Full News

Court Upholds Long-Term Capital Gains Treatment for Assessee's Share Sales

Court Upholds Long-Term Capital Gains Treatment for Assessee's Share Sales

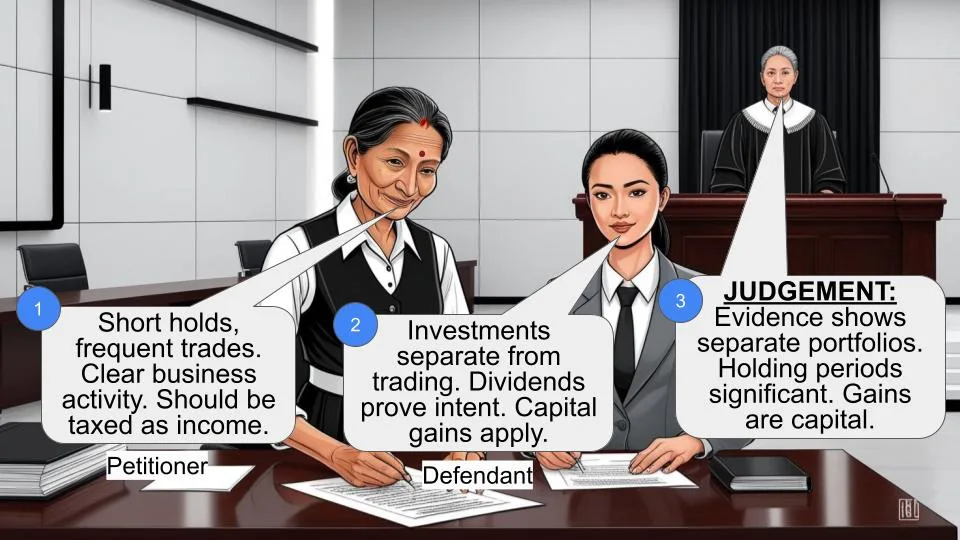

The tax department (the Revenue) was challenging how an individual taxpayer (the assessee) reported their income from selling shares. The tax folks thought it should be treated as business income, but the court sided with the taxpayer, saying it was actually long-term capital gains. It's a win for the taxpayer.

Case Name**: COMMISSIONER OF INCOME TAX VS BRIJESH BHAGWATILAL LAVTI

**Key Takeaways**:

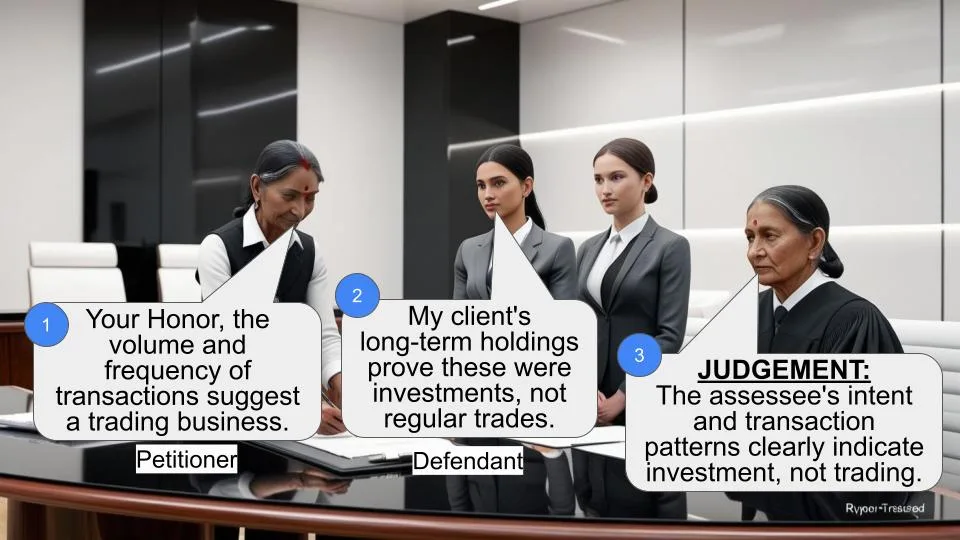

1. The court emphasized that the intention of the assessee at the time of purchasing shares is crucial in determining whether it's an investment or trading activity.

2. Having two portfolios (investment and trading) is possible, and income can be assessed under both "capital gains" and "business income" heads.

3. For salaried individuals, occasional share transactions are more likely to be seen as investments rather than trading activities.

4. The volume, frequency, and holding period of share transactions are important factors in determining their nature.

**Issue**:

The main question here was: Should the gains from the assessee's sale of shares be treated as long-term capital gains (as claimed by the assessee) or as business income (as argued by the tax department)?

**Facts**:

Alright, let's break this down:

1. The assessee was a salaried individual who filed a tax return showing income from salary and some income from share transactions.

2. They reported Rs. 83,712 as income from share trading and claimed Rs. 53,84,239 as exempt income from long-term capital gains on share sales.

3. The Assessing Officer disagreed and treated the entire Rs. 53,84,239 as business income.

4. The case went through appeals, first to the Commissioner of Income Tax (Appeals) and then to the Income Tax Appellate Tribunal, both of which ruled in favor of the assessee.

5. The tax department then appealed to the High Court, which is the judgment we're looking at now.

**Arguments**:

The tax department's side:

- They argued that the assessee was actually in the business of trading shares, so all the income should be taxed as business income.

The assessee's side:

- They maintained that they were just an investor, not a trader.

- Most of their share transactions resulted in long-term capital gains, with only a small portion being short-term.

**Key Legal Precedents**:

The judgment mentions a circular from the Central Board of Direct Taxes (CBDT Circular No. 4/2007 dated 15-06-2007) that provides guidance on this issue . This circular, referring to a Supreme Court judgment, acknowledges that taxpayers can have both investment and trading portfolios in shares.

**Judgement**:

The High Court dismissed the tax department's appeal, agreeing with the lower authorities. Here's why:

1. They found that the assessee, being a salaried person, was primarily an investor, not a share trader.

2. The court noted that only a small portion (Rs. 83,712) of the total gains came from short-term transactions, while the bulk (Rs. 53,84,239) was from shares held for a long period.

3. They considered factors like the volume and frequency of share transactions, which supported the assessee's claim of being an investor.

4. The court concluded that the Commissioner (Appeals) and the Tribunal had correctly applied both the facts and the law in this case.

**FAQs**:

1. Q: Does this mean all salaried individuals' share transactions will be treated as investments?

A: Not necessarily. Each case is judged on its own merits, considering factors like transaction frequency, volume, and holding period.

2. Q: What's the tax benefit of long-term capital gains versus business income?

A: Long-term capital gains often have a more favorable tax rate compared to business income, which is why this distinction matters.

3. Q: Can a person have both investment and trading activities in shares?

A: Yes, the CBDT circular acknowledges that a taxpayer can have both investment and trading portfolios.

4. Q: What factors does the court consider in determining if someone is an investor or a trader?

A: The court looks at things like the person's primary occupation, the volume and frequency of share transactions, and how long they hold onto the shares.

1. Revenue is in appeal against the judgment of the Income Tax Appellate Tribunal ('the Tribunal', for short) dated 27-5-2011. For the assessment year 2006-07, the following questions have been presented for our consideration:-

A. Whether in the facts and circumstances of the case and in law the Ld. ITAT is right in treating the gain on sale of shares amounting to Rs.70,15,820/- as long- term Capital Gain as against business income treated by the AO?

B. Whether in the facts and circumstances of the case and in law the Ld. ITAT has erred in holding the assessee as 'Investor' and not as a 'Trader' in shares and thereby treating the resultant gain on sale of shares as 'Long Term Capital Gain?

2. The questions pertain to the issue whether the respondent assessee can be stated to be engaged in the business of trading in shares. In case of an assessee belonging to the same family, under very similar circumstances, we had upheld the Tribunal's judgment making following observations:-

“The assessee as a salaried class person had filed a return of income in which he had shown the gross total income of Rs.3,95,001/- which included his income from salary as well as a sum of Rs.83,712/- towards receipt from share trading. The assessee had also claimed as exempt income of Rs.53,96,468/- towards long term capital gain out of sale of shares. The Assessing Officer, however, held that the assessee was trading in shares and accordingly taxed the entire income of Rs.53,96,468/- as the income from profit and gains of business and profession.

The assessee carried the matter in appeal. The appellate authority took note of the circular of CBDT clarifying the position with respect to share trading/investment in shares and concluded that the Assessing Officer failed to take into account such clarification as well as the decisions of the Apex Court. He was of the opinion that looking to the material on record, it cannot be stated that the assessee was in the business of trading in shares.

Revenue, aggrieved by the decision of the Commissioner (Appeals), carried the matter before the Tribunal. The Tribunal upheld the Commissioner's view making following observations:-

“4. We have considered the rival submissions on either side and have also perused the material available on record. For the purpose of finding out the nature of transaction as to whether it is an investment or adventure in the nature of trade, one has to see the intention of the assessee at the time of purchase of the shares. The assessee is only an employee having salary income. In the return of income as seen from the assessment order, the assessee has claimed Rs.83,712 from share trading and another sum of Rs.53,84,239 as exempt income on sale of certain sales. This Rs.53,84,239 was treated by the assessing officer as business income on sale of shares. We find that the CBDT in its circular No.4/2007 dated 15-06-2007 examined this issue and after referring to the judgment of the apex court, instructed all its officers that it is possible for the taxpayer to have two portfolios, i/e/ investment portfolio. When the assessee has two portfolios, the income has to be assessed both under the head “capital gains” as well as “business income”. In this case, the assessee is a salaried employee.

Therefore, the question of maintaining two portfolio does not arise for consideration. The assessee invested his funds as investment and whenever it was convenient, it was sold. The intention of the assessee at the time of purchase is very clear that it is an investment and not to trade in shares. Merely because, on one or two occasions there was also purchase and sale of shares, we cannot say that the assessee is trading in shares. The transaction as extracted by the assessing officer in the assessment order shows that the assessee never intended to trade in shares and being salaried person intended to investor. Therefore, the profit on sale shares has to be classified as capital gain either as short term capital gain or long term capital gain depending upon the period holding. Since the CIT(A) has directed the assessing officer to treat the same as capital gain we do not find any infirmity in the order of lower authority. Accordingly the same is confirmed.”

Having heard learned counsel for the revenue and having perused the documents on record, we are of the opinion that the Commissioner as well as the Tribunal concurrently found as a matter of fact that looking to the relevant factors including the amount of share holding of the assessee, the volume and the frequency of the purchase and sale of shares etc., it cannot be stated that the assessee was in the business of trading of shares. More significantly, we find that the assessee had sold shares only worth Rs.83,712/- during the year under consideration inviting short term capital gain. As against that, bulk of the shares were held by the assessee for a long period of time inviting long term capital gain for a total sum of Rs.53,84,239/-. Totality of the facts and circumstances of the case would lead to an inescapable conclusion that CIT (Appeals) as well as the Tribunal correctly applied the factual and legal position. No question of law arises. Resultantly, the tax appeal is dismissed.”

3. In the result, the tax appeal is dismissed.

( Akil Kureshi, J. ) ( Harsha Devani, J. )

×

Similar Ripples

Questions

Court Upholds Long-Term Capital Gains Treatment for Assessee's Share Sales

Write your CommentSimilar Posts

Generic

- Reportdata/5391.pdf