Investor's Dual Portfolio Strategy Upheld: Tax Treatment as Capital Gains Affir…

Full News

Investor's Dual Portfolio Strategy Upheld: Tax Treatment as Capital Gains Affirmed

Investor's Dual Portfolio Strategy Upheld: Tax Treatment as Capital Gains Affirmed

This case involves a dispute between the Commissioner of Income Tax (the appellant) and Suresh R. Shah (the respondent) regarding the tax treatment of income earned from share transactions. The Income Tax Appellate Tribunal (ITAT) ruled in favor of the respondent, affirming that the income should be treated as capital gains rather than business income. The High Court dismissed the appeal by the Revenue, upholding the ITAT's decision.

Case Name**:

COMMISSIONER OF INCOME TAX VS Suresh R. Shah

**Key Takeaways**:

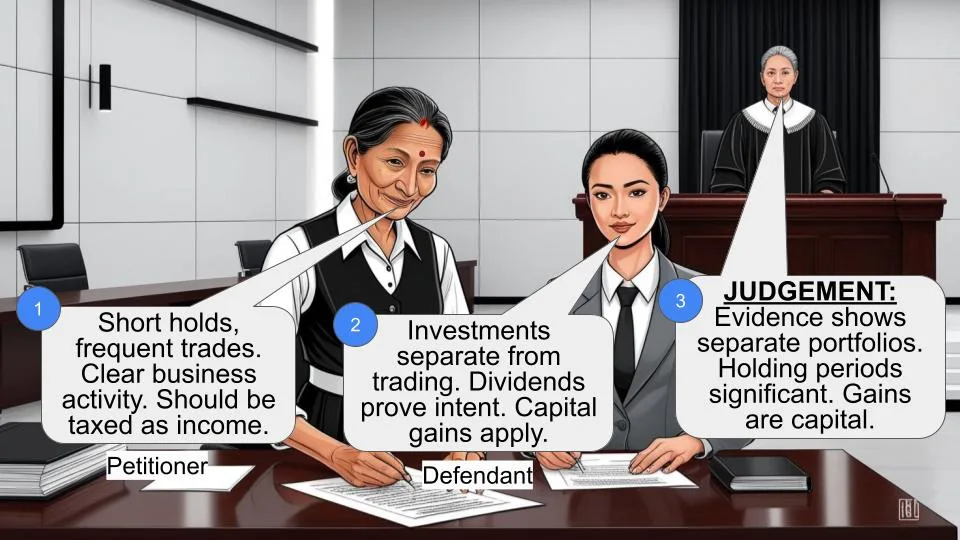

1. An assessee can maintain two separate portfolios: one for share investments and another for share trading business.

2. The nature of income from share transactions (capital gains vs. business income) depends on various factors, not just the presence of speculation loss.

3. Appellate authorities' findings of fact, if not perverse, are generally not subject to review by higher courts.

**Issue**:

Was the Income Tax Appellate Tribunal (ITAT) justified in upholding the treatment of the assessee's income from share transactions as capital gains instead of business income, despite the assessee showing speculation loss?

**Facts**:

1. The case relates to the Assessment Year 2006-07 (previous year ending 31/3/2006) .

2. The respondent, Suresh R. Shah, is engaged in the textile business .

3. The Assessing Officer initially rejected the respondent's claim for taxation under capital gains and treated the income as business income .

4. The respondent had reported a speculation loss of Rs. 13,483/- in share trading .

5. The CIT (Appeals) allowed the respondent's appeal, holding that the income should be assessed as capital gains .

6. The ITAT upheld the CIT (Appeals) order, concluding that the respondent was an investor in shares .

**Arguments**:

Revenue's Arguments:

1. The assessee showed speculation loss, indicating involvement in share trading business.

2. The income should be treated as business income rather than capital gains.

Assessee's Arguments:

1. The income from share transactions should be treated as capital gains.

2. The assessee maintained separate portfolios for investment and trading activities.

**Key Legal Precedents**:

1. CIT vs. Gopal Purohit (228 CTR (Bom.) 582): This case established that there is no bar for an assessee to maintain two separate portfolios, one for share investments and another for share trading business .

**Judgement**:

1. The High Court dismissed the appeal by the Revenue .

2. The court upheld the ITAT's decision that the respondent was an investor in shares and entitled to be taxed under the head of capital gains .

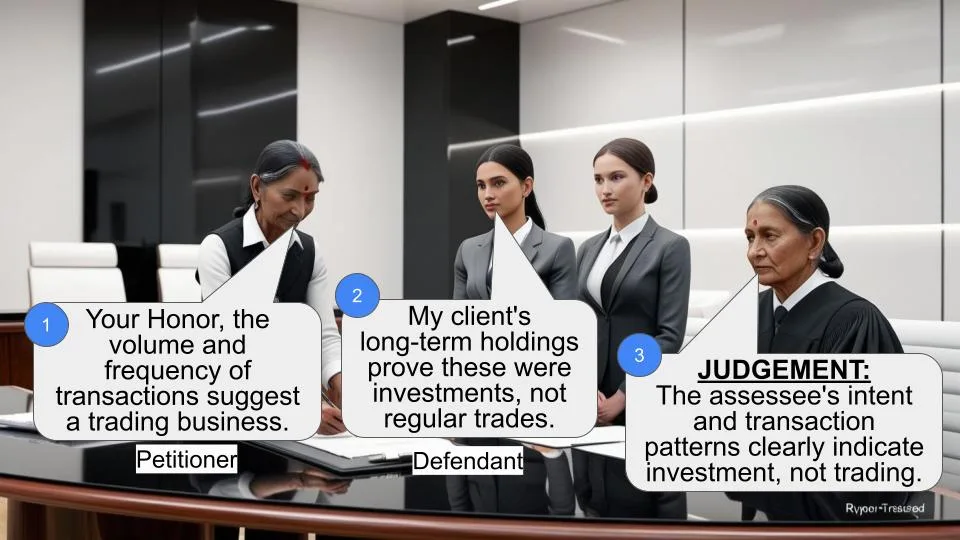

3. The court found that the ITAT's decision was based on factual findings, including:

a. The respondent had not borrowed funds for investments .

b. Long-term gains were attributable to shares of 4 companies, with 3 held for 5-12 years .

c. 93% of short-term gains/losses were from shares of six companies, all held for over a month .

4. The court concluded that no substantial question of law arose for consideration .

**FAQs**:

Q1: Why did the court uphold the treatment of income as capital gains despite the presence of speculation loss?

A1: The court followed the precedent set in CIT vs. Gopal Purohit, which allows an assessee to maintain separate portfolios for investment and trading. The presence of speculation loss alone doesn't determine the nature of all share-related income.

Q2: What factors did the ITAT consider in determining that the assessee was an investor?

A2: The ITAT considered factors such as the duration of shareholding (some shares held for 5-12 years), the absence of borrowed funds for investments, and the pattern of short-term gains/losses.

Q3: Can an individual have both capital gains and business income from share transactions?

A3: Yes, the judgment affirms that an individual can maintain separate portfolios for investment (leading to capital gains) and trading (leading to business income).

Q4: What is the significance of this judgment for other taxpayers?

A4: This judgment reinforces the principle that the nature of income from share transactions is determined by various factors and that maintaining separate portfolios for investment and trading is permissible.

Q5: Why didn't the High Court intervene in the ITAT's decision?

A5: The High Court found that the ITAT's decision was based on factual findings that were not perverse. In such cases, higher courts generally do not interfere with concurrent findings of fact by lower appellate authorities.

1) This appeal by the Revenue under Section 260A (of Income Tax Act, 1961) (hereinafter referred to as the “said Act”) is from the Order dated 10/11/2010 of the Income Tax Appellate Tribunal (hereinafter referred to as the Tribunal) relates to Assessment Year 2006-07 (previous year ending 31/3/2006). Being aggrieved by the Order dated 10/11/2010, the appellant has formulated the following questions of law for consideration by this Court:

A) Whether on the facts and circumstances of the case and in law the ITAT was justified in upholding the order of CIT(A) Mumbai dated 17/9/2009 bearing No. CIT(A)-35/ACIT/25(2) ITA 4328/08-09 despite the facts the Assessee has shown speculation loss and still accepted the claim of Assessee and directed A.O. to accept the claim of Assessee as short term capital gain and long term capital gain instead of share trading business income?

B) Whether on the facts and in the circumstances of the case and in law, the ITAT was justified in upholding the claim of the Assessee that Assessee indulged in investment in shares without considering the facts and the investigation of the A.O. and the decision of the Hon’ble Supreme Court relied by the A.O. and the facts the Assessee himself has shown speculation loss Rs.13,483/- in share trading business?

2) The respondent is engaged in textile business. By an order dated 23/12/2008 passed under Section 143(3) of the Income Tax Act, 1961 the Assessing officer took a view that the respondent was not an investor in shares but dealer in shares and therefore, rejected the claim of the respondent for being taxed under the head capital gains in respect of the income earned from purchase and sale of shares. This was inter alia on the basis that the respondent had also returned speculation loss of Rs. 13,483/-. Consequently by the above assessment order the total income assessed was Rs.1.92 crores as against the returned income of Rs. 36,213/-.

3) On appeal, the CIT (Appeals) by an order dated 17/9/2009 allowed the appeal of the respondent holding that the respondent was an investor in shares and therefore, income earned on purchases and sale of shares is investment and the same would have to be assessed as his income under the head capital gains and not as income from the head Profits and Gains from the business or profession.

4) Being aggrieved, the revenue/appellant preferred an appeal to the Tribunal. On 10/11/2010 the Tribunal after examining the evidence upheld the order of CIT(A) and concluded that the respondent was an investor in shares and entitled to be taxed under the head capital gains in respect of purchase and sale of shares. The Tribunal after examining the facts found that the respondent had not borrowed any funds for its investments and that the long terms gains were attributable to only shares of 4 companies and 3 of them were held for a period of about 5 to 12 years. So far as short terms capital gains were concerned the Tribunal held that about 93% of the short terms gain/loss was attributable to shares of six companies and in any case all the shares were held for periods ranging in excess of 1 month. With regard to the fact that the respondent had returned speculation loss in his return, the Tribunal followed the decision of this Court in the matter of CIT V/s. Gopal Purohit reported in 228 CTR (Bom.) 582 to hold that there is no bar for an assessee to maintain two separate portfolios, one relating to investment in shares and another relating to business activities involving dealing in shares. Further this Court also held that the aforesaid finding is a pure finding of fact.

5) The appellate authorities have thus come to findings of fact after examining the relevant material. The same is not perverse.

6) On the above concurrent findings of fact by CIT (Appeals) and the Tribunal, no substantial question of law arises for consideration by this Court.

7) The appeal is therefore, dismissed. No order as to costs.

( M.S. SANKLECHA, J. ) ( S. J. VAZIFDAR, J.)

×

Similar Ripples

Questions

Investor's Dual Portfolio Strategy Upheld: Tax Treatment as Capital Gains Affirmed

Write your CommentSimilar Posts

Generic

- Reportdata/5756.pdf