"Court Upholds Mandatory Interest on Unpaid Advance Tax in Builder's Case"

Full News

"Court Upholds Mandatory Interest on Unpaid Advance Tax in Builder's Case"

"Court Upholds Mandatory Interest on Unpaid Advance Tax in Builder's Case"

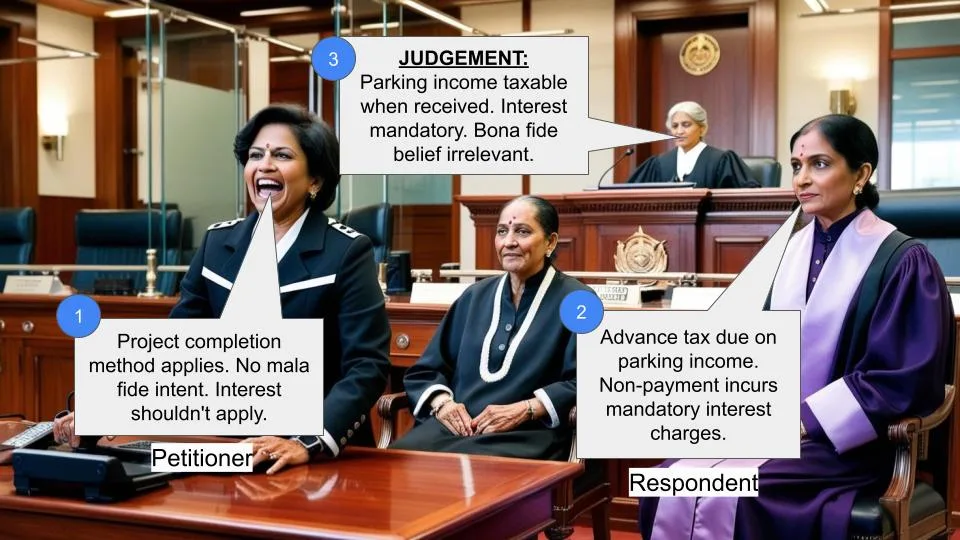

This case involves a builder who failed to pay advance tax on parking charges income, believing it should be taxed under the project completion method. The court ruled that the income was taxable in the year received and upheld the levy of mandatory interest for non-payment of advance tax.

Get the full picture - access the original judgement of the court order here.

Case Name:

Sudhir G. Borgaonkar Vs Assistant Commissioner of Income Tax (High Court of Bombay)

Income Tax Appeal No.332 of 2013

Key Takeaways:

1. Income from parking charges on vacant land is taxable in the year received, separate from project completion.

2. Non-payment of advance tax due to a mistaken belief doesn't exempt from interest charges.

3. Interest under Section 234B (of Income Tax Act, 1961) is mandatory and compensatory, regardless of the assessee's intentions.

Issue:

Was the Income Tax Appellate Tribunal (ITAT) justified in holding that the assessee was liable to pay interest under sections 234A (of Income Tax Act, 1961) and 234B (of Income Tax Act, 1961), even when the assessee had a bona fide belief that its income would be 'nil'?

Facts:

1. The appellant is a builder and developer following the project completion method for tax purposes.

2. During assessment for AY 2003-04, it was found that Rs.15.48 lakhs from parking charges was taxable in AY 2000-01.

3. The appellant hadn't filed a return for AY 2000-01, believing this income would be taxed upon project completion.

4. A notice under Section 148 (of Income Tax Act, 1961) was issued, and the income was assessed for AY 2000-01.

5. The Commissioner of Income Tax (Appeals) initially set aside the Assessing Officer's order, but the Tribunal reversed this decision.

6. The Assessing Officer then charged interest under Sections 234A (of Income Tax Act, 1961) and 234B (of Income Tax Act, 1961) for default in advance tax payment.

Arguments:

1. Appellant's Argument:

The appellant argued that interest shouldn't be charged under Section 234B (of Income Tax Act, 1961) without a finding of mala fide intent in non-payment of advance tax.

2. Revenue's Argument:

The Revenue contended that the appellant was obliged to pay advance tax on the parking charges income for AY 2000-01.

Key Legal Precedents:

1. CIT v/s. Anjum M. H. Ghaswala 252 ITR 1:

The Supreme Court held that levy of interest under Sections 234A (of Income Tax Act, 1961) and 234B (of Income Tax Act, 1961) is mandatory and compensatory in nature.

2. CIT v/s. Bokaro Steel Ltd. (1999) 236 ITR 315:

This case was cited but found inapplicable to the current situation.

3. Prime Securities Ltd. v/s. ACIT 333 ITR 464:

The court found this case misplaced in the current context.

Judgement:

The court dismissed the appeal, upholding the ITAT's decision that the assessee was liable to pay interest under Section 234B (of Income Tax Act, 1961). The court agreed that the appellant was obliged to pay advance tax on the parking charges income, and non-payment would carry the burden of interest under Section 234B (of Income Tax Act, 1961).

FAQs:

Q1: Does a bona fide belief of nil income exempt an assessee from paying interest on unpaid advance tax?

A1: No, the court ruled that even with a bona fide belief, the assessee is still liable for mandatory interest charges.

Q2: How did the court view the project completion method in this case?

A2: The court agreed with the Tribunal that parking charges income was separate from project completion and taxable in the year received.

Q3: What is the nature of interest under Section 234B (of Income Tax Act, 1961) according to this judgment?

A3: The court affirmed that interest under Section 234B (of Income Tax Act, 1961) is mandatory and compensatory, based on the Supreme Court's decision in Anjum Ghaswala.

Q4: Can an assessee avoid interest charges if they didn't file a return due to a mistaken belief?

A4: No, the judgment indicates that the obligation to pay advance tax exists regardless of whether a return was filed.

Q5: How does this judgment impact builders and developers?

A5: It clarifies that income from ancillary activities like parking charges should be taxed separately from project-related income, and advance tax should be paid accordingly.

1. This Appeal by the Revenue under Section 260 (of Income Tax Act, 1961)A of the Income Tax Act, 1961 (the Act), challenges the order dated 5th October, 2012 passed by the Income Tax Appellate Tribunal (the Tribunal) for the Assessment Year 200001.

2. The Appellant has formulated the following questions of law for our consideration:

“ Whether on the facts and in the circumstances of the case and on a proper interpretation of s. 234A and s.234B of the Act, the ITAT was justified in holding that the assessee was liable to pay interest under those sections; when admittedly the assessee had a bona fide belief and a strong arguable case that its income for the relevant A. Y. would be 'nil' and hence, no default in payment of advance tax had occurred?”.

3. The Appellant is engaged in business as builder and developer following the project completion method for purposes of paying its taxes. During the course of assessment proceedings for Assessment Year 2003-04, it was noticed that a miscellaneous income of Rs.1.32 Crores offered to tax in A. Y. 200304 was claimed to have been received during the Assessment Years 199596 to 2003-04. During the course of assessment proceedings for Assessment Year 2003-04, it was found that an amount of Rs.15.48 lakhs was income chargeable to tax in Assessment Year 2000-01 being income generated on account of parking charges collected on the vacant land available with the Appellant and had nothing to do with any of the projects being executed by the Appellant. As the Appellant had not filed his return of income for the Assessment Year 2000-01, a notice under Section 148 (of Income Tax Act, 1961) was issued. Consequent thereto, the income received from parking charges of Rs.15.48 lakhs was assessed to tax for the Assessment Year 2000-01.

4. On appeal by the Appellant Assessee, the Commissioner of Income Tax (Appeals) [CIT(A)] set aside the order of the Assessing Officer. This on the ground that the amount earned by exploiting vacant land is an amount rateable to the costs of the project and therefore, properly offered to tax in the Assessment Year 200304. This conclusion was reached on the basis of the decision of the Supreme Court in CIT v/s. Bokaro Steel Ltd. (1999) 236 ITR 315.

5. On further appeal by the Revenue, the Tribunal set aside the order of the CIT(A) holding that amount received on account of parking charges is not a part of any project and is business income and chargeable to tax for the Assessment Year 200001. It was also held that the decision of the Apex Court in Bokaro Steel Ltd. (supra) is inapplicable.

6. Thereafter while giving effect to the order of the Tribunal in quantum proceeding, the Assessing Officer charged interest under Section 234 (of Income Tax Act, 1961)A and 234B of the Act, inter alia in respect of default in payment of advance tax for the Assessment Year 200001. On appeal, the CIT(A) by order dated 22nd July, 2011 upheld charging of interest under Section 234A (of Income Tax Act, 1961) and 234B (of Income Tax Act, 1961) as charged by the Assessing Officer. On further appeal by the Assessee, the Tribunal by the impugned order dated 5th October, 2012 placed reliance upon the decision of the Supreme Court in CIT v/s. Anjum M. H. Ghaswala 252 ITR 1 wherein it is held that levy of interest under Sections 234 (of Income Tax Act, 1961)A and 234B are mandatory and compensatory in nature. Thus upholding the order of the Assessing Officer charging interest.

7. Mr. Naniwadekar, learned Counsel appearing for the Appellant at the very outset submits that the grievance is limited to charging of interest under Section 234B (of Income Tax Act, 1961). It is submitted that no question of charging interest for delayed payment of advance tax under Section 234B (of Income Tax Act, 1961) can arise in the absence of a finding that non- payment of advance tax was mala fide. In support, he places reliance upon the decision of this Court in the matter of Prime Securities Ltd. v/s. ACIT 333 ITR 464 and particularly emphasizes fact that the CIT(A) had in quantum proceedings accepted the contention of the Appellant.

8. As against the above, Mr. Malhotra learned Counsel appearing for the Respondent supports the impugned order of the Tribunal including its observations that the decision of the Apex Court in Bokaro Steel Ltd., (supra) is inapplicable.

9. In the present facts, the Appellant had not originally filed its return of income and, therefore, there was no occasion for him to make any advance payment. This nonfiling of return of income was on the basis of the Appellant's stand that in view of project completion method followed by him, the income earned on parking charges would have to be returned when the project was completed. This was not accepted as the amount received on account of parking charges was not a part of any project. Thus parking charges was brought to tax in Assessment Year 200001. On facts in quantum proceedings, it has been held by the Tribunal that the amount received on parking charges has nothing to do with the appellant's project and was assessable to tax in Assessment Year 200001. This has been accepted by the Appellant. If this be so, the Appellant was obliged to pay Advance tax and nonpayment of the same would carry with it the further burden on interest under Section 234B (of Income Tax Act, 1961). This is so in view of Anjum Ghaswala (supra) where it is held that payment of interest is mandatory and compensatory.

10. The reliance by the Appellant on the decision of this Court in Prime Securities (supra) is misplaced as it was not the case of the Revenue that the the assessee therein had committed any default in payment of advance tax at the time when the Advance tax was paid. The Court further held that at the time of making payment of Advance tax, it was not possible to anticipate events and make payment of advance tax on that basis. In the present case, it is the case of the Revenue that there is default on the part of the Appellant in paying Advance tax on account of parking charges received by it for Assessment Year 200001.

11 In view of the above and particularly, the decision of the Supreme Court in Anjum Ghaswala (supra), we see no substantial question of law arising to entertain this appeal.

12 Accordingly, appeal dismissed. No order as to costs.

(G.S.KULKARNI,J.) (M.S.SANKLECHA,J.)

×

Similar Ripples

Questions

"Court Upholds Mandatory Interest on Unpaid Advance Tax in Builder's Case"

Write your CommentSimilar Posts

Generic

- Reportdata/3995.pdf