Court Sets Aside Garnishee Order, Directs Speedy Appeal Hearing in Tax Dispute

Full News

Court Sets Aside Garnishee Order, Directs Speedy Appeal Hearing in Tax Dispute

Court Sets Aside Garnishee Order, Directs Speedy Appeal Hearing in Tax Dispute

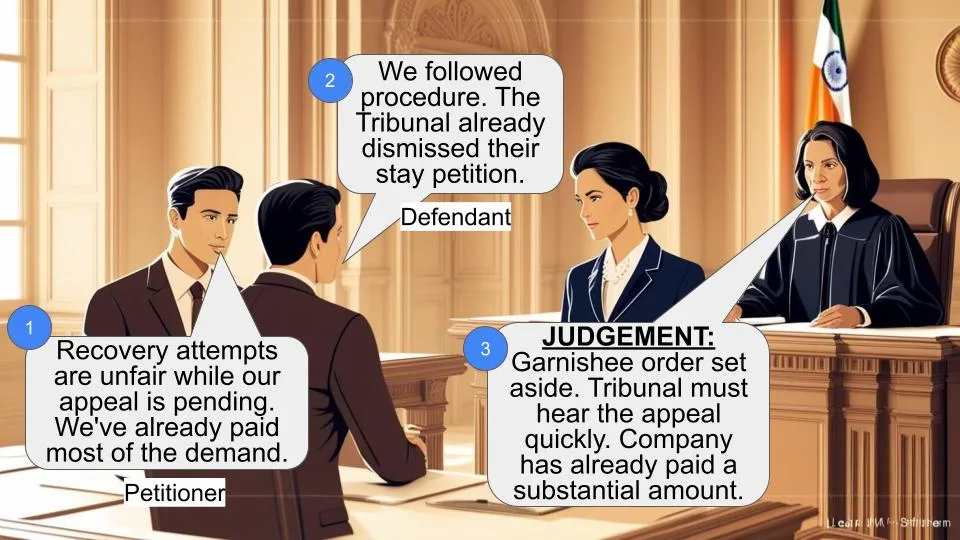

A company called Caplin Point Laboratories Limited was in a tax dispute with the Deputy Commissioner of Income Tax. The company had filed an appeal against a tax demand, and while that was pending, the tax department tried to recover the disputed amount. The court stepped in, set aside the recovery attempts, and told the tribunal to hear the appeal quickly.

Get the full picture - access the original judgement of the court order here

Case Name:

Caplin Point Laboratories Limited vs Deputy Commissioner of Income Tax (High Court of Madras)

W.P.No.25504 of 2004 and W.P.M.P.No.30992 of 2004

Date: 19th April 2012

Key Takeaways:

1. The court favors letting appeals run their course before aggressive tax recovery.

2. Substantial payment of disputed tax can work in the taxpayer's favor.

3. Courts may intervene to pause recovery actions when appeals are pending.

4. Tribunals are encouraged to expedite hearings in such cases.

Issue:

The main question here was: Should the tax department be allowed to recover a disputed tax amount through garnishee orders when an appeal is pending before the Income Tax Appellate Tribunal?

Facts:

1. Caplin Point Laboratories Limited filed a tax return for the 1995-96 assessment year.

2. The tax department reopened the assessment and increased the taxable income.

3. The company appealed to the Commissioner of Income Tax (Appeals), who sided with the tax department.

4. The company then appealed to the Income Tax Appellate Tribunal.

5. While this appeal was pending, the tax department issued a garnishee order to recover the disputed amount.

6. The total demand was Rs.60,64,793, but the company had already paid Rs. 52,33,773.

7. Only Rs.5,00,760 was the actual tax component; the rest was interest.

Arguments:

The company's side:

- They argued that their appeal had a good chance of success.

- They claimed the tax department wrongly denied them benefits under Section 80HHC (of Income Tax Act, 1961).

- They said the garnishee order was illegal and unjustified.

The tax department's side:

- They argued they followed the correct legal procedure for recovery.

- They pointed out that the Tribunal had dismissed the company's stay petition.

Key Legal Precedents:

Interestingly, this judgment doesn't cite specific legal precedents. Instead, it focuses on the facts of the case and the provisions of the Income Tax Act, particularly Sections 220(2) and 226(3) .

Judgement:

The court sided with the company. Here's what they decided:

1. They set aside the garnishee order and attachment notice.

2. They directed the Income Tax Appellate Tribunal to hear the company's appeal quickly, preferably within six weeks.

3. They noted that the company had already paid a substantial portion of the demand.

4. They mentioned that the company could file a waiver petition for the interest component under Section 220(2) (of Income Tax Act, 1961) .

FAQs:

1. Q: What's a garnishee order?

A: It's an order that allows the tax department to collect money owed to them directly from a third party who owes money to the taxpayer.

2. Q: Why did the court set aside the garnishee order?

A: Because the company's appeal was still pending, and they had already paid a significant portion of the demanded amount.

3. Q: Does this mean the company doesn't have to pay the tax?

A: Not necessarily. The court just paused the recovery process until the appeal is heard. The final tax liability will depend on the outcome of the appeal.

4. Q: What's the significance of Section 80HHC (of Income Tax Act, 1961)?

A: It's a section of the Income Tax Act that provided deductions for profits earned from export business. The company claimed they were wrongly denied this benefit.

5. Q: Can the tax department try to recover the amount again?

A: They'll have to wait for the Tribunal's decision on the appeal. If the Tribunal rules in favor of the tax department, they might initiate recovery proceedings again.

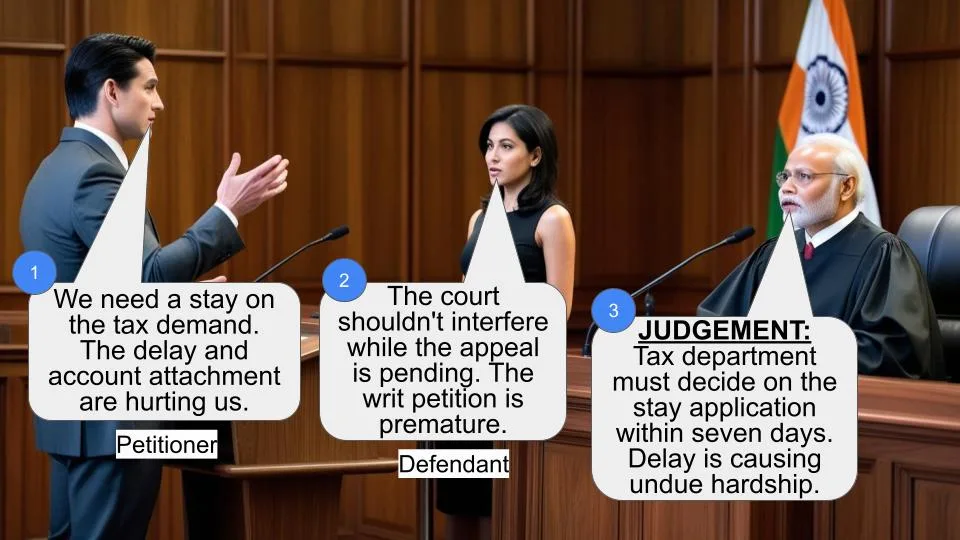

1. The Writ Petition is filed seeking the relief of issuance of writ of mandamus to forbear the 1st and 2nd respondents from initiating and or continuing any recovery proceedings for recovery of the disputed demand relating to the assessment year 1995-96 in respect of which an appeal and stay petition are pending before the 5th respondent, pending disposal of the said appeal and the petition for stay by the said respondent.

2. The petitioner is engaged in the manufacture and sale of pharmaceutical products. Relevant assessment year is 1995-96 and the corresponding accounting year ended on 31.3.1995. The petitioner/ assessee filed his return of income on 28.11.1995 admitting total income of Rs.2,57,270/- after claiming deduction under Section 80HHC (of Income Tax Act, 1961) and 80I (of Income Tax Act, 1961) of Rs.1,76,116 and Rs.1,44,463/- respectively. The said assessment was processed under Section 143(1)(a) of the Income Tax Act, 1961. Subsequently, the assessing officer issued a notice under Section 148 (of Income Tax Act, 1961) on 18.2.2000 for reopening the assessment. Objecting the same, the petitioner also filed a letter dated 9.3.2000. The assessing officer completed the assessment under Section 143 (of Income Tax Act, 1961) read with Section 147 (of Income Tax Act, 1961) and determined the total income at Rs.5,77,850/-. While completing the assessment, the assessing officer disallowed the claim of deduction under Section 80HHC (of Income Tax Act, 1961) and 80I (of Income Tax Act, 1961). Aggrieved by that, the assessee filed an appeal before the Commissioner of Income-tax (Appeals) and the Commissioner of Income-tax (Appeals) dismissed the appeal confirming the order of assessment. Aggrieved by that, the assessee filed an appeal before the Income-tax Appellate Tribunal and the same is still pending. When the Commissioner of Income-tax (Appeals) dismissed the appeal, the revenue initiated recovery proceedings by way of issuing garnishee order under Section 226(3) of the Income Tax Act, 1961. Aggrieved by that, the petitioner/assessee filed present writ petition challenging the garnishee order.

3. Learned counsel for the petitioner vehemently contended that aggrieved by the order of the Commissioner of Income-tax (Appeals) the petitioner preferred an appeal before the Income-tax Appellate Tribunal and the chance of petitioner's success before the Tribunal is very bright and further it is stated that the assessing officer as well as the first appellate authority wrongly denied the benefit of Section 80HHC of the Income Tax Act, 1961. The passing of garnishee order is wrong, illegal, without any basis and justification.

4. Learned counsel appearing for the respondents 1 and 2 contended that the revenue has correctly followed the procedure as prescribed under the statute and correctly initiated recovery proceedings by issuing garnishee order. Learned counsel further submits that the stay petition preferred by the petitioner before the Tribunal was also dismissed and so the garnishee order passed by the revenue is in accordance with law and the same should be confirmed.

5. Heard the learned counsel appearing on either side and perused the material documents on record.

6. It is pertinent to note that the petitioner/assessee filed appeal before the Income-tax Appellate Tribunal against the order passed by the Commissioner of Income-tax (Appeals) as early as 2003 and the same is still pending. Now it is also very relevant to note that as per the letter of the Assistant Commissioner of Income-tax, Company Circle-i(3), Chennai, dated 18.4.2012 in PAN.No.AABCC2667F/1995-96 addressed to the learned counsel for respondent, the total demand is Rs.60,64,793/-. Out of the said sum, only Rs.5,00,760/- is due towards tax component and the balance amount relates to the interest levied under section 220(2) of the Income Tax Act, 1961 and the assessee also already paid a sum of Rs.52,33,773/- towards the tax and credit was also given by the revenue. Against the levy of interest under Section 220 of the Income Tax Act, 1961, the petitioner can also file waiver petition before the concerned Commissioner of Income-tax under Section 220(2) (of Income Tax Act, 1961).

7. Taking into consideration of the above facts and circumstances, the impugned garnishee order passed by the 2nd respondent Tax Recovery Officer dated 1.9.2004 and the attachment notice are set aside and the 5th respondent Income-tax Appellate Tribunal is directed to take up the appeal relating to the petitioner in I.T.A.No.222/Mds/2003, consider the same after giving opportunity to the petitioner to substantiate his case and pass orders in accordance with law as expeditiously as possible, preferably within a period of six weeks from the date of receipt of copy of this order.

8. With this observation, the writ petition is disposed of. However, there is no order as to costs. Consequently, the connected miscellaneous petition is closed.

19.04.2012

Index:Yes/No

Internet:Yes/No

Copy to:

1. The Deputy Commissioner of Income-tax, Company Circle-I(3), 121 (of Income Tax Act, 1961), N.H.Road, Chennai 600 034,

2.The Tax Recovery Officer, Company Circle-I, 121, N.H.Road, Chennai 600 034,

3. The Manager, Catholic Syrian Bank Limited, Mount Road Branch, Chennai,

4. M/s.May India Laboratories Pvt.Ltd., 3, Lakshman Street, T.Nagar, Chennai 6000 017,

5. Income Tax Appellate Tribunal, A3/II Floor, 'Rajaji Bhavan', Besant Nagar, Chennai 600 090.

P.P.S.JANARTHANA RAJA,J.

19.04.2012

×

Similar Ripples

Questions

Court Sets Aside Garnishee Order, Directs Speedy Appeal Hearing in Tax Dispute

Write your CommentSimilar Posts

Generic

- Reportdata/5913.pdf