing of the appeals cumulatively considered, disclose that there was total lack of bonafides in its approach. It also requires to be stated that in the case on hand, not refiling the appeal papers within the time prescribed and by allowing the delay to the extent of nearly 1727 days, definitely calls for a stringent scrutiny and cannot be accepted as having been explained without proper reasons. As has been laid down by this Court, Courts are required to weigh the scale of balance of justice in respect of both parties and the same principle cannot be given a go-by under the guise of liberal approach even if it pertains to refiling. The filing of an application for condoning the delay of 1727 days in the matter of refiling without disclosing reasons, much less satisfactory reasons only results in the Respondents not deserving any indulgence by the Court in the matter of condonation of delay. The Respondents had filed the suit for specific performance and when the trial Court found that the claim for specific performance based on the agreement was correct but exercised its discretion not to grant the relief for specific performance but grant only a payment of damages and the Respondents were really keen to get the decree for specific performance by filing the appeals, they should have shown utmost diligence and come forward with justifiable reasons when an enormous delay of five years was involved in getting its appeals registered.”

It is also useful to extract paragraph Nos.14 to 17 of the judgment in Tamilnadu Mercantile Bank's case.

“14. We are unable to agree with the reasoning of the learned Judge that no litigant ordinarily stands to benefit by instituting a proceeding beyond time. It is common knowledge that by delaying a matter, evidence relating to the matter in dispute may disappear and very often the party concerned may think that preserving the relevant records would be unnecessary in view of the fact that there was no further proceeding. If a litigant chooses to approach the Court long after the time prescribed under the relevant provisions of the law, he cannot say that no prejudice would be caused to the other side by the delay being condoned. The other side would have in all probability destroyed the records thinking that the records would not be relevant as there was no further proceeding in the matter. Hence to view a matter of condonation of delay with a presupposition that no prejudice will be caused by the condonation of delay to the respondent in that application will be fallacious. In our view, each case has to be decided on the facts and circumstances of the case. Length of the delay is a relevant matter to be taken into account while considering whether the delay should be condoned or not. It is not open to any litigant to fix his own period of limitation for instituting proceedings for which law has prescribed period of limitation.

17.... Once it is held that a party has lost his right to have the matter considered on merits because of his own inaction for a long time, it cannot be presumed to be non-deliberate delay, and in such circumstances of the case, he cannot be heard to plead that substantial justice deserved to be preferred as against technical considerations. We are of the view that the question of limitation is not merely a technical consideration. Rules of limitation are based on principles of sound public policy and principles of equity. It is a litigant liable to have a Damocles' sword hanging over his head indefinitely for a period to be determined at the whims and fancies of the opponent?”

6. Keeping in mind, the principles of law, extracted supra and while applying the same to the facts of this case, we find that the appellant has not made out a case. As rightly observed by the Tribunal, the reasons are too vague and too general.

7. Material on record also disclose that earlier, when the order of the Assessing Officer, dated 23.03.2004, was challenged, before the Commissioner of Income-Tax (Appeal), there was a delay of 367 days, in filing the said appeal. Reasons assigned by the appellant therein were that search was conducted under the mistaken impression that he was a close associate of one Mr.S.Thiagarajan, who had floated a chit and that the appellant was hoping that the said S.Thiagarajan, would assist him and take steps. Ignorance of income tax procedure was also pleaded.

8. Perusal of the appeallate order, dated 26.12.2005, shows that considering the fact that the appellant was not well versed with Income-Tax provisions and also of the fact that search was conducted only in connection with the affairs of Thiru.Thiyagarajan and in the interest of fair justice, the Commissioner of Income-Tax (Appeals), has condoned the delay, taken up the appeal in I.T.A.No.65/05-06 and passed orders. Thus, it could be seen that discretion to condone the delay has been exercised by the first appellate authority on the abovesaid grounds.

9. While that be so, the appellant should have been more diligent in prosecuting his case, before the Income Tax Appellate Tribunal, Chennai, particularly, when he had suffered an adverse order. Though the impugned order, dated 26.12.2005, has been received by the family members of the appellant, long back, he has not exercised due care and attention and not diligent in prosecuting the second appeal before the Income-Tax Appellate Tribunal, within time. Inaction is per se apparent.

10. As per the statutory provision, appeal before the Income-Tax Appellate Tribunal ought to have been filed within 60 days. But the same has been preferred after an inordinate delay of 3389 days. Testing the sufficiency of cause, we are of the view that the appellant has not satisfied the principles of law, so as to enable this Court to exercise discretion in his favour, to condone the delay. Substantial questions of law raised by the appellant are answered in the negative, against the appellant.

11. In the result, the Tax Case Appeal is dismissed. No costs.

(S.M.K., J.) (D.K.K., J.)

07.06.2016

Index: Yes

Internet: Yes

×

Similar Ripples

Questions

Court Upholds Dismissal of Appeal Due to 3389-Day Delay, Emphasizing Importance of Timely Filing

Write your CommentSimilar Posts

Generic

- Reportdata/2794.pdf