Court Upholds Lease Premium as Capital Expenditure, Dismisses Tax Deduction Cla…

Full News

Court Upholds Lease Premium as Capital Expenditure, Dismisses Tax Deduction Claim

Court Upholds Lease Premium as Capital Expenditure, Dismisses Tax Deduction Claim

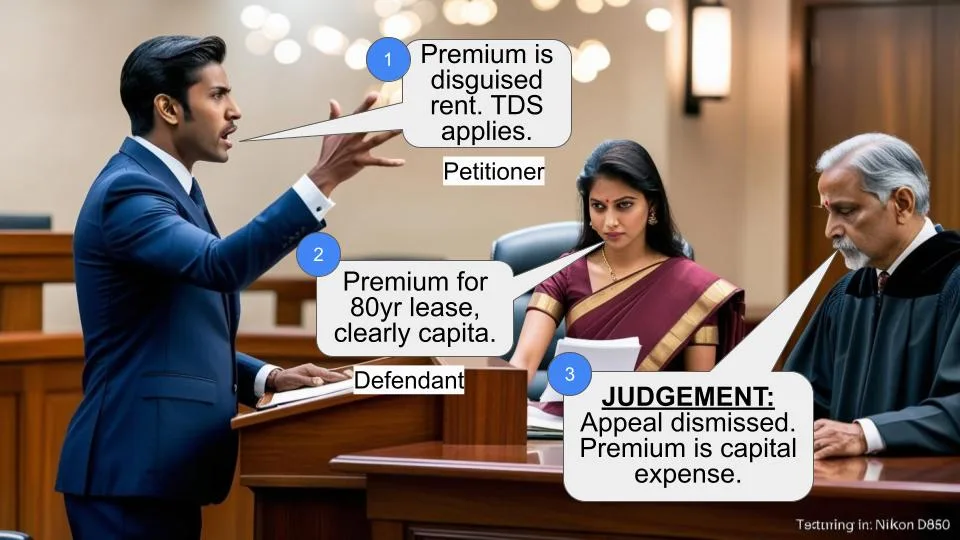

This case involves the Commissioner of Income Tax (the Revenue) appealing against a decision made by the Income Tax Appellate Tribunal (ITAT) regarding the classification of a lease premium paid by the Indian Newspaper Society (the Assessee) to the Mumbai Metropolitan Regional Development Authority (MMRDA). The court dismissed the Revenue's appeal, affirming that the lease premium was indeed a capital expenditure and not subject to tax deduction at source under Section 194I (of Income Tax Act, 1961).

Get the full picture - access the original judgement of the court order here

Case Name:

Commissioner of Income Tax Vs The Indian News Paper Society (High Court of Delhi)

ITA 918/2015

Date: 10th December 2015

Key Takeaways:

1. Lease premiums for long-term leases (80 years in this case) are typically considered capital expenditure.

2. The intention of parties, as evidenced by lease agreement clauses, is crucial in determining the nature of payments.

3. The treatment of receipts by the receiving party (MMRDA in this case) can influence the classification of the payment.

4. Courts are reluctant to condone extraordinary delays in filing appeals without substantial justification.

Issue:

Was the lease premium paid by the Assessee to MMRDA for an 80-year lease a capital expenditure (not subject to tax deduction at source) or a revenue expenditure (subject to tax deduction at source under Section 194I (of Income Tax Act, 1961))?

Facts:

1. The Assessee (Indian Newspaper Society) paid a total of Rs.88,72,55,000 to MMRDA on 27th December 2005 and 18th February 2008 as lease premium.

2. The lease was for a plot of land at Bandra-Kurla Complex, Mumbai, for a period of 80 years.

3. The lease agreement, dated 9th April 2008, clearly stated that the payment was a lease premium, not rent.

4. The annual rent payable by the Assessee to MMRDA was a nominal sum of Rs.10,415.

5. The Revenue filed the appeal with an extraordinary delay of 740 days.

Arguments:

Revenue's Arguments:

1. The lease premium was essentially advance rent camouflaged as a premium.

2. The nominal annual rent suggests that the premium was actually covering the rent for 80 years.

3. Any payment of rent for land would attract Tax Deducted at Source (TDS) under Section 194I (of Income Tax Act, 1961).

Assessee's Arguments:

1. The lease agreement clearly distinguishes between the premium and the annual rent.

2. The premium was a capital expenditure for acquiring long-term lease rights.

3. MMRDA treated the receipt as a capital receipt, not as income.

Key Legal Precedents:

1. A.R. Krishnamurthy v. Commissioner of Income Tax 172 ITR 311 (SC)

2. R. K. Palshikar 172 ITR 311 (SC)

3. Durga Khanna v. Commissioner of Income Tax 72 ITR 796 (SC)

4. Krishak Bharati Cooperative Ltd. v. Deputy Commissioner of Income Tax (2013) 350 ITR 24 (Del)

These cases established that payments made for transfer of leasehold rights for long periods are generally considered benefits of an enduring nature, i.e., capital expenditure. The Durga Khanna case specifically held that premium or salami is prima facie not income, and the onus is on the Revenue to prove otherwise.

Judgement:

The court dismissed the Revenue's appeals on two grounds:

1. The extraordinary delay of 740 days in re-filing the appeals was not condoned.

2. On merits, the court agreed with the ITAT's decision that the lease premium was a capital expenditure, not subject to TDS under Section 194I (of Income Tax Act, 1961).

The court based its decision on three key factors:

1. The lease agreement clearly stated the payment was a lease premium, not rent.

2. The lease was for 80 years with "all rights, easements and appurtenances."

3. MMRDA treated the receipt as a capital receipt, not as taxable income.

FAQs:

1. Q: What is the difference between a lease premium and rent?

A: A lease premium is typically a one-time payment made at the beginning of a long-term lease, while rent is a recurring payment for the use of property.

2. Q: Why is the classification of the payment as capital or revenue expenditure important?

A: It affects tax treatment. Capital expenditures are generally not deductible immediately but may be depreciated over time, while revenue expenditures are usually deductible in the year they're incurred.

3. Q: What is Section 194I (of Income Tax Act, 1961)?

A: It's a provision that requires deduction of tax at source on certain payments made as rent.

4. Q: How does the length of the lease affect the classification of payments?

A: Generally, payments for very long-term leases (like 80 years in this case) are more likely to be considered capital expenditures because they provide a benefit of an enduring nature.

5. Q: Why was the delay in filing the appeal significant?

A: Courts have strict timelines for filing appeals. Extraordinary delays without proper justification can lead to dismissal of the appeal, as happened in this case.

ITA 918/2015 and CM No. 29413/2015 (for condonation of delay in re- filing the appeal)

ITA 920/2015 and CM No. 29546/2015 (for condonation of delay in re- filing the appeal)

1. These are two appeals by the Revenue under Section 260A (of Income Tax Act, 1961) (‘Act’) directed against the common order dated 20th June 2013 passed by the Income Tax Appellate Tribunal (‘ITAT’) in ITA Nos. 5207 & 5208/Del/2012 for Assessment Years (‘AYs’) 2008-09 and 2010-11 respectively.

2. At the very outset, the Court would like to observe that there is an extraordinary delay of 740 days in re-filing of these appeals. The explanation offered is the standard one regarding the practice directions issued by this Court for e-filing of the appeals. As has already been observed by this Court in several orders, the practice directions were issued after consultation with the bar and after giving sufficient time for the bar to get acquainted with the requirement of e-filing. Additionally, the Court has also provided scanning machines at the filing counter so that no difficulty is caused to the bar for switching over to the system of e-filing. In any event, the delay of over two years on this ground is wholly unacceptable. Consequently, the Court is not persuaded to condone the extraordinary delay of 740 days in re-filing the appeals.

3. Nevertheless the appeals have also been examined on merits. The short point urged by the Revenue in these appeals is that the lease premium paid by the Assessee to the Mumbai Metropolitan Regional Development Authority (‘MMRDA’) on 27th December 2005 and 18th February 2008 in the total sum of Rs.88,72,55,000 for acquiring a plot of land on an 80 year lease at Bandra- Kurla Complex, Mumbai was in the nature of a capital expense not falling within the ambit of Section 194I (of Income Tax Act, 1961). While the Assessing Officer (‘AO’) treated it as revenue expenditure, the Commissioner of Income Tax (Appeals) [‘CIT (A)’] reversed it and held it to be in the nature of a capital expense not requiring deduction of tax at source under Section 194I (of Income Tax Act, 1961).The ITAT has in the impugned order concurred with the CIT (A) and dismissed the Revenue’s appeals.

4. Mr. Rohit Madan, learned Senior Standing counsel for the Revenue submitted that the actual annual rent was a nominal sum and, therefore, what in fact was paid by the Assessee to MMRDA was in the nature of advance rent. According to him, the premium paid had camouflaged the annual rent payable over the period of 80 years for the land in question. He submitted that under Section 194I (of Income Tax Act, 1961), any payment of rent for land would attract TDS. He placed reliance on a large number of decisions including Commissioner of Income Tax, Tamil Nadu v. Madras Auto Service (P) Ltd. [1998] 233 ITR 468 (SC) and the decision of the Madras High Court in Commissioner of Income Tax v. Gemini Arts P. Ltd. (2002) 254 ITR 201. He also referred to the recent decision of this Court in Krishak Bharati Cooperative Ltd. v. Deputy Commissioner of Income Tax (2013) 350 ITR 24 (Del).

5. Mr. Sunil Fernandes, learned counsel appearing for the Assessee referred to the specific factual findings of the CIT (A) at its discussion of the clauses of the lease agreement which have been set out in extenso by the ITAT in the impugned order.

6. At the outset, it requires to be noticed that under Section 194I (of Income Tax Act, 1961) the responsibility for deducting tax at source arises when a person pays "to a resident any income by way of rent.” The deduction has to be effected “at the time of credit of such income to the account of the payee or at the time of payment thereof in cash or by the issue of a cheque or draft or by any other mode...” at the rate specified in Section 194I (of Income Tax Act, 1961). The critical word,therefore, is “income" in the hands of the payee. On facts it requires to be first noted that the clauses of the lease agreement with MMRDA dated 9th April 2008 clearly state that the payment of Rs.88,52,75,000 is only on the ground of lease premium and not rent. There is no provision in the lease agreement for adjustment of the premium amount against the annual rent of Rs.10,415 payable by the Assessee to MMRDA.

7. The second factor is that under the lease agreement, the plot of land “together with all the rights, easements and appurtenances and the like for 80 years commencing from 01. 04.2008” was demised to the Assessee. A third factor which has been noticed in the impugned order of the ITAT is that in the writ petition filed by the Assessee in the Bombay High Court, being WP (C) N0. 1504 of 2001, an affidavit has been filed by the Revenue in which it accepted that “MMRDA has construed the receipt of premium as a capital receipt not eligible to tax.” The above three undisputed factual aspects, in the considered view of the Court, conclusively settle the issue whether the premium paid to the MMRDA by the Assessee in terms of the lease agreement is, in fact, only a capital and not a revenue expenditure.

8. The impugned order of the ITAT refers to several decisions of the Supreme Court including A.R. Krishnamurthy v. Commissioner of Income Tax 172 ITR 311 (SC) and R. K. Palshikar 172 ITR 311 (SC) which have construed the payment made for transfer of leasehold rights for long period of time as a benefit of an enduring nature. The recent decision of this Court in Krishak Bharati (supra) also decides this particular issue likewise although on the facts of that case, the appeal of the that Assessee was dismissed. In Durga Khanna v. Commissioner of Income Tax 72 ITR 796 (SC), the Supreme Court held that, prima facie, premium or salami was not income and the onus was on the Revenue to show that facts existed which would make it a revenue payment. The decisions cited by Mr. Madan clearly turned on their own facts. As far as the present case is concerned, the facts brought on record, and which have not been contested by the Revenue, unmistakably show that the payment of the lease premium for the land given on lease to the Assessee for a period of 80 years with “all the rights, easements and appurtenances” was in the nature of a capital expenditure. This coupled with the fact that the MMRDA did not treat the receipt as income clinches the issue in favour of the Assessee and against the Revenue.

9. This being the main issue on merits, the Court does not consider it necessary to decide the other issue of limitation that arises in AY 2008-09.

10. The appeals are accordingly dismissed both on the ground of the extraordinary delay of 740 days in re-filing the appeals as well as on merits.

S. MURALIDHAR, J

VIBHU BAKHRU, J

DECEMBER 10, 2015

×

Similar Ripples

Questions

Court Upholds Lease Premium as Capital Expenditure, Dismisses Tax Deduction Claim

Write your CommentSimilar Posts

Generic

- Reportdata/3246.pdf